A Third-Party Collector Validation Notice is a legal requirement under the FDCPA that allows consumers to dispute a debt. When a collection agency contacts you, they must provide written proof of the amount owed and the original creditor's identity. Understanding your rights helps prevent unfair collection practices. To simplify the process, below are some ready to use template.

Image cover: Mastering the Debt Validation Letter: Free Templates and Expert Samples

Letter Samples List

- Initial Third-Party Debt Validation Notice Letter

- Disputed Debt Verification Response Letter

- Original Creditor Information Notice Letter

- Itemized Account Balance Validation Letter

- Proof Of Debt Obligation Notice Letter

- Consumer Rights Disclosure Validation Letter

- Identity Theft Fraud Investigation Notice Letter

- Medical Account Collection Validation Letter

- Time-Barred Debt Collection Validation Letter

- Multiple Accounts Consolidation Validation Letter

- Post-Judgment Collection Validation Notice Letter

- Final Request Debt Verification Notice Letter

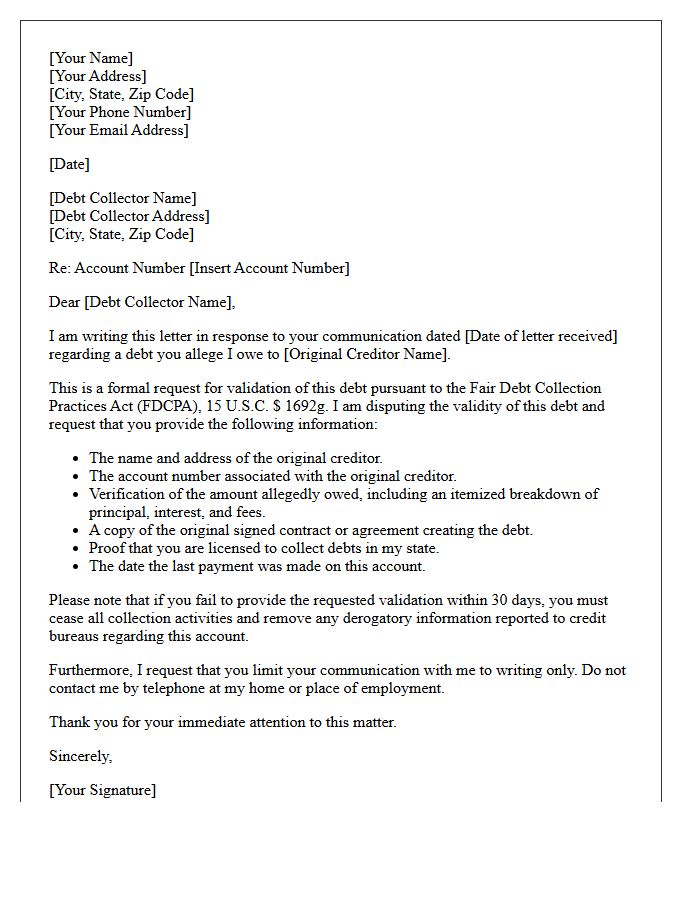

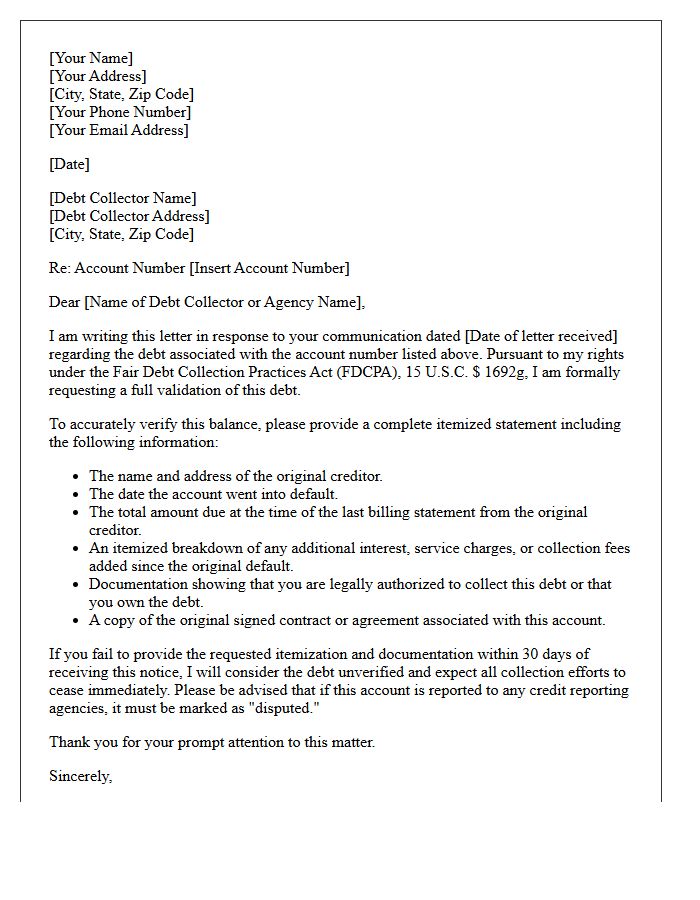

Initial Third-Party Debt Validation Notice Letter

Under the Fair Debt Collection Practices Act (FDCPA), debt collectors must send an Initial Third-Party Debt Validation Notice within five days of first contact. This critical document outlines your right to dispute the balance and request proof of the debt's legitimacy. Consumers have a thirty-day window to respond in writing to stop collection activities until the debt is verified. Failing to act can result in the debt being assumed valid, making this letter your primary defense against unauthorized collection attempts and errors.

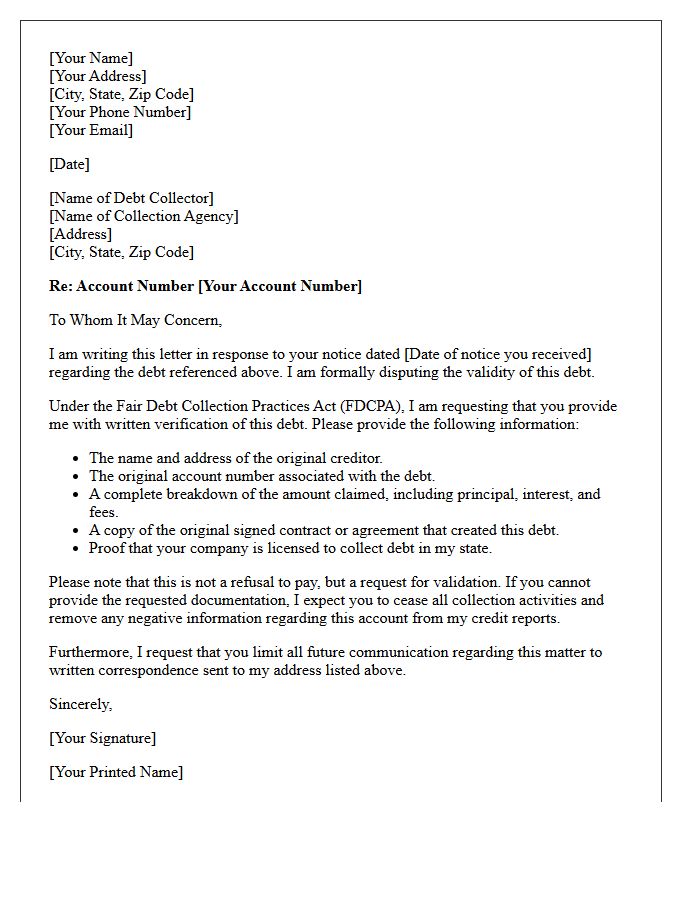

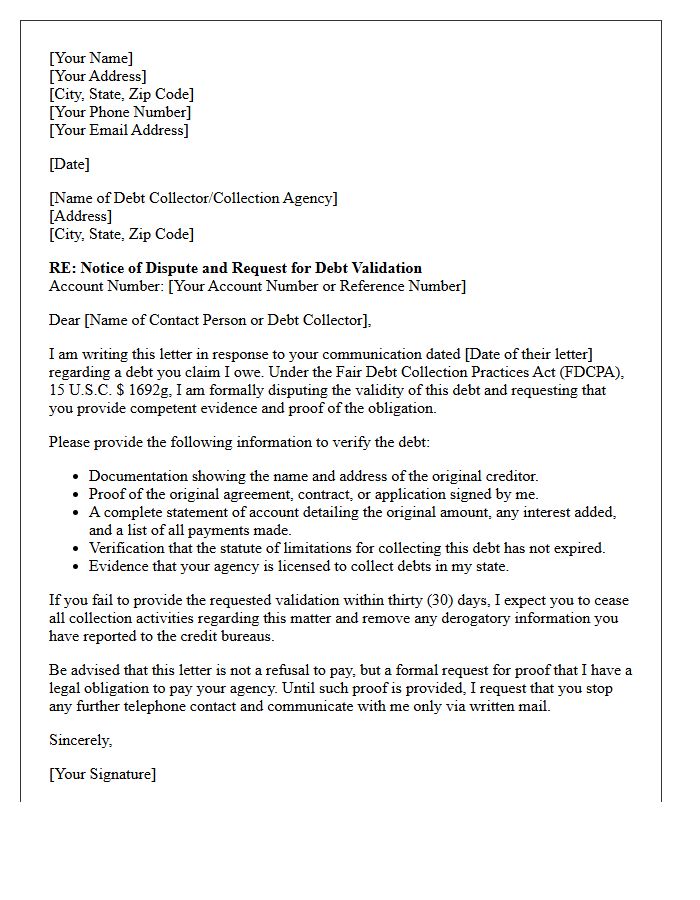

Disputed Debt Verification Response Letter

A Disputed Debt Verification Response Letter is a formal legal notice sent to collection agencies under the Fair Debt Collection Practices Act (FDCPA). This document demands verifiable proof that the alleged debt is valid, accurate, and legally enforceable. Upon receipt, collectors must cease all communication until they provide written evidence of the original contract and payment history. Sending this letter protects your consumer rights, prevents unauthorized reporting to credit bureaus, and ensures you are not held liable for fraudulent, expired, or incorrect financial claims.

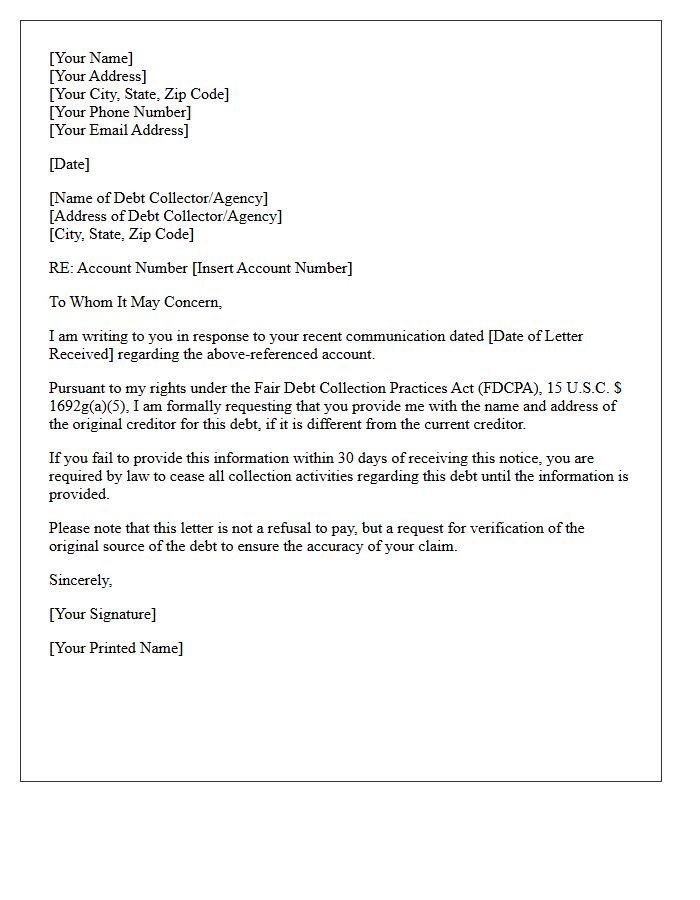

Original Creditor Information Notice Letter

An Original Creditor Information Notice Letter is a formal legal notification sent to consumers when a debt is sold or transferred. This document serves as official verification of the debt's origin, identifying the company that first extended the credit. Understanding this letter is essential for debt validation and ensuring the collector's legal standing. Under consumer protection laws, receiving this notice allows you to confirm the accuracy of the balance and verify the identity of the current owner before making payments, protecting you from potential scams or duplicate billing errors.

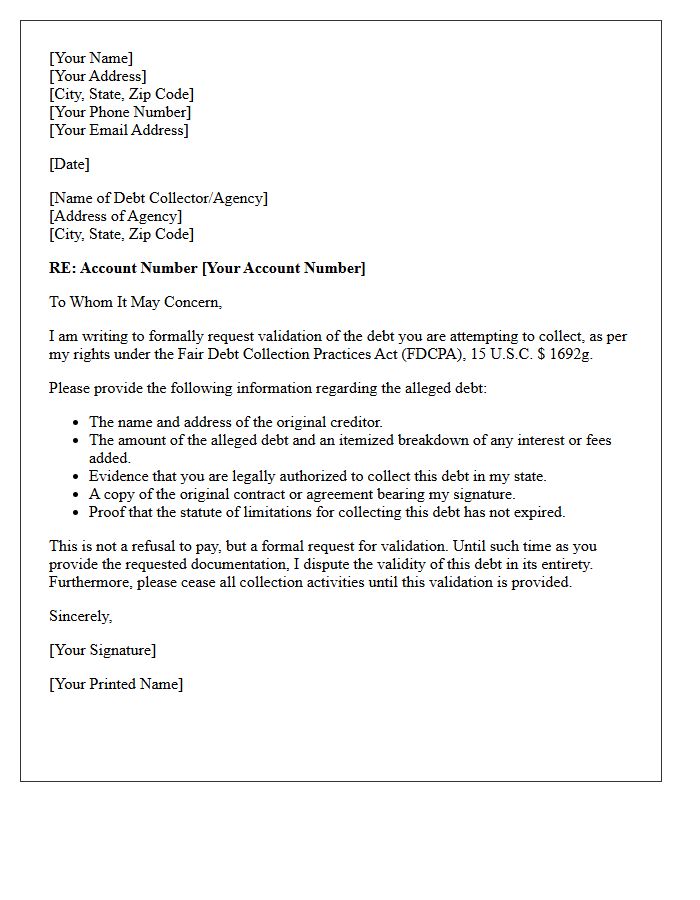

Itemized Account Balance Validation Letter

An Itemized Account Balance Validation Letter is a formal request sent to debt collectors to verify the legitimacy and accuracy of a debt. It requires the collector to provide a detailed breakdown of the total amount, including original principal, interest, and fees. Under the Fair Debt Collection Practices Act (FDCPA), this document protects consumers from unauthorized charges or mistaken identities. Requesting this validation ensures you are not paying expired or fraudulent claims, making it a critical tool for debt verification and maintaining a healthy credit report.

Proof Of Debt Obligation Notice Letter

A Proof of Debt Obligation Notice Letter is a formal legal document used by creditors to officially assert a financial claim against a debtor, typically during insolvency or bankruptcy proceedings. It serves as verified evidence of the amount owed, including interest and penalties. Providing accurate documentation is essential to ensure a claim is recognized for repayment priority. This notice ensures transparency and protects the creditor's rights during the debt recovery process, establishing a clear record of the obligation within the legal framework of asset liquidation or restructuring.

Consumer Rights Disclosure Validation Letter

A Consumer Rights Disclosure Validation Letter is a critical legal tool used to verify debt authenticity. Under the Fair Debt Collection Practices Act (FDCPA), you have the right to request written proof of a debt's validity within thirty days of initial contact. This letter forces collectors to provide the original creditor's name and the exact amount owed. Sending this document protects you against identity theft and inaccurate reporting, ensuring you are not pressured into paying unverified claims while maintaining your financial integrity and legal protections.

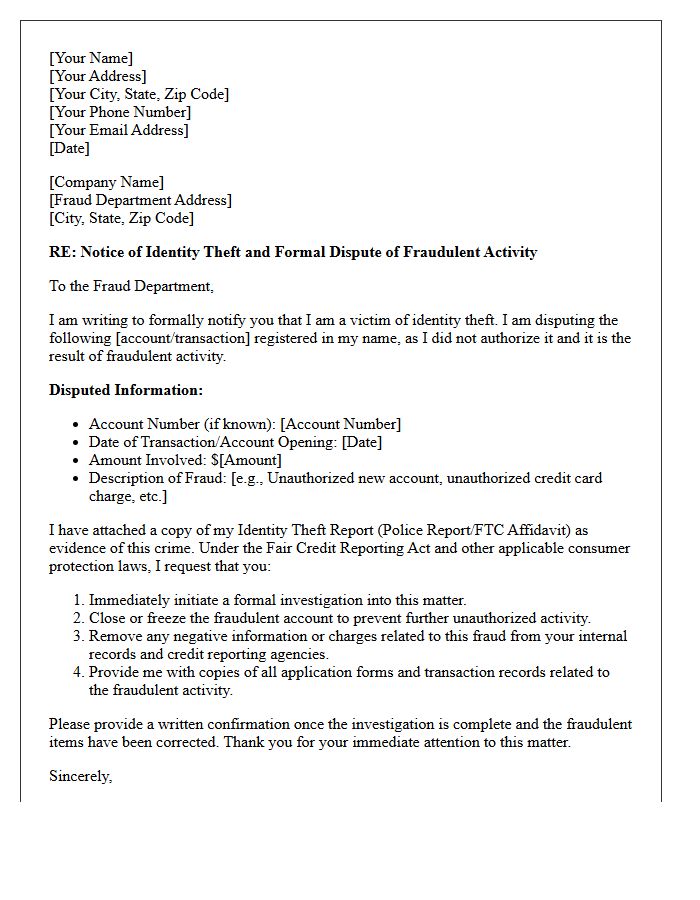

Identity Theft Fraud Investigation Notice Letter

An Identity Theft Fraud Investigation Notice Letter is a critical document sent to creditors or credit bureaus to formally dispute unauthorized transactions. This notice initiates a mandatory legal inquiry into suspicious activity under the Fair Credit Reporting Act. It should include your identity theft report and specific details of the fraudulent accounts. Providing this written notification protects your consumer rights, halts collection efforts, and is a vital step toward restoring your credit reputation. Always send it via certified mail to maintain a verifiable paper trail for your records.

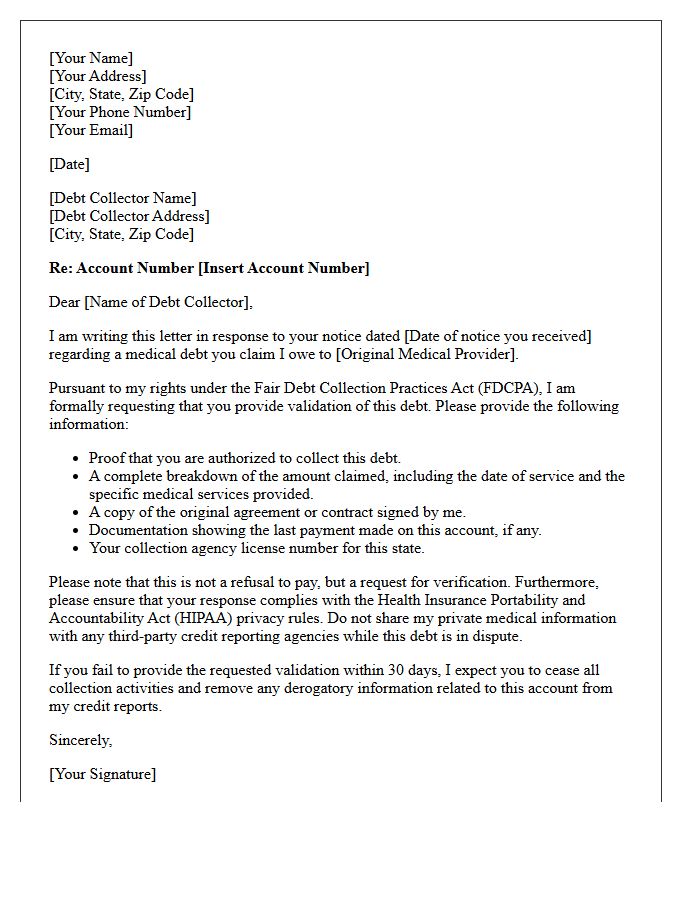

Medical Account Collection Validation Letter

A medical account collection validation letter is a formal request sent to debt collectors to verify the legal validity of an alleged medical debt. Under the Fair Debt Collection Practices Act (FDCPA), you have thirty days to request this verification in writing. This process ensures the debt amount is accurate and confirms the collector has the legal right to pursue payment. It also protects your rights under HIPAA, as collectors must provide proof without violating your medical privacy. Always keep copies of your correspondence to maintain a clear paper trail for legal protection.

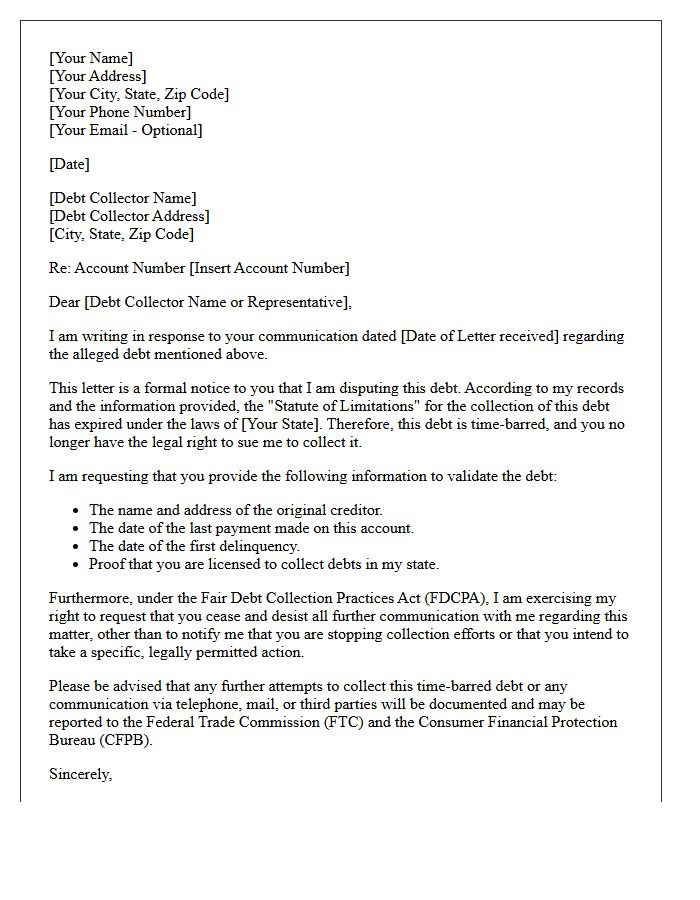

Time-Barred Debt Collection Validation Letter

A Time-Barred Debt Collection Validation Letter is a critical legal tool used to dispute old debts that have surpassed the statute of limitations. Sending this formal notice informs collectors that they no longer have the legal right to sue for payment. It is essential to demand debt validation without making any partial payments or acknowledging ownership, as doing so can inadvertently restart the clock on expired debt. Always keep copies of your correspondence to protect your consumer rights under the Fair Debt Collection Practices Act (FDCPA).

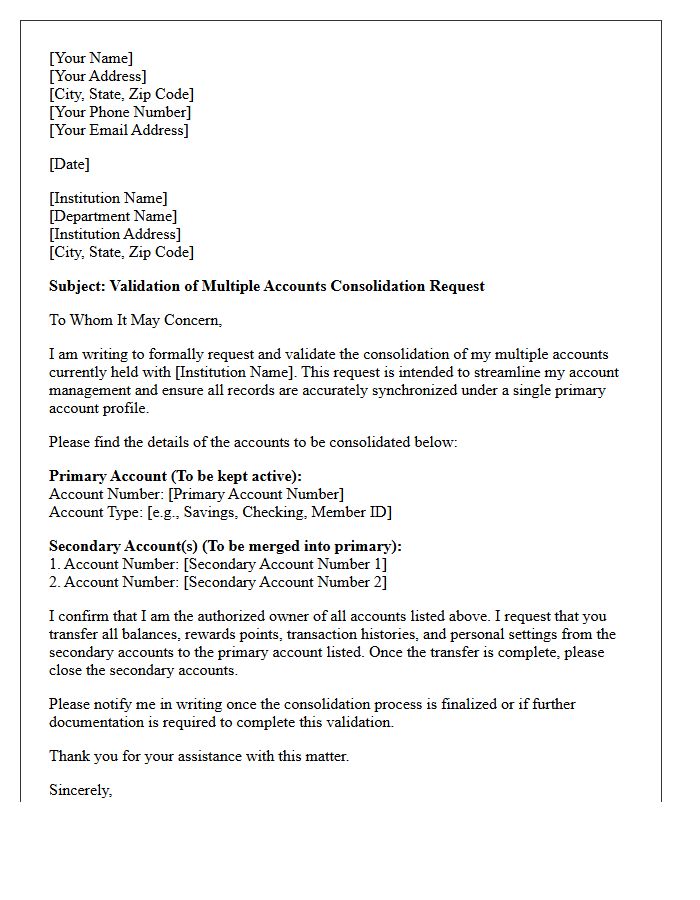

Multiple Accounts Consolidation Validation Letter

A Multiple Accounts Consolidation Validation Letter is a critical document sent by debt collectors to confirm the merging of several debts into a single file. This notice ensures debt accuracy by listing each original account, the respective balances, and the total consolidated amount owed. It serves as your legal opportunity to dispute discrepancies or verify the collector's right to pursue the combined sum. Reviewing this letter promptly is essential for maintaining clear credit records and preventing potential overcharges during the repayment process.

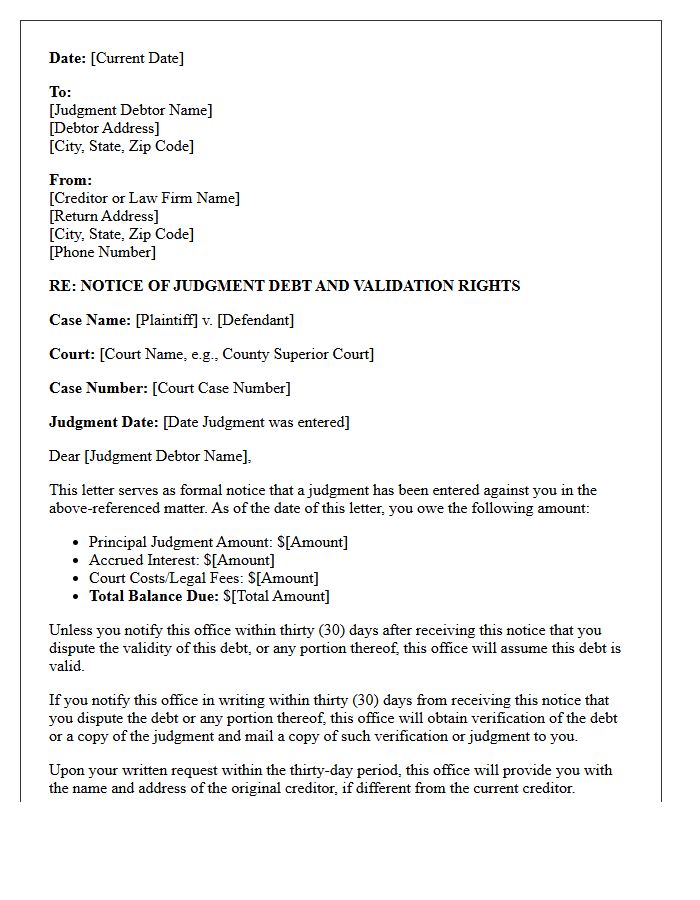

Post-Judgment Collection Validation Notice Letter

A Post-Judgment Collection Validation Notice Letter is a critical legal document sent after a court ruling. It confirms the judgment debt amount and informs the debtor of their legal rights to dispute the balance. This notice is essential for maintaining compliance with the Fair Debt Collection Practices Act (FDCPA). It provides a formal 30-day window for the consumer to request verification of the debt. Understanding this letter is vital for both creditors seeking enforcement and debtors needing to ensure the recorded judgment details are accurate before further collection actions proceed.

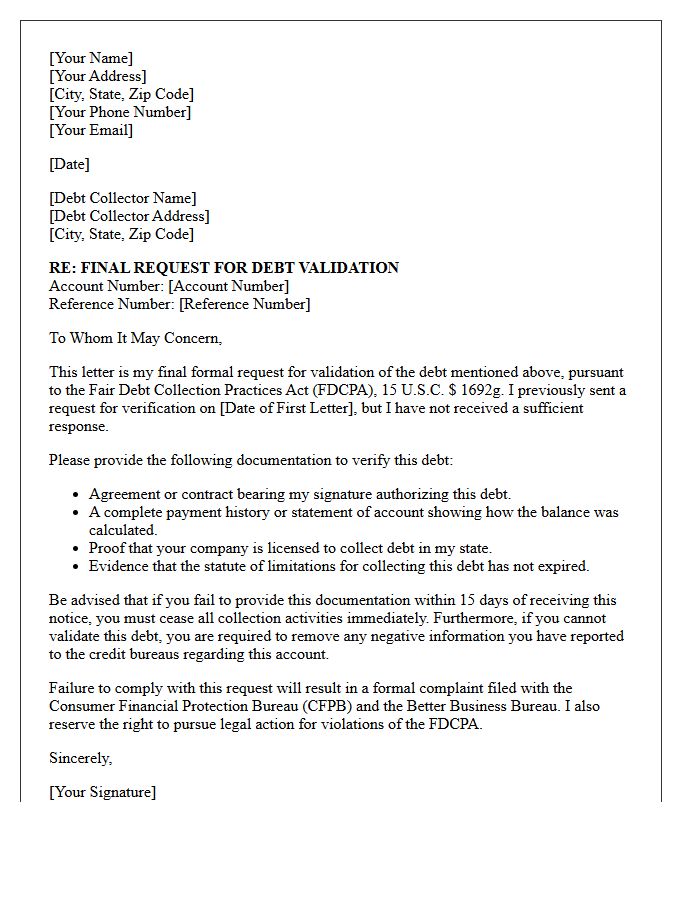

Final Request Debt Verification Notice Letter

A Debt Verification Notice Letter is your final legal opportunity to dispute an unverified claim. Upon receiving this notice, you have thirty days to exercise your rights under the Fair Debt Collection Practices Act (FDCPA). Sending a formal response forces the collector to provide written proof of the debt's validity and their legal authority to collect it. Failure to act within this window can lead to automatic verification, damaging your credit score and potentially resulting in legal judgments or wage garnishment. Always keep copies of all correspondence for your records.

What is a Third-Party Collector Validation Notice?

A Third-Party Collector Validation Notice is a legally required written statement sent by a debt collection agency to a consumer. It must be sent within five days of the initial contact and contains essential details regarding the debt, including the amount owed, the name of the creditor, and the consumer's rights to dispute the claim.

What information must be included in a debt validation notice?

Under the Fair Debt Collection Practices Act (FDCPA), the notice must include the total amount of the debt, the name of the current creditor, and a statement notifying the consumer they have 30 days to dispute the debt in writing. It must also explain that the collector will provide verification of the debt if requested within that timeframe.

How long do I have to respond to a validation notice?

Consumers have exactly 30 days from the date they receive the validation notice to dispute the debt or request original creditor information. If a written dispute is submitted within this "validation period," the third-party collector must cease all collection activities until they provide the requested verification.

Is a validation notice the same as a verification of debt?

No. A validation notice is the initial document sent by the collector to inform you of your rights and the debt details. A debt verification is the evidence or documentation provided by the collector after a consumer has formally disputed the debt or requested proof that the claim is legitimate.

What should I do if I receive a validation notice for a debt I don't owe?

If you receive a notice for an incorrect debt, you should send a formal debt dispute letter to the third-party collector within 30 days. Clearly state that you are disputing the debt and request full verification. This action prevents the debt from being automatically assumed valid and protects your rights under federal law.

Comments