A Conditional Policy Reinstatement Agreement outlines the specific requirements a policyholder must meet to restore lapsed insurance coverage. It typically involves proof of insurability and payment of overdue premiums to reactivate protection. Understanding these legal terms ensures continuous financial security and clarity on insurer obligations. To help you draft your own documentation, below are some ready to use template.

Image cover: Conditional Policy Reinstatement: Official Agreement Templates and Essential Samples

Letter Samples List

- Conditional Policy Reinstatement Offer Letter

- Pending Payment Conditional Policy Reinstatement Letter

- Statement Of Good Health Conditional Reinstatement Letter

- Vehicle Inspection Conditional Policy Reinstatement Letter

- Commercial Liability Conditional Reinstatement Agreement Letter

- Life Insurance Conditional Policy Reinstatement Letter

- Property Inspection Conditional Reinstatement Agreement Letter

- Notice Of Lapsed Policy And Conditional Reinstatement Letter

- Signed Conditional Reinstatement Agreement Acknowledgment Letter

- Conditional Policy Reinstatement Agreement Approval Letter

- Conditional Policy Reinstatement Agreement Denial Letter

- Grace Period Extension Conditional Reinstatement Letter

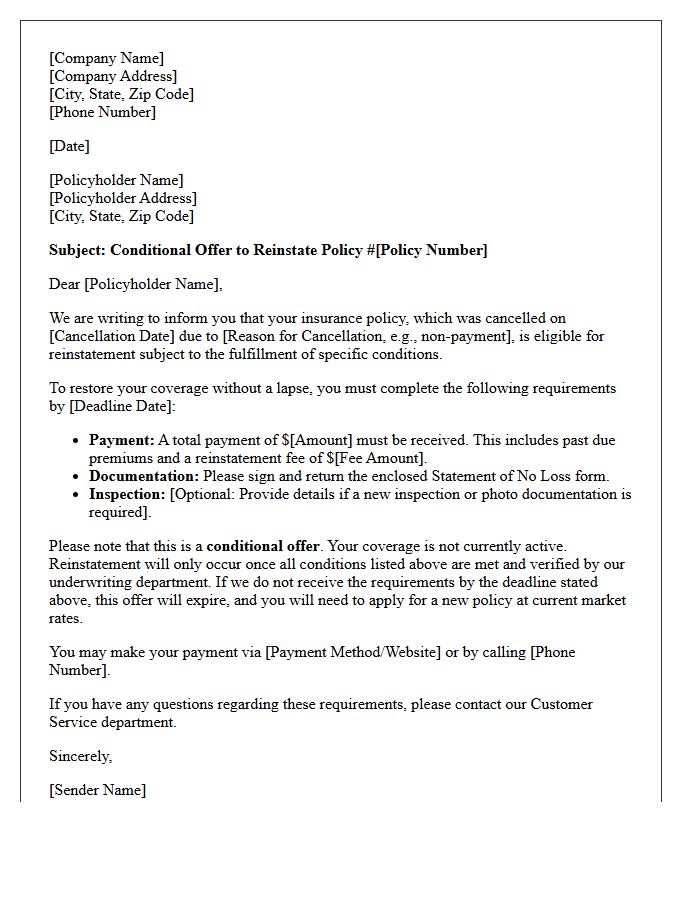

Conditional Policy Reinstatement Offer Letter

A Conditional Policy Reinstatement Offer Letter is a formal notice from an insurer allowing a policyholder to restore lapsed coverage. The most critical requirement is that the payment must be honored by the bank to take effect. Receiving the letter does not guarantee immediate protection; coverage remains suspended until all specified underwriting conditions are met and the premium is processed. Failure to comply with the deadline or terms outlined in the document will result in the permanent termination of the insurance policy without further notice.

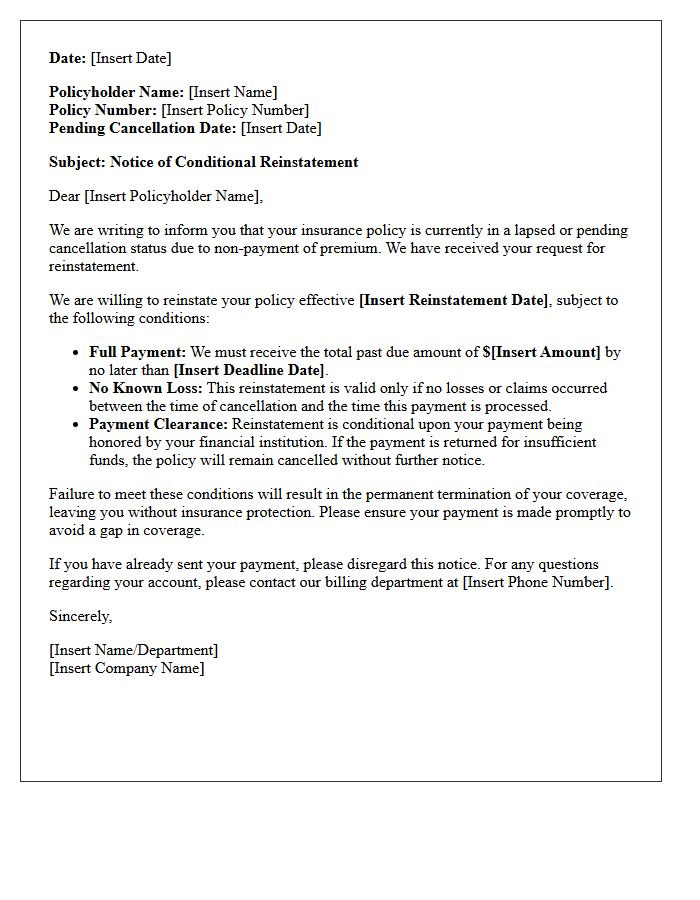

Pending Payment Conditional Policy Reinstatement Letter

A Pending Payment Conditional Policy Reinstatement Letter is a formal notice sent to policyholders after a lapse in coverage due to non-payment. It outlines the specific conditions required to restore insurance, such as paying all outstanding premiums and submitting a statement of no losses. Reinstatement is not guaranteed until the insurer accepts the payment and approves the application. Acting quickly is essential to avoid a permanent termination of benefits and to ensure continuous protection against potential liabilities or property losses during the gap period.

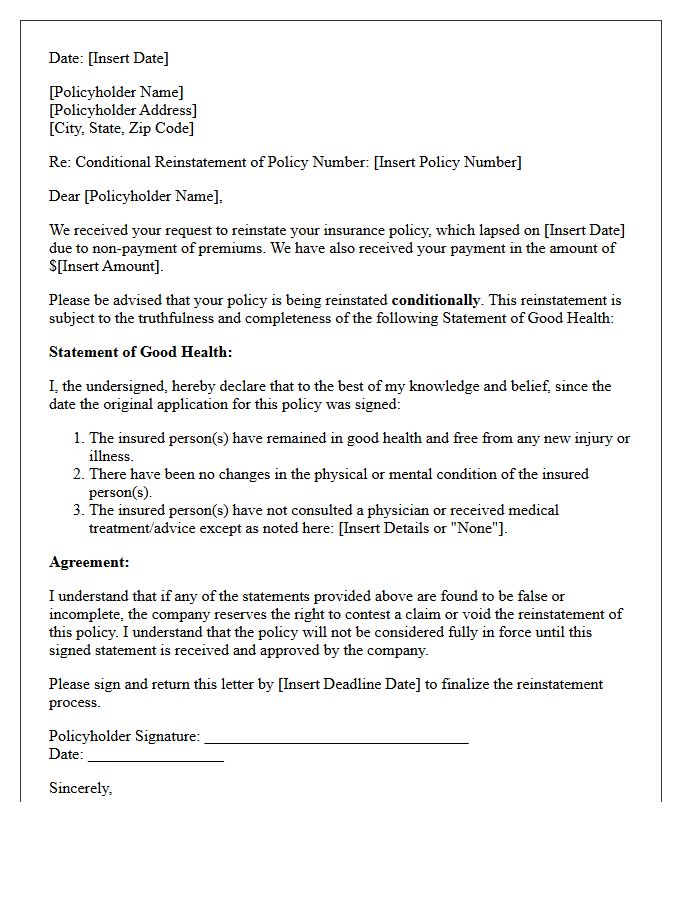

Statement Of Good Health Conditional Reinstatement Letter

A Statement of Good Health is a mandatory document required for the conditional reinstatement of a lapsed insurance policy. It serves as a formal declaration that the insured's medical condition has not declined since the original coverage ended. Insurers use this letter to reassess risk before restoring protection. To ensure approval, policyholders must provide accurate health details and pay outstanding premiums. Failure to disclose new pre-existing conditions can lead to claim denials or policy cancellation, making honest disclosure vital for successfully reactivating your life or health insurance coverage.

Vehicle Inspection Conditional Policy Reinstatement Letter

A Vehicle Inspection Conditional Policy Reinstatement Letter is a formal notice from an insurer allowing a lapsed policy to be reactivated. The reinstatement is strictly contingent upon providing proof of the vehicle's current condition. Owners must undergo a professional inspection to verify that no pre-existing damage occurred during the coverage gap. Failure to submit this documentation within the specified timeframe will result in permanent cancellation. This process ensures the insurance company mitigates risk while offering policyholders a final opportunity to restore their essential automotive protection and legal compliance.

Commercial Liability Conditional Reinstatement Agreement Letter

A Commercial Liability Conditional Reinstatement Agreement Letter is a legal document used to restore lapsed insurance coverage. This agreement specifies the conditions an insured party must meet, such as paying overdue premiums and certifying that no losses occurred during the gap period. It acts as a formal bridge to restart protection while protecting the insurer from pre-existing claims. Understanding these terms is crucial to ensuring your business regains active policy status without permanent loss of liability protection or legal vulnerabilities.

Life Insurance Conditional Policy Reinstatement Letter

A Life Insurance Conditional Policy Reinstatement Letter is a formal notification sent after a coverage lapse. It outlines the specific requirements needed to restore your benefits. Receiving this conditional approval means your policy is not yet active; you must typically provide a statement of health and pay all outstanding premiums. The insurer evaluates your current insurability before fully reinstating the contract. It is crucial to respond immediately, as these offers have strict deadlines. Failure to meet every condition will result in a permanent loss of protection and death benefit eligibility.

Property Inspection Conditional Reinstatement Agreement Letter

A Property Inspection Conditional Reinstatement Agreement Letter is a formal document used by lenders to restore a delinquent mortgage. It outlines specific requirements, such as completing necessary repairs or passing a property inspection, to ensure the home's value is maintained. By signing, the borrower agrees to resolve physical or financial defaults within a set timeframe. This agreement is crucial for foreclosure prevention, as successful compliance leads to the reinstatement of the loan terms, allowing the homeowner to regain good standing with the financial institution.

Notice Of Lapsed Policy And Conditional Reinstatement Letter

A Notice of Lapsed Policy and Conditional Reinstatement Letter informs you that your insurance coverage has ended due to unpaid premiums. This critical document offers a limited window to restore your benefits. To reactivate the policy, you must typically pay all overdue amounts and meet specific underwriting requirements, such as a statement of good health. Reinstatement is not automatic; the insurer must approve your application. Acting quickly is essential to avoid a permanent loss of protection and the potential for higher rates when seeking a new policy elsewhere.

Signed Conditional Reinstatement Agreement Acknowledgment Letter

A Signed Conditional Reinstatement Agreement Acknowledgment Letter is a formal document confirming that a lapsed policy or contract is being restored under specific requirements. It serves as legal proof that the policyholder understands the mandatory conditions, such as paying overdue premiums or passing health screenings, necessary to maintain coverage. This letter protects both parties by outlining the exact compliance terms required to avoid future termination. Promptly returning this signed acknowledgment ensures that your reinstatement process remains valid and that your protective benefits are fully secured without further interruption.

Conditional Policy Reinstatement Agreement Approval Letter

A Conditional Policy Reinstatement Agreement Approval Letter confirms that an insurer is willing to restore a lapsed policy, provided specific contingencies are met. It is not an immediate guarantee of coverage. Policyholders must typically pay outstanding premiums and provide updated evidence of insurability within a strict timeframe. Until the company formally verifies these requirements and sends a final confirmation, the policy remains inactive. Carefully reviewing the deadlines and conditions listed in this letter is essential to prevent a permanent loss of protection and maintain financial security.

Conditional Policy Reinstatement Agreement Denial Letter

A Conditional Policy Reinstatement Agreement Denial Letter notifies a policyholder that their request to restore a lapsed insurance policy has been rejected. This formal notice typically outlines specific reasons for the denial, such as missed deadlines, insufficient payment, or failing to meet updated underwriting requirements. Receiving this letter means the previous coverage remains inactive, leaving the individual or asset unprotected. It is crucial to review the rejection grounds immediately to determine if an appeal is possible or if seeking a new insurance provider is necessary to maintain continuous protection.

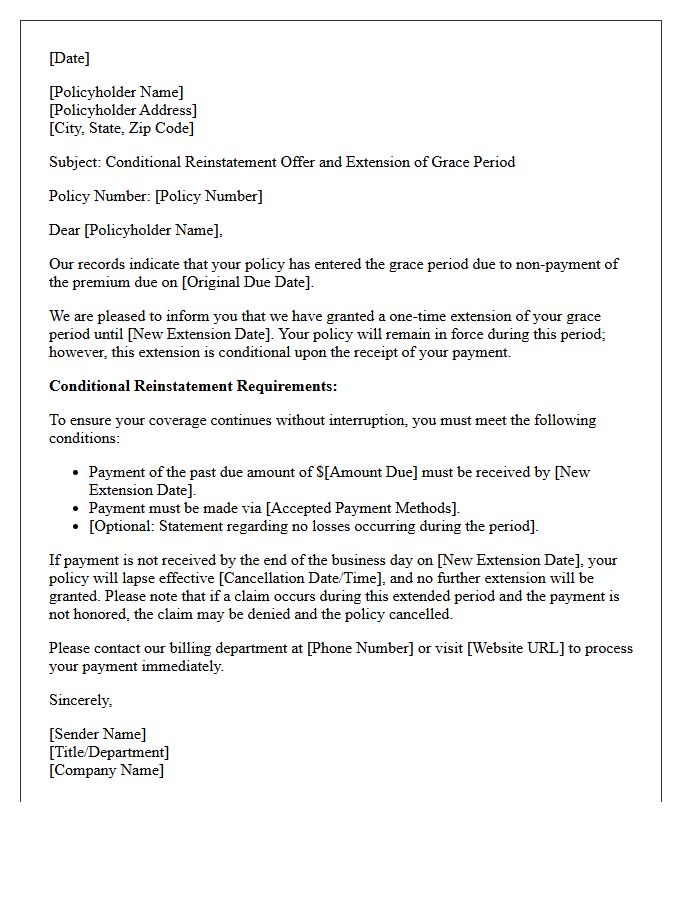

Grace Period Extension Conditional Reinstatement Letter

A Grace Period Extension Conditional Reinstatement Letter is a formal notice allowing policyholders to restore lapsed insurance coverage under specific terms. It typically requires the immediate payment of overdue premiums and a signed Statement of Good Health to confirm no losses occurred during the gap. This document acts as a temporary extension, offering a final opportunity to maintain protection without a full reapplication. Understanding these eligibility requirements is crucial, as failure to comply within the specified deadline results in permanent policy termination and a total loss of benefits.

What is a Conditional Policy Reinstatement Agreement?

A Conditional Policy Reinstatement Agreement is a legal document issued by an insurance company that outlines the specific requirements a policyholder must meet to restore a lapsed or cancelled policy to active status. Coverage is not fully restored until all conditions, such as premium payments and proof of insurability, are satisfied and approved by the insurer.

What are the common requirements for a policy reinstatement to be approved?

Most agreements require the policyholder to pay all past-due premiums plus interest, submit a formal reinstatement application, and provide evidence of continued insurability. This evidence may include a new medical exam or a "statement of good health" to ensure the risk profile has not significantly changed since the policy lapsed.

Does a Conditional Policy Reinstatement Agreement provide immediate coverage?

No, the agreement does not provide immediate or "interim" coverage. Protection is "conditional," meaning the insurer is not liable for claims occurring between the lapse date and the official reinstatement date. Coverage only resumes once the insurance company confirms in writing that all conditions have been met and the policy is officially back in force.

Is there a time limit for requesting a reinstatement after a policy lapse?

Yes, most insurance contracts include a reinstatement period, typically ranging from two to five years from the date of the premium default. If a policyholder fails to initiate the Conditional Policy Reinstatement Agreement within this window, the policy is permanently terminated, and a new policy must be purchased at current market rates.

What happens if a claim occurs while the reinstatement is still "conditional"?

If a loss occurs after the agreement is signed but before the insurer has officially approved the reinstatement, the claim will likely be denied. Because the agreement is conditional, the policy is not considered active until the underwriting process is complete and the company has formally accepted the risk.

Comments