Understanding a Life Insurance Age-Banded Rate Increase is essential for policyholders facing rising premiums. These adjustments occur during renewal as you move into older age brackets with higher mortality risks. Managing these cost shifts ensures your coverage remains affordable while maintaining necessary financial protection. To help you communicate these changes effectively, below are some ready to use template.

Image cover: Managing Life Insurance Age-Banded Rate Hikes: Renewal Templates and Sample Notices

Letter Samples List

- Upcoming Age-Banded Rate Increase Renewal Letter

- Understanding Your Life Insurance Premium Increase Letter

- Annual Policy Review And Age-Bracket Adjustment Letter

- Life Insurance Coverage Options And Renewal Letter

- Term Life Conversion Opportunity And Renewal Letter

- Strategies To Manage Your Age-Banded Rate Increase Letter

- Client Appreciation And Renewal Premium Update Letter

- Emphasizing Your Life Insurance Value Renewal Letter

- Policy Renewal And Beneficiary Information Update Letter

- Final Notice Of Age-Banded Renewal Rate Letter

- Dependent Coverage Age-Banded Rate Increase Letter

- Policy Illustration And Age-Banded Renewal Letter

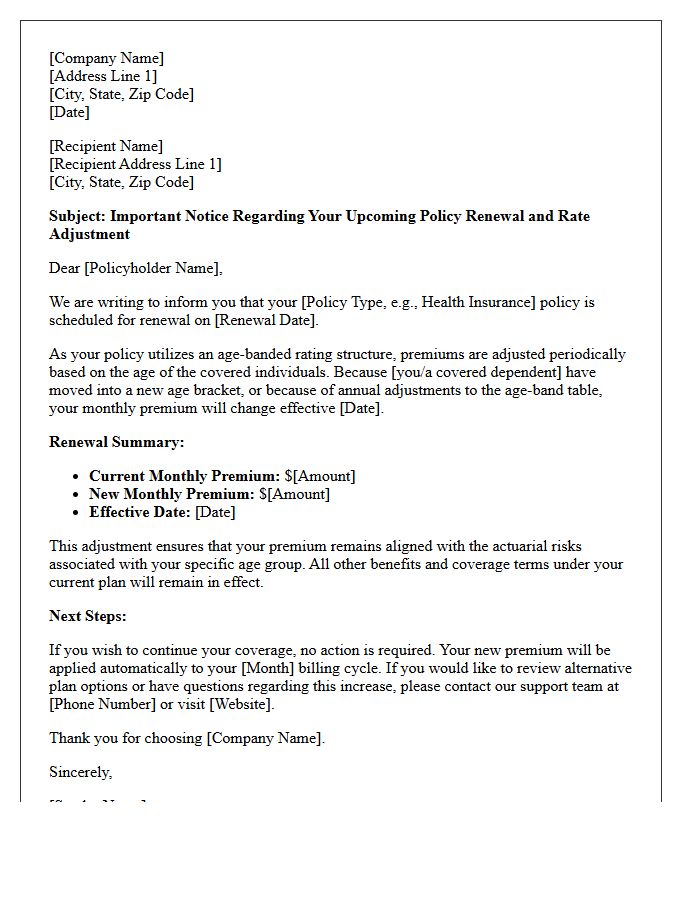

Upcoming Age-Banded Rate Increase Renewal Letter

Your Age-Banded Rate Increase renewal letter indicates a premium adjustment based on your birthday moving you into a new insurance bracket. This standard re-rating process occurs because health risks statistically increase with age. It is essential to review your Renewal Notice early to compare updated monthly costs against your current budget. If the new premium is too high, you may explore alternative plans or subsidies during the open enrollment period to ensure continuous, affordable coverage. Always verify the effective date to avoid unexpected billing changes.

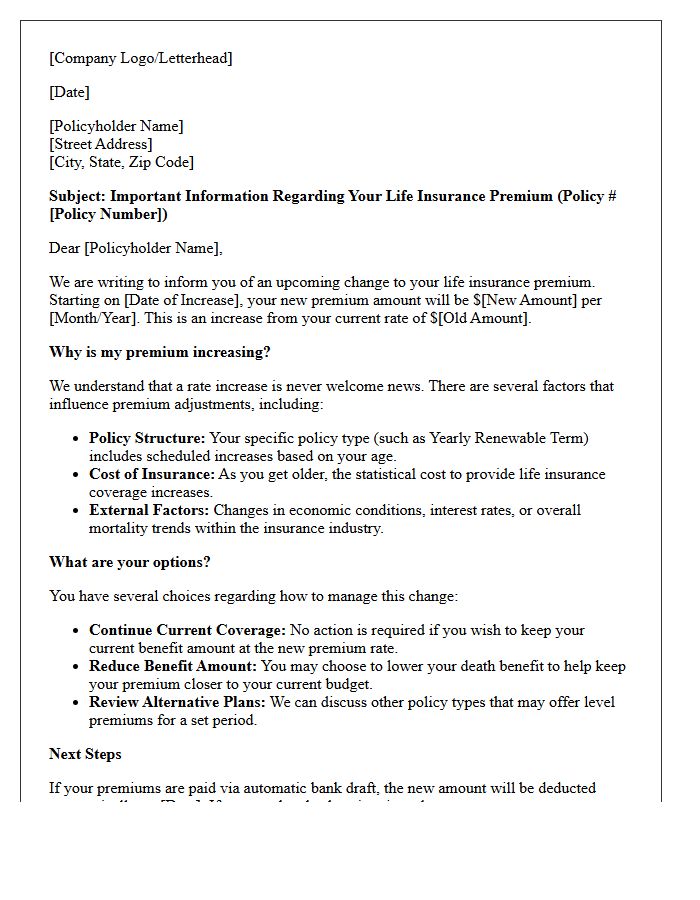

Understanding Your Life Insurance Premium Increase Letter

Receiving a life insurance premium increase letter usually signals the end of a level-premium period. Most term life insurance policies feature fixed rates that jump significantly once the initial term expires. This occurs because your age and health risks increase over time. Review your letter to identify the new payment schedule and the renewal date. To avoid high costs, compare new quotes or consider re-underwriting for a different policy. Understanding these adjustments helps you maintain essential coverage without overpaying for your financial protection.

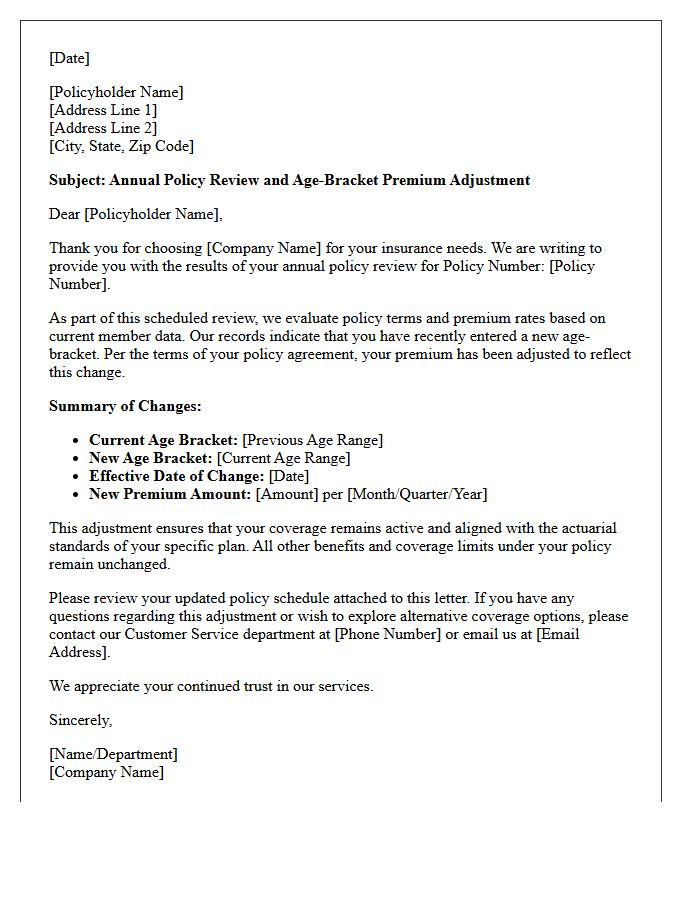

Annual Policy Review And Age-Bracket Adjustment Letter

An Annual Policy Review and Age-Bracket Adjustment Letter is a critical notification from your insurer regarding coverage updates. It informs policyholders about premium increases that occur as they enter a new age category. Reviewing this document ensures your life or health insurance remains aligned with current financial goals. It provides an essential opportunity to evaluate coverage adequacy, update beneficiary designations, and compare market rates. Ignoring these adjustments may lead to unexpected costs or lapses in protection as your insurance needs and risk profile evolve over time.

Life Insurance Coverage Options And Renewal Letter

Understanding your life insurance coverage options is vital when you receive a renewal letter. This document typically outlines upcoming premium increases and policy adjustments. You can choose to maintain current benefits, reduce coverage to lower costs, or convert term policies into permanent protection. Reviewing these terms ensures your beneficiaries remain financially secure. Always compare the renewal rates against new market quotes to guarantee the best value. Timely action is necessary to avoid a lapse in protection, ensuring your financial legacy stays intact as your personal needs evolve over time.

Term Life Conversion Opportunity And Renewal Letter

A Term Life Conversion Opportunity allows policyholders to transition temporary coverage into a permanent policy without a new medical exam. This is crucial if your health has declined. The Renewal Letter typically arrives as your initial term expires, outlining significantly higher premium costs for extending the current policy. Reviewing these documents promptly is essential to avoid a lapse in protection or excessive costs. Act before the conversion deadline specified in your letter to secure lifelong coverage and lock in level premiums based on your current age.

Strategies To Manage Your Age-Banded Rate Increase Letter

When you receive an age-banded rate increase letter, the most important step is to compare alternative plans immediately to offset rising costs. Review your current coverage needs and consider health savings accounts or higher deductibles to lower monthly premiums. Since these adjustments typically occur annually based on your age bracket, proactive market research ensures you remain on the most cost-effective tier. Don't simply accept the new rate; evaluate network changes and subsidy eligibility to manage your healthcare budget effectively while maintaining essential benefits and quality care.

Client Appreciation And Renewal Premium Update Letter

A client appreciation and renewal premium update letter is a critical communication tool for maintaining customer retention. It expresses gratitude for their continued loyalty while clearly explaining upcoming policy adjustments or rate changes. To remain effective, the message must highlight the value provided and justify the premium update through improved services or market shifts. Providing transparent details ensures trust and encourages timely renewals. Always include a clear call to action, inviting clients to discuss their coverage options to ensure their evolving needs are met before the next billing cycle begins.

Emphasizing Your Life Insurance Value Renewal Letter

Your Life Insurance Value Renewal Letter is a critical document that outlines upcoming changes to your policy. It primarily details premium adjustments and updated coverage benefits, ensuring your financial protection remains intact. Reviewing this notice allows you to assess if your current plan still aligns with your long-term goals. Pay close attention to the renewal date to avoid any unintended lapses in coverage. Understanding these updates empowers you to make informed decisions about your future security and potential policy enhancements during the transition period.

Policy Renewal And Beneficiary Information Update Letter

A policy renewal letter confirms your ongoing coverage while highlighting essential updates to premiums and benefit terms. It is the critical period to ensure your protection remains active and aligned with current financial goals. Simultaneously, you must review and update beneficiary information to guarantee that death benefits are distributed according to your latest wishes. Neglecting these changes can lead to legal complications or unintended asset distribution. Always verify contact details and beneficiary designations during each renewal cycle to maintain comprehensive security for your loved ones.

Final Notice Of Age-Banded Renewal Rate Letter

A Final Notice of Age-Banded Renewal Rate is a critical document indicating that your insurance premiums will increase because you have entered a new age bracket. Unlike flat-rate plans, these costs escalate at specific milestones defined by the insurer. It is vital to review your coverage immediately to ensure the policy remains affordable. Since this is a final notice, failure to respond or pay the updated amount may lead to a lapse in coverage. Always compare these new rates against alternative market options to maintain cost-effective protection as you age.

Dependent Coverage Age-Banded Rate Increase Letter

A Dependent Coverage Age-Banded Rate Increase Letter notifies policyholders of premium adjustments driven by a dependent's aging into a higher bracket. Unlike flat rates, age-banded pricing calculates costs based on specific age tiers. When a child or young adult reaches a new threshold, their individual risk profile changes, triggering an automatic price rise. It is essential to review these notices to understand updated monthly obligations and ensure the benefit elections remain cost-effective for your family's budget. Always verify the effective date to avoid unexpected billing discrepancies in your healthcare coverage.

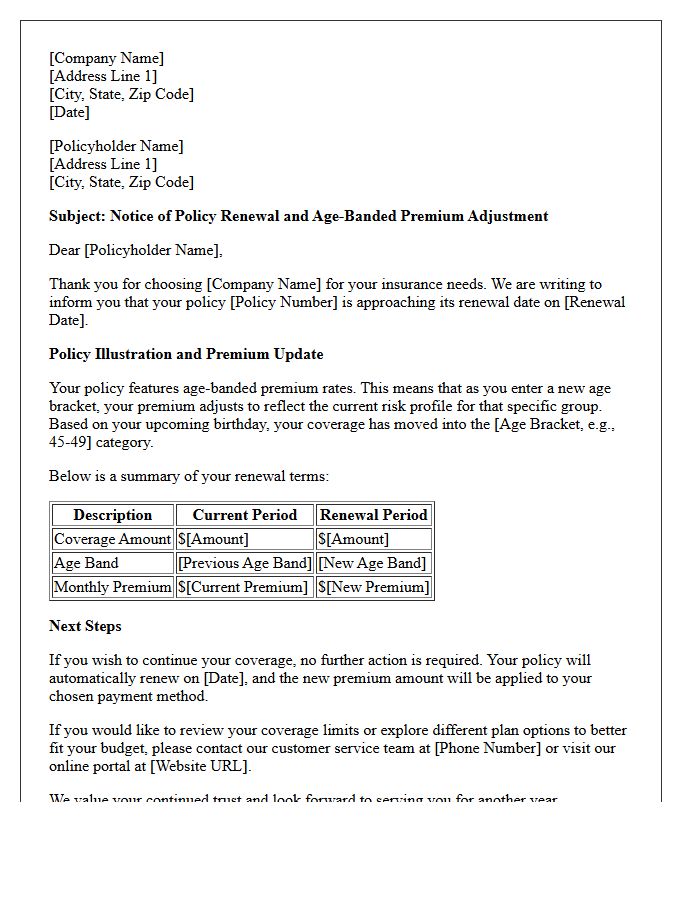

Policy Illustration And Age-Banded Renewal Letter

A Policy Illustration provides a detailed projection of your insurance benefits and potential cash value over time. It is essential for understanding long-term costs versus coverage. When you receive an Age-Banded Renewal Letter, it indicates that your premiums will increase as you move into a higher age bracket. Reviewing these documents together helps you anticipate future premium hikes and assess if the policy remains affordable. Always compare the illustrated non-guaranteed elements against the guaranteed minimums to ensure your financial plan stays on track as you age.

What is an age-banded life insurance renewal?

An age-banded renewal is a scheduled adjustment where life insurance premiums increase as the policyholder enters a new age bracket, typically every five or ten years (e.g., ages 35, 40, 45).

Why do my life insurance premiums increase at specific age intervals?

Premiums increase at specific intervals because age-banded rates are based on the statistical mortality risk associated with your current age group rather than a fixed rate for the life of the policy.

How often do age-banded rate increases occur?

The frequency of rate increases depends on your policy terms, but they most commonly occur on the policy anniversary following your birthday when you move into a new five-year age band (e.g., moving from the 40-44 bracket to the 45-49 bracket).

Can I avoid age-banded premium hikes by switching to a level term policy?

Yes, transitioning to a level term life insurance policy allows you to lock in a fixed premium for a set duration (such as 10, 20, or 30 years), which prevents the periodic cost increases associated with age-banded renewals.

Will my life insurance coverage amount decrease when my age-banded rate increases?

In most standard policies, your coverage amount (death benefit) remains the same during an age-banded renewal, but the cost per thousand dollars of coverage increases to reflect the higher risk associated with older age groups.

Comments