Managing your real estate portfolio requires efficient debt management strategies. An Investment Property Mortgage Acceleration Notice allows lenders to demand immediate repayment of the full loan balance if specific contractual terms are breached or during strategic refinancing. Understanding these legal triggers is essential for protecting your equity and maintaining positive cash flow. Below are some ready to use template options to streamline your professional correspondence.

Image cover: Accelerate Your Returns: Investment Property Mortgage Notice Templates and Samples

Letter Samples List

- Notice of Default and Intent to Accelerate Investment Property Mortgage Letter

- Final Demand and Mortgage Acceleration Notice Letter

- Investment Property Delinquent Tax Mortgage Acceleration Letter

- Due-on-Sale Clause Violation Acceleration Notice Letter

- Lapsed Hazard Insurance Mortgage Acceleration Warning Letter

- Commercial Property Abandonment and Loan Acceleration Letter

- Notice of Acceleration and Assignment of Rents Letter

- Investment Property Breach of Covenant Acceleration Letter

- Formal Notice of Investment Loan Acceleration and Foreclosure Initiation Letter

- Mortgage Acceleration Reinstatement Quotation Letter

- Investment Property Receivership and Acceleration Notice Letter

- Unauthorized Property Alteration Mortgage Acceleration Letter

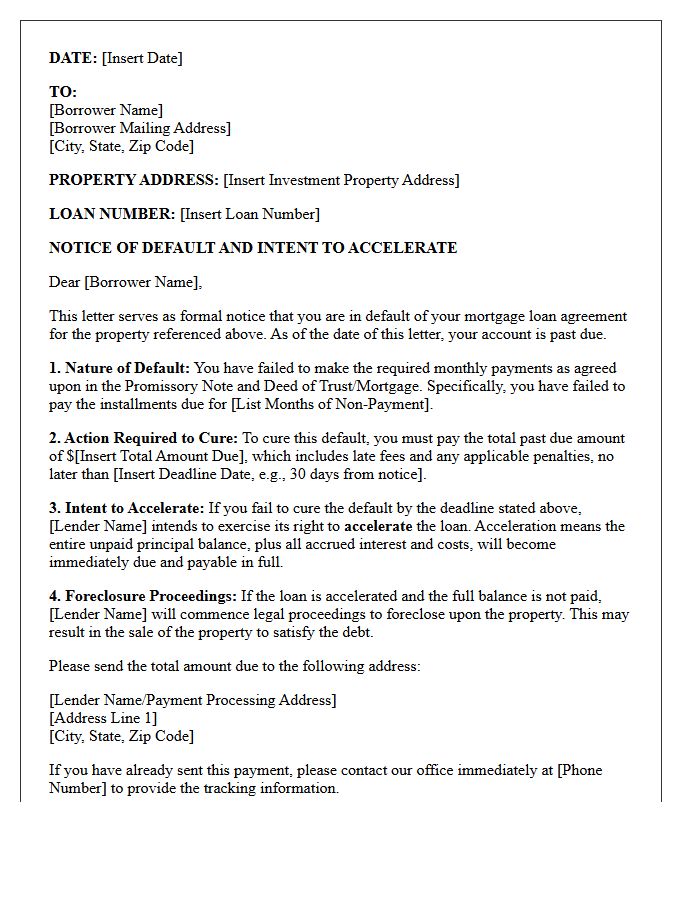

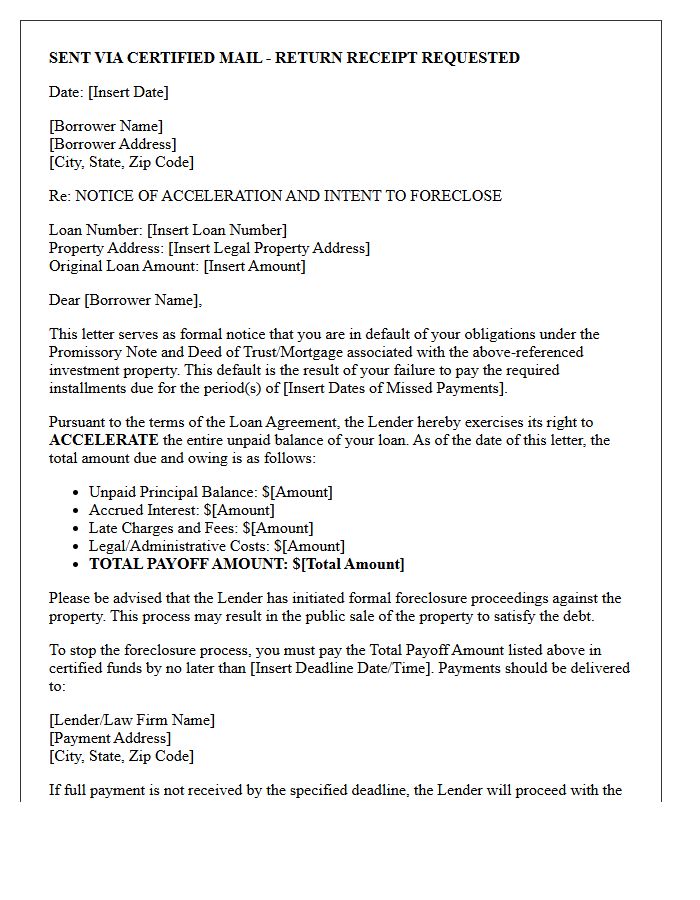

Notice of Default and Intent to Accelerate Investment Property Mortgage Letter

Receiving a Notice of Default and Intent to Accelerate is a critical legal warning for investment property owners. This formal letter signifies that you have breached your loan agreement, typically through missed payments. It serves as the final step before the lender demands the entire loan balance immediately. To prevent a foreclosure sale, investors must "cure the default" by paying all arrears plus fees within the specified deadline. Ignoring this notice risks total loss of the asset and severe credit damage. Immediate legal or financial consultation is essential to explore reinstatement or workout options.

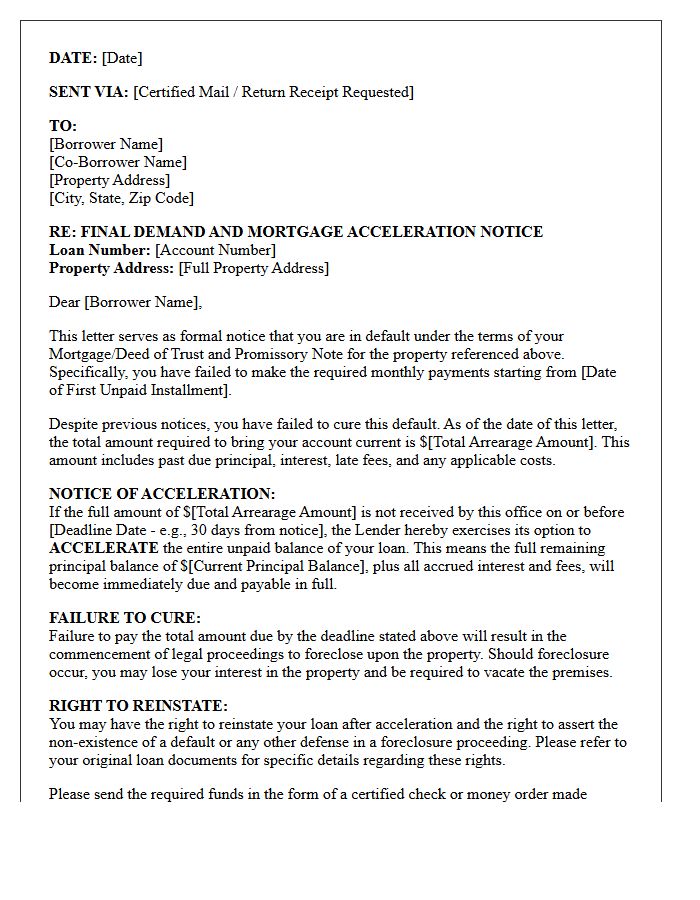

Final Demand and Mortgage Acceleration Notice Letter

A Final Demand and Mortgage Acceleration Notice Letter is a critical legal warning from a lender indicating that a loan is in formal default. This document notifies the borrower that the entire loan balance is now due immediately, rather than just the missed payments. Receiving this letter is the final step before the foreclosure process begins. Homeowners must act quickly to explore loss mitigation options, such as loan modification or reinstatement, to prevent the permanent loss of their property and severe damage to their credit score.

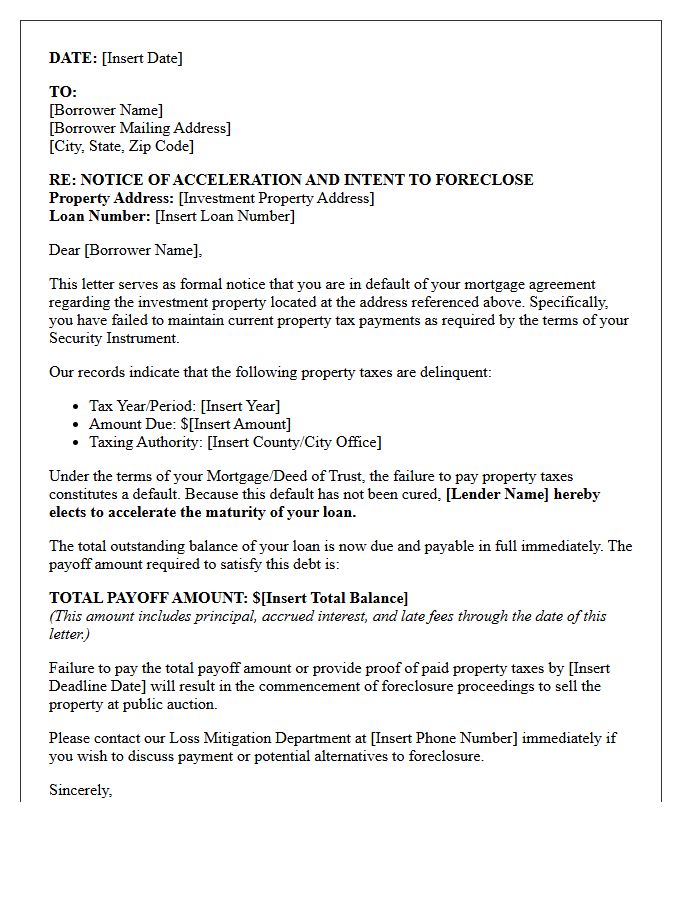

Investment Property Delinquent Tax Mortgage Acceleration Letter

An investment property delinquent tax mortgage acceleration letter is a formal notice from a lender triggered by unpaid property taxes. Since outstanding taxes create a priority lien that supersedes the mortgage, lenders view this as a default. This letter warns the borrower that the entire remaining loan balance is now due immediately. To avoid foreclosure, investors must urgently pay the overdue taxes or negotiate a reinstatement. Maintaining an escrow account or providing proof of payment is essential to protect the asset from legal seizure and total loss of equity.

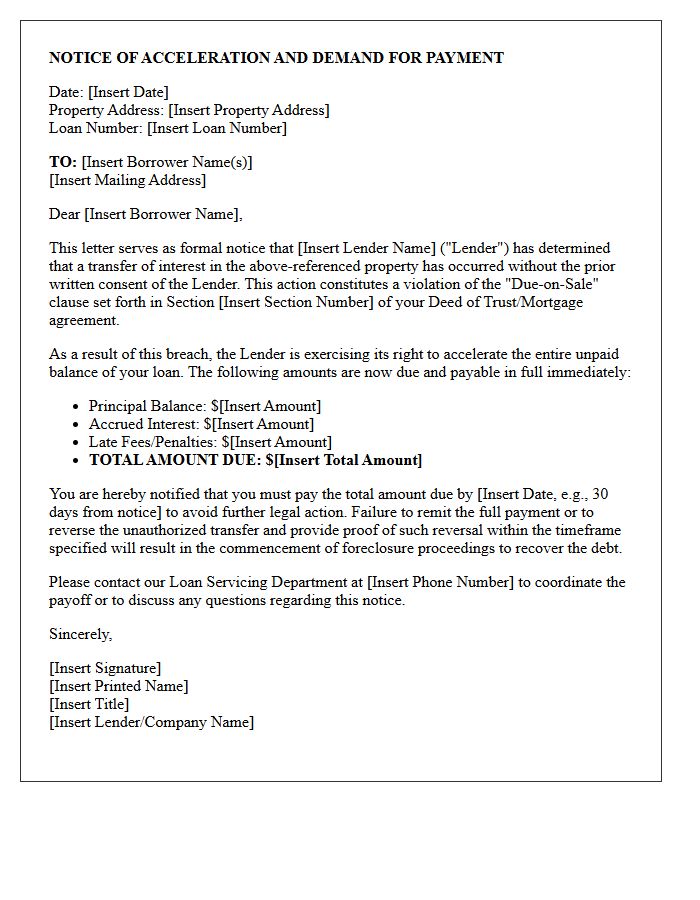

Due-on-Sale Clause Violation Acceleration Notice Letter

A Due-on-Sale Clause Violation Acceleration Notice Letter is a formal legal notification issued by a lender when a property title is transferred without prior consent. This document informs the borrower that they have breached the mortgage contract terms. Consequently, the lender exercises their right to demand immediate repayment of the entire remaining loan balance. Failure to resolve this violation typically leads to foreclosure proceedings. Homeowners must understand that unauthorized transfers, including placing property into certain trusts or LLCs, can trigger this acceleration of debt, requiring urgent legal or financial consultation.

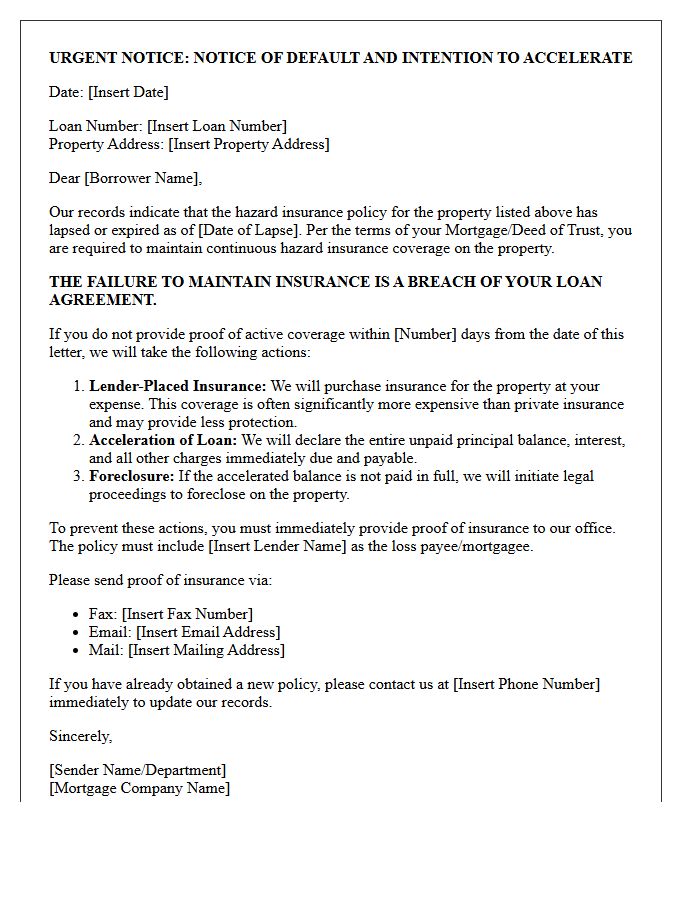

Lapsed Hazard Insurance Mortgage Acceleration Warning Letter

A Lapsed Hazard Insurance Mortgage Acceleration Warning Letter is a critical notice from your lender stating that your homeowners insurance has expired. This document serves as a formal alert that you are in breach of your loan contract. Failure to provide proof of coverage can trigger acceleration, making the entire loan balance due immediately. To avoid foreclosure or expensive force-placed insurance, you must urgently renew your policy and submit the updated declarations page to your mortgage servicer to maintain compliance and protect your property investment.

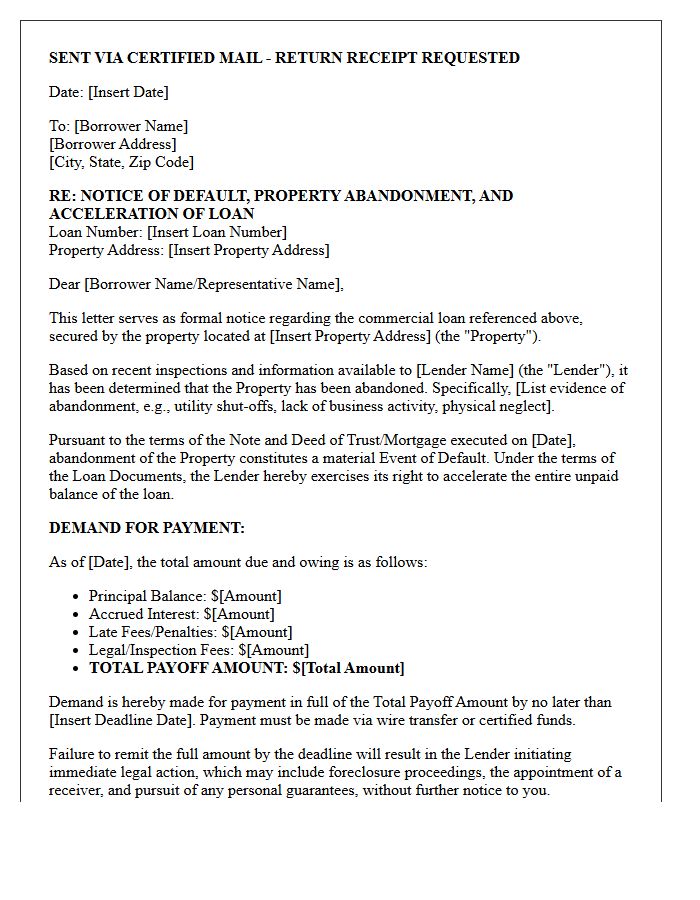

Commercial Property Abandonment and Loan Acceleration Letter

A Commercial Property Abandonment occurs when a tenant permanently vacates premises and ceases rent payments, often triggering a default. Consequently, lenders may issue a Loan Acceleration Letter. This critical legal notice demands immediate repayment of the entire outstanding mortgage balance rather than standard installments. Understanding the relationship between property vacancy and debt acceleration is vital for investors to avoid foreclosure. Timely communication with lenders and reviewing specific "acceleration clauses" in your loan agreement are essential steps to mitigate financial loss and protect your commercial real estate assets from total seizure.

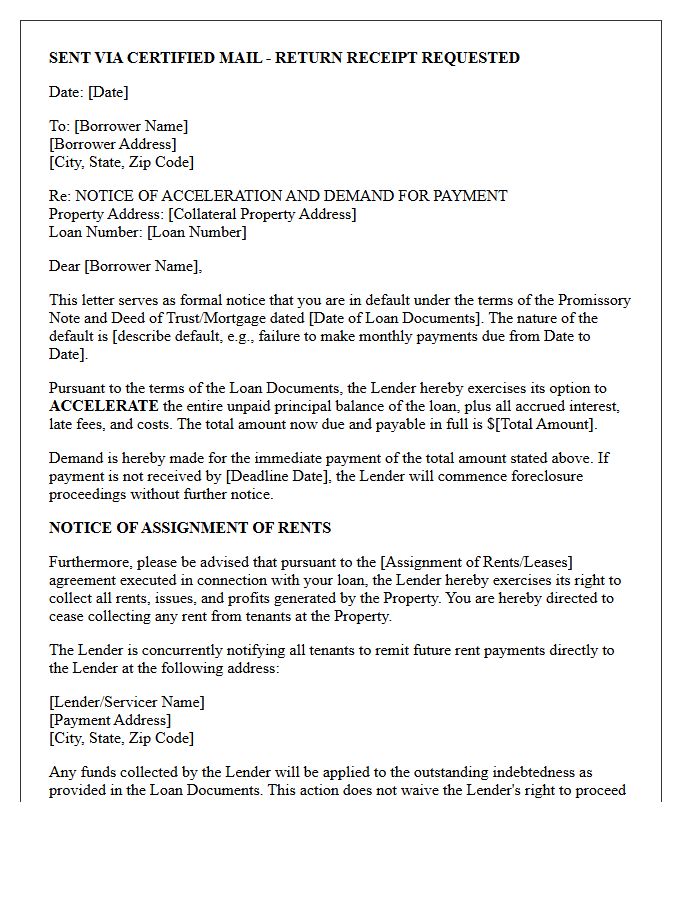

Notice of Acceleration and Assignment of Rents Letter

A Notice of Acceleration and Assignment of Rents is a critical legal document sent by lenders during a mortgage default. It officially triggers the acceleration clause, demanding immediate full repayment of the loan balance. Simultaneously, the lender exercises its right to collect any rental income generated by the property directly from tenants. This action is a final warning before foreclosure proceedings begin. Borrowers must act quickly to negotiate a reinstatement or risk losing their property and income stream to the creditor.

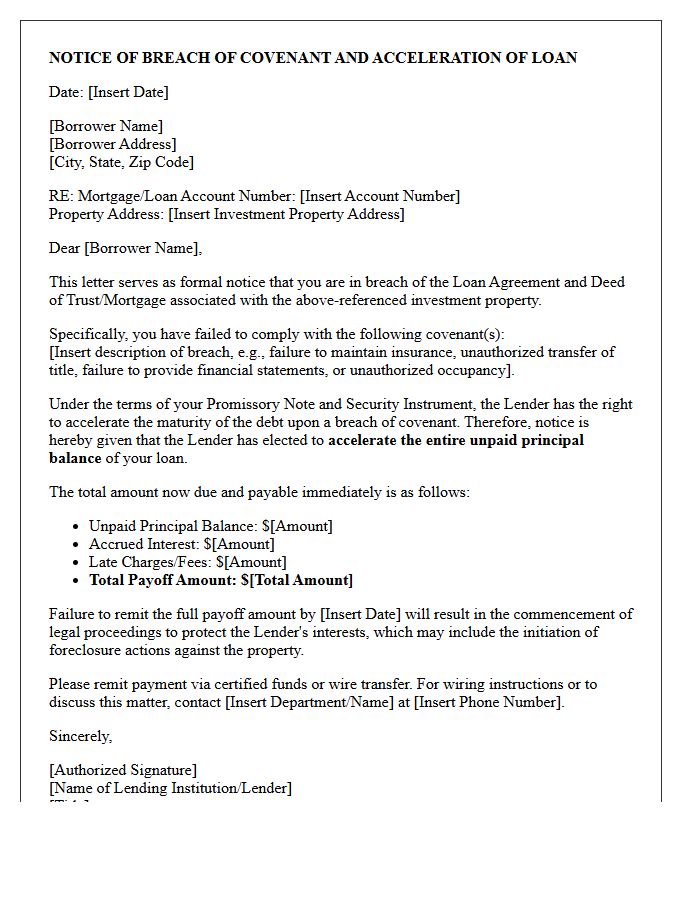

Investment Property Breach of Covenant Acceleration Letter

An Acceleration Letter is a formal legal notice issued when a borrower commits a breach of covenant in an investment property loan agreement. This document notifies the debtor that the entire outstanding loan balance is now due immediately, rather than through scheduled installments. Common triggers include non-payment, unauthorized property transfers, or failure to maintain insurance. Receiving this letter is the final step before the lender initiates foreclosure proceedings. Investors must act quickly to cure the default or negotiate a reinstatement to avoid losing the asset and damaging their credit profile.

Formal Notice of Investment Loan Acceleration and Foreclosure Initiation Letter

A formal notice of investment loan acceleration and foreclosure initiation signifies that a lender has declared the entire loan balance due immediately following a default. This legal document warns the borrower that foreclosure proceedings have officially commenced to reclaim the property. It is critical to review the specific cure period provided, as this is often the final opportunity to resolve arrears before the asset is liquidated. Receiving this letter requires urgent action to explore loss mitigation, refinancing, or legal defense to prevent the permanent loss of the investment collateral.

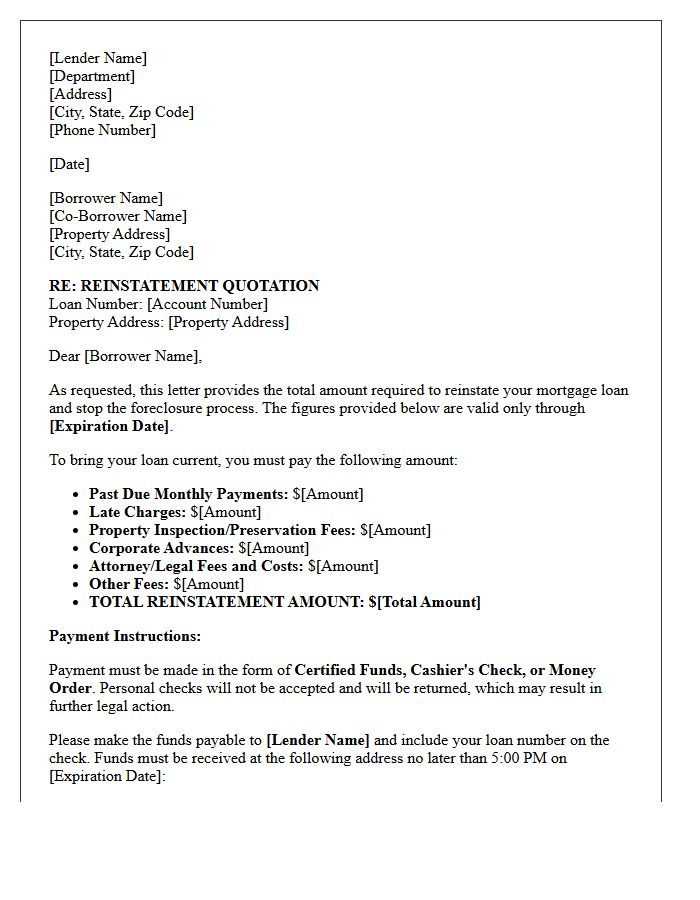

Mortgage Acceleration Reinstatement Quotation Letter

A Mortgage Acceleration Reinstatement Quotation Letter is a formal document issued by lenders after a borrower defaults. It specifies the exact total amount required to bring a delinquent loan current and stop the foreclosure process. This statement outlines past-due principal, interest, late fees, and legal costs. Understanding this letter is critical because it provides a reinstatement deadline; payments made after this date may be rejected. It serves as the final opportunity for homeowners to resolve default status and restore their original payment schedule before a property is forcibly liquidated.

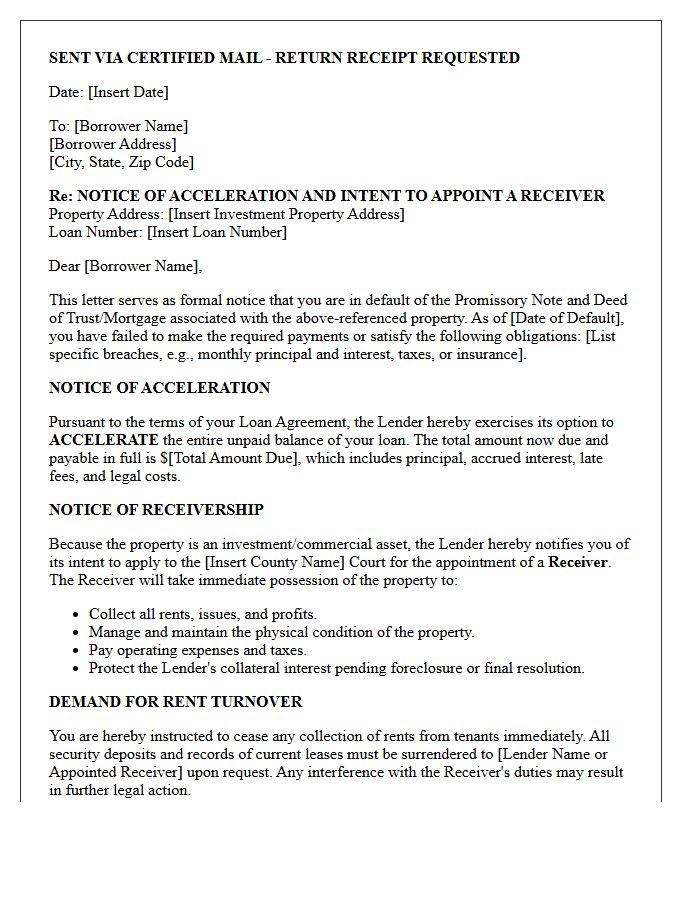

Investment Property Receivership and Acceleration Notice Letter

An Acceleration Notice Letter is a critical legal notification issued by lenders when a borrower defaults on a mortgage. It demands immediate full repayment of the outstanding loan balance, effectively canceling the installment plan. In the context of investment properties, this step often triggers Property Receivership. A court-appointed receiver takes control of the asset to collect rents, manage operations, and protect the property's value for the creditor. Understanding these documents is vital, as they signal the final stage before potential foreclosure and the loss of management rights over the investment.

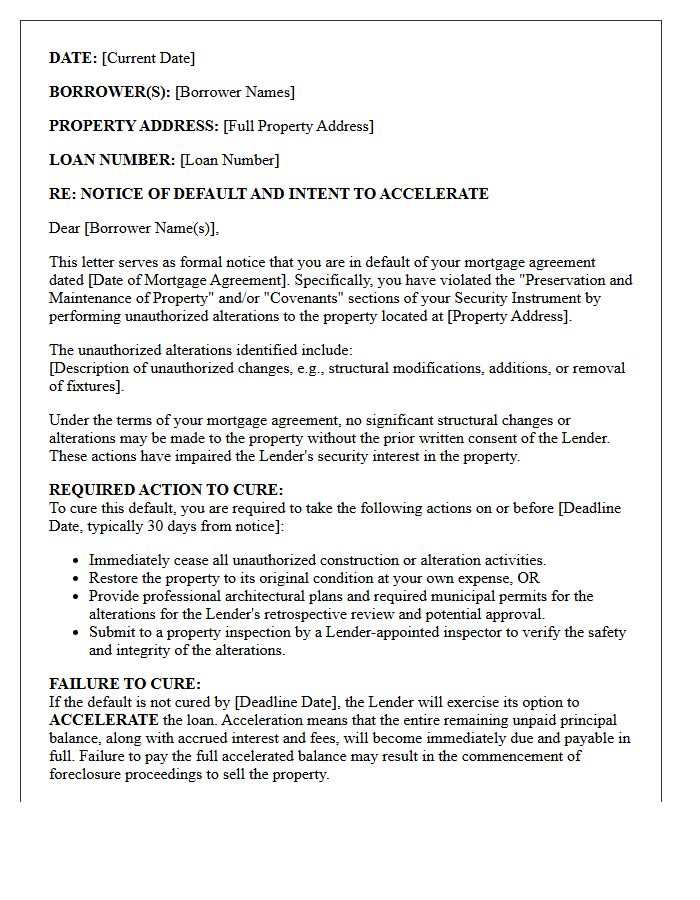

Unauthorized Property Alteration Mortgage Acceleration Letter

An Unauthorized Property Alteration Mortgage Acceleration Letter is a legal notice sent by lenders when a borrower modifies a property without prior consent. Most loan contracts include covenants requiring permission for structural changes to protect the asset's value. If violated, the lender may invoke the acceleration clause, demanding full repayment of the remaining loan balance immediately. To avoid foreclosure, homeowners must obtain written authorization before starting renovations or quickly negotiate a resolution to restore the property to its original state as defined in the deed of trust.

What is an Investment Property Mortgage Acceleration Notice?

An acceleration notice is a formal legal demand from a lender requiring the borrower to pay the entire remaining balance of an investment property mortgage immediately. This typically occurs after a default, such as missed payments or a breach of loan covenants, effectively canceling the installment repayment plan.

What triggers a mortgage acceleration clause for real estate investors?

Common triggers include consecutive missed mortgage payments, unauthorized transfer of the property title, failure to maintain required hazard insurance, or neglecting to pay property taxes. For investment loans, a breach of specific commercial occupancy requirements can also initiate the acceleration process.

Can I stop the acceleration process on my investment property?

In many cases, investors can stop acceleration through a process called "reinstatement." This involves paying the full amount of past-due installments, late fees, and legal costs before the deadline specified in the notice. Some lenders may also be open to loan modifications or a deed-in-lieu of foreclosure to settle the debt.

How long do I have to respond to an acceleration notice before foreclosure?

The timeline typically ranges from 30 to 90 days, depending on the state's judicial or non-judicial foreclosure laws and the specific terms of the mortgage contract. The notice will provide a specific "cure date" by which the default must be remedied to avoid a foreclosure sale.

Does a mortgage acceleration notice affect my credit score as an investor?

Yes, receiving an acceleration notice indicates a serious delinquency and impending foreclosure, which can significantly lower your credit score. This status is reported to credit bureaus and can hinder your ability to secure financing for future investment properties or business ventures for several years.

Comments