A Pre-Acceleration Right to Cure Notice is a formal legal notification sent by lenders to borrowers in default. It informs the homeowner of the specific breach, the amount required to reinstate the loan, and a deadline to prevent foreclosure acceleration. Understanding this document is crucial for protecting your property rights. To assist your process, below are some ready to use template.

Image cover: Mastering the Pre-Acceleration Right to Cure: Essential Notice Templates and Best Practices

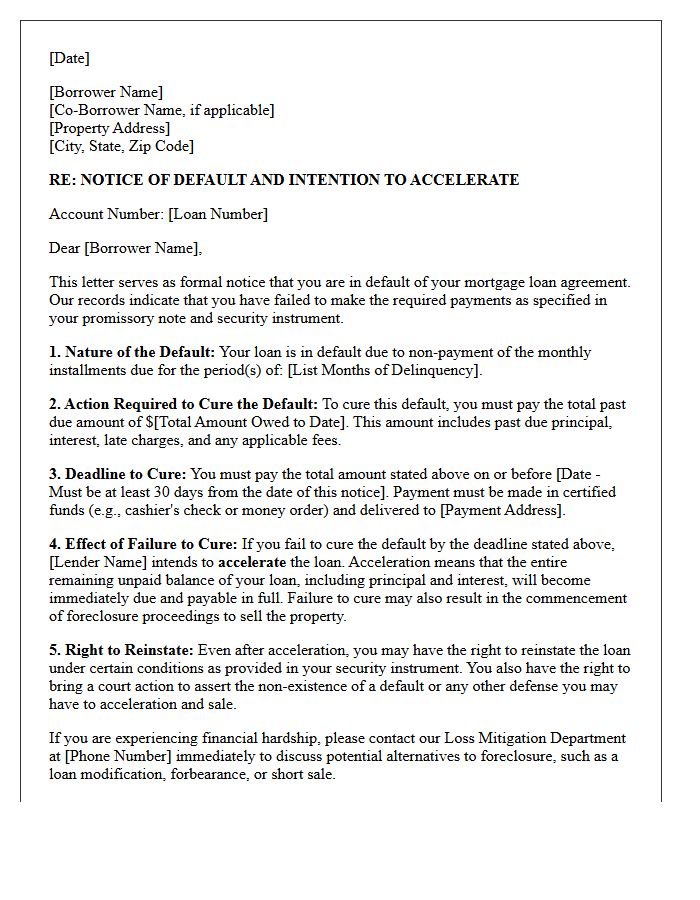

Letter Samples List

- Initial Pre-Acceleration Right to Cure Notice Letter

- Final Pre-Acceleration Right to Cure Warning Letter

- Conventional Mortgage Pre-Acceleration Right to Cure Letter

- FHA Loan Pre-Acceleration Right to Cure Notice Letter

- VA Loan Pre-Acceleration Right to Cure Demand Letter

- Commercial Mortgage Pre-Acceleration Right to Cure Letter

- Residential Mortgage Pre-Acceleration Right to Cure Letter

- State Specific Pre-Acceleration Right to Cure Notice Letter

- Second Warning Pre-Acceleration Right to Cure Letter

- Foreclosure Avoidance Pre-Acceleration Right to Cure Letter

- Investor Backed Pre-Acceleration Right to Cure Letter

- Default Resolution Pre-Acceleration Right to Cure Letter

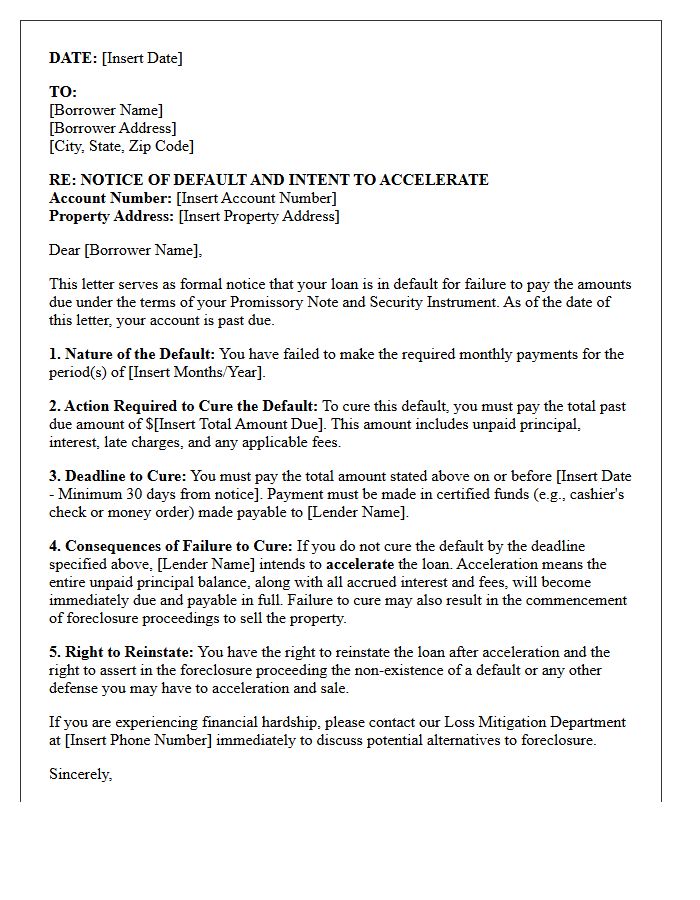

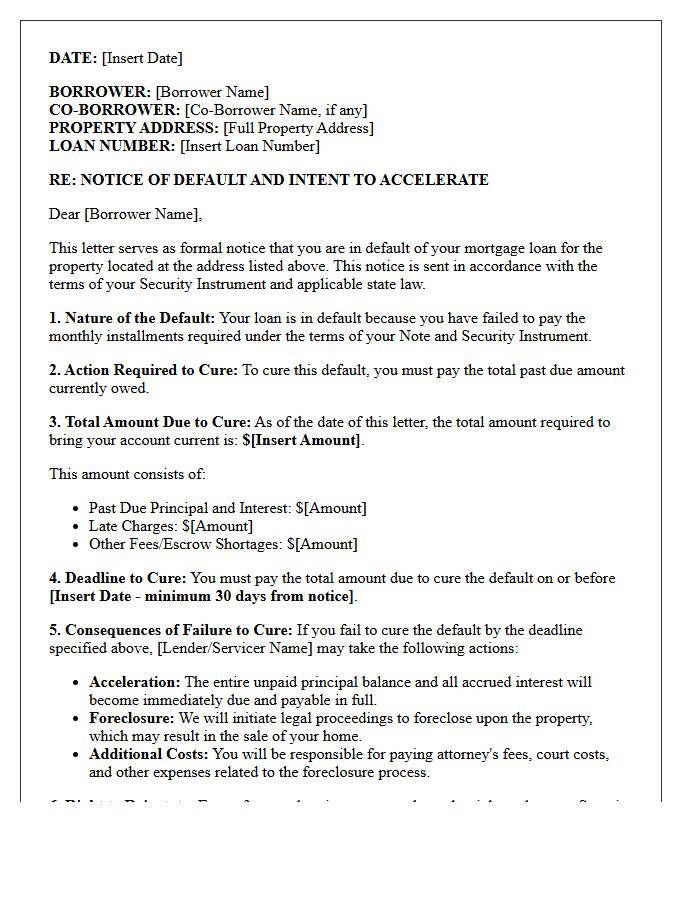

Initial Pre-Acceleration Right to Cure Notice Letter

An Initial Pre-Acceleration Right to Cure Notice Letter is a critical legal document sent by mortgage lenders before initiating foreclosure. It formally notifies borrowers of a default, specifying the exact amount needed to reinstate the loan. This notice grants a mandatory period, typically thirty days, to pay the arrears and "cure" the delinquency. Failure to resolve the debt allows the lender to accelerate the entire loan balance, making the full amount due immediately. Receiving this letter is a final warning to seek loss mitigation and protect your property rights.

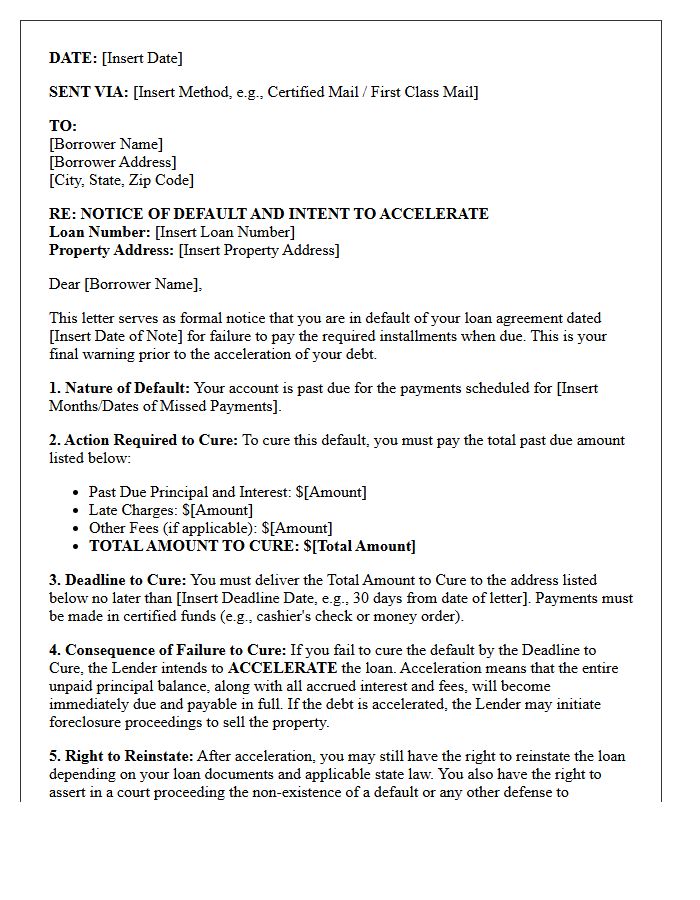

Final Pre-Acceleration Right to Cure Warning Letter

The Final Pre-Acceleration Right to Cure Warning Letter is a critical legal notice sent to borrowers in default. It serves as a formal notification that the lender intends to demand the full mortgage balance through acceleration unless the specific arrears are paid. This document outlines the exact amount required to reinstate the loan, provides a strict deadline for payment, and details the borrower's rights to avoid foreclosure. Receiving this letter is the final opportunity to rectify a delinquency before the lender initiates formal legal action or a trustee sale.

Conventional Mortgage Pre-Acceleration Right to Cure Letter

A Right to Cure Letter is a mandatory formal notice sent by lenders before starting foreclosure. This pre-acceleration document informs borrowers of a specific default, typically overdue payments, and provides a deadline to resolve the debt. To prevent the full loan balance from becoming immediately due, the homeowner must pay the total arrears by the specified date. Understanding this letter is critical because it represents the final opportunity to reinstate the mortgage and avoid legal proceedings. Failure to act on this notice grants the lender the right to accelerate the debt and sell the property.

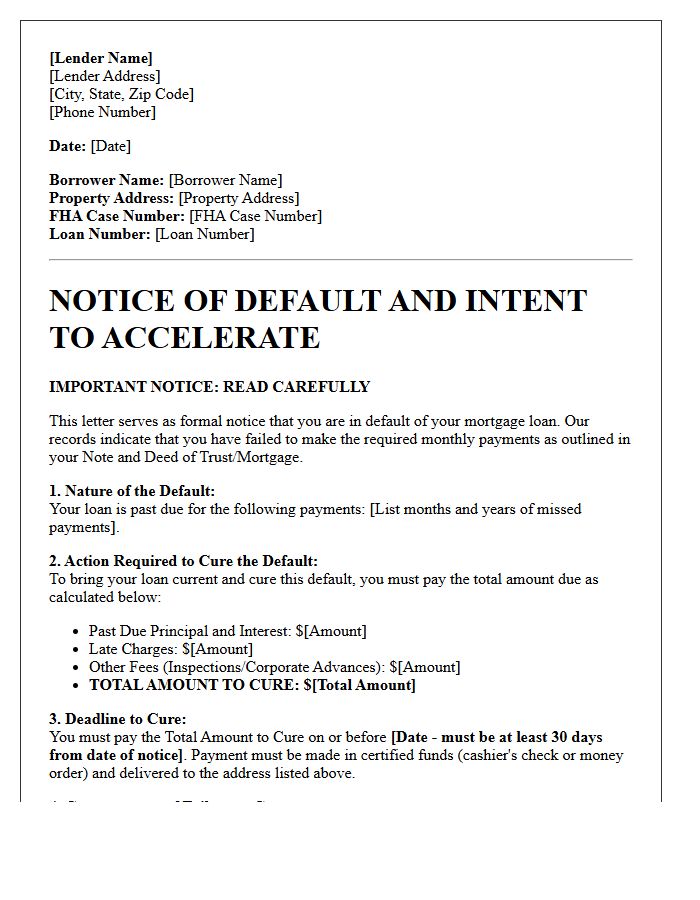

FHA Loan Pre-Acceleration Right to Cure Notice Letter

An FHA Loan Pre-Acceleration Right to Cure Notice Letter is a critical legal document sent to borrowers in default. This notice provides a thirty-day window to resolve mortgage arrears before the lender initiates formal foreclosure proceedings. It serves as a final opportunity to reinstate the loan by paying the total overdue amount, including late fees. Understanding this letter is essential because it outlines your specific rights to avoid acceleration, ensuring you have a clear path to save your home through loss mitigation or full repayment before legal action begins.

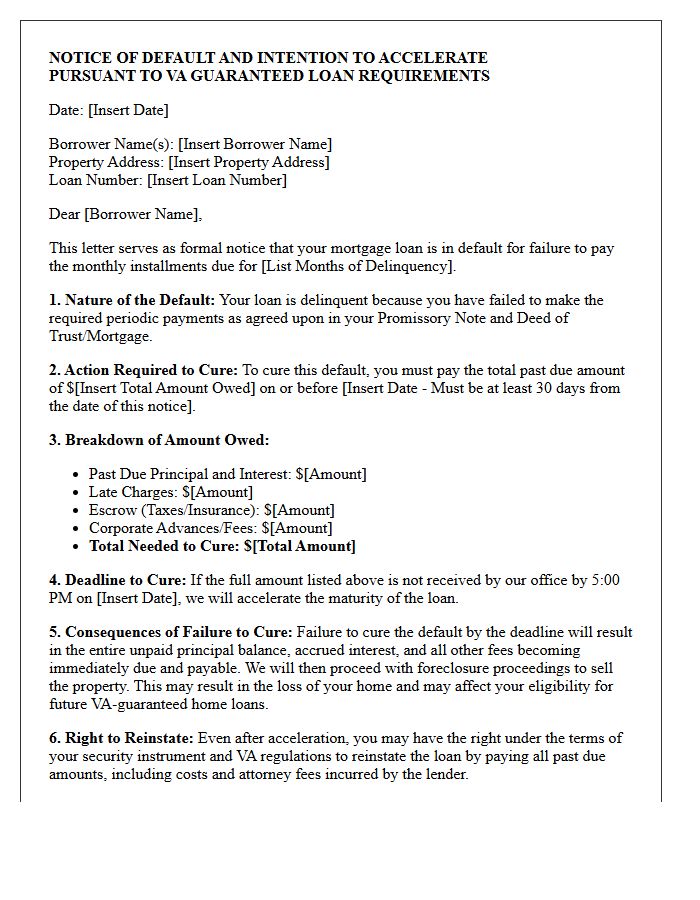

VA Loan Pre-Acceleration Right to Cure Demand Letter

A VA Loan Pre-Acceleration Right to Cure Demand Letter is a mandatory legal notice sent to veterans who have defaulted on their mortgage. This critical document informs the borrower of their right to reinstate the loan by paying the past-due balance within a specific timeframe, typically 30 days. It serves as a final warning before the lender accelerates the debt to initiate foreclosure. Receiving this letter is a vital window to pursue loss mitigation options, such as repayment plans or loan modifications, to protect your home and veteran benefits.

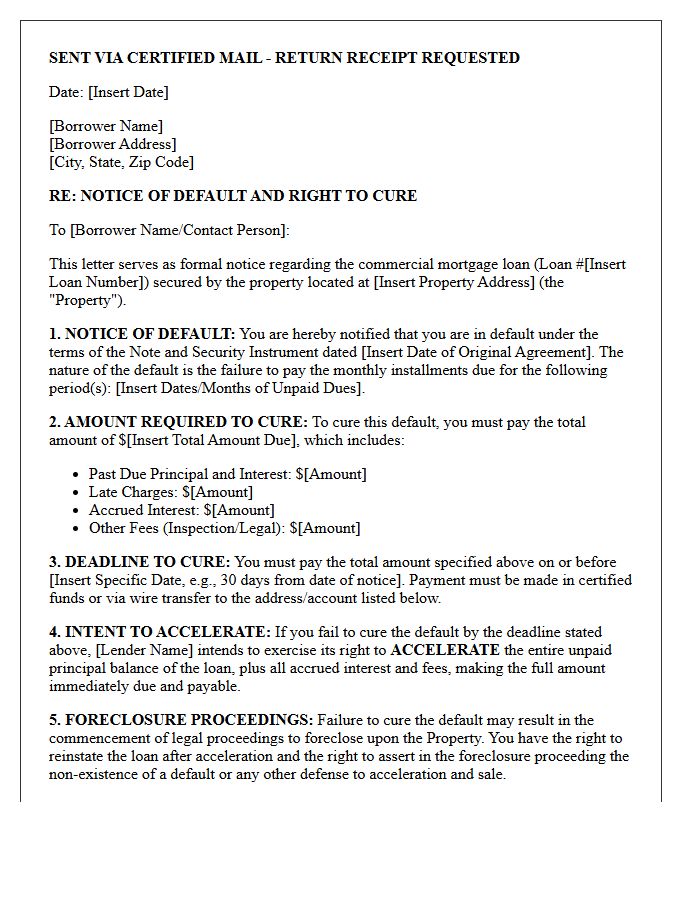

Commercial Mortgage Pre-Acceleration Right to Cure Letter

A Commercial Mortgage Pre-Acceleration Right to Cure Letter is a formal legal notice sent to borrowers following a loan default. This mandatory document outlines the specific breach, the exact amount required to rectify the delinquency, and a strict compliance deadline. It serves as a final opportunity to restore the loan to good standing before the lender exercises the right to accelerate the debt, making the entire balance due immediately. Understanding this letter is critical for commercial property owners to prevent foreclosure proceedings and preserve their investment equity through timely remedial action.

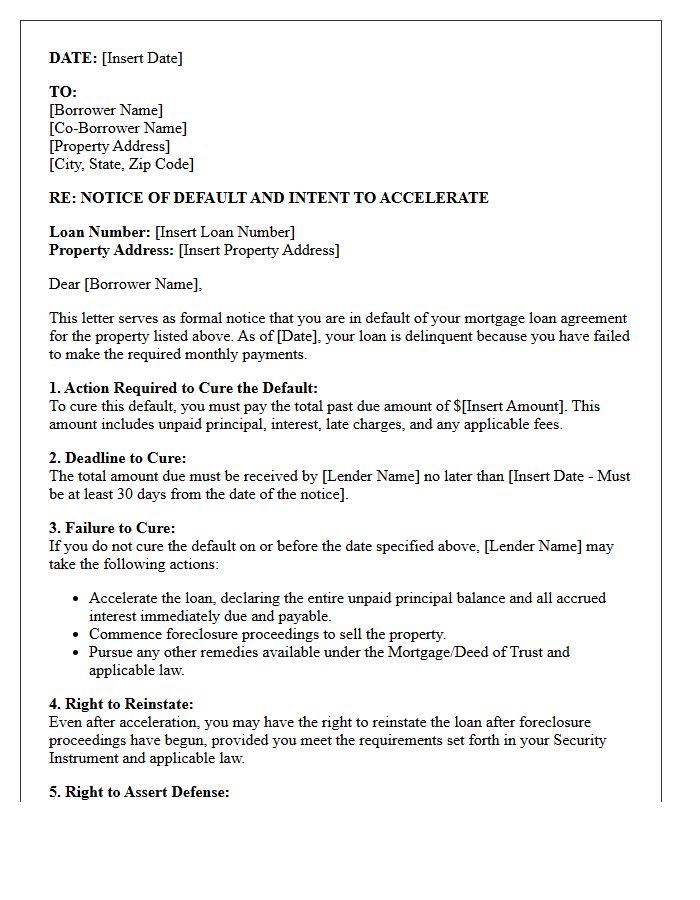

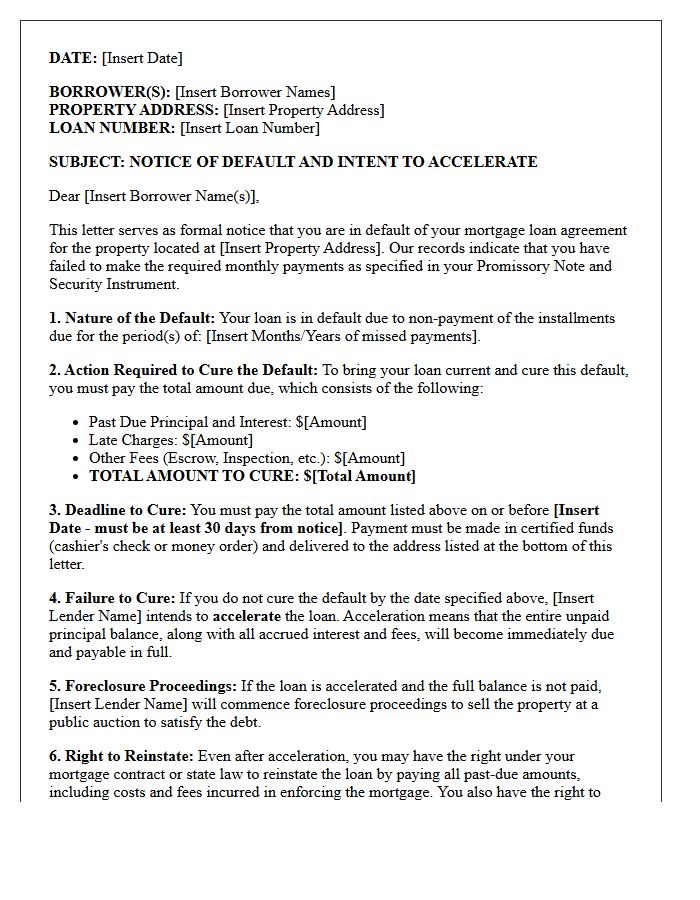

Residential Mortgage Pre-Acceleration Right to Cure Letter

A residential mortgage pre-acceleration right to cure letter is a mandatory legal notice sent to borrowers in default. This document informs homeowners of their specific delinquency and provides a final opportunity to reinstate the loan by paying the overdue balance. It serves as a critical consumer protection, outlining the exact actions required to avoid foreclosure. Failure to satisfy the terms within the designated timeframe allows the lender to accelerate the debt, making the entire mortgage balance due immediately and initiating formal legal proceedings against the property.

State Specific Pre-Acceleration Right to Cure Notice Letter

A State Specific Pre-Acceleration Right to Cure Notice Letter is a mandatory legal document sent to borrowers in default. This notice informs the homeowner of their delinquency and provides a specific timeframe to pay the outstanding balance. It is a critical procedural safeguard that must strictly adhere to state-level statutes. Failure to provide accurate information regarding the amount due or the deadline can legally invalidate the foreclosure process, protecting the borrower's consumer rights before the lender accelerates the entire loan balance for collection.

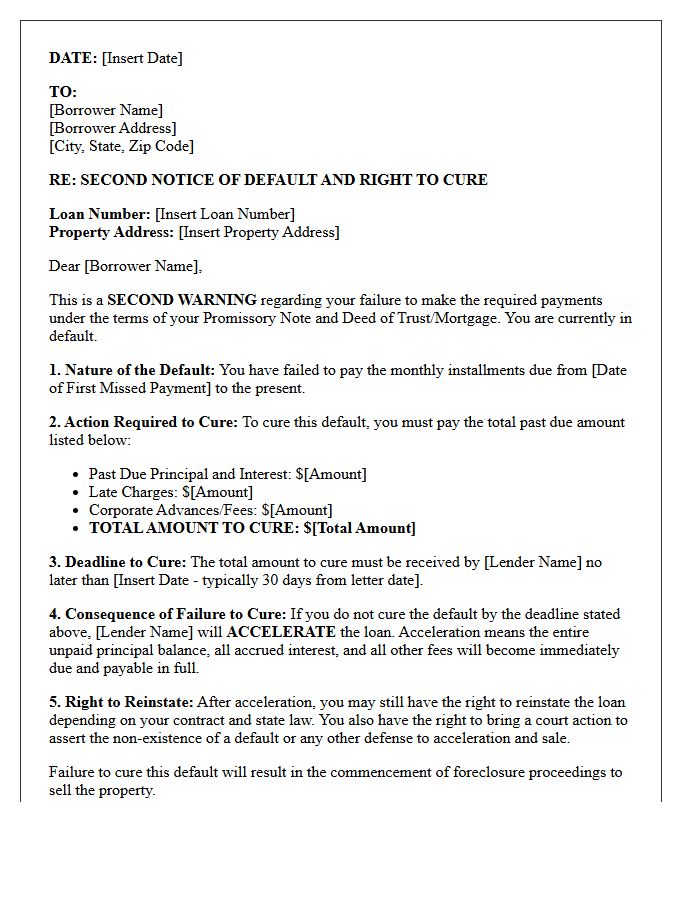

Second Warning Pre-Acceleration Right to Cure Letter

A Second Warning Pre-Acceleration Right to Cure Letter is a formal notice sent by a lender before initiating foreclosure. It serves as a final opportunity for borrowers to resolve loan defaults by paying the total overdue balance within a specific timeframe. This document outlines the exact amount owed, the deadline for payment, and the consequences of inaction. Failure to comply typically results in acceleration, making the entire mortgage balance due immediately and authorizing the lender to commence legal foreclosure proceedings to reclaim the property.

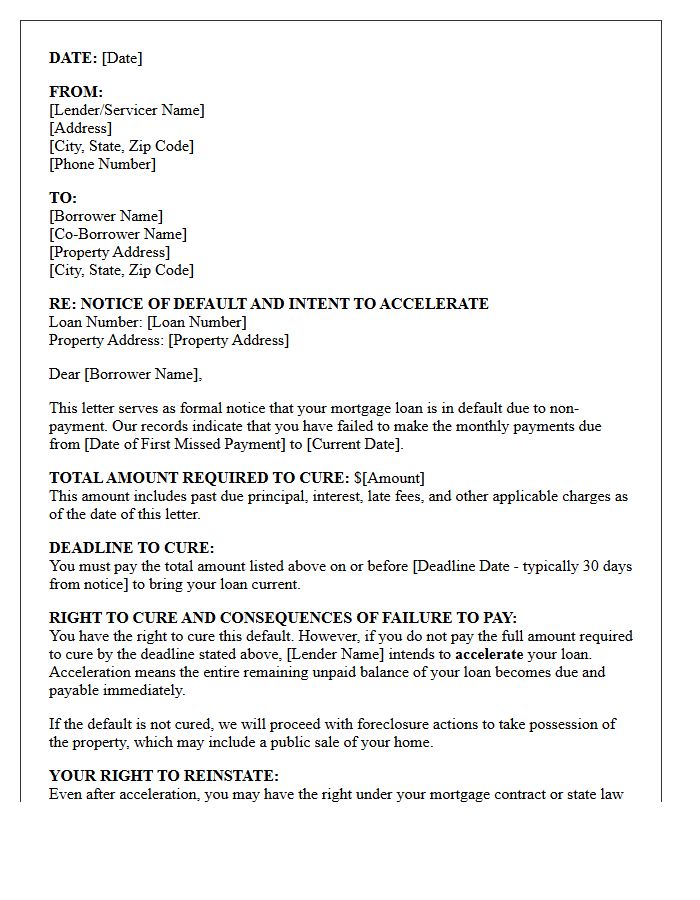

Foreclosure Avoidance Pre-Acceleration Right to Cure Letter

A Foreclosure Avoidance Pre-Acceleration Right to Cure Letter is a mandatory legal notice sent by lenders before starting foreclosure. It informs homeowners of a specific default, such as missed payments, and provides a deadline to pay the arrears. This "right to cure" allows borrowers to reinstate their mortgage and avoid full loan acceleration. Understanding this document is vital because it outlines the exact steps needed to stop foreclosure proceedings. If the deadline passes without payment or a workout plan, the lender can demand the entire loan balance immediately.

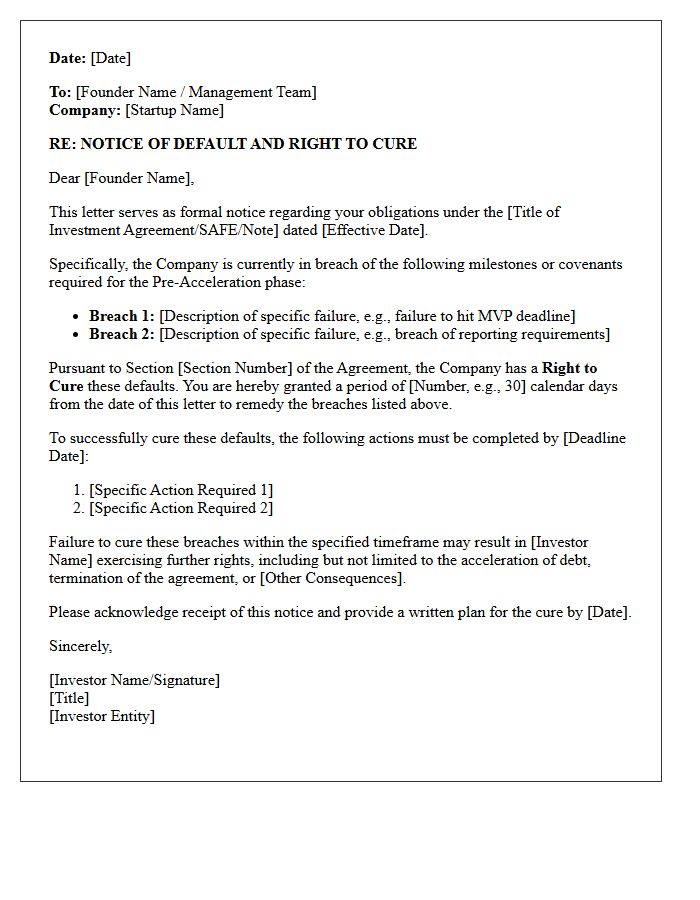

Investor Backed Pre-Acceleration Right to Cure Letter

An Investor Backed Pre-Acceleration Right to Cure Letter is a formal notice issued by lenders before declaring a loan default. It provides distressed startups a final opportunity to rectify specific breaches, such as missed payments or covenant violations, within a set timeframe. For venture-backed companies, this document is critical for maintaining financial stability and avoiding immediate foreclosure. Successfully curing the default preserves the cap table and ensures the business remains viable for future funding rounds, preventing the lender from accelerating the full debt repayment prematurely.

Default Resolution Pre-Acceleration Right to Cure Letter

A Default Resolution Pre-Acceleration Right to Cure Letter is a formal legal notice sent by mortgage lenders before initiating foreclosure. This document informs borrowers of a specific default, typically missed payments, and provides a deadline to resolve the delinquency. It serves as a mandatory warning, granting the homeowner a final opportunity to pay the outstanding balance to reinstate the loan. Failure to act within the specified timeframe allows the lender to accelerate the debt, making the entire loan balance due immediately and moving the property toward a foreclosure sale.

What is a Pre-Acceleration Right to Cure Notice?

A Pre-Acceleration Right to Cure Notice is a formal legal notification sent by a mortgage lender to a borrower in default, specifying the exact amount needed to reinstate the loan and providing a deadline to pay before the lender calls the entire balance due.

What information must be included in a Right to Cure Notice?

The notice must clearly state the nature of the default, the specific action required to cure the default, a deadline (typically 30 days), and a warning that failure to cure may result in the acceleration of the loan and a subsequent foreclosure sale.

How much time do I have to respond to a Pre-Acceleration Notice?

Most standard mortgage contracts and state laws require lenders to provide a minimum of 30 days from the date of the notice for the borrower to pay the past-due amount and "cure" the default to avoid acceleration.

Can a lender start foreclosure before the Right to Cure period expires?

No, the lender is legally prohibited from initiating formal foreclosure proceedings or accelerating the debt until the time period specified in the Pre-Acceleration Right to Cure Notice has fully elapsed without the default being resolved.

What happens if I fail to cure the default by the deadline?

If the deadline passes without payment, the lender may "accelerate" the loan, meaning the full remaining principal balance becomes due immediately, and the property can be moved into the formal foreclosure process.

Comments