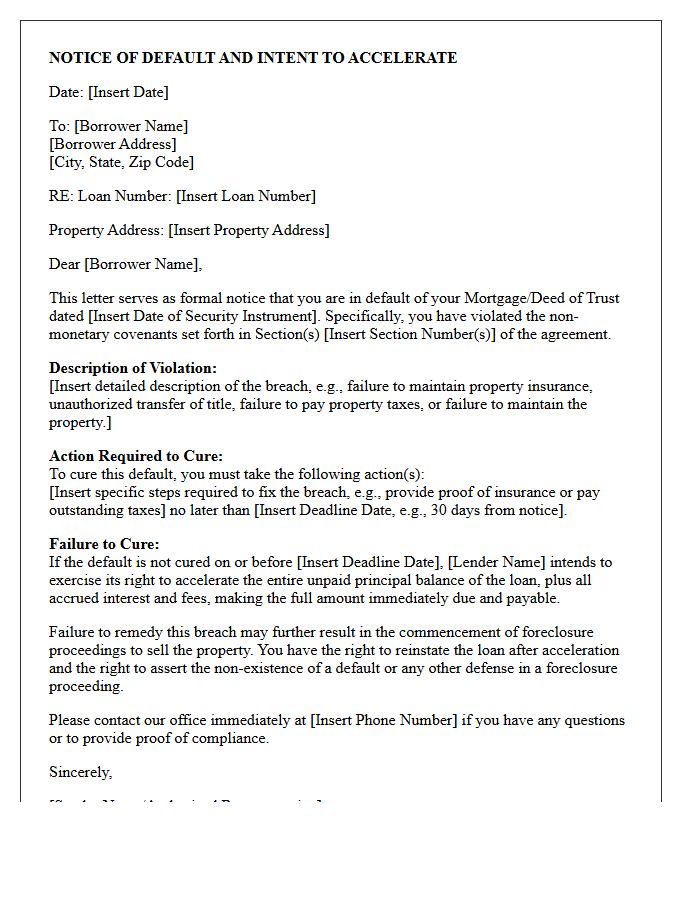

A Non-Monetary Default Acceleration Notice is a formal legal demand issued when a borrower breaches loan covenants unrelated to payments, such as failing to maintain insurance or unauthorized property transfers. This notice informs the borrower that the entire loan balance is now due immediately. Understanding these triggers is essential for proactive debt management. Below are some ready to use template.

Image cover: Demand for Immediate Remedy: Non-Monetary Default and Acceleration Notice Templates

Letter Samples List

- Unauthorized Property Transfer Default Acceleration Letter

- Lapse Of Hazard Insurance Non-Monetary Acceleration Letter

- Delinquent Property Tax Lien Default Acceleration Letter

- Breach Of Primary Occupancy Requirement Acceleration Letter

- Severe Property Damage And Waste Default Acceleration Letter

- Unauthorized Subordinate Financing Notice Of Acceleration Letter

- Illegal Property Usage Non-Monetary Default Acceleration Letter

- Homeowners Association Lien Breach Acceleration Letter

- Unauthorized Structural Alteration Default Acceleration Letter

- Failure To Provide Financial Statements Acceleration Letter

- Intentional Cloud On Title Default Acceleration Letter

- Violation Of Non-Monetary Mortgage Covenants Acceleration Letter

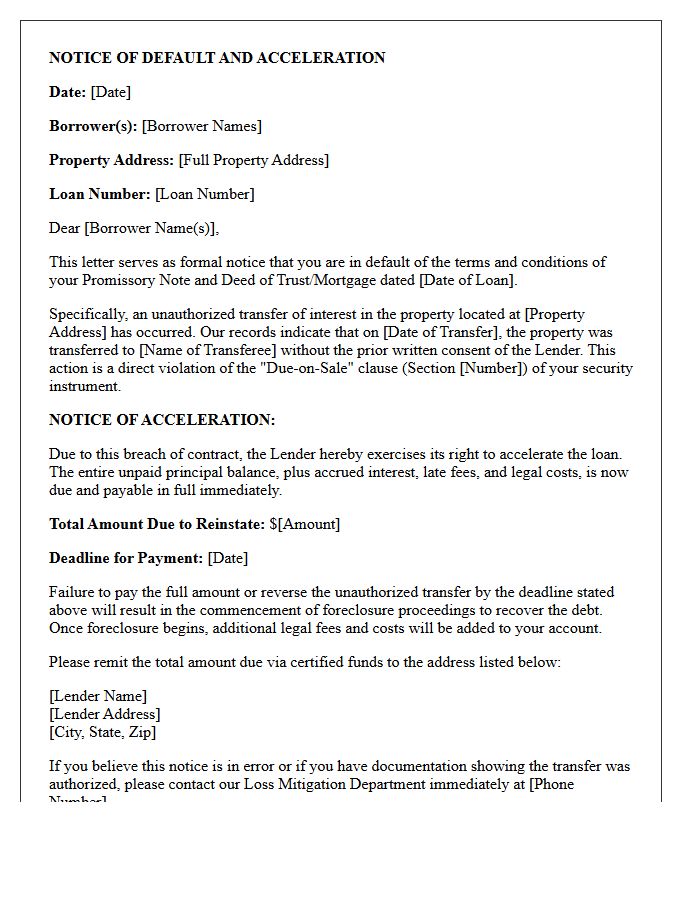

Unauthorized Property Transfer Default Acceleration Letter

An Unauthorized Property Transfer Default Acceleration Letter is a formal legal notice issued by a lender when a borrower transfers real estate ownership without prior consent. This action violates the Due-on-Sale clause found in most mortgage contracts. The letter informs the borrower that the lender is exercising its right to accelerate the loan, demanding immediate repayment of the entire outstanding balance. Failure to resolve this breach or pay the full amount typically leads to foreclosure proceedings to recover the debt through a forced sale of the property.

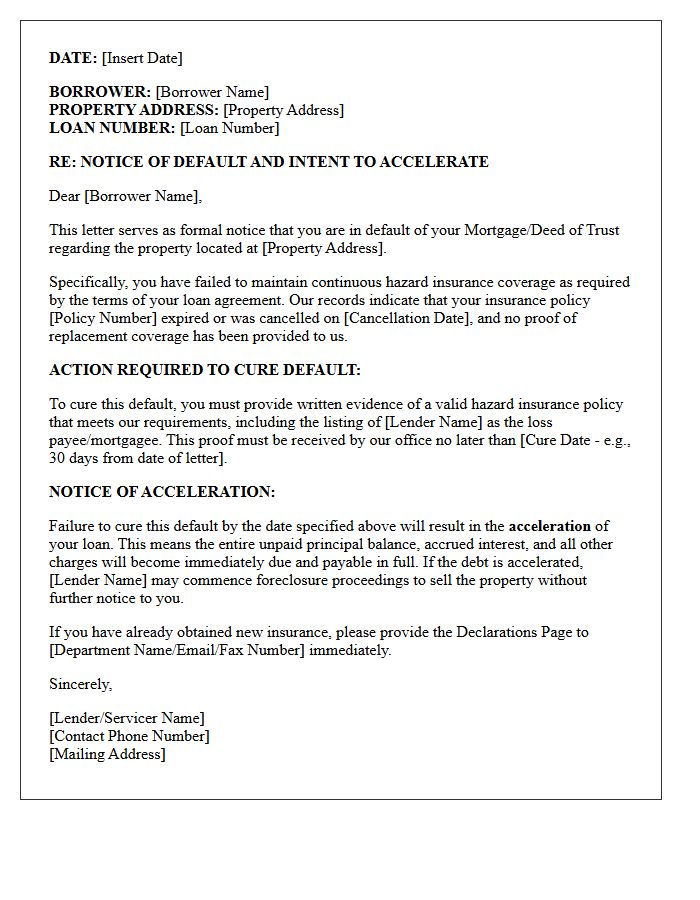

Lapse Of Hazard Insurance Non-Monetary Acceleration Letter

A Lapse of Hazard Insurance Non-Monetary Acceleration Letter is a formal legal notice sent by mortgage lenders when a borrower fails to maintain required property coverage. Since insurance protects the collateral, this breach constitutes a non-monetary default under the deed of trust. If the homeowner does not provide proof of active coverage or resolve the lapse immediately, the lender may exercise the acceleration clause, demanding full repayment of the entire loan balance and potentially initiating foreclosure proceedings to mitigate financial risk.

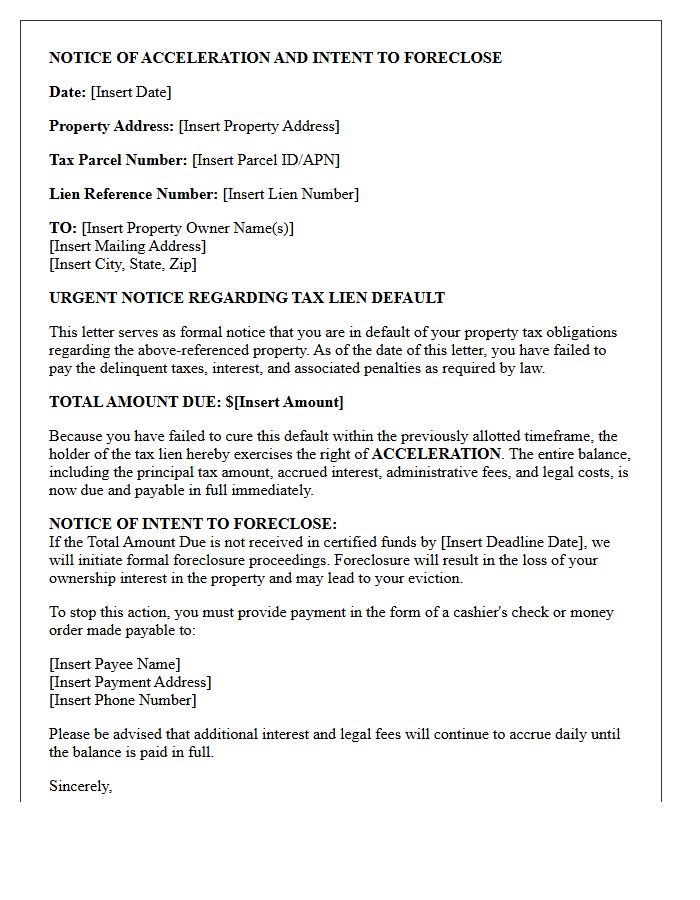

Delinquent Property Tax Lien Default Acceleration Letter

A Delinquent Property Tax Lien Default Acceleration Letter is a formal legal notice issued when a homeowner fails to meet tax obligations. This acceleration clause demands immediate payment of the entire outstanding balance, rather than just missed installments. Receiving this document signifies the final stage before a tax lien foreclosure begins. To prevent the loss of property, owners must act quickly to settle the debt or negotiate a payment plan. Ignoring this notice typically leads to a foreclosure sale, where the government or an investor acquires the property title.

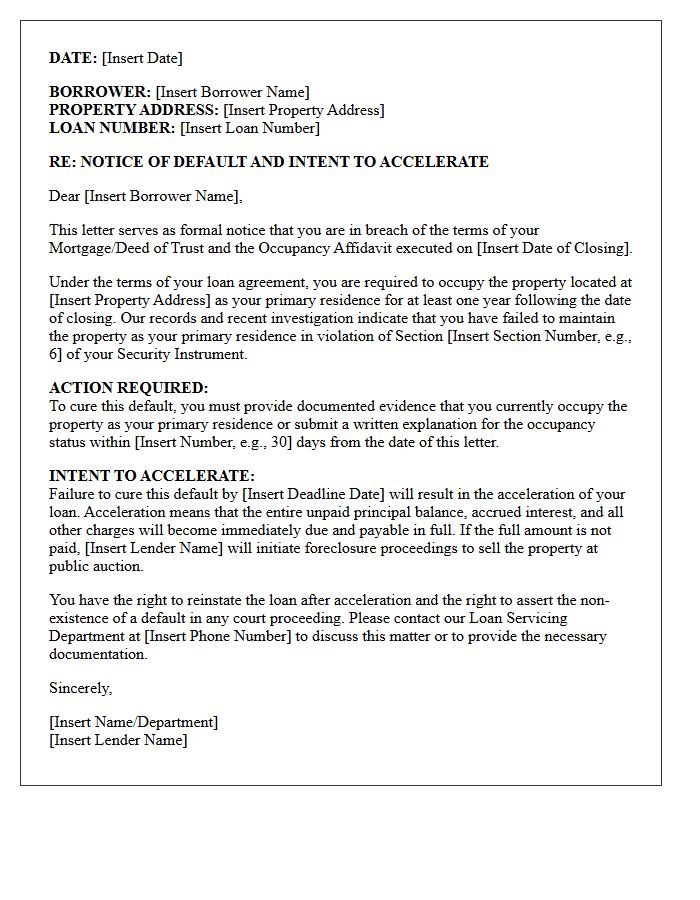

Breach Of Primary Occupancy Requirement Acceleration Letter

A Breach of Primary Occupancy Requirement Acceleration Letter is a formal legal notice issued by a lender when a borrower fails to live in their property as a principal residence. This violation of occupancy covenants triggers a default, allowing the bank to demand immediate full repayment of the mortgage balance. Homeowners must provide proof of residency promptly to avoid potential foreclosure. Maintaining primary occupancy is crucial because owner-occupied loans typically offer lower interest rates and specific legal protections that investment properties do not receive under standard mortgage agreements.

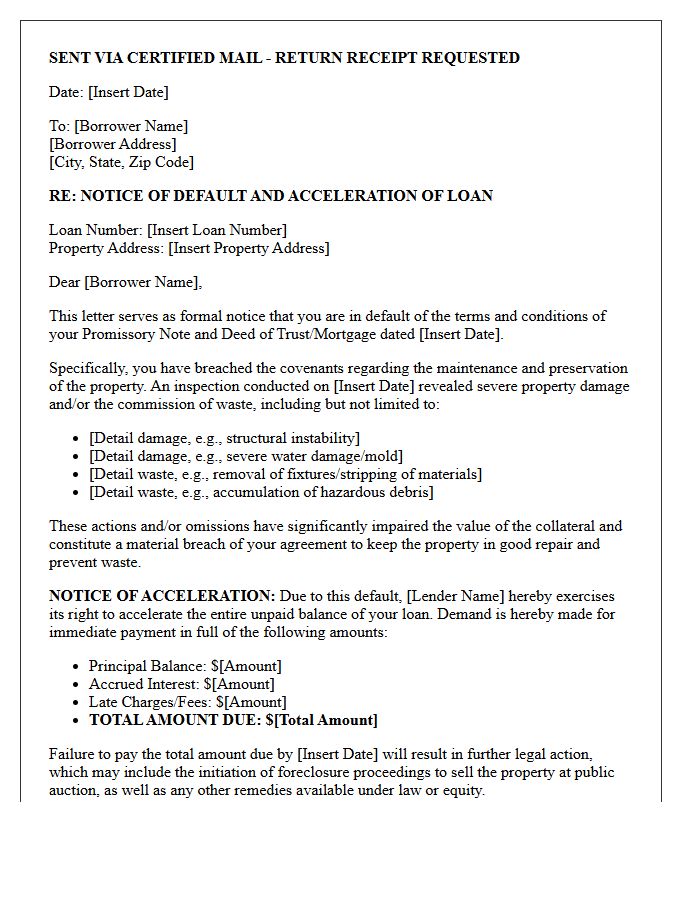

Severe Property Damage And Waste Default Acceleration Letter

A Severe Property Damage and Waste Default Acceleration Letter is a formal legal notice sent by a lender to a borrower. It triggers immediate repayment of the total loan balance due to significant physical destruction or neglect that diminishes the asset's value. This document serves as a final warning that the borrower has breached the security instrument by failing to maintain the property. If the hazardous conditions or waste are not cured within the specified timeframe, the lender will proceed with foreclosure to protect their financial interest in the collateral.

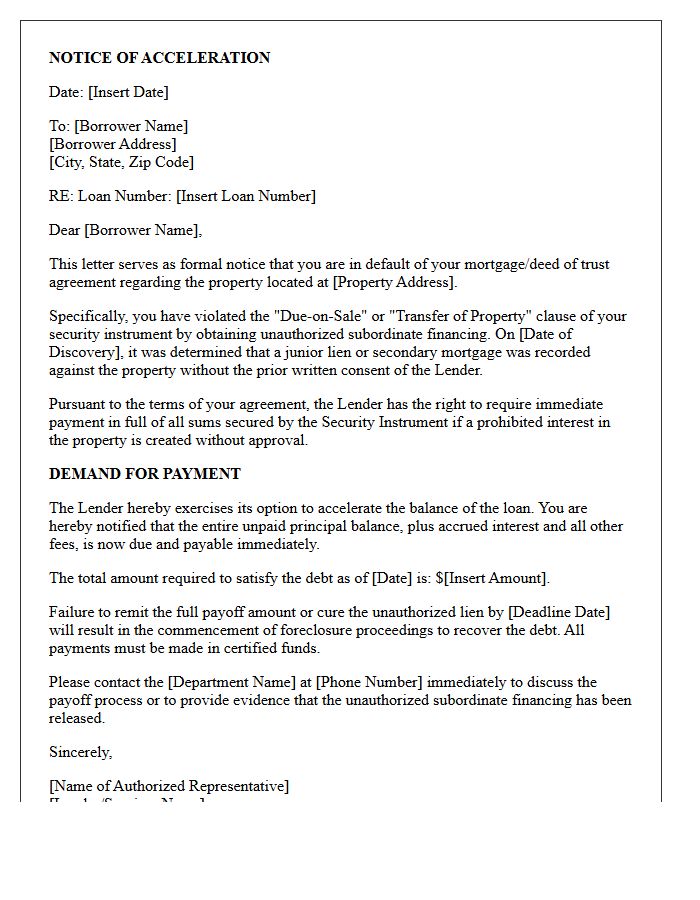

Unauthorized Subordinate Financing Notice Of Acceleration Letter

An Unauthorized Subordinate Financing Notice of Acceleration is a legal warning sent when a borrower takes out a second mortgage without the primary lender's consent. This violates the due-on-sale clause, allowing the lender to demand immediate full repayment of the loan balance. To avoid foreclosure, homeowners must either pay the debt in full or resolve the breach by terminating the unauthorized junior lien. Timely communication with the servicer is critical to preventing legal action and protecting your property equity from liquidation.

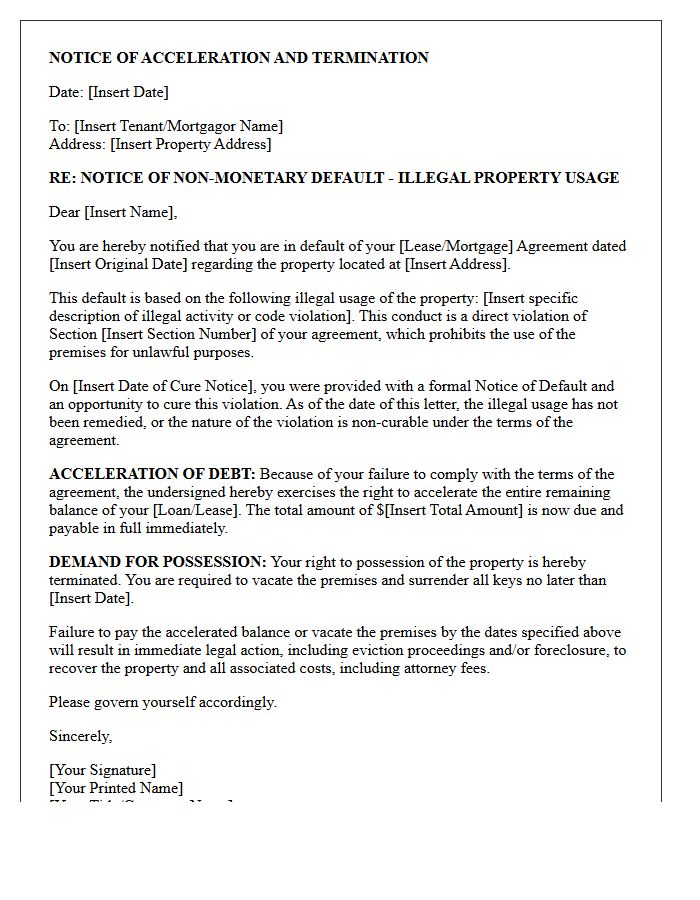

Illegal Property Usage Non-Monetary Default Acceleration Letter

An Illegal Property Usage Non-Monetary Default Acceleration Letter is a formal legal notice issued when a tenant or owner violates zoning laws, safety codes, or lease restrictions. Unlike financial arrears, this breach involves unauthorized activities like commercial operations in residential zones or criminal conduct. If the violation is not cured within the specified timeframe, the lender or landlord can accelerate the debt, demanding immediate full payment or initiating eviction. This document serves as critical evidence that the agreement was breached, justifying the termination of the contract due to non-compliance with usage covenants.

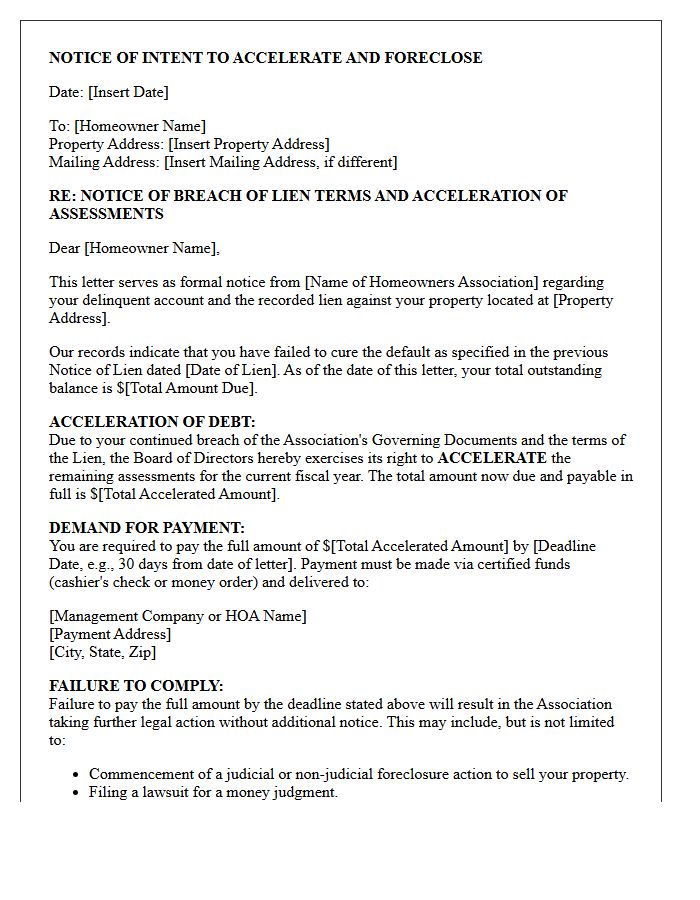

Homeowners Association Lien Breach Acceleration Letter

A Homeowners Association Lien Breach Acceleration Letter is a formal legal notice issued when a homeowner fails to pay assessments. This document signifies the foreclosure process initiation by demanding the immediate payment of the entire outstanding balance. The acceleration clause allows the HOA to declare all future periodic dues for the fiscal year due instantly. Receiving this letter means the association may soon place a lien on the property title, potentially leading to a forced sale to recover debts, making urgent legal or financial response critical to protect homeownership.

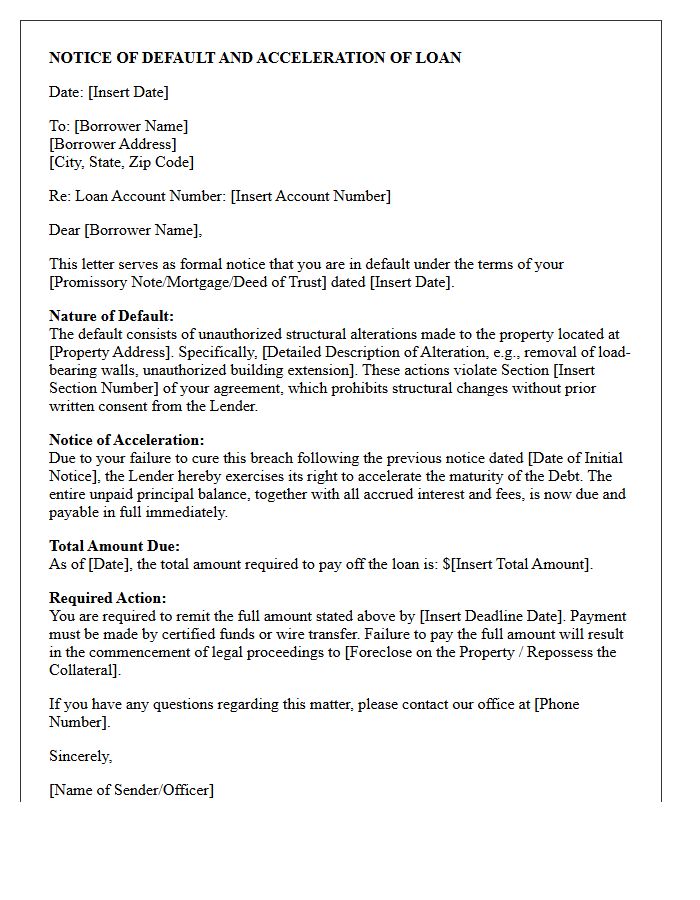

Unauthorized Structural Alteration Default Acceleration Letter

An Unauthorized Structural Alteration Default Acceleration Letter is a formal legal notice issued by a lender when a borrower modifies a property without prior written consent. This document warns that violating loan covenants regarding property integrity can trigger a default. If the alterations are not rectified or approved within the specified timeframe, the lender may exercise the acceleration clause. This action demands immediate full repayment of the remaining mortgage balance, potentially leading to foreclosure proceedings to protect the lender's collateral value and security interest.

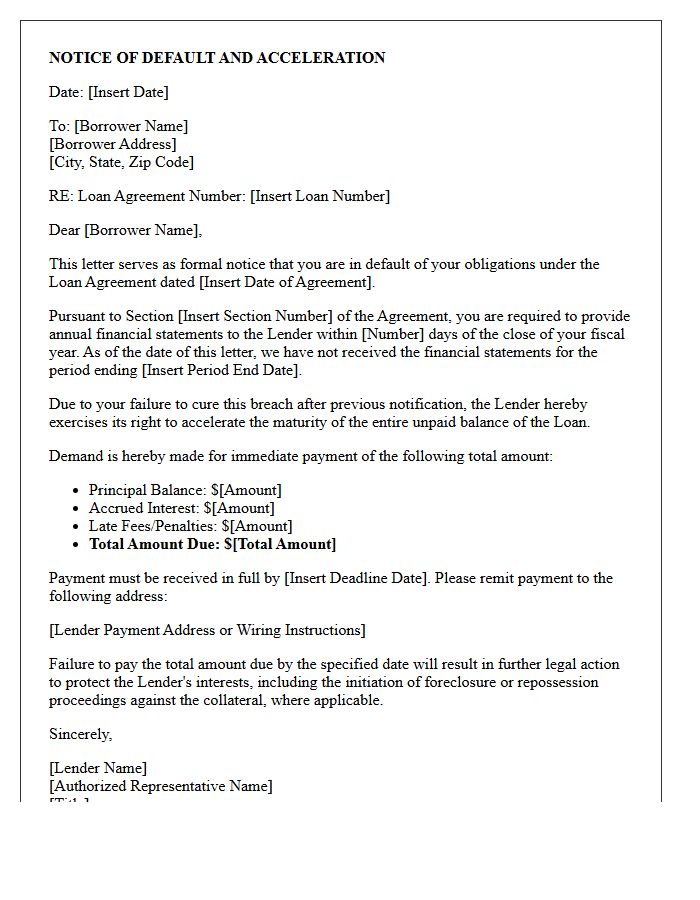

Failure To Provide Financial Statements Acceleration Letter

A Failure To Provide Financial Statements Acceleration Letter is a formal legal notice issued by a lender when a borrower breaches reporting covenants. This document warns that failing to submit required financial disclosures allows the creditor to accelerate the debt, making the entire outstanding balance due immediately. It serves as a final opportunity to cure the default before the lender pursues foreclosure or liquidation. Maintaining transparent communication and meeting reporting deadlines are critical to preventing loan default and protecting your business's credit standing and operational stability.

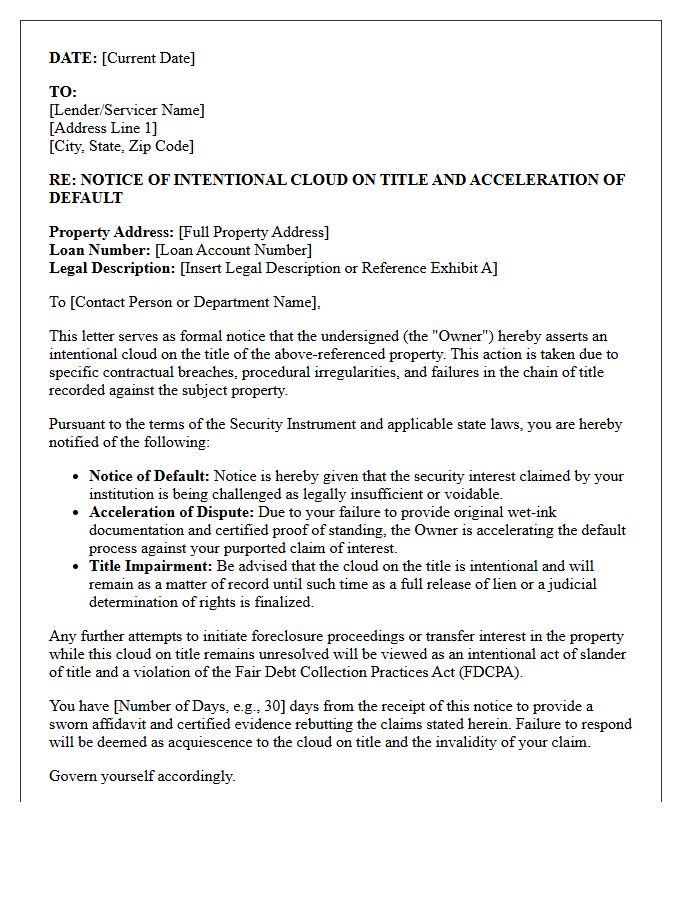

Intentional Cloud On Title Default Acceleration Letter

An Intentional Cloud on Title occurs when a Default Acceleration Letter is strategically issued to trigger a legal dispute regarding property ownership. This document notifies the borrower that the full loan balance is due immediately following a breach of contract. By formalizing the default, lenders create a public record that prevents the owner from selling or refinancing without resolving the debt. Understanding this process is critical because it solidifies the lender's priority claim, effectively blocking clear title transfer until the underlying foreclosure proceedings or payment demands are satisfied.

Violation Of Non-Monetary Mortgage Covenants Acceleration Letter

A violation of non-monetary mortgage covenants occurs when a borrower breaches loan terms unrelated to payments, such as failing to maintain property insurance or neglecting essential repairs. When these conditions are unmet, the lender issues an acceleration letter. This formal notice declares the entire loan balance due immediately. Failure to cure the specific default within the provided timeframe allows the lender to initiate foreclosure proceedings. Understanding this letter is critical, as it signifies that technical non-compliance can trigger the total loss of the property, regardless of your payment history.

What is a Non-Monetary Default Acceleration Notice?

A Non-Monetary Default Acceleration Notice is a formal legal notification from a lender to a borrower stating that the entire loan balance is due immediately because of a breach of contract terms not related to payments, such as failure to maintain insurance or unauthorized property transfers.

Can a lender accelerate a loan for reasons other than missing payments?

Yes, lenders can trigger acceleration through non-monetary defaults if the borrower violates specific loan covenants, including failure to pay property taxes, committing waste on the property, or providing false information on the original credit application.

What should I do if I receive a notice of acceleration for a non-monetary breach?

Upon receiving the notice, you should immediately review your loan agreement to verify the alleged breach, consult with legal counsel, and determine if the contract provides a "cure period" to rectify the specific violation before the acceleration becomes irreversible.

How does a non-monetary default differ from a monetary default?

A monetary default occurs specifically when a borrower fails to make scheduled principal or interest payments, whereas a non-monetary default involves the violation of "technical" covenants or obligations intended to protect the lender's collateral and risk profile.

Is it possible to reverse a Non-Monetary Default Acceleration Notice?

Reversing the acceleration typically requires "curing" the default-such as obtaining the required insurance or paying delinquent taxes-within the timeframe specified in the notice of intent, or successfully negotiating a waiver or forbearance agreement with the lender.

Comments