Receiving a Veterans Affairs Loan Notice of Intent to Accelerate is a critical warning that your mortgage holder plans to demand full repayment due to default. This formal notice is a final step before foreclosure proceedings begin for eligible service members. Understanding your options for reinstatement or loss mitigation is essential to saving your home. Below are some ready to use template.

Image cover: VA Loan Notice of Intent to Accelerate: Essential Templates and Compliance Guide

Letter Samples List

- Mortgage Lender Official Letterhead

- Issuance Date Of The Letter

- Borrower Mailing Address For Letter

- Veterans Affairs Loan Number Letter Reference

- Subject Property Address Of Letter

- Statement Of Default In Letter

- Total Past Due Amount Letter Notice

- Thirty Day Cure Deadline Letter Directive

- Intent To Accelerate Loan Letter Declaration

- Foreclosure Action Warning Letter Clause

- Servicemembers Civil Relief Act Letter Disclosure

- Veterans Affairs Financial Counseling Letter Recommendation

- Loss Mitigation Options Letter Enclosure

- Mortgage Servicer Contact Letter Information

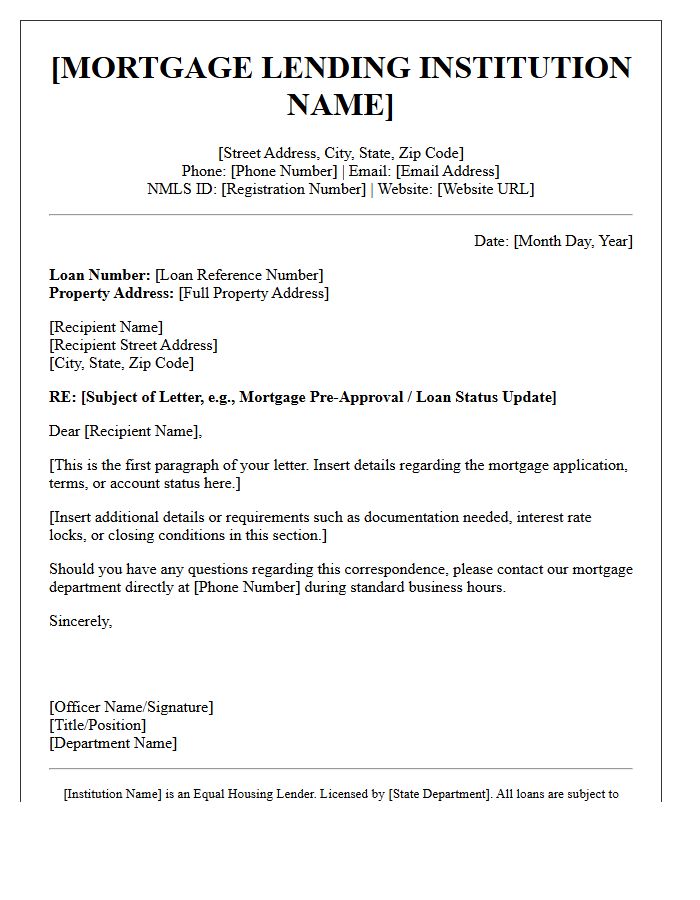

Mortgage Lender Official Letterhead

A Mortgage Lender Official Letterhead serves as essential proof of institutional authenticity for legal and financial documents. It must display the lender's full corporate name, registered address, and contact information. For borrowers, a Pre-Approval Letter on formal letterhead is critical when making real estate offers, as it verifies financial backing to sellers. Key identifiers like the NMLS number or corporate logo ensure the document is legitimate and binding. Always verify that mortgage statements and formal commitments feature these standardized details to prevent fraud and ensure smooth underwriting processes.

Issuance Date Of The Letter

The issuance date of a letter is the formal record of when the document was officially generated and released. It serves as the legal effective date for timelines, deadlines, and notification periods. This date is critical for compliance and tracking validity in administrative or legal proceedings. Always ensure this date is accurate, as it establishes the chronological baseline for all subsequent actions or responses required by the recipient.

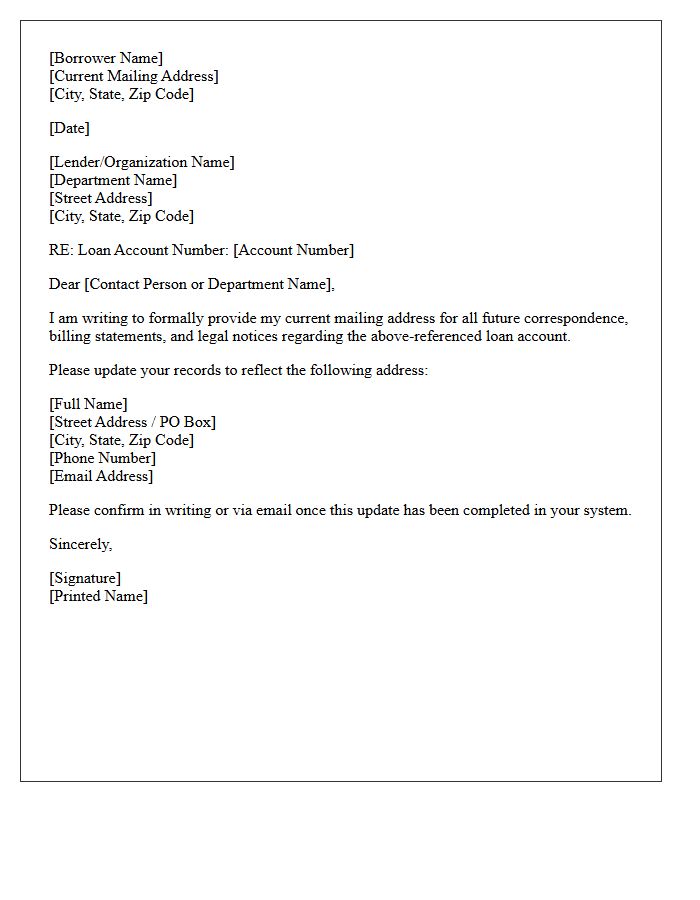

Borrower Mailing Address For Letter

The borrower mailing address is the verified location where a lender sends official legal notices, statements, and compliance letters. Ensuring this information is accurate is critical to prevent missed payment deadlines or a loss of rights during the loan term. Borrowers must provide a physical or postal address where they can reliably receive written correspondence. If you move, you must immediately update your contact details with the financial institution to ensure delivery confirmation and maintain continuous communication regarding your debt obligations and account status.

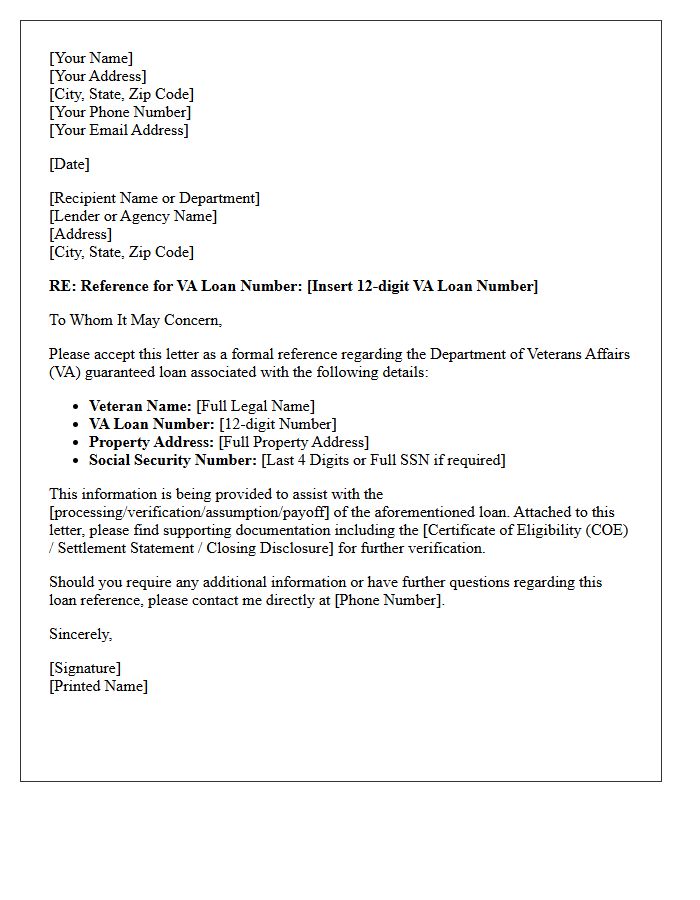

Veterans Affairs Loan Number Letter Reference

A Veterans Affairs Loan Number Letter Reference is a critical document used to identify your specific VA loan case. This unique twelve-digit identifier connects your Certificate of Eligibility to your mortgage application, allowing lenders to access the VA portal. It is essential for verifying your entitlement status and processing the funding fee. Keep this reference letter accessible, as it serves as the primary tracking tool for the Department of Veterans Affairs throughout your home buying or refinancing journey.

Subject Property Address Of Letter

The Subject Property Address is the most critical identifier in a real estate or legal letter, ensuring all parties correctly recognize the physical location under discussion. It must be accurate and complete, including the street number, name, unit, city, and zip code to prevent legal ambiguities or processing delays. Providing a precise address maintains clear communication and ensures the document is correctly filed against the intended real estate asset in official records or contractual agreements.

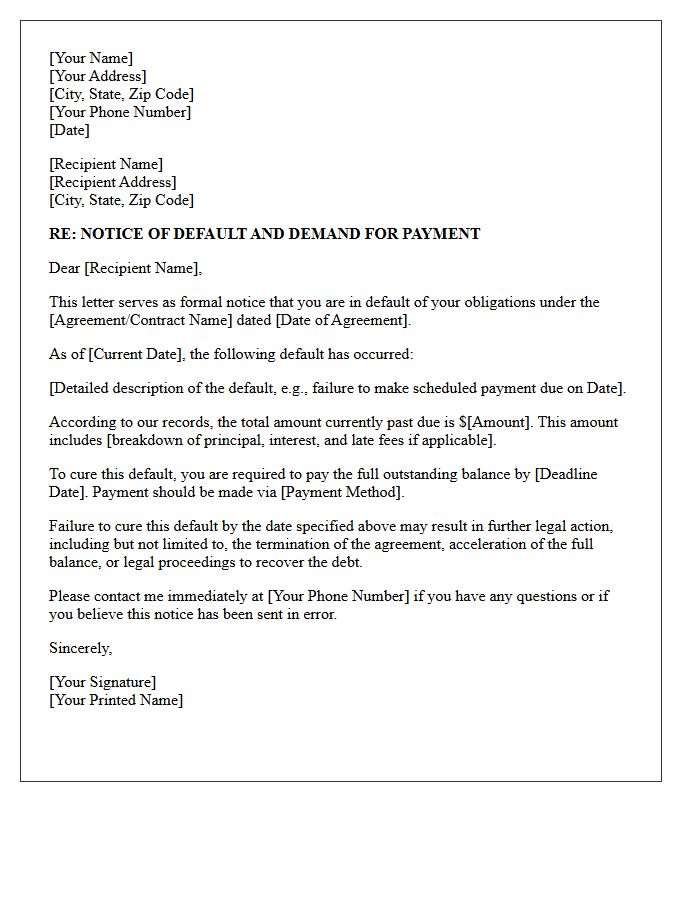

Statement Of Default In Letter

A Statement of Default is a formal legal notification issued when a borrower fails to fulfill contractual obligations. This document explicitly outlines the specific breach of contract, such as missed payments or late fees. It serves as a mandatory precursor to further legal action or foreclosure. Receiving this letter is critical because it initiates a grace period for the debtor to cure the default. Ignoring this notice can lead to severe consequences, including asset repossession, accelerated debt repayment demands, and significant damage to your long-term credit rating.

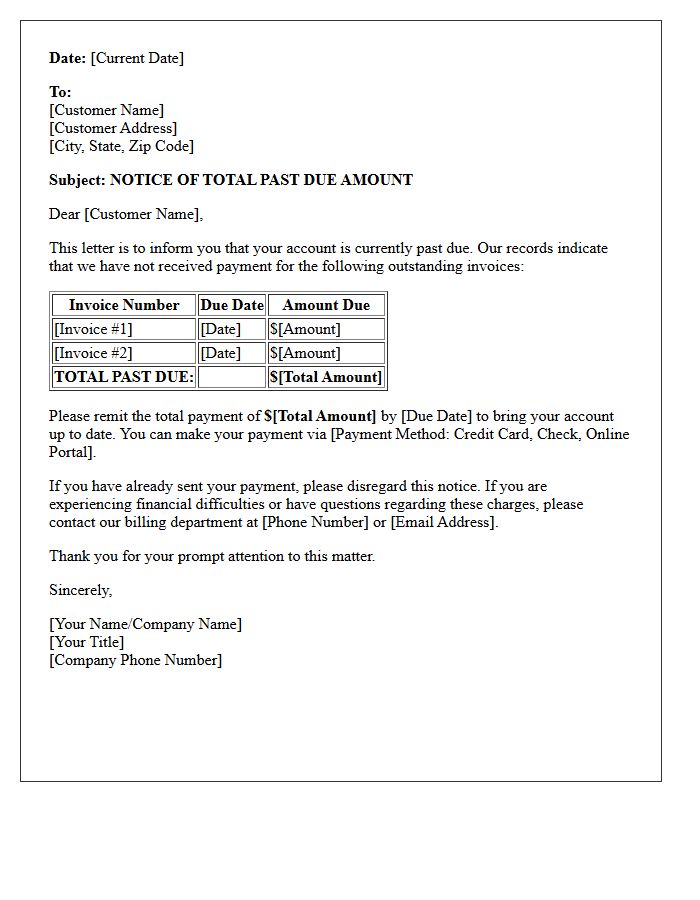

Total Past Due Amount Letter Notice

A Total Past Due Amount Letter Notice serves as a formal demand for payment regarding overdue balances. It outlines the outstanding debt, including any accumulated late fees or interest charges. Receiving this notice is a critical warning to settle obligations before the account is referred to a collection agency or impacts your credit score. To resolve the issue, verify the accuracy of the listed amount and contact the creditor immediately to discuss repayment options or dispute errors. Prompt action is essential to maintain financial standing and avoid legal consequences.

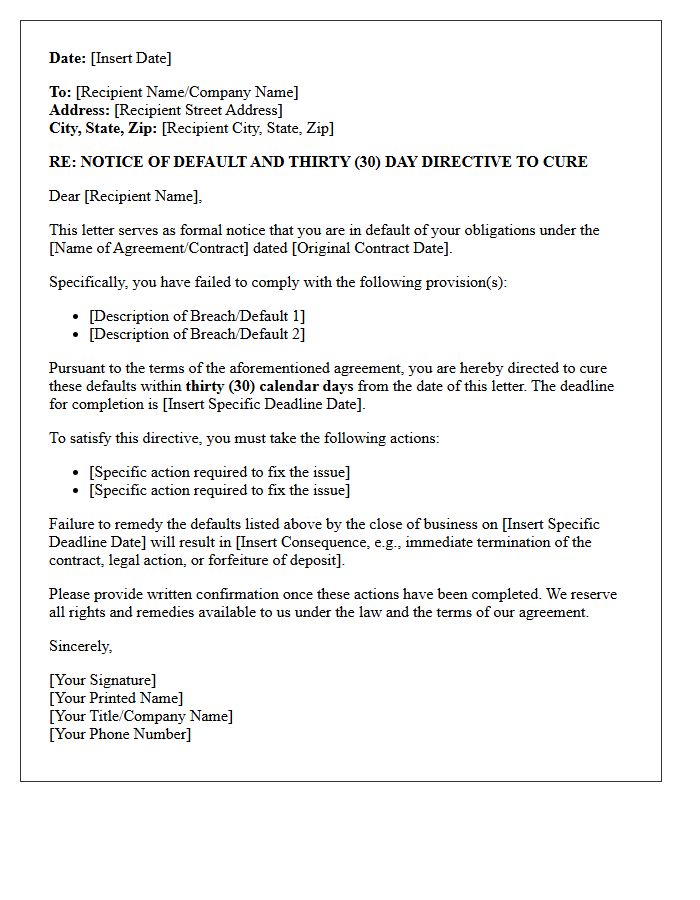

Thirty Day Cure Deadline Letter Directive

A Thirty Day Cure Deadline Letter Directive is a formal legal notice issued to a party in breach of contract. It identifies specific violations and provides a mandatory window of thirty days to rectify the issues before further legal action or contract termination occurs. This directive serves as an essential procedural safeguard, ensuring the defaulting party has a fair opportunity to resolve non-compliance. Understanding the exact deadline is critical, as failing to perform the required corrective actions within this timeframe typically results in immediate forfeiture of rights or severe financial penalties.

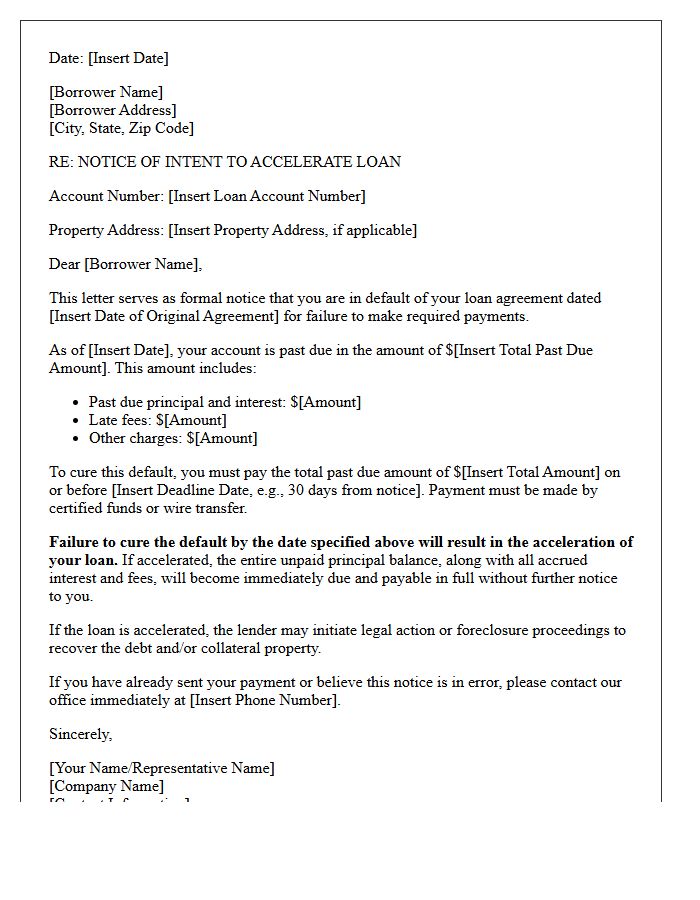

Intent To Accelerate Loan Letter Declaration

An Intent to Accelerate is a formal legal notice sent by a lender warning a borrower that their full loan balance will become due immediately if a default is not cured. This letter serves as a final declaration before the foreclosure or repossession process begins. It outlines the specific amount needed to reinstate the loan and provides a strict deadline for payment. Understanding this document is critical because failing to act within the specified timeframe typically results in the loss of legal protections and the acceleration of the entire debt.

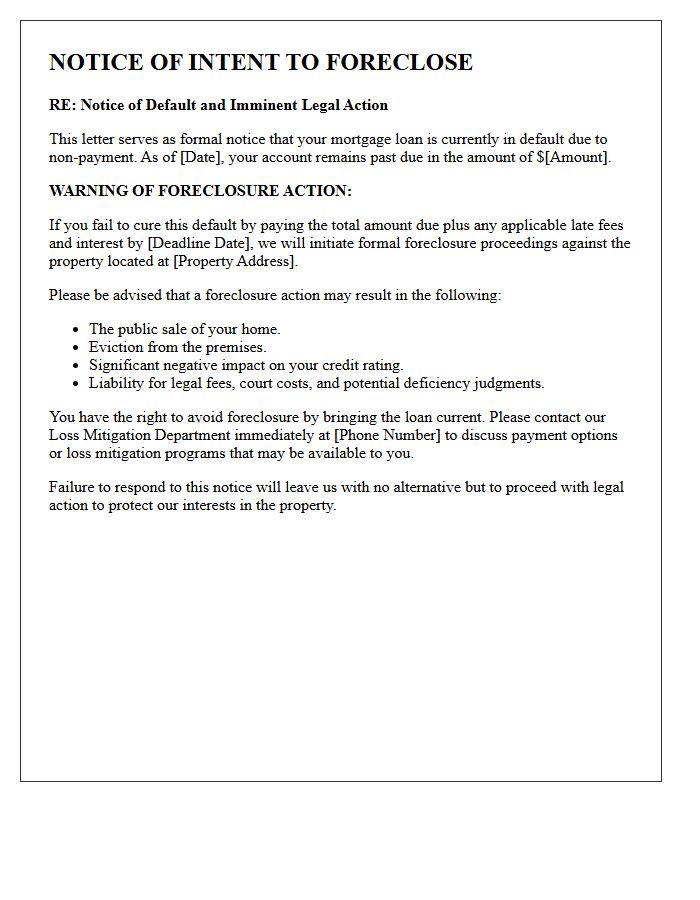

Foreclosure Action Warning Letter Clause

A foreclosure action warning letter clause is a critical legal notice sent by lenders to borrowers in default. This provision serves as a formal acceleration notice, informing the homeowner that failure to cure the delinquency within a specific timeframe will trigger a lawsuit. It outlines the total amount owed, the deadline for payment, and the borrower's right to reinstate the mortgage. Understanding this clause is essential because it represents the final opportunity to resolve debt before the foreclosure process officially begins in court, potentially leading to the loss of property ownership.

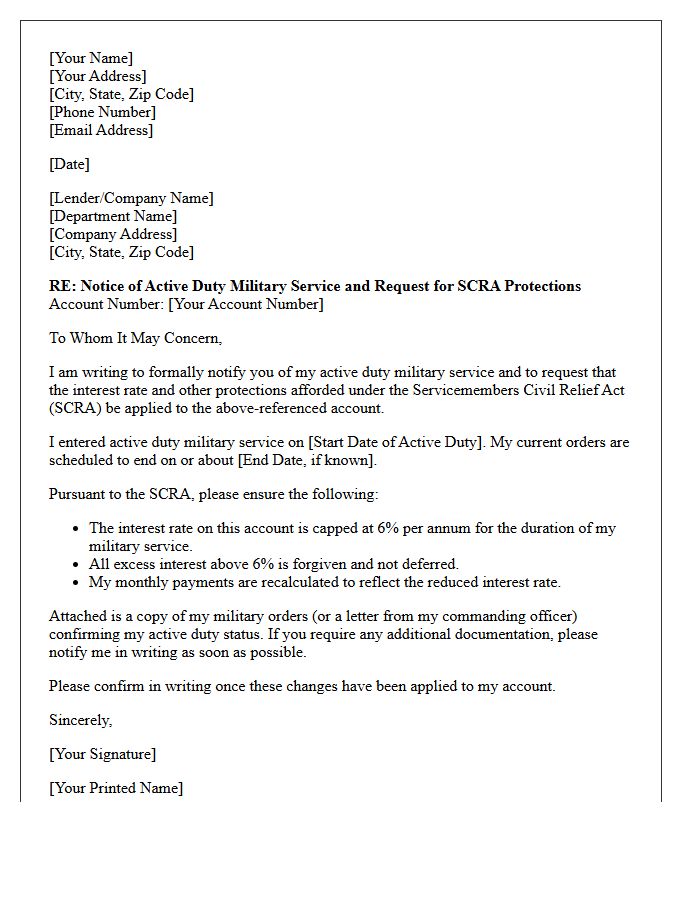

Servicemembers Civil Relief Act Letter Disclosure

The Servicemembers Civil Relief Act (SCRA) provides essential legal protections for active-duty military personnel. A disclosure letter is a formal notification used to invoke federal rights, such as interest rate caps limited to 6%, protection against eviction, and the ability to terminate residential or automobile leases early. To secure these benefits, servicemembers must provide written notice and a copy of their military orders to creditors or landlords. This disclosure ensures financial stability and prevents legal judgments while serving, reflecting the SCRA's core mission of safeguarding those on active duty from civil liabilities.

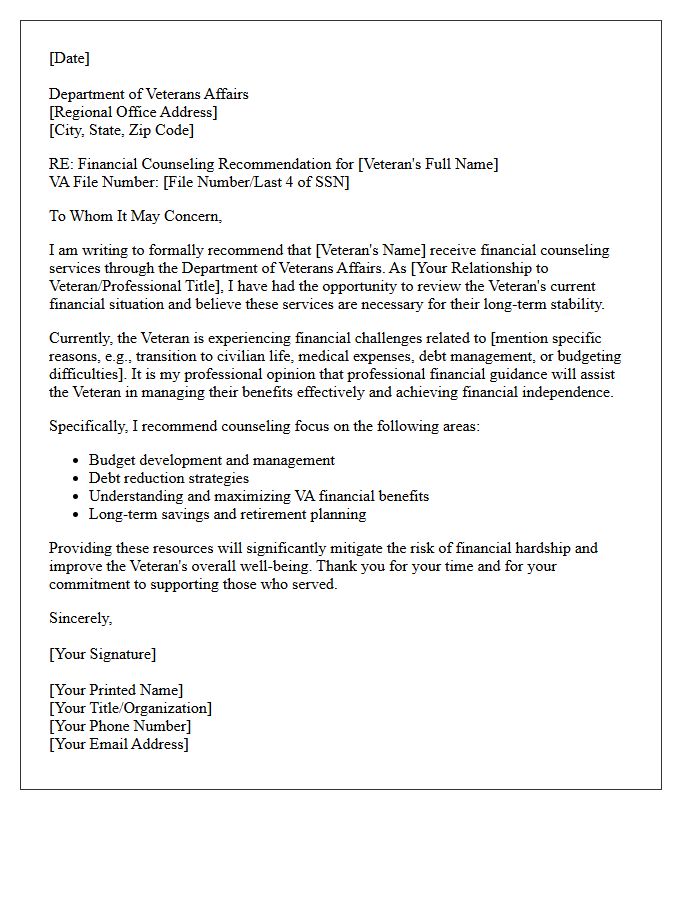

Veterans Affairs Financial Counseling Letter Recommendation

A Veterans Affairs financial counseling letter provides professional evidence regarding a claimant's ability to manage their fiduciary affairs. This documentation is critical when the VA evaluates potential incompetency status. It typically includes a clinical assessment of the veteran's financial judgment and cognitive capacity to handle benefit payments. Obtaining a strong recommendation letter from a licensed specialist can prevent the appointment of an unnecessary fiduciary, ensuring the veteran retains legal autonomy over their disability compensation and personal monetary decisions during the ratings process.

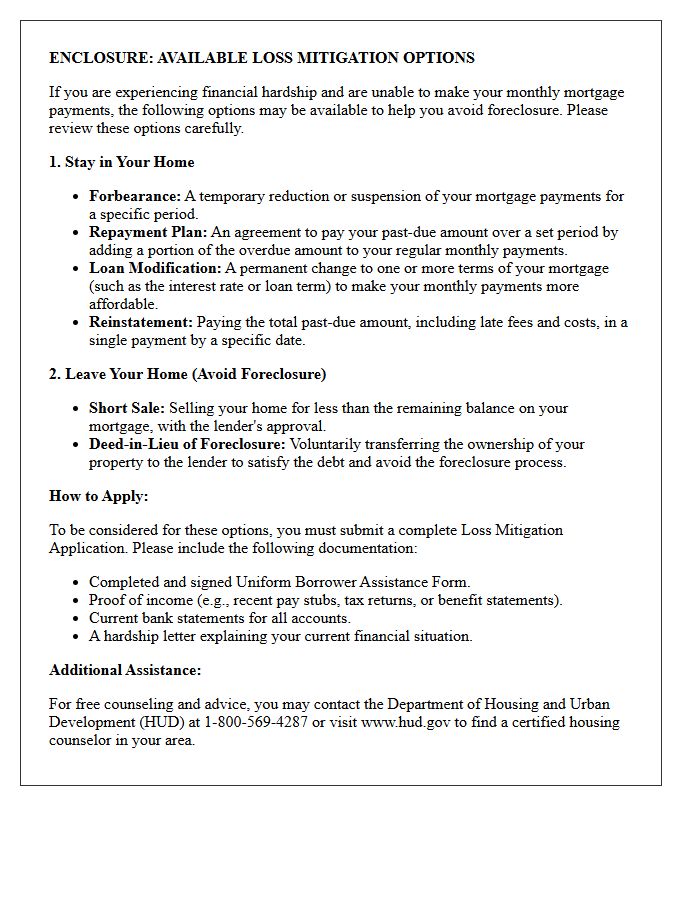

Loss Mitigation Options Letter Enclosure

A Loss Mitigation Options Letter Enclosure is a critical document sent by mortgage servicers to homeowners facing financial hardship. It outlines available foreclosure alternatives, such as loan modifications, repayment plans, or short sales. Reviewing this letter promptly is essential because it includes specific eligibility requirements and strict deadlines for submission. Understanding these options helps borrowers stabilize their housing situation and protect their credit. Always verify the required documentation listed in the enclosure to ensure a complete application and increase the chances of securing a formal loss mitigation agreement with the lender.

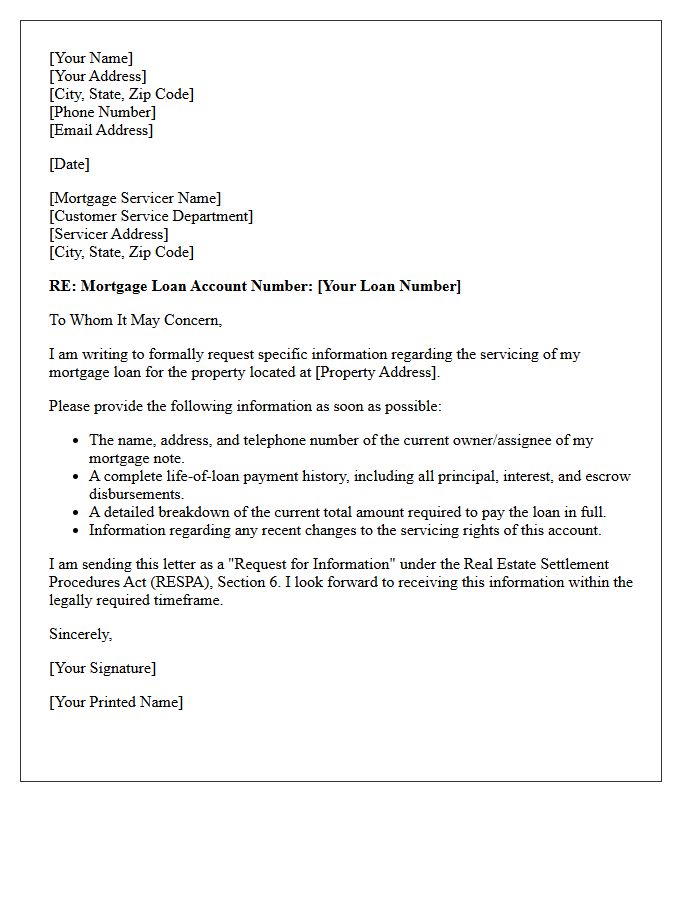

Mortgage Servicer Contact Letter Information

A mortgage servicer contact letter provides essential details about who manages your home loan. It must include the new servicer's name, their mailing address, and the specific date the transfer occurs. Key information includes the customer service phone number and instructions for sending monthly payments. Reviewing this document ensures your funds reach the correct institution, preventing late fees or credit reporting errors. Always verify that the payment amount and escrow details remain consistent during the transition to maintain financial stability and protect your home investment.

What is a VA Loan Notice of Intent to Accelerate?

A VA Loan Notice of Intent to Accelerate is a formal legal warning from your mortgage servicer stating that because you have defaulted on your payments, the lender plans to call the entire balance of the loan due immediately. This document serves as the final step before the lender officially initiates the foreclosure process.

What causes a VA loan to receive a Notice of Intent to Accelerate?

This notice is typically triggered when a borrower falls 90 days (three consecutive payments) behind on their mortgage. Under Department of Veterans Affairs guidelines, lenders must notify the borrower of their intent to accelerate the debt to provide a final window for the homeowner to cure the default or seek loss mitigation options.

Can I stop a foreclosure after receiving a VA Notice of Intent to Accelerate?

Yes, you can stop the foreclosure process by "curing" the default, which involves paying the total past-due amount including late fees and legal costs before the deadline expires. Additionally, you may avoid acceleration by qualifying for VA-specific alternatives such as a loan modification, repayment plan, or a VA Purchase of Loans (VAPOL).

How long do I have to respond to a VA Notice of Intent to Accelerate?

Typically, the notice provides a 30-day window from the date of the letter to pay the delinquent amount or reach an agreement with the servicer. If the deadline passes without action, the lender will "accelerate" the loan, meaning you can no longer simply pay the arrears to stop foreclosure; you would be required to pay the full loan balance.

Who can help me if I receive an acceleration notice on my VA loan?

Borrowers should immediately contact their mortgage servicer's loss mitigation department. Additionally, you should contact a VA Loan Technician at the nearest Regional Loan Center (RLC) by calling 877-827-3702. The VA provides financial counseling and can intercede with lenders to help veterans explore all available home retention options.

Comments