An Adverse Action Letter is a formal notification issued when an application is denied because a candidate or consumer failed to submit necessary paperwork. Providing clear communication ensures legal compliance and maintains transparency throughout the screening process. Understanding the specific requirements for these notices is essential for professional documentation. Below are some ready to use templates.

Image cover: Professional Adverse Action Letter Templates for Missing Documentation

Letter Samples List

- Adverse Action Letter for Missing Income Verification

- Notice of Adverse Action Letter for Incomplete Tax Returns

- Mortgage Denial Adverse Action Letter for Unprovided Bank Statements

- Failure to Provide Appraisal Documentation Adverse Action Letter

- Incomplete Application Adverse Action Letter for Missing W-2 Forms

- Adverse Action Letter for Failure to Submit Proof of Insurance

- Missing Proof of Earnest Money Adverse Action Letter

- Adverse Action Letter for Unsupplied Identification Documents

- Failure to Provide Gift Funds Documentation Adverse Action Letter

- Mortgage Adverse Action Letter for Missing Title Disclosures

- Adverse Action Letter for Incomplete Employment Verification

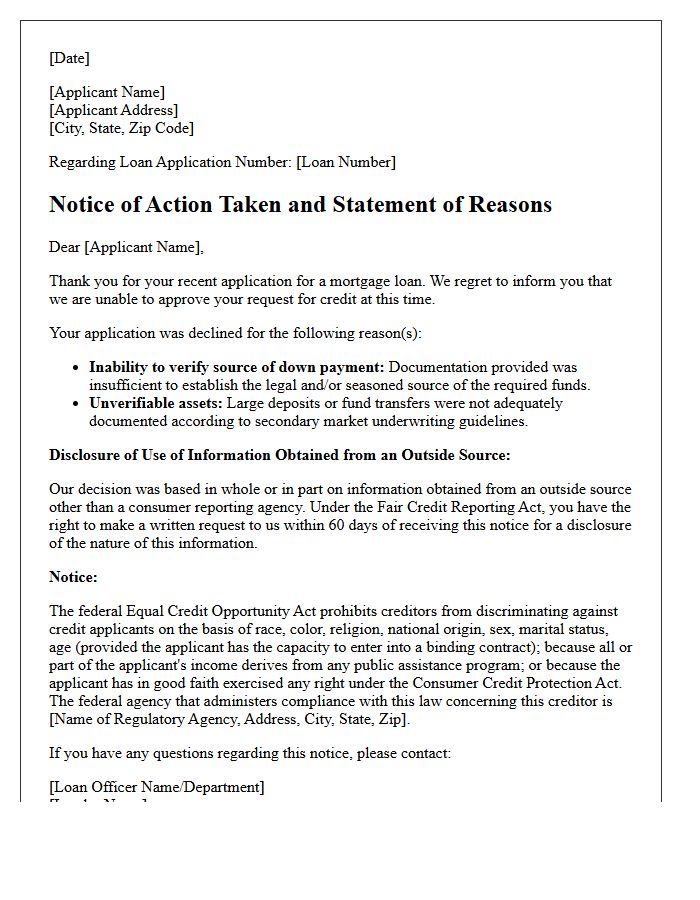

- Unprovided Down Payment Sourcing Adverse Action Letter

- Adverse Action Letter for Failure to Provide Credit Letter of Explanation

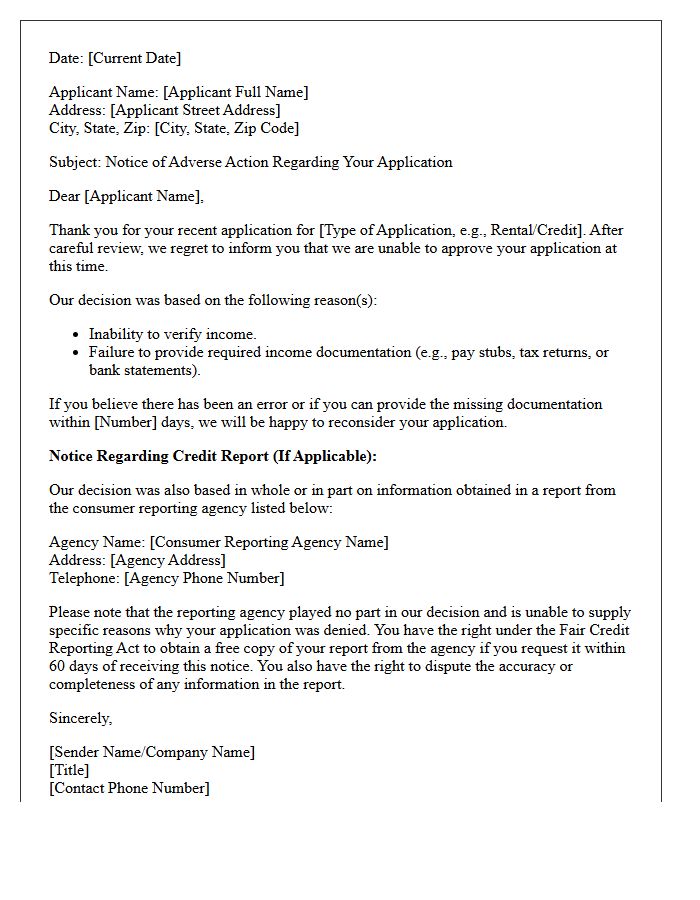

Adverse Action Letter for Missing Income Verification

An Adverse Action Letter is a formal notice sent to applicants when a credit or rental application is denied due to incomplete documentation. If you fail to provide proof of earnings, the lender cannot verify your ability to repay, leading to a denial based on missing income verification. Under the Fair Credit Reporting Act, this letter must clearly state the specific reasons for the decision and provide contact information for the reporting agency used. It is a legal requirement that ensures transparency while allowing you to rectify documentation errors or dispute inaccuracies.

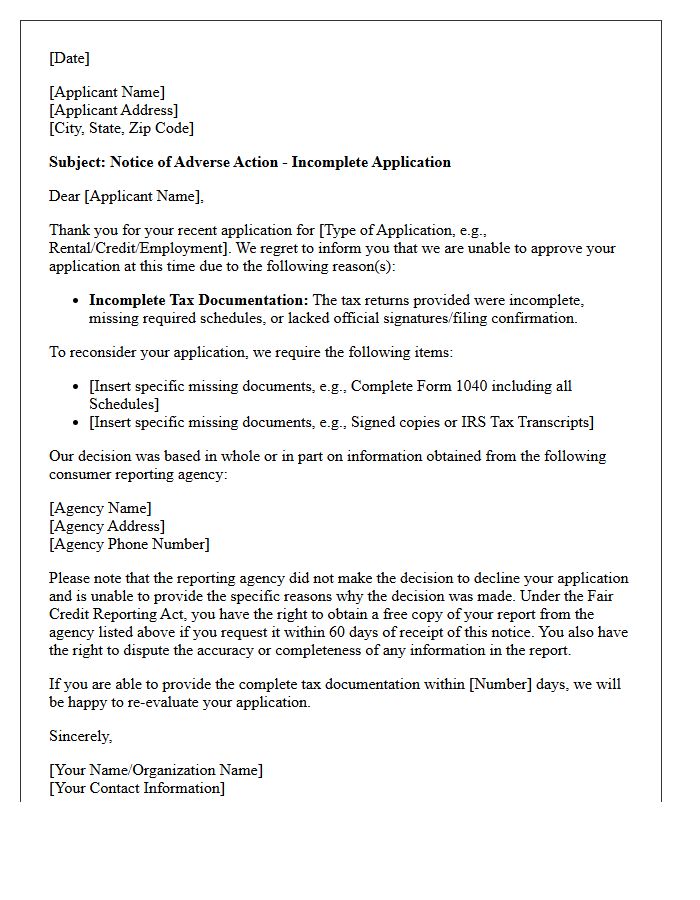

Notice of Adverse Action Letter for Incomplete Tax Returns

A Notice of Adverse Action for incomplete tax returns is a formal notification that your credit or loan application cannot be approved due to missing financial documentation. Lenders require full tax records to verify income and assess repayment capacity. Receiving this letter means the underwriting process is paused or denied because the information provided was insufficient. To resolve this, you must submit the missing schedules or signed forms promptly. Failure to provide a complete tax filing prevents the creditor from making a favorable lending decision based on your true financial standing.

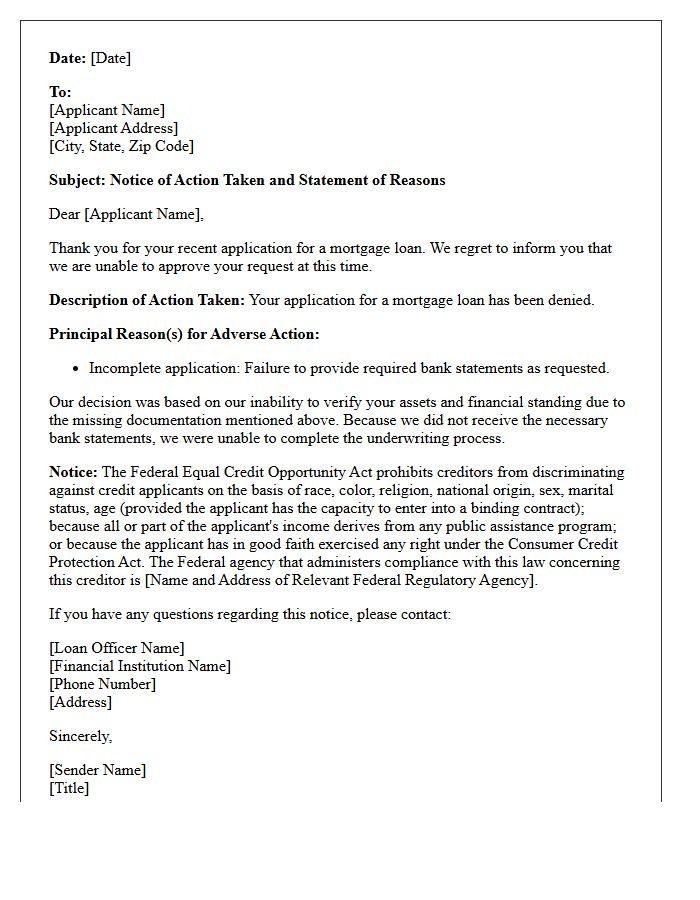

Mortgage Denial Adverse Action Letter for Unprovided Bank Statements

If you receive a mortgage denial adverse action letter citing missing bank statements, it means the lender could not verify your financial liquidity or assets. Federal law requires this formal notice to explain why your application was rejected. To resolve this, you must provide complete, multi-page documents showing all transaction histories. Failure to submit these records prevents lenders from conducting mandatory risk assessments and debt-to-income calculations. Review the letter carefully to identify the specific missing periods and resubmit the requested documentation promptly to reconsider your loan eligibility.

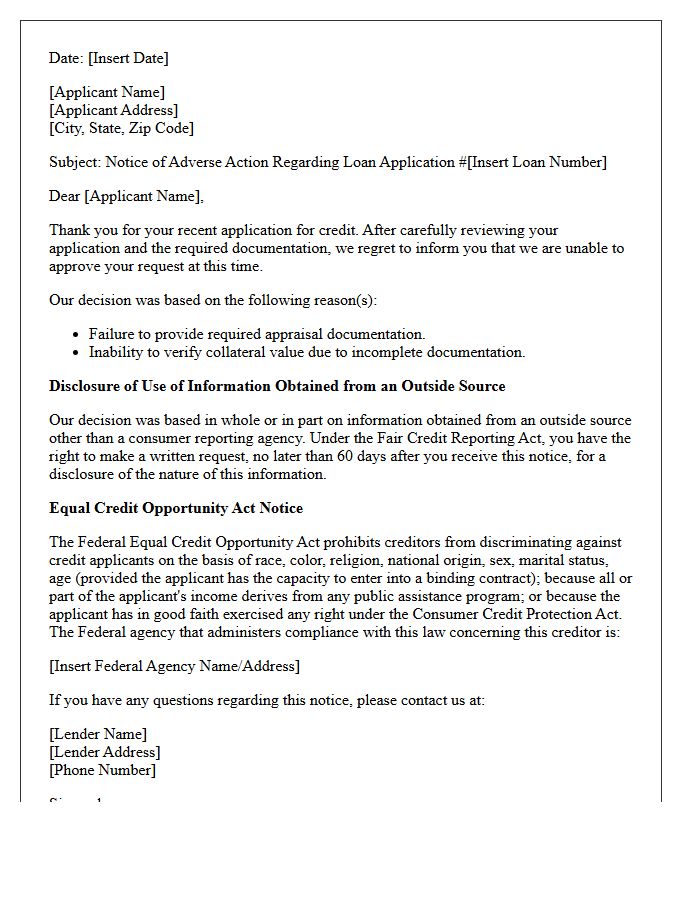

Failure to Provide Appraisal Documentation Adverse Action Letter

Under the Equal Credit Opportunity Act (ECOA), lenders must provide a notice of right to receive a copy of all written appraisals. If a loan is denied or an application is withdrawn, a Failure to Provide Appraisal Documentation Adverse Action Letter informs the applicant of the specific reasons for the credit decision. This ensures transparency and regulatory compliance. Borrowers must receive copies of valuations promptly, typically no later than three days before closing. Failure to deliver these documents or the required notice can lead to significant legal penalties and compliance violations for financial institutions.

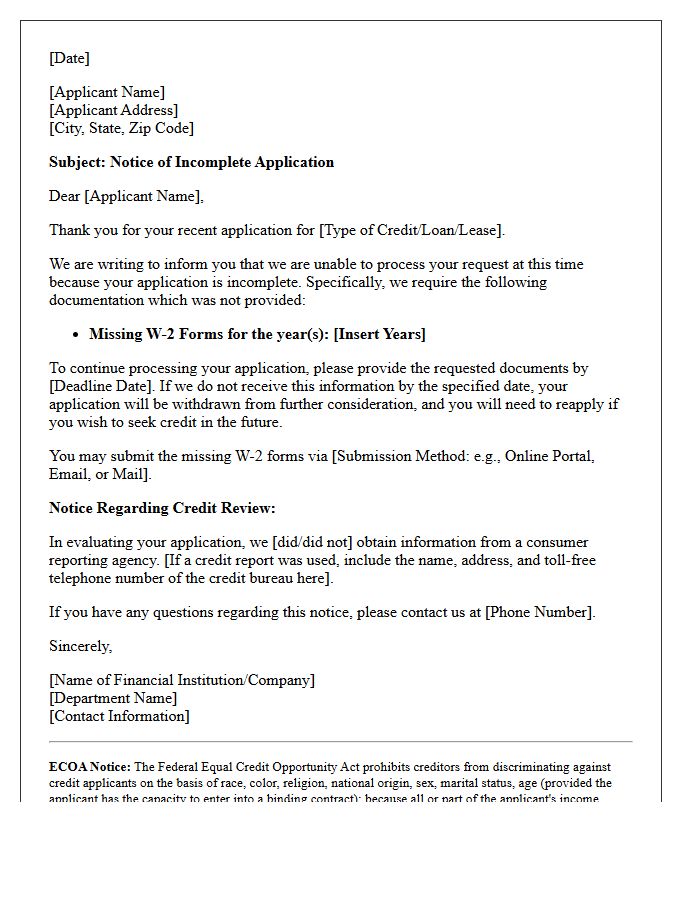

Incomplete Application Adverse Action Letter for Missing W-2 Forms

When a mortgage or credit application is paused due to missing tax documentation, lenders issue an Incomplete Application Adverse Action Letter. This formal notice specifies that missing W-2 forms prevent a final credit decision. To avoid a formal denial, applicants must provide the requested earnings statements within the stated notice period. Under the Equal Credit Opportunity Act (ECOA), this letter protects consumers by clearly identifying the required information. Timely submission of these forms is essential to reactivate the underwriting process and secure financing approval without further delays or reapplication fees.

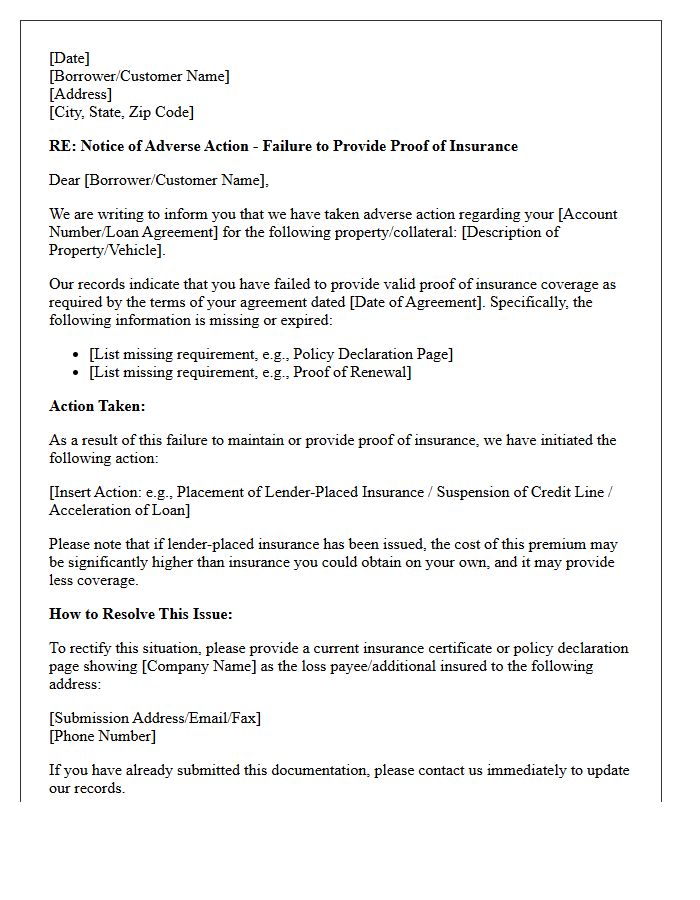

Adverse Action Letter for Failure to Submit Proof of Insurance

An Adverse Action Letter is a formal notice sent by lenders when a borrower fails to provide required proof of insurance. This document informs you that your non-compliance has triggered a negative change in your loan terms, such as the implementation of force-placed insurance. This lender-placed coverage is typically more expensive and offers less protection than private policies. To resolve this, you must immediately submit valid insurance documentation to your financial institution to avoid additional costs, potential loan default, or vehicle repossession.

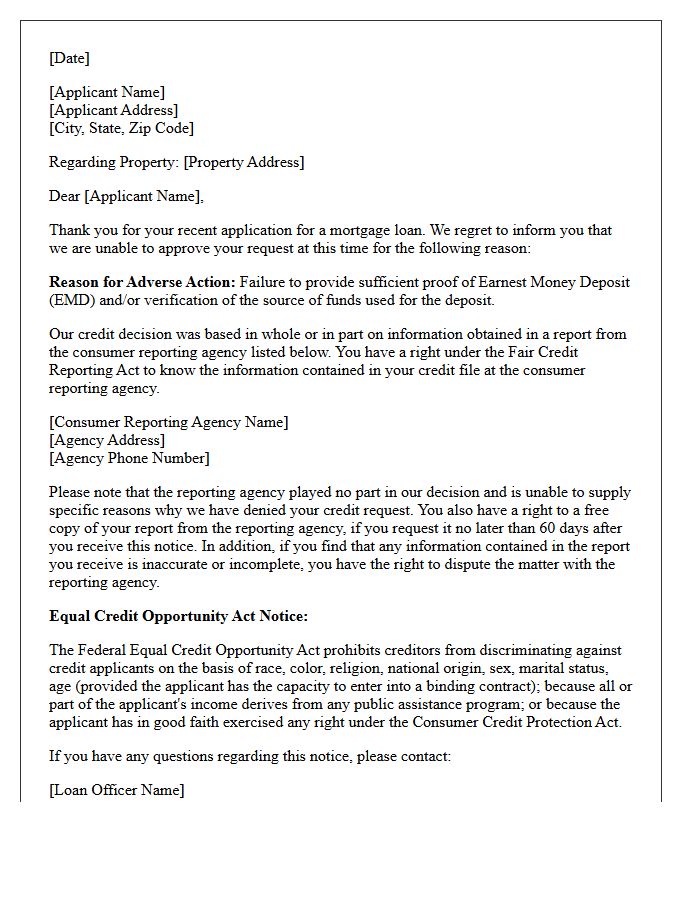

Missing Proof of Earnest Money Adverse Action Letter

A Missing Proof of Earnest Money adverse action letter is a formal notification issued when a mortgage application is denied or suspended. Lenders require verified documentation of the source of funds to comply with anti-money laundering regulations and solvency standards. If a borrower fails to provide a cleared check or bank statement showing the deposit, the loan cannot proceed. Receiving this letter means the underwriting process has halted due to insufficient financial paper trails, potentially jeopardizing the real estate transaction and the purchase agreement timelines.

Adverse Action Letter for Unsupplied Identification Documents

An Adverse Action Letter is a mandatory legal notice issued when a consumer's application is denied due to unsupplied identification documents. Under the Fair Credit Reporting Act, lenders must inform you if missing verification prevented approval. This document typically outlines the specific reasons for the denial and provides instructions on how to provide the necessary proof of identity. To protect your consumer rights, you should review the letter immediately and submit the requested KYC verification to resolve any discrepancies or potential identity theft concerns affecting your record.

Failure to Provide Gift Funds Documentation Adverse Action Letter

A Failure to Provide Gift Funds Documentation Adverse Action Letter is a formal notification issued by lenders when a mortgage application is denied. The denial occurs because the applicant failed to supply required verification, such as a gift letter or bank statements, proving that down payment assistance is a non-repayable gift. To avoid this, borrowers must ensure a clear paper trail that satisfies anti-money laundering regulations. Receiving this letter means the loan file is closed due to incomplete financial transparency regarding source of funds.

Mortgage Adverse Action Letter for Missing Title Disclosures

A mortgage adverse action letter is a formal notice issued when a lender denies or changes credit terms. Receiving one due to missing title disclosures indicates that essential documentation regarding property ownership or liens was not provided. This failure prevents the lender from verifying a clear title, which is a critical requirement for securing the loan. To resolve this, applicants must coordinate with their title company to ensure all legal disclosures are accurately filed. Promptly addressing these gaps is vital to potentially overturning the denial and proceeding with the home financing process.

Adverse Action Letter for Incomplete Employment Verification

An Adverse Action Letter is a mandatory legal notice required under the Fair Credit Reporting Act (FCRA) when an employer denies a job based on background check findings. If a candidate provides incomplete employment verification, the employer must first issue a pre-adverse notice, allowing the individual time to correct records or provide missing documentation. Failing to follow this compliance process can lead to legal penalties. This letter ensures transparency, informing the applicant of their rights to dispute inaccuracies before a final hiring decision is made.

Unprovided Down Payment Sourcing Adverse Action Letter

An Unprovided Down Payment Sourcing Adverse Action Letter is a formal notice issued when a lender denies a mortgage application due to unverified funds. Federal law requires this disclosure if the applicant fails to document the legal origin of their down payment or closing costs. This document outlines specific reasons for the rejection, such as insufficient paper trails for large deposits or non-compliant gift funds. Understanding these notices is critical for maintaining regulatory compliance and addressing financial transparency issues before reapplying for a home loan.

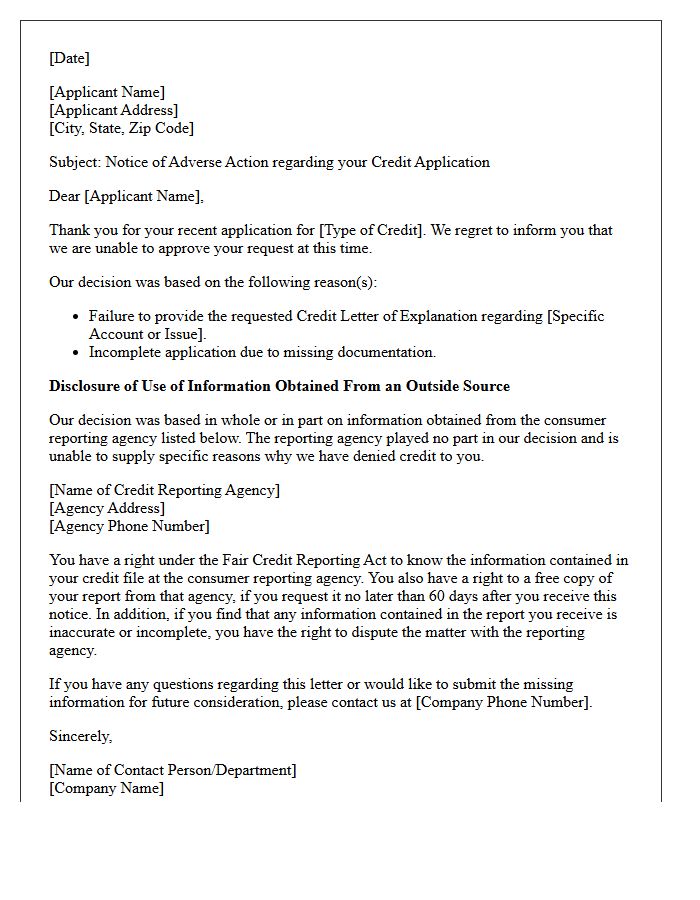

Adverse Action Letter for Failure to Provide Credit Letter of Explanation

An Adverse Action Letter is a formal notice issued when a lender denies a credit application based on information in a consumer report. If a lender requests a Letter of Explanation regarding past delinquencies or financial gaps and the applicant fails to provide it, the application may be rejected. This notice is a legal requirement under the Equal Credit Opportunity Act (ECOA). It must clearly state the specific reasons for denial, ensuring transparency and allowing the consumer to address underlying credit issues or dispute inaccuracies with the reporting bureaus.

What is an adverse action letter for failure to provide documentation?

An adverse action letter is a formal notice sent to an applicant stating that their application for credit, employment, or insurance has been denied because they failed to submit the specific documents required to complete the verification process.

Why did I receive an adverse action notice regarding missing documents?

You received this notice because the information provided in your initial application was incomplete, and the supplemental documentation requested by the reviewer was not received within the mandatory timeframe, preventing a final decision.

Can I reopen my application after receiving a denial for insufficient documentation?

In most cases, you must submit a new application; however, some institutions allow a grace period to provide the missing paperwork. You should contact the entity that issued the letter immediately to see if the file can be reopened without a new credit inquiry.

Does a denial for failure to provide documentation affect my credit score?

The denial itself does not impact your credit score. However, the hard inquiry performed during the application process may have a minor effect, and the underlying reason for the denial will be noted in the lender's internal records.

What specific documents are usually required to avoid an adverse action?

Commonly requested items include recent pay stubs, federal tax returns, proof of residency, valid government-issued identification, or social security verification to satisfy legal "Know Your Customer" (KYC) requirements.

Comments