Receiving an adverse action letter due to a low credit score can be discouraging, but it is a legal requirement under the FCRA. This document explains why your application was denied and provides details on the credit bureau used. Understanding these notices is essential for improving your financial standing. To help you respond professionally, below are some ready to use templates.

Image cover: Professional Adverse Action Notice Templates for Credit Score Denials

Letter Samples List

- Pre-Approval Mortgage Denial Adverse Action Letter for Low Credit Score

- Conventional Home Loan Adverse Action Letter Due to Low FICO Score

- Mortgage Refinance Decline Letter for Insufficient Credit Rating

- FHA Mortgage Application Adverse Action Letter for Low Credit Score

- Home Equity Line of Credit Rejection Letter Based on Credit Score

- Jumbo Mortgage Loan Adverse Action Letter for Inadequate Credit Score

- Investment Property Mortgage Denial Letter Due to Poor Credit History

- Second Mortgage Adverse Action Letter for Substandard Credit Score

- VA Home Loan Rejection Letter for Low Credit Score Qualifications

- Construction Mortgage Loan Adverse Action Letter Due to Low Credit Score

- Adjustable Rate Mortgage Decline Letter for Low Credit Score Profile

- First-Time Homebuyer Pre-Qualification Adverse Action Letter for Low Credit Score

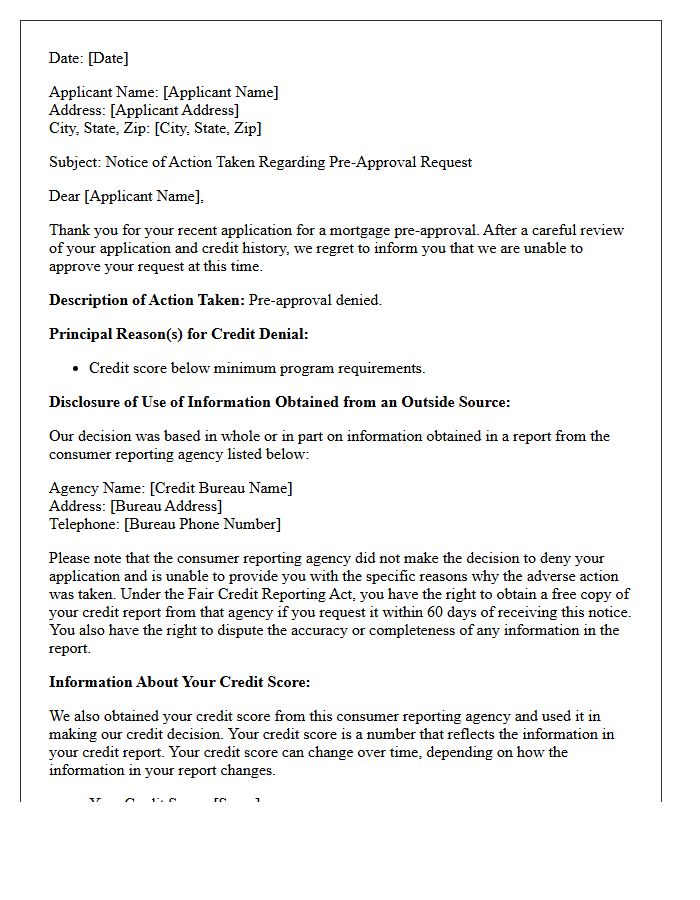

Pre-Approval Mortgage Denial Adverse Action Letter for Low Credit Score

A Pre-Approval Mortgage Denial occurs when a lender rejects your application after reviewing your financial profile. If the decision is based on a low credit score, the lender must legally provide an Adverse Action Letter. This document is crucial because it discloses the specific reasons for denial and identifies which credit bureau provided the data. Understanding these factors allows you to dispute inaccuracies or implement a strategy to improve your creditworthiness. Reviewing this letter is the first step toward correcting financial issues and securing a future home loan approval.

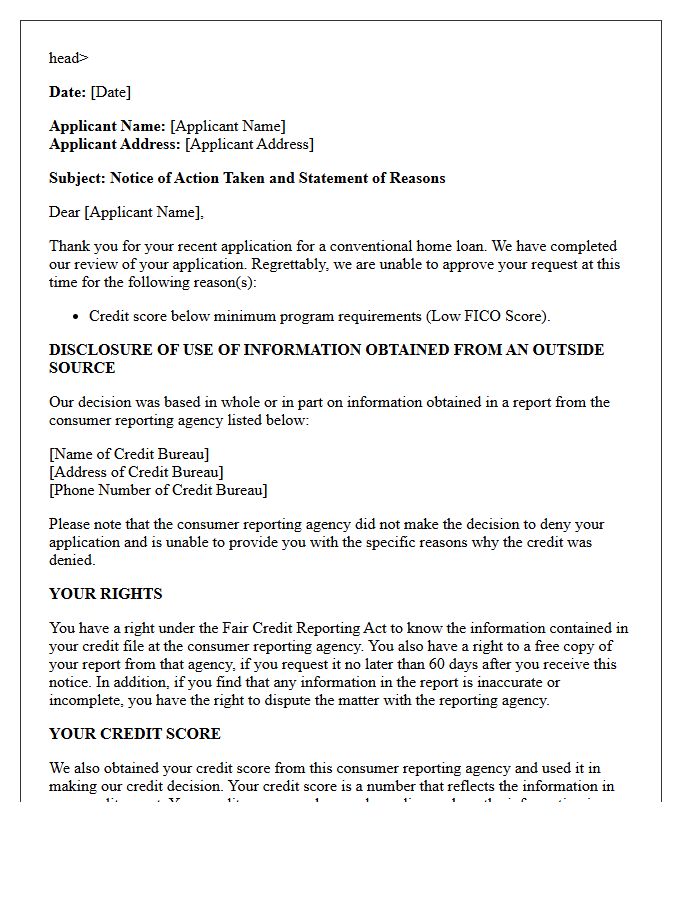

Conventional Home Loan Adverse Action Letter Due to Low FICO Score

A conventional home loan adverse action letter is a formal notice issued when a lender denies a mortgage application. Receiving this due to a low FICO score means your credit rating fell below the investor's minimum requirements or specific risk thresholds. Legally mandated by the FCRA, this letter must disclose the specific credit bureau used, the exact credit score, and the primary factors negatively impacting your eligibility. Reviewing these reasons is essential for correcting errors and improving your financial profile to secure future financing with better interest rates.

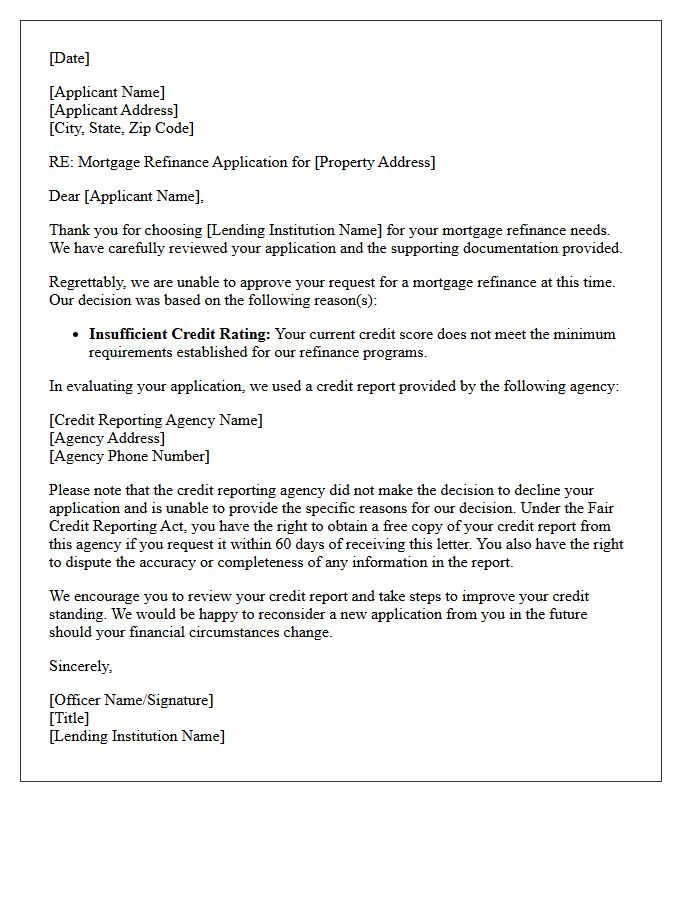

Mortgage Refinance Decline Letter for Insufficient Credit Rating

Receiving a mortgage refinance decline letter due to an insufficient credit rating means your current credit score failed to meet the lender's minimum eligibility requirements. This document identifies specific adverse action factors, such as high credit utilization or late payments, that influenced the decision. To improve future approval odds, you should request a free credit report to dispute errors and focus on debt reduction. Understanding these reasons is essential for rebuilding your financial profile before reapplying for a lower interest rate or better loan terms.

FHA Mortgage Application Adverse Action Letter for Low Credit Score

Receiving an FHA Mortgage Application Adverse Action Letter is a formal notice that your loan was denied due to a low credit score. This document is a legal requirement under the ECOA, detailing the specific reasons for rejection and identifying the credit reporting agency used. It is important to review the letter to check for inaccuracies on your profile. While FHA loans offer flexibility, lenders often impose "overlays" requiring higher scores. Use this feedback to improve your credit before reapplying to ensure you meet the necessary qualification thresholds.

Home Equity Line of Credit Rejection Letter Based on Credit Score

Receiving a Home Equity Line of Credit (HELOC) rejection letter due to a low credit score indicates that you currently fall below the lender's risk threshold. Lenders prioritize high scores to ensure repayment stability. To move forward, review the Adverse Action Notice provided, which must disclose the specific score used and the credit bureau involved. Focus on debt-to-income ratio improvements and correcting credit report errors before reapplying. Enhancing your financial profile increases your chances of securing competitive rates and future approval for leveraging your home's equity.

Jumbo Mortgage Loan Adverse Action Letter for Inadequate Credit Score

Receiving an Adverse Action Letter for a jumbo mortgage indicates your application was denied due to an inadequate credit score. Because jumbo loans exceed conforming limits and represent higher risk, lenders enforce stringent credit requirements, often requiring scores above 720. This formal notice is legally mandated by the FCRA, detailing the specific credit bureau used and your right to a free report. To improve future eligibility, focus on debt-to-income ratios and correcting report errors, as these private-market loans lack government backing and demand prime creditworthiness for approval.

Investment Property Mortgage Denial Letter Due to Poor Credit History

Receiving an investment property mortgage denial letter due to poor credit history indicates that your financial profile failed to meet lender risk standards. High debt-to-income ratios or low FICO scores suggest a greater default risk, leading to a loan rejection. To improve future outcomes, review your credit report for inaccuracies, reduce existing liabilities, and ensure consistent on-time payments. Rebuilding your creditworthiness is essential for securing favorable interest rates and professional financing for real estate ventures. Always request the specific reasons for denial to address underlying financial weaknesses effectively.

Second Mortgage Adverse Action Letter for Substandard Credit Score

A Second Mortgage Adverse Action Letter is a formal notice issued by lenders when denying a junior lien application due to a substandard credit score. Under the Equal Credit Opportunity Act, creditors must disclose the specific reasons for denial and provide the credit reporting agency's details. This document helps applicants understand how their creditworthiness impacted the decision and outlines their right to request a free credit report copy. Reviewing these notices is essential for identifying errors and improving financial standing for future lending opportunities.

VA Home Loan Rejection Letter for Low Credit Score Qualifications

Receiving a VA home loan rejection letter due to a low credit score indicates you do not currently meet the lender's minimum credit requirements. While the VA does not set a specific score, most lenders require a 620 benchmark. This letter is an Adverse Action Notice, outlining why your application was denied. To improve future chances, focus on credit repair by paying down debt and correcting report errors. Remember, a rejection is not permanent; you can reapply once your financial profile aligns with lender overlays and federal eligibility standards.

Construction Mortgage Loan Adverse Action Letter Due to Low Credit Score

A construction mortgage adverse action letter is a formal notice issued when a lender denies your loan application. When triggered by a low credit score, the document must specify the credit reporting agency used and the factors impacting your rating. This notification is required by the Equal Credit Opportunity Act to ensure transparency. Understanding these specific reasons allows borrowers to dispute inaccuracies or improve their financial standing before reapplying for construction financing. Reviewing the provided credit disclosure is essential for identifying the risk factors that led to the loan rejection.

Adjustable Rate Mortgage Decline Letter for Low Credit Score Profile

Receiving an Adjustable Rate Mortgage (ARM) decline letter signifies that your application was rejected, primarily due to a low credit score profile. Lenders view lower scores as a high default risk, especially when interest rates fluctuate. This formal notice, or adverse action letter, must disclose your specific credit score and the primary reasons for denial. To improve future eligibility, focus on credit restoration by reducing outstanding debt and correcting report errors. Strengthening your financial profile is essential to securing favorable mortgage terms and stabilizing your long-term housing costs.

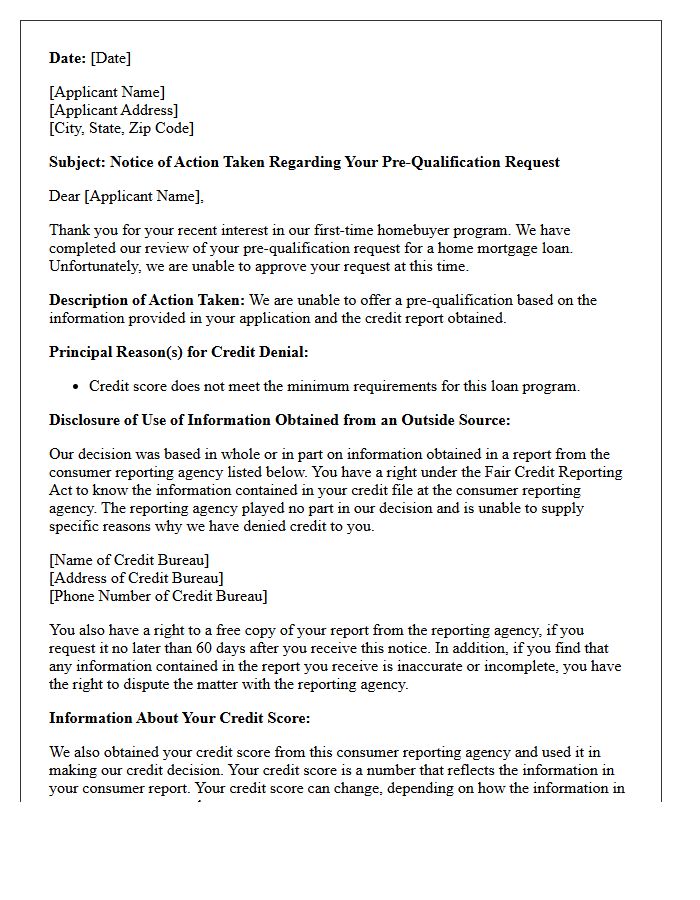

First-Time Homebuyer Pre-Qualification Adverse Action Letter for Low Credit Score

Receiving an Adverse Action Letter is a formal notice that your mortgage pre-qualification was denied due to a low credit score. Under the Equal Credit Opportunity Act, lenders must provide this document explaining why you were turned down. It typically lists the specific credit bureaus used and your numerical score. Use this feedback as a roadmap to improve your financial standing by disputing errors or paying down debt. Understanding these reasons is the first step toward building the credit profile necessary to secure a future home loan.

What is an adverse action letter for a low credit score?

An adverse action letter is a formal notice sent by a lender to inform an applicant that their request for credit, employment, or insurance has been denied or granted on less favorable terms due to information found in their credit report, such as a low credit score.

Why did I receive an adverse action notice after applying for credit?

You received this notice because the lender determined that your credit score did not meet their specific requirements for approval. Under the Fair Credit Reporting Act (FCRA), lenders must disclose if a credit score played a role in a negative lending decision.

What information must be included in a low credit score adverse action letter?

The letter must include the name and contact information of the credit bureau that provided the report, your specific credit score, the date the score was calculated, and the key factors (such as high utilization or late payments) that negatively impacted your score.

Does receiving an adverse action letter hurt my credit score?

No, the letter itself does not impact your credit score. However, the hard inquiry generated when you applied for credit may cause a temporary, slight decrease in your score, regardless of whether you were approved or denied.

How can I get a free credit report after being denied for a low score?

Following a denial, you are legally entitled to one free copy of your credit report from the bureau listed in your adverse action letter. You must request this report within 60 days of receiving the notice to review your data for errors or inaccuracies.

Comments