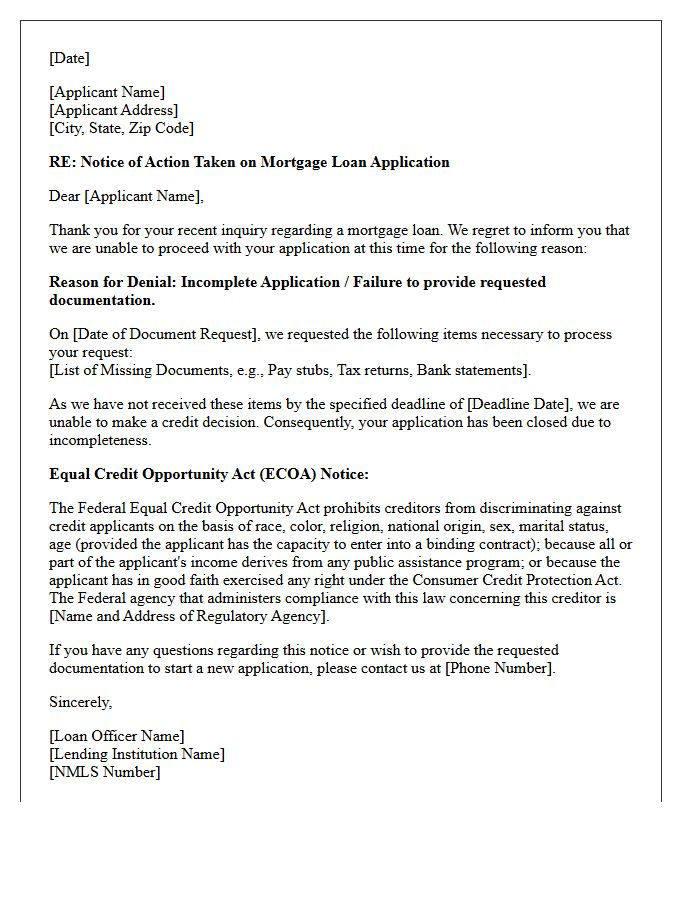

When a borrower fails to provide necessary documentation, lenders must issue an Adverse Action Letter for Incomplete Mortgage Application to comply with federal regulations. This notice informs the applicant of missing information and the resulting file closure. Understanding this compliance requirement ensures transparency and legal protection during the lending process. Below are some ready to use templates.

Image cover: Streamline Your Mortgage Denials: Professional Templates for Incomplete Applications

Letter Samples List

- Adverse Action Letter for Incomplete Mortgage Application

- Incomplete Mortgage Application Adverse Action Letter

- Notice of Adverse Action Letter for Missing Application Information

- Mortgage Denial Letter Due to Incomplete Application

- Adverse Action Letter for Unfinished Mortgage Application

- Incomplete Credit Application Adverse Action Letter

- Mortgage Lending Adverse Action Letter for Missing Documents

- Adverse Action Letter for Abandoned Mortgage Application

- Notice of Incomplete Mortgage Application Adverse Action Letter

- Adverse Action Letter for Deficient Mortgage Application

- Mortgage Loan Rejection Letter for Incomplete Application

- Incomplete Mortgage File Adverse Action Letter

- Adverse Action Letter for Unreturned Mortgage Application Documents

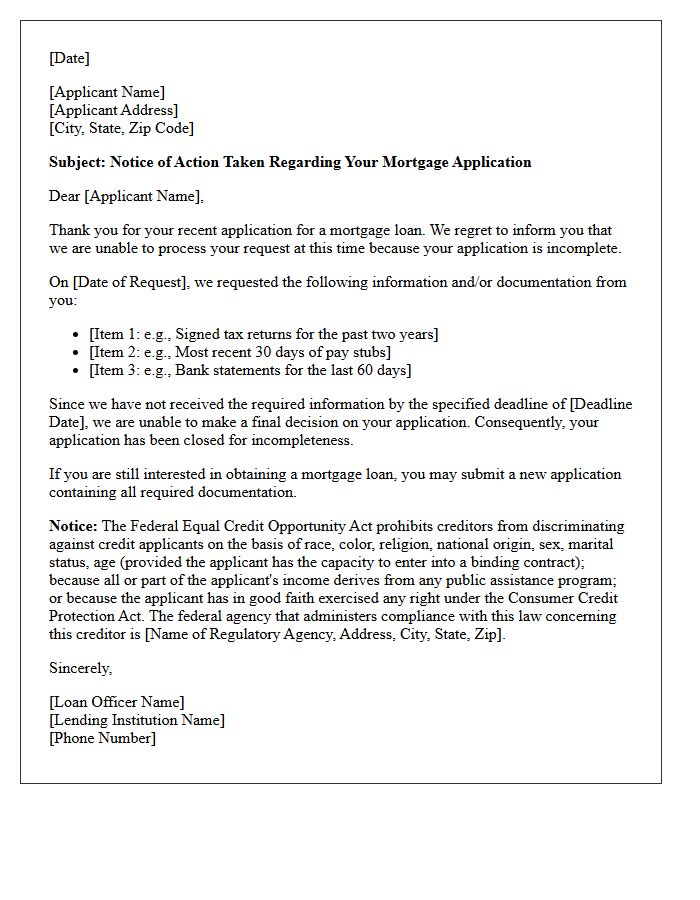

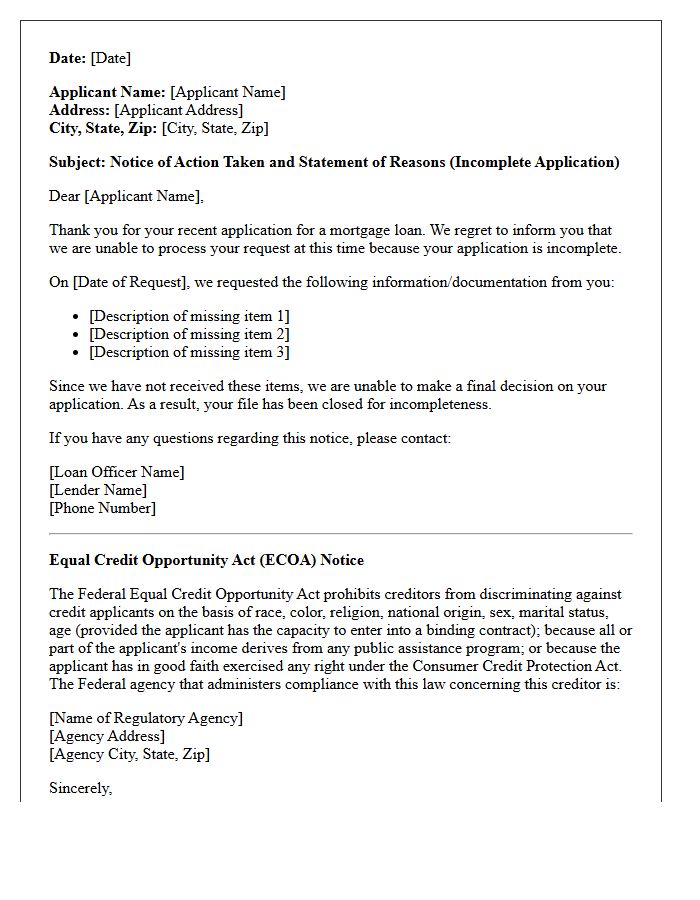

Adverse Action Letter for Incomplete Mortgage Application

When you submit an unfinished mortgage application, lenders must issue an Adverse Action Letter if they cannot proceed. Under the Equal Credit Opportunity Act, this notice informs you that your file was closed due to incompleteness. This is not necessarily a credit denial; it simply means the lender lacks specific documentation to make a decision. To resume the process, you must provide the missing information within the specified timeframe. Always review the letter carefully to identify exactly which documents are required to reactivate your home loan request promptly.

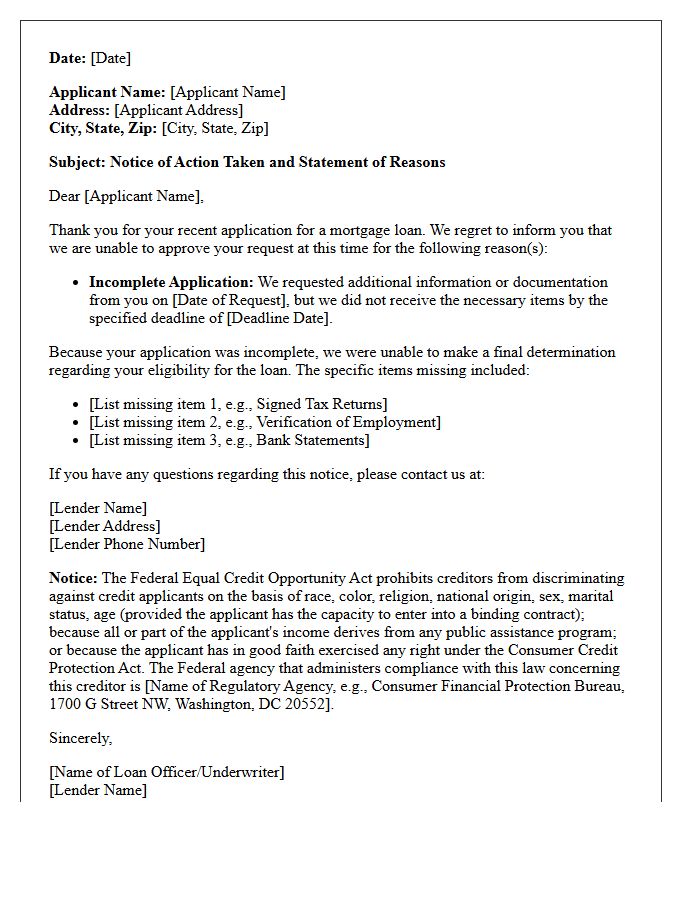

Incomplete Mortgage Application Adverse Action Letter

When a lender issues an Incomplete Mortgage Application Adverse Action Letter, it serves as a formal notification under the ECOA. This document specifies the missing information required to process your loan request. To avoid a final denial, you must provide the requested documentation by the stated deadline. This transparency ensures consumer protection and clarifies why credit cannot be granted in its current state. Receiving this notice is a critical opportunity to rectify application deficiencies and keep your home financing goals on track through timely cooperation with your loan officer.

Notice of Adverse Action Letter for Missing Application Information

A Notice of Adverse Action for missing information is a legal requirement under the Equal Credit Opportunity Act (ECOA). When a creditor cannot process your request due to incomplete data, they must issue this formal notification. It identifies the specific documentation or details needed to make a decision. Receiving this letter does not necessarily mean a final denial; however, you must provide the missing information within the specified timeframe to prevent a permanent rejection of your application. Always review the letter carefully to ensure your credit profile remains accurate.

Mortgage Denial Letter Due to Incomplete Application

Receiving a mortgage denial letter due to an incomplete application means the lender could not make a credit decision because required documentation was missing. Common omissions include unsigned forms, missing pay stubs, or incomplete tax returns. To resolve this, review the Notice of Incomplete Application, which lists the specific items needed to finalize the review. Providing these documents promptly allows the lender to reopen your file. Ensuring a complete submission is the most critical step to avoid delays and move toward securing your home loan approval.

Adverse Action Letter for Unfinished Mortgage Application

An adverse action letter for an unfinished mortgage application is a formal notice sent when a lender stops processing your file. This occurs because the application was left incomplete or required documentation was never provided. It is important to know that this notice does not necessarily mean a credit denial, but rather a file closure due to inactivity. Under the Equal Credit Opportunity Act (ECOA), lenders must inform you of the specific reasons your application could not proceed to ensure transparency in the lending process.

Incomplete Credit Application Adverse Action Letter

An Incomplete Credit Application Adverse Action Letter is a formal notice required by the ECOA when a lender cannot process a request due to missing information. Unlike a standard rejection, this letter must clearly specify the required documentation needed to complete the review. It provides the applicant with a set deadline to submit these details. If the consumer fails to respond within the timeframe, the application is closed; however, if they comply, the lender must proceed with a full credit evaluation. This process ensures transparency and regulatory compliance.

Mortgage Lending Adverse Action Letter for Missing Documents

A mortgage lending adverse action letter triggered by missing documents is a formal notification that your application cannot proceed due to incomplete information. This notice is a legal requirement under the Equal Credit Opportunity Act, ensuring transparency in the lending process. It specifies which documents were absent, such as income verification or tax returns, and provides a deadline for submission. Receiving this letter does not necessarily mean a final denial; however, failure to provide the requested files within the stated timeframe will result in a formal application withdrawal or rejection.

Adverse Action Letter for Abandoned Mortgage Application

When an applicant fails to provide required documentation, lenders issue an Adverse Action Letter to formally close the file. This notice is a regulatory requirement under the Equal Credit Opportunity Act (ECOA) to ensure transparency. It informs the borrower that the application was denied or withdrawn due to incompleteness. Receiving this letter does not necessarily impact your credit score, but it provides a legal record of the decision. Always review the notice to understand if specific missing information led to the abandoned status of your mortgage request.

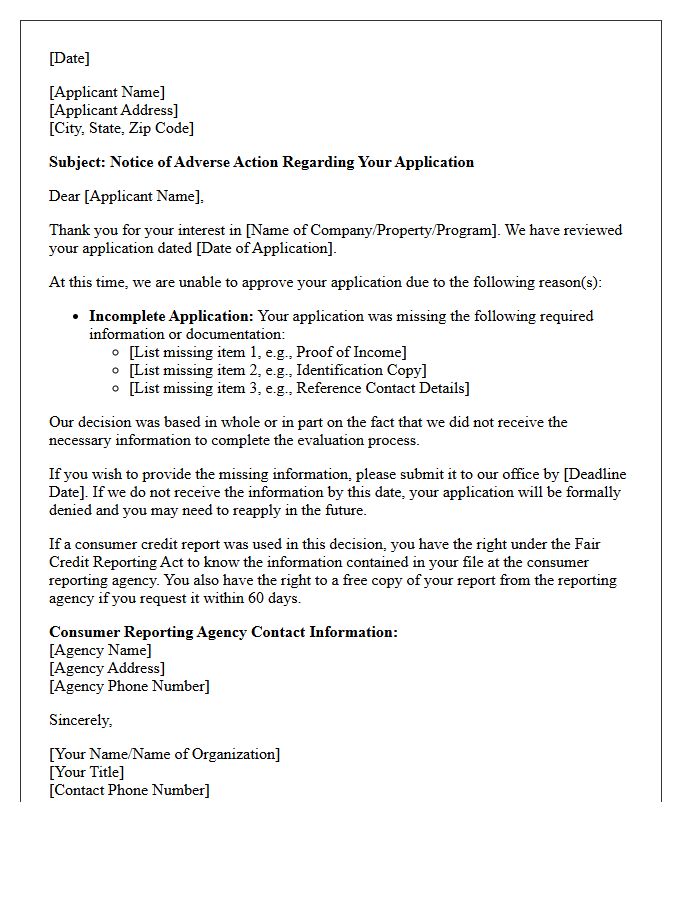

Notice of Incomplete Mortgage Application Adverse Action Letter

A Notice of Incomplete Mortgage Application is a critical disclosure sent by lenders when a file lacks necessary documentation to make a credit decision. Under the Equal Credit Opportunity Act (ECOA), lenders must provide this written notice specifying the missing items and a clear deadline for submission. If you fail to provide the requested information by the date listed, the application is typically denied for incompleteness. Promptly responding to this letter is the only way to keep your mortgage request active and avoid a formal adverse action rejection.

Adverse Action Letter for Deficient Mortgage Application

An Adverse Action Letter is a formal notice lenders must issue when denying a mortgage application. Under the Equal Credit Opportunity Act, this document explains the specific reasons for rejection, such as a low credit score or insufficient income. Receiving this letter is critical because it allows you to identify financial deficiencies and contest inaccuracies in your credit report. Reviewing these details helps you rectify issues before reapplying, ensuring you understand exactly why your application was considered deficient or high-risk according to the lender's underwriting standards.

Mortgage Loan Rejection Letter for Incomplete Application

Receiving a mortgage rejection letter for an incomplete application signifies that the lender lacked sufficient documentation to evaluate your creditworthiness. This is not a final denial based on financial failure, but a procedural stop. To resolve this, review the specific list of missing items-such as tax returns, bank statements, or employment verification-and resubmit promptly. Ensuring all required disclosures are signed and submitted is critical to restarting the underwriting process and securing your home loan approval without further delays or unnecessary credit inquiries.

Incomplete Mortgage File Adverse Action Letter

An Incomplete Mortgage File Adverse Action Letter is a formal notice sent when a lender cannot process a loan due to missing documentation. Under the Equal Credit Opportunity Act (ECOA), lenders must notify applicants within 30 days if an application is incomplete. This letter specifies the exact information required and provides a deadline for submission. Failure to provide the requested items results in a denial or withdrawal of the request. It ensures transparency and allows borrowers the opportunity to finalize their file for a full credit decision.

Adverse Action Letter for Unreturned Mortgage Application Documents

Lenders issue an Adverse Action Letter when a mortgage application is denied or withdrawn due to incomplete documentation. This formal notice is legally required under the Equal Credit Opportunity Act (ECOA) if you fail to provide requested financial records within the specified timeframe. Receiving this letter does not necessarily mean your credit is poor; it simply indicates the file was closed for non-compliance. To resume the process, you must typically reapply or promptly submit the missing paperwork to satisfy underwriting requirements and demonstrate financial transparency.

What is an Adverse Action Letter for an incomplete mortgage application?

An Adverse Action Letter for an incomplete application is a formal notice sent by a mortgage lender to an applicant stating that their loan request cannot be processed further due to missing documentation or information required to make a credit decision.

Why did I receive an Adverse Action notice for an incomplete application?

You received this notice because the lender did not receive all the necessary documents-such as tax returns, pay stubs, or bank statements-within the specified timeframe required to verify your eligibility for a mortgage loan.

Does an Adverse Action Letter for an incomplete application affect my credit score?

The letter itself does not impact your credit score. However, the initial "hard pull" inquiry performed by the lender when you first applied may have a minor, temporary effect on your credit rating.

What information must a lender provide in a notice of incompleteness?

Under the Equal Credit Opportunity Act (ECOA), the lender must provide a written statement listing the specific information needed to complete the application and a reasonable deadline for submission before the application is closed.

Can I reopen my mortgage application after receiving an Adverse Action Letter?

In most cases, you cannot reopen a closed application and must submit a new mortgage application with the required documentation. It is best to contact your loan officer immediately to determine if the previous file can be updated or if a new start is necessary.

Comments