Lenders must issue an Adverse Action Letter when a mortgage application is denied due to unacceptable property conditions. This formal notice explains specific safety, structural, or valuation issues that prevent the collateral from meeting secondary market standards. Understanding these regulatory requirements ensures compliance and transparency throughout the lending process. Below are some ready to use templates.

Image cover: Professional Templates and Samples for Property Condition Adverse Action Letters

Letter Samples List

- Adverse Action Letter for Unacceptable Property Condition

- Notice of Adverse Action Letter for Collateral Deficiency

- Mortgage Denial Letter for Insufficient Property Value

- Loan Rejection Letter for Structural Property Issues

- Adverse Action Letter for Hazardous Property Conditions

- Property Ineligibility Adverse Action Letter

- Adverse Action Letter for Zoning and Land Use Violations

- Mortgage Decline Letter for Unpermitted Property Additions

- Collateral Rejection Letter for Substandard Property Condition

- Appraisal Denial Letter for Inadequate Property Maintenance

- Adverse Action Letter for Uninhabitable Property State

- Loan Denial Letter for Unresolved Property Title Defects

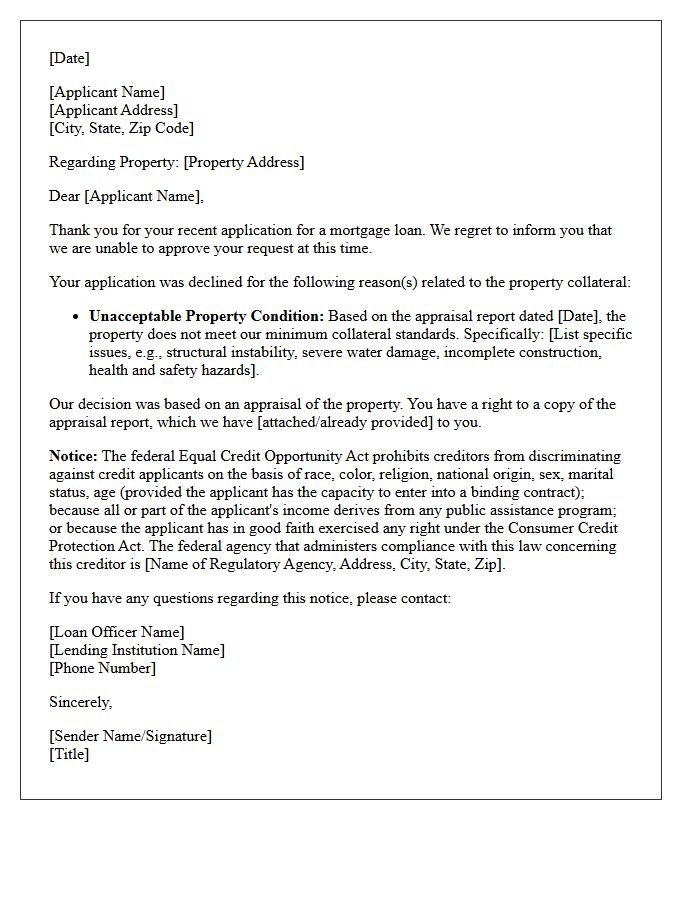

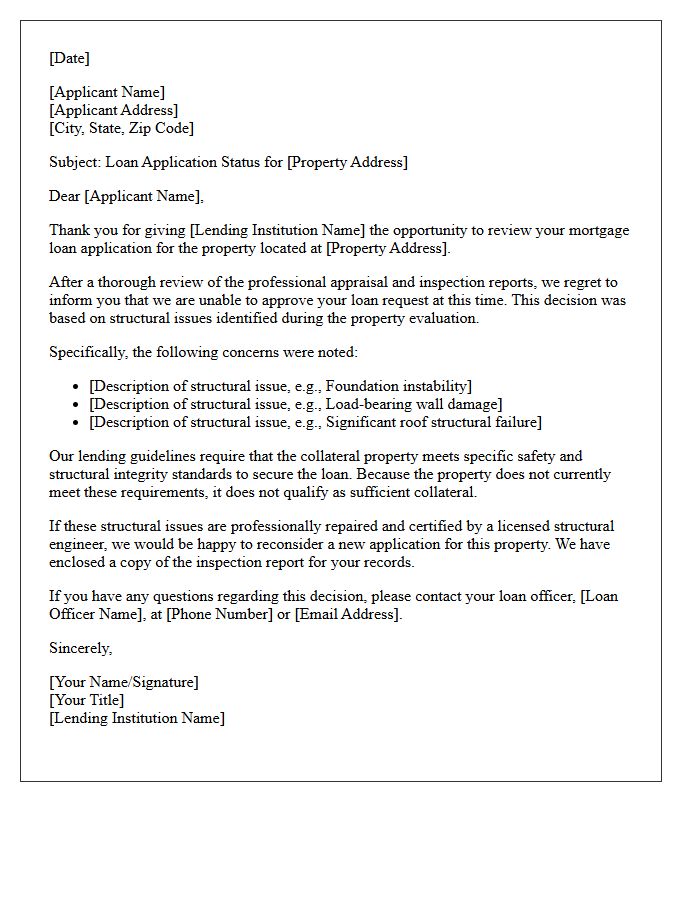

Adverse Action Letter for Unacceptable Property Condition

An Adverse Action Letter for unacceptable property condition is a formal notice issued by a lender when a mortgage application is denied due to issues found during an appraisal. It informs the applicant that the collateral's physical state, such as structural damage or safety hazards, fails to meet underwriting standards. Understanding the specific deficiencies listed is crucial, as it allows borrowers to negotiate repairs or seek alternative financing. This document ensures transparency and compliance with federal consumer protection laws regarding credit decisions based on property eligibility.

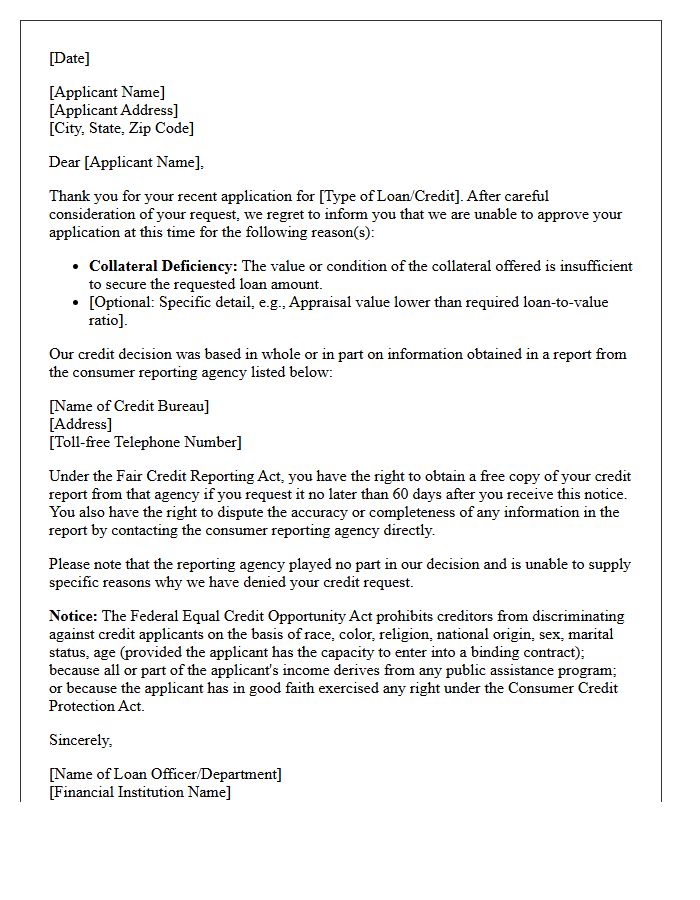

Notice of Adverse Action Letter for Collateral Deficiency

A Notice of Adverse Action Letter for collateral deficiency is a formal notification issued when a lender denies or modifies credit terms because the collateral value is insufficient to secure the loan. This notice is a legal requirement under the Equal Credit Opportunity Act. It must clearly state the specific reasons for the decision, such as an inadequate appraisal or low equity. Receiving this letter allows the applicant to verify the accuracy of the valuation and ensures transparency in the lending process while protecting consumer rights against arbitrary credit denials.

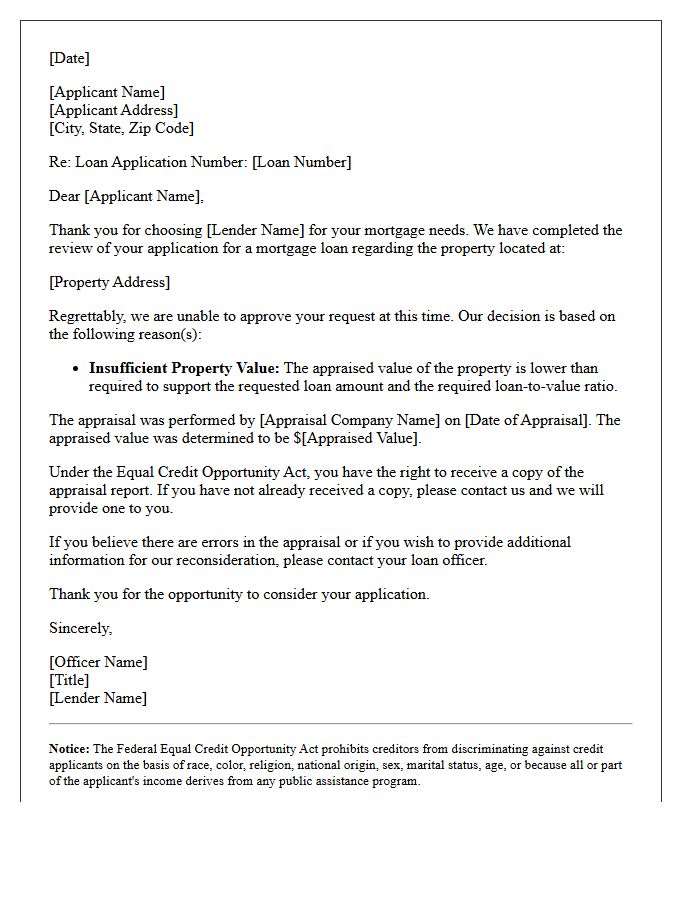

Mortgage Denial Letter for Insufficient Property Value

Receiving a mortgage denial letter for insufficient property value means the house appraised for less than the purchase price or loan amount. Lenders use the loan-to-value ratio to mitigate risk; if the collateral's market worth is too low, they cannot secure the debt. To resolve this, you can request an appraisal rebuttal, pay a larger down payment to cover the gap, or renegotiate the sale price with the seller. Understanding this discrepancy is vital for securing financing and ensuring you do not overpay for your investment.

Loan Rejection Letter for Structural Property Issues

A loan rejection letter due to structural property issues indicates that the building's physical integrity fails to meet lender safety standards. Common triggers include foundation cracks, roof damage, or outdated wiring that pose a financial risk to the collateral. Since the property secures the mortgage, lenders will deny financing if costly repairs threaten its long-term value. Reviewing the appraisal report is essential to identify specific defects. To move forward, you must either negotiate seller repairs, seek a specialized rehabilitation loan, or find a property in better condition to satisfy underwriting requirements.

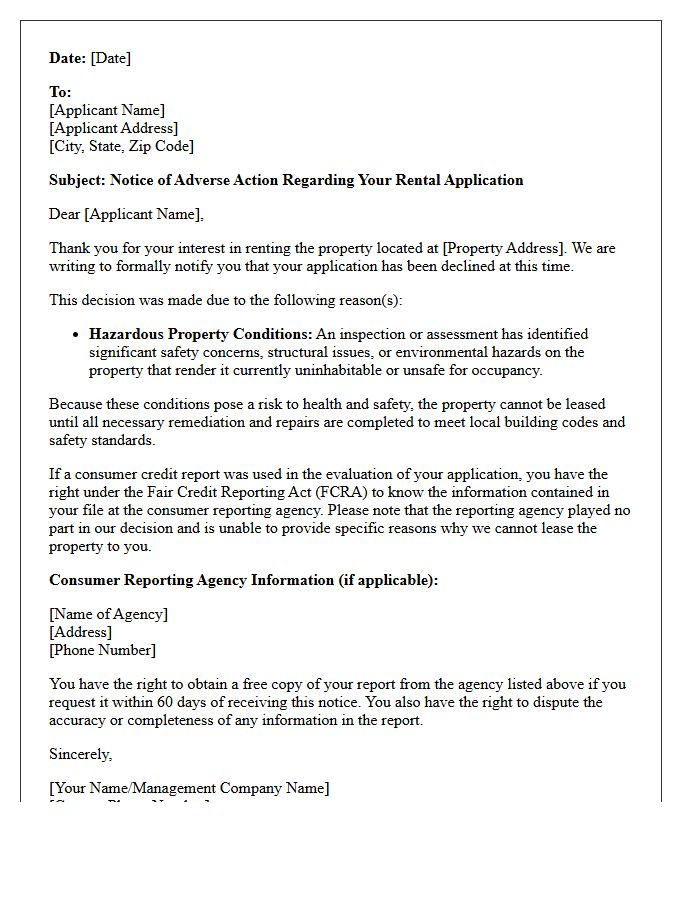

Adverse Action Letter for Hazardous Property Conditions

An Adverse Action Letter for hazardous property conditions is a formal notification sent when a rental application is denied due to safety risks or structural defects. Federal law requires landlords to provide specific reasons for rejection to ensure transparency. This document protects both parties by documenting uninhabitable conditions or liability concerns discovered during inspections. If you receive one, it signifies that the property fails to meet basic habitability standards, potentially posing a danger to occupants. Understanding these letters is crucial for maintaining legal compliance and ensuring tenant protection in the housing market.

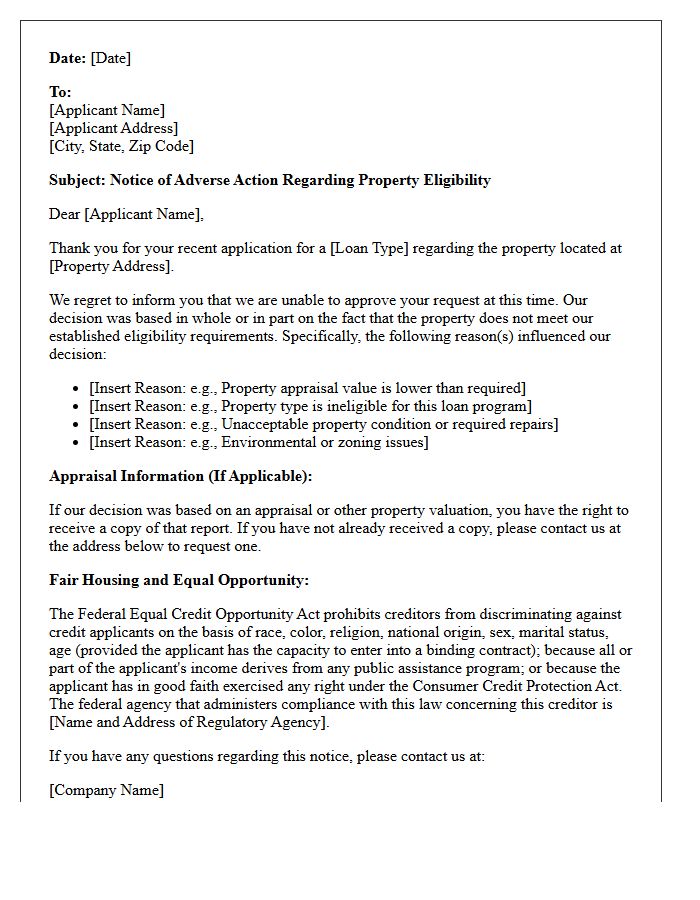

Property Ineligibility Adverse Action Letter

A Property Ineligibility Adverse Action Letter is a formal notice sent when a mortgage application is denied due to collateral issues discovered during an appraisal. This document explains that the property value or condition does not meet specific lender requirements, rather than a reflection of the applicant's creditworthiness. Key reasons may include structural defects, insufficient market value, or non-compliance with zoning laws. Federal regulations require lenders to disclose these specific findings to ensure transparency and provide the applicant with written notification of the financing rejection.

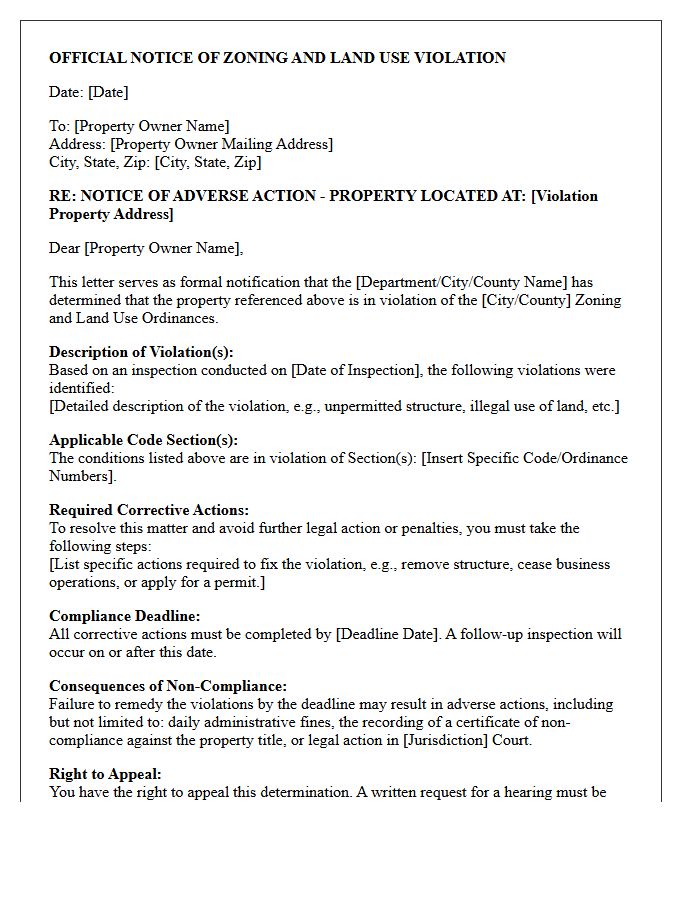

Adverse Action Letter for Zoning and Land Use Violations

An Adverse Action Letter serves as formal notice regarding zoning or land use violations. It informs property owners that their application was denied or that enforcement penalties are being pursued due to non-compliance with local ordinances. Key details include the specific code sections violated and the necessary corrective measures required to achieve legal standing. It is essential to review the appeals process and deadlines immediately, as failing to respond can lead to fines, liens, or legal injunctions against the property. Promptly addressing these letters ensures due process rights are protected.

Mortgage Decline Letter for Unpermitted Property Additions

Receiving a mortgage decline letter due to unpermitted property additions signifies that the lender views the home as a high-risk collateral. Non-compliant structures often violate local building codes, potentially leading to forced demolition or expensive legal fines. Appraisers may exclude the square footage of illegal additions, resulting in a valuation shortfall that prevents loan approval. To resolve this, homeowners must typically obtain retroactive permits or restore the property to its original state to meet strict secondary market underwriting standards and ensure structural safety for the lender.

Collateral Rejection Letter for Substandard Property Condition

A collateral rejection letter notifies a borrower that their loan application is denied because the property condition is substandard. Lenders issue this when an appraisal reveals structural issues, safety hazards, or deferred maintenance that devalues the asset. It is important to know that this rejection focuses on the collateral risk rather than your creditworthiness. Receiving this document allows you to seek repairs, negotiate price reductions, or identify a different property that meets underwriting standards to secure financing successfully.

Appraisal Denial Letter for Inadequate Property Maintenance

An appraisal denial letter due to inadequate property maintenance is a formal notification that a mortgage application was rejected because the home's physical condition poses a risk to the lender's collateral value. Significant issues like structural damage, peeling lead paint, or systemic neglect can prevent a property from meeting minimum safety and habitability standards. Borrowers must typically address these deferred maintenance concerns or complete specific repairs before the loan can be reconsidered. Understanding these deficiencies is crucial for resolving valuation hurdles and securing financing in a competitive real estate market.

Adverse Action Letter for Uninhabitable Property State

If a property is deemed uninhabitable due to severe safety or structural defects, lenders will issue an Adverse Action Letter to formally deny financing. This mandatory notice complies with the Equal Credit Opportunity Act, explaining that the collateral fails to meet minimum habitability standards. Borrowers must understand that property condition is a primary regulatory requirement for most mortgage approvals. Receiving this letter signifies that the loan cannot proceed until documented remediations occur or the property meets specific state-defined safety codes for residency.

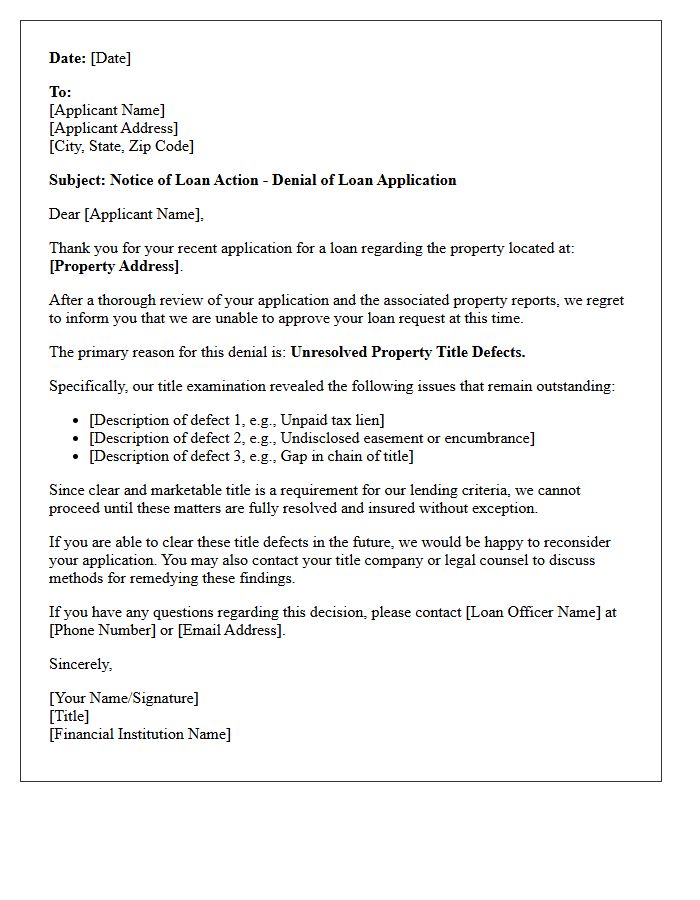

Loan Denial Letter for Unresolved Property Title Defects

A loan denial letter due to unresolved property title defects signifies that a lender has rejected your mortgage application because of legal claims or encumbrances discovered during a title search. Common issues include unpaid taxes, boundary disputes, or undisclosed liens that threaten the lender's security interest. Until these defects are cleared through corrective deeds or legal settlements, the property cannot serve as collateral. Receiving this notice requires immediate action to resolve the clouds on the title to secure future financing and ensure the legal ownership of the real estate asset.

What is an Adverse Action Letter for an unacceptable property condition?

An Adverse Action Letter is a formal notice sent to a loan applicant stating that their mortgage application has been denied or modified because the subject property failed to meet the lender's specific safety, soundness, or structural integrity standards.

What are common reasons for a property to be deemed unacceptable?

Common reasons include severe deferred maintenance, structural instability, presence of hazardous materials, inadequate utilities, or "subject to" appraisal repairs that the seller refuses to complete, which prevent the collateral from meeting secondary market requirements.

Can I still get a loan if I receive a denial based on property condition?

Yes, you may be able to secure financing by switching to a renovation loan (like an FHA 203k), requesting that the seller makes the necessary repairs before closing, or finding a lender with more flexible portfolio guidelines regarding property standards.

Does an unacceptable property condition affect my credit score?

No, receiving an Adverse Action Letter based on the property's physical condition does not impact your credit score. The denial is tied to the collateral's value and safety, not your personal creditworthiness or financial history.

How can a seller respond to a loan denial triggered by property condition?

A seller can respond by addressing the specific deficiencies listed in the appraisal or inspection report, lowering the sale price to accommodate a cash buyer, or providing a credit at closing if the lender allows for a repair escrow to fix the issues post-closing.

Comments