Lenders issue an Adverse Action Letter when a low property appraisal prevents loan approval on requested terms. This formal notice explains the valuation discrepancy and outlines your rights under the Equal Credit Opportunity Act. Understanding this document is essential for navigating financing hurdles or appealing the results. To help you communicate effectively, below are some ready to use template.

Image cover: Navigating Low Appraisals: Adverse Action Letter Templates and Best Practices

Letter Samples List

- Adverse Action Letter for Low Property Appraisal

- Notice of Adverse Action Letter Due to Insufficient Appraisal Value

- Mortgage Loan Denial Letter for Low Appraisal

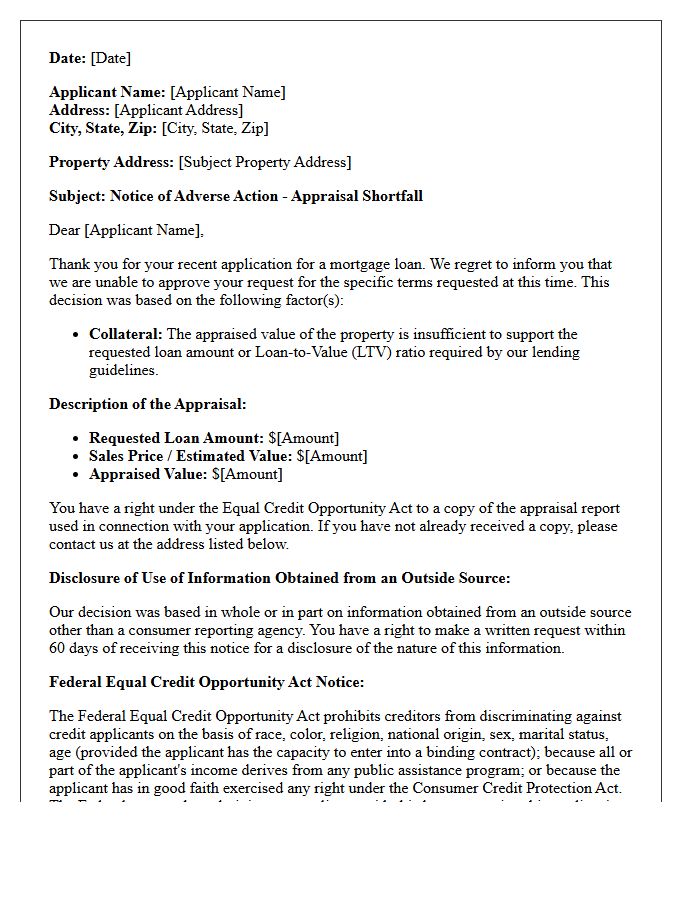

- Appraisal Shortfall Adverse Action Letter

- Low Property Valuation Adverse Action Letter

- Statement of Credit Denial Letter for Under-Appraised Property

- Mortgage Application Rejection Letter Due to Appraisal Value

- Inadequate Collateral Value Adverse Action Letter

- Property Appraisal Discrepancy Adverse Action Letter

- Home Loan Declination Letter for Low Property Appraisal

- Insufficient Property Value Adverse Action Letter

- Real Estate Appraisal Deficit Loan Denial Letter

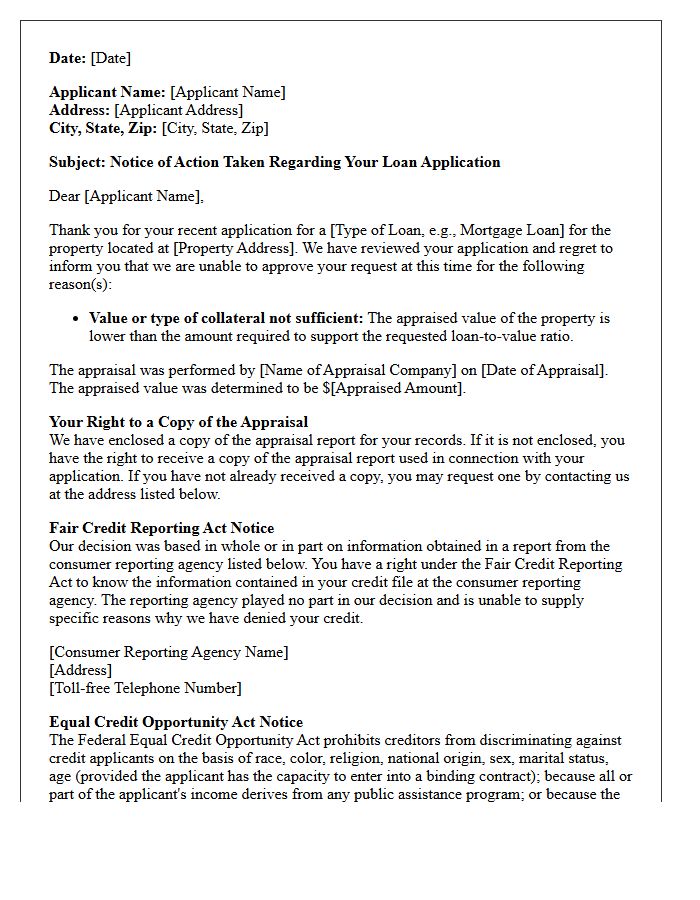

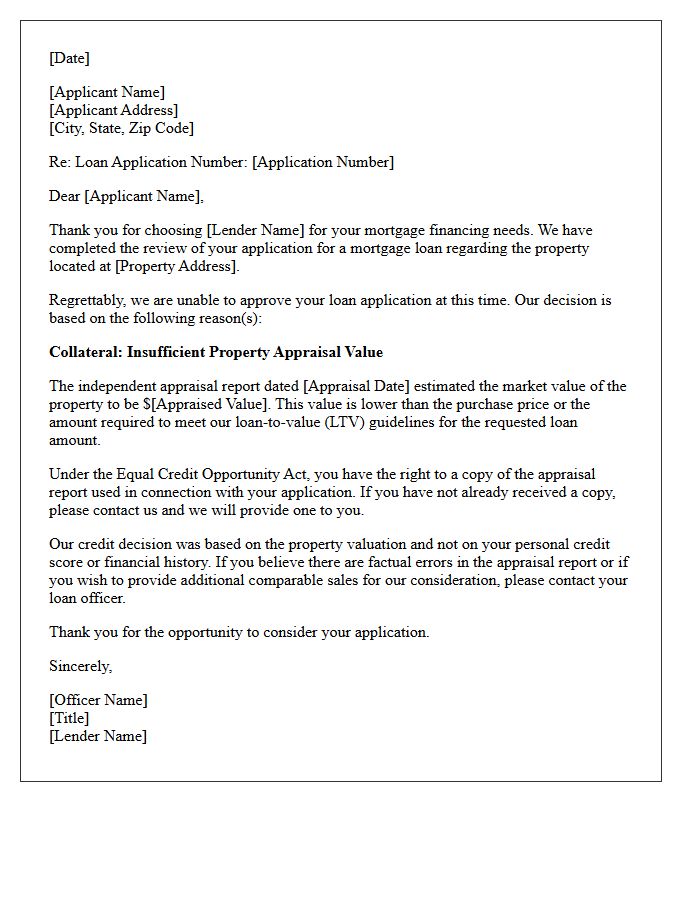

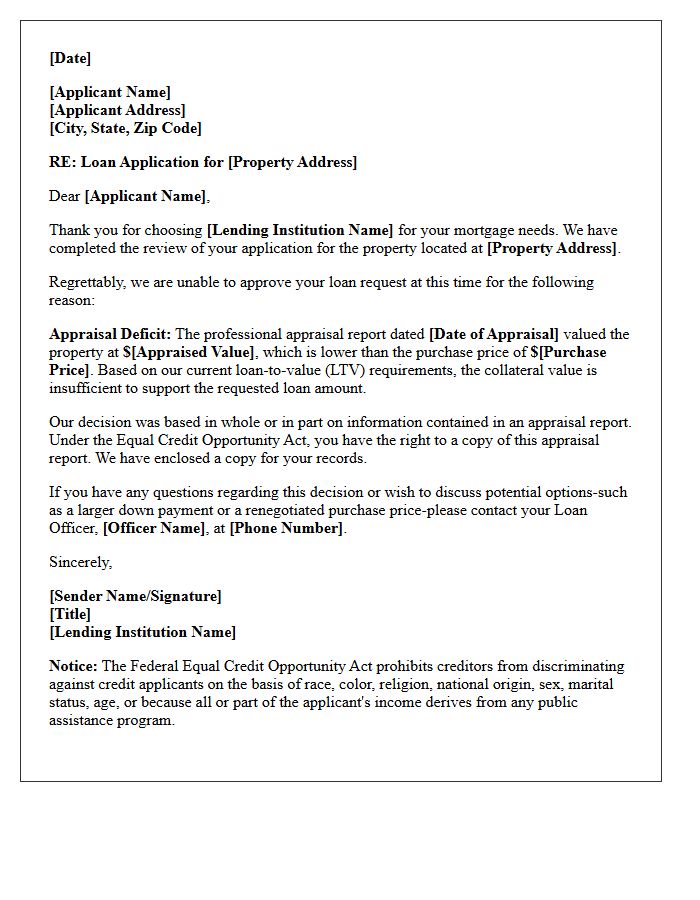

Adverse Action Letter for Low Property Appraisal

An Adverse Action Letter is a formal notice issued by lenders when a mortgage application is denied or terms change due to a low property appraisal. This document is required by law to explain that the collateral value did not meet the loan-to-value requirements. It protects consumers by providing transparency under the Equal Credit Opportunity Act. Receiving this letter allows you to review the appraisal for errors, dispute the valuation through a rebuttal, or negotiate a lower sales price with the seller to proceed with the financing.

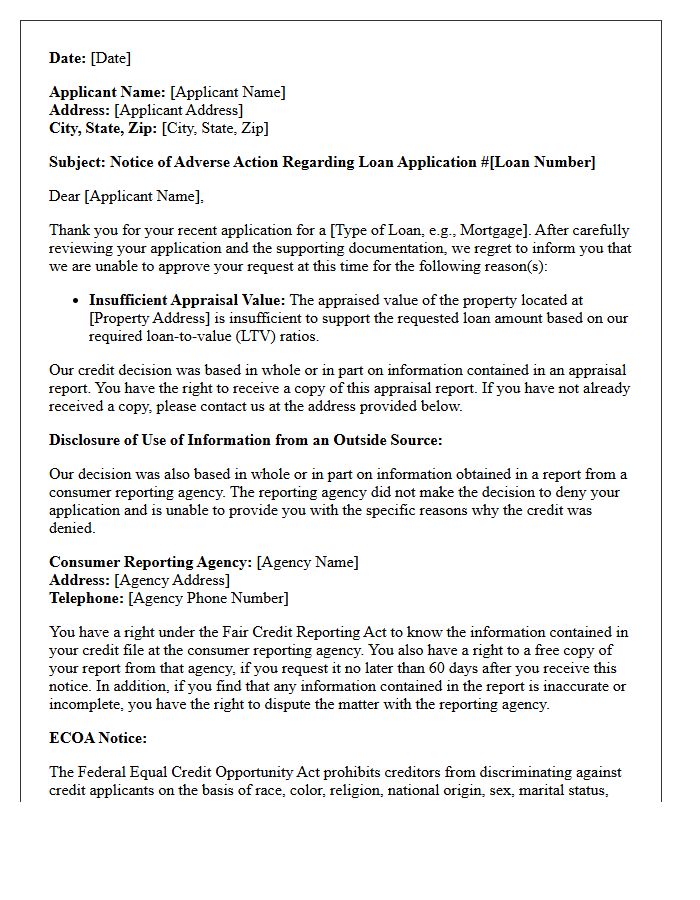

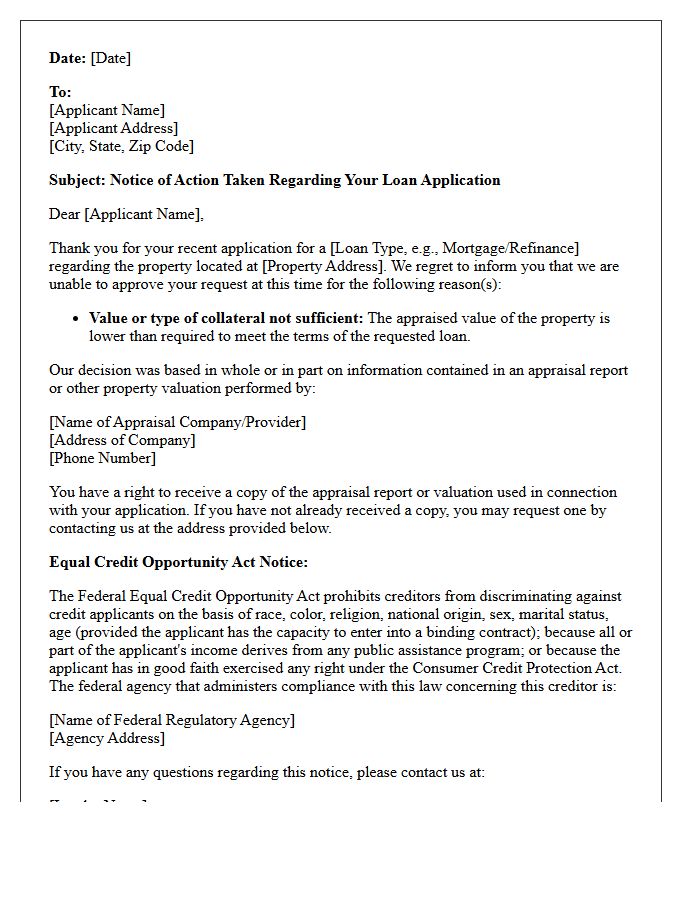

Notice of Adverse Action Letter Due to Insufficient Appraisal Value

A Notice of Adverse Action is a mandatory legal document sent when a mortgage application is denied or terms are modified due to an insufficient appraisal value. This letter informs the borrower that the property's market value did not meet the lender's required loan-to-value ratio. Under the Equal Credit Opportunity Act (ECOA), lenders must provide specific reasons for the decision and notify you of your right to receive a copy of the appraisal report to dispute potential errors or market inaccuracies.

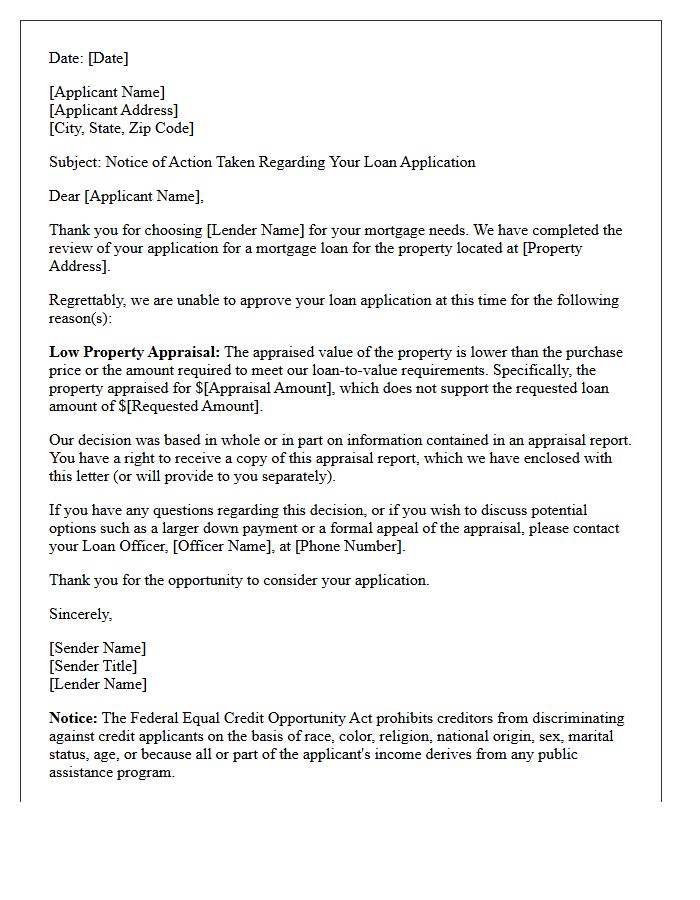

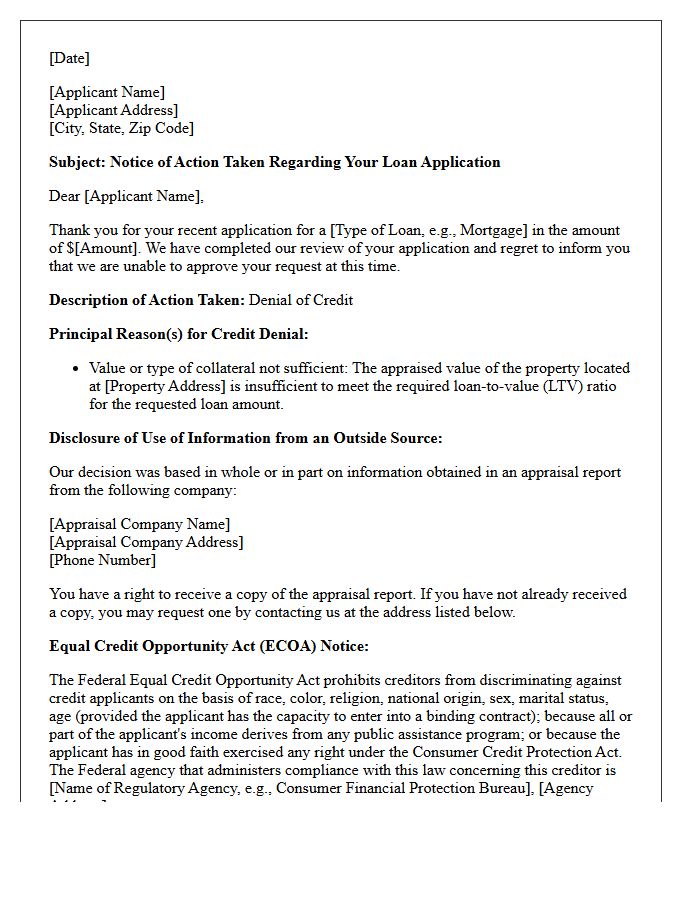

Mortgage Loan Denial Letter for Low Appraisal

A mortgage loan denial letter due to a low appraisal occurs when a property's market value falls below the agreed purchase price. Lenders use the loan-to-value ratio to determine risk; if the appraisal is short, the collateral is insufficient for the requested loan amount. Borrowers can respond by requesting a reconsideration of value, covering the price gap with cash, or renegotiating with the seller to lower the price. Review the letter carefully to identify the exact valuation discrepancy and understand your options for appeal or restructuring the deal.

Appraisal Shortfall Adverse Action Letter

An Appraisal Shortfall Adverse Action Letter is a formal notice sent to mortgage applicants when a property's appraised value is lower than the purchase price. This document is legally required under the Equal Credit Opportunity Act (ECOA) if the lender denies the loan, reduces the amount, or changes terms due to the valuation. It protects consumers by providing transparency regarding the lending decision. Borrowers receive a copy of the appraisal report to review for errors or to negotiate a reconsideration of value before finalizing their home financing options.

Low Property Valuation Adverse Action Letter

A Low Property Valuation Adverse Action Letter is a formal notice issued by a lender when a mortgage application is denied because the appraisal amount is lower than the purchase price. This document is a regulatory requirement under the Equal Credit Opportunity Act (ECOA). It informs the borrower that the collateral value is insufficient to secure the requested loan amount. Receiving this letter allows the applicant to request a free copy of the appraisal report to dispute inaccuracies or negotiate a lower sale price with the seller.

Statement of Credit Denial Letter for Under-Appraised Property

A Statement of Credit Denial is a formal notice lenders must provide when a loan is rejected due to a low valuation. If your mortgage application fails because of an under-appraisal, federal law requires the lender to explain the specific reasons in writing. This document helps you identify if the denial was based on collateral insufficiency rather than creditworthiness. Understanding this letter allows you to challenge the appraisal errors or request a Reconsideration of Value (ROV) to potentially salvage your real estate transaction and financing options.

Mortgage Application Rejection Letter Due to Appraisal Value

Receiving a mortgage rejection letter due to a low appraisal means the property's market value is less than the loan amount requested. Lenders use the Loan-to-Value (LTV) ratio to assess risk; if the appraisal falls short, the collateral is insufficient to secure the debt. To proceed, you can request a reconsideration of value, provide a larger down payment to cover the gap, or negotiate a lower purchase price with the seller. Understanding this discrepancy is vital for resolving financing hurdles and ensuring a fair market investment.

Inadequate Collateral Value Adverse Action Letter

An Inadequate Collateral Value Adverse Action Letter is a formal notice issued when a loan is denied because the asset's appraised worth fails to secure the requested debt. Under the Equal Credit Opportunity Act, lenders must provide specific reasons for this adverse action. It is crucial to understand that this rejection often stems from a professional valuation report or LTV ratio calculation. Borrowers have the legal right to receive a copy of the appraisal to contest discrepancies or identify market factors that impacted the decision.

Property Appraisal Discrepancy Adverse Action Letter

A Property Appraisal Discrepancy Adverse Action Letter is a formal notice sent by lenders when a valuation gap prevents loan approval on requested terms. If an appraisal comes in lower than the purchase price, it directly affects the loan-to-value ratio, potentially leading to a denial or a requirement for a larger down payment. Federal law requires creditors to provide this written explanation, ensuring transparency regarding the collateral assessment. Borrowers have the right to review the report and dispute inaccuracies through a reconsideration of value process to address the discrepancy.

Home Loan Declination Letter for Low Property Appraisal

Receiving a home loan declination letter due to a low property appraisal means the lender's valuation is less than your contract price. This creates a funding gap because banks limit financing based on the appraised value, not the purchase price. To move forward, you can request a rebuttal of value by providing better comparable sales, negotiate a lower price with the seller, or cover the difference in cash. This document is a formal notice that your current loan-to-value ratio does not meet underwriting guidelines for approval.

Insufficient Property Value Adverse Action Letter

An Insufficient Property Value Adverse Action Letter is a formal notice issued when a mortgage application is denied due to a low appraisal. It informs the borrower that the collateral's market value does not meet the lender's required loan-to-value ratio. Under the Equal Credit Opportunity Act, lenders must provide this written explanation within thirty days. Borrowers have the right to receive a free copy of the appraisal report to dispute valuation errors or factual inaccuracies that led to the loan rejection.

Real Estate Appraisal Deficit Loan Denial Letter

Receiving a Real Estate Appraisal Deficit Loan Denial Letter occurs when a property's appraised value is lower than the agreed purchase price. Lenders issue this notice because the collateral fails to support the requested loan-to-value ratio. To proceed, buyers must either negotiate a lower price, provide a larger cash down payment to cover the gap, or request a reconsideration of value. Understanding this document is vital, as it legally outlines why financing was rejected based on current market data and comparable sales findings.

What is an adverse action letter for a low property appraisal?

An adverse action letter is a formal notice sent by a lender to a loan applicant explaining that credit has been denied, or terms have changed, because the property's appraised value was lower than the purchase price or requested loan amount.

Why did I receive an adverse action notice after my home appraisal?

You received this notice because the independent appraisal report valued the property at less than the agreed-upon sales price, resulting in a loan-to-value (LTV) ratio that exceeds the lender's specific underwriting guidelines for the requested mortgage.

Can I dispute the appraisal value mentioned in my adverse action letter?

Yes, you have the right to request a "Reconsideration of Value" (ROV). You must provide the lender with evidence of factual errors in the report or suggest comparable properties that the appraiser may have overlooked during the initial valuation.

What are my options if a low appraisal triggers an adverse action?

If a low appraisal affects your loan approval, you can choose to pay the difference in cash, negotiate a lower sales price with the seller, request a second appraisal, or provide additional collateral to meet the lender's loan-to-value requirements.

Does a low property appraisal adverse action affect my credit score?

No, receiving an adverse action letter due to a low property appraisal is based on the collateral's value, not your creditworthiness. While the initial credit inquiry (hard pull) by the lender may affect your score, the denial based on the appraisal itself does not.

Comments