When a lender rejects a request to take over an existing loan, they must issue an Adverse Action Letter for Mortgage Assumption Denial. This formal notice explains the specific reasons for the refusal, ensuring compliance with fair lending laws and providing transparency for the applicant. Understanding these requirements is essential for regulatory adherence. Below are some ready to use templates.

Image cover: Mortgage Assumption Denial: Adverse Action Notice Templates and Compliance Guide

Letter Samples List

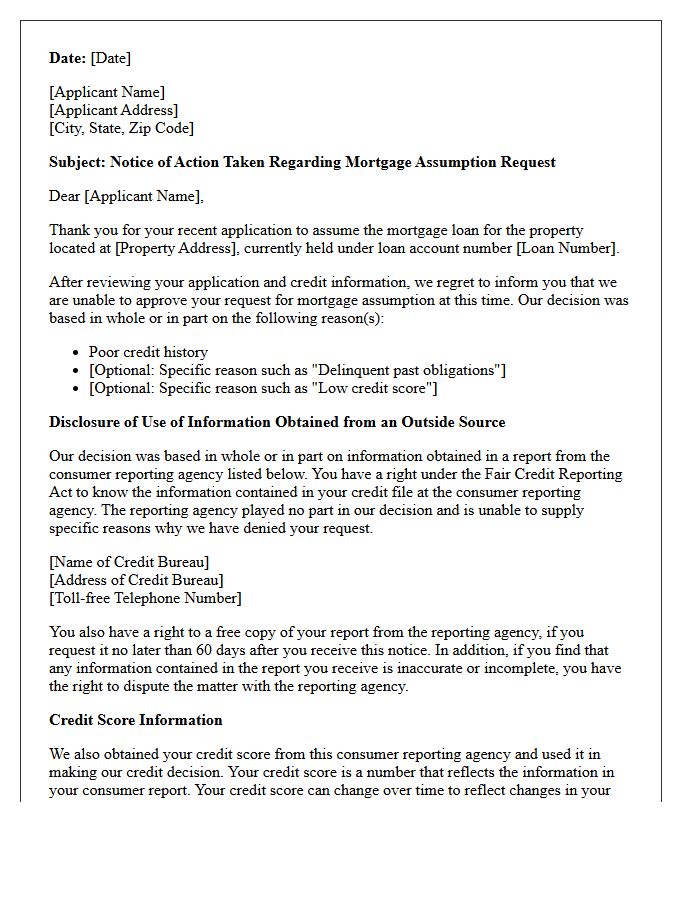

- Adverse Action Letter for Mortgage Assumption Denial Due to Poor Credit History

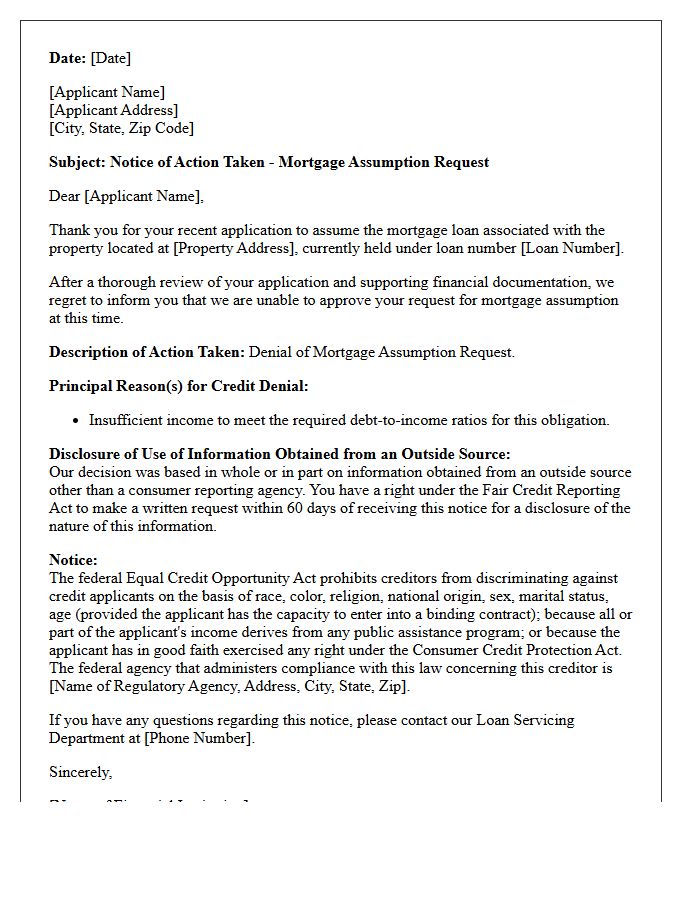

- Insufficient Income Adverse Action Letter for Mortgage Assumption Rejection

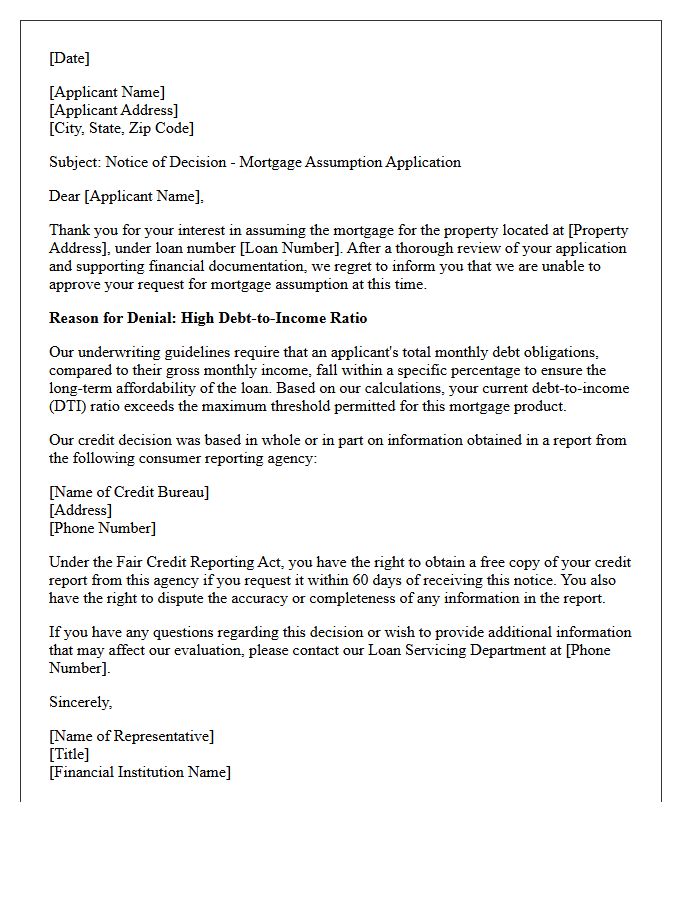

- High Debt-to-Income Ratio Mortgage Assumption Denial Letter

- Adverse Action Letter for Mortgage Assumption Denial Based on Unverifiable Employment

- Incomplete Application Adverse Action Letter for Mortgage Assumption Processing

- Mortgage Assumption Denial Letter Due to Insufficient Liquid Assets

- Adverse Action Letter for Mortgage Assumption Denial Regarding Recent Bankruptcy

- Unsatisfactory Payment History Adverse Action Letter for Mortgage Assumption

- Adverse Action Letter for Mortgage Assumption Denial Due to Unpaid Tax Liens

- Credit Freeze Adverse Action Letter for Mortgage Assumption Denial

- Adverse Action Letter for Co-Applicant Mortgage Assumption Denial

- Non-Owner Occupancy Mortgage Assumption Denial Adverse Action Letter

Adverse Action Letter for Mortgage Assumption Denial Due to Poor Credit History

When a lender rejects a mortgage assumption request, they must issue an Adverse Action Letter. This mandatory document explains that the applicant's poor credit history failed to meet underwriting standards. It provides transparency by disclosing the specific credit score used and the contact details of the reporting bureau. Understanding this letter is crucial for identifying errors or negative factors impacting your creditworthiness. Under the Equal Credit Opportunity Act, this notice ensures applicants are informed of why they were denied the legal transfer of loan liability.

Insufficient Income Adverse Action Letter for Mortgage Assumption Rejection

When a lender denies a mortgage assumption due to insufficient income, they must issue an adverse action letter. This document legally notifies the applicant that their documented earnings fail to meet the debt-to-income requirements necessary to take over the existing loan. The letter serves as transparency, detailing the specific financial reasons for rejection and providing information on how to obtain a free credit report. Understanding these income deficiencies is essential for applicants to address financial gaps or seek a co-signer before reapplying to assume the mortgage liability.

High Debt-to-Income Ratio Mortgage Assumption Denial Letter

A mortgage assumption denial letter for a high Debt-to-Income (DTI) ratio informs an applicant that their monthly financial obligations exceed the lender's qualifying threshold. This rejection occurs when your total debt payments, including the assumed mortgage, are too high relative to your gross income. Lenders view this as an increased risk of default. To contest this decision, review your credit report for errors, document additional income sources, or pay down existing balances to lower your ratio before requesting a formal reconsideration of the assumption application.

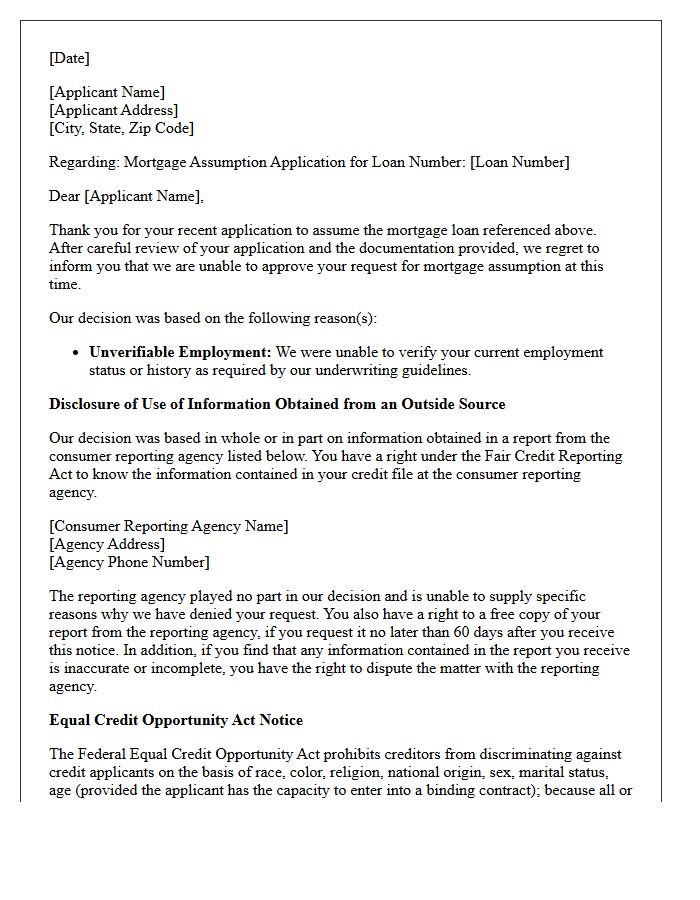

Adverse Action Letter for Mortgage Assumption Denial Based on Unverifiable Employment

If a lender denies a mortgage assumption due to unverifiable employment, they must issue an Adverse Action Letter. This document is a legal requirement under the Equal Credit Opportunity Act. It informs the applicant that their income sources could not be authenticated through standard documentation or employer contact. To resolve this, applicants should request the specific reasons for the denial and provide alternative proof of stability, such as tax returns or bank statements, to demonstrate repayment capacity and ensure the mortgage assumption process continues successfully.

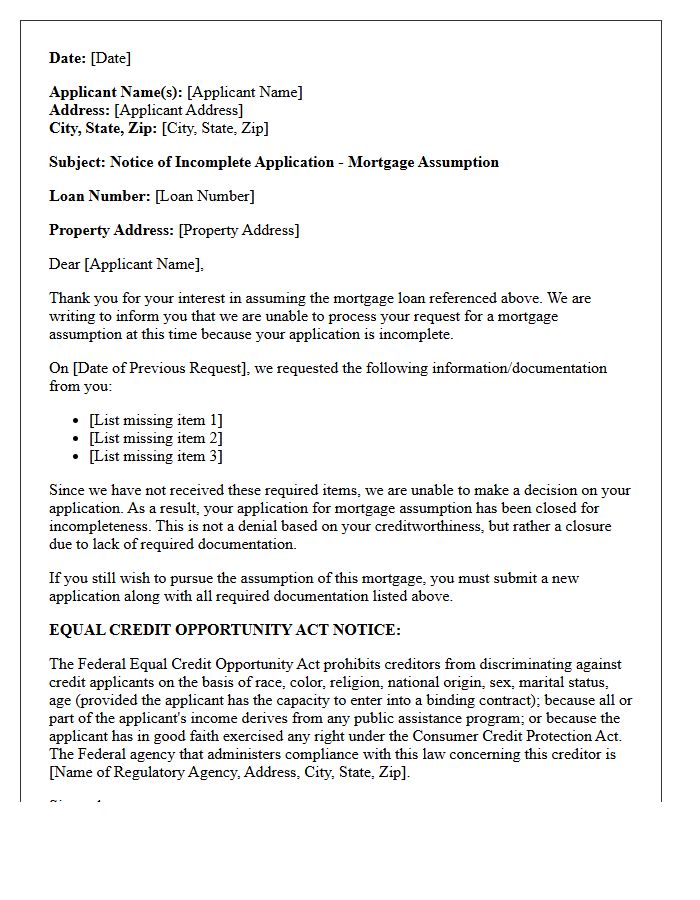

Incomplete Application Adverse Action Letter for Mortgage Assumption Processing

When processing a mortgage assumption, lenders issue an Incomplete Application Adverse Action Letter if the applicant fails to provide required documentation. This notice serves as a formal Notice of Incompleteness under Regulation B. It must specify the missing information and provide a clear deadline for submission. If the applicant does not comply within the stated timeframe, the lender will deny the assumption request. This document is a critical compliance requirement, ensuring transparency and protecting consumer rights during the credit decision process for assuming an existing loan.

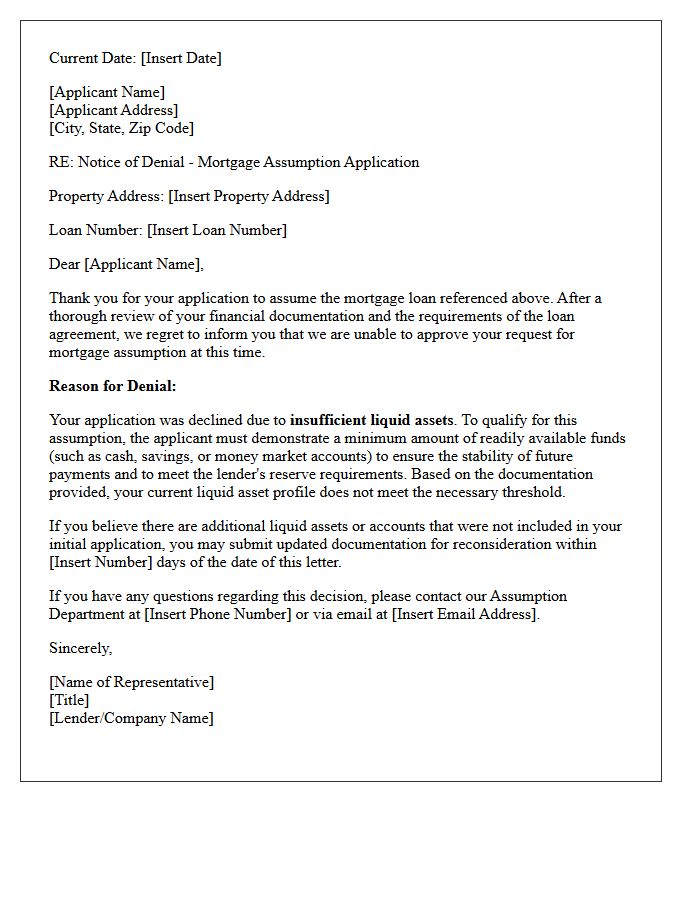

Mortgage Assumption Denial Letter Due to Insufficient Liquid Assets

A mortgage assumption denial letter citing insufficient liquid assets indicates that the applicant fails to meet the lender's cash reserve requirements. Lenders mandate specific levels of accessible capital to ensure the new borrower can cover closing costs, down payments, and several months of future mortgage obligations. Even with a high income, a lack of liquid funds like savings or stocks suggests a higher default risk. To overturn this decision, applicants must provide documented proof of additional liquid resources or source a gift fund to demonstrate financial stability.

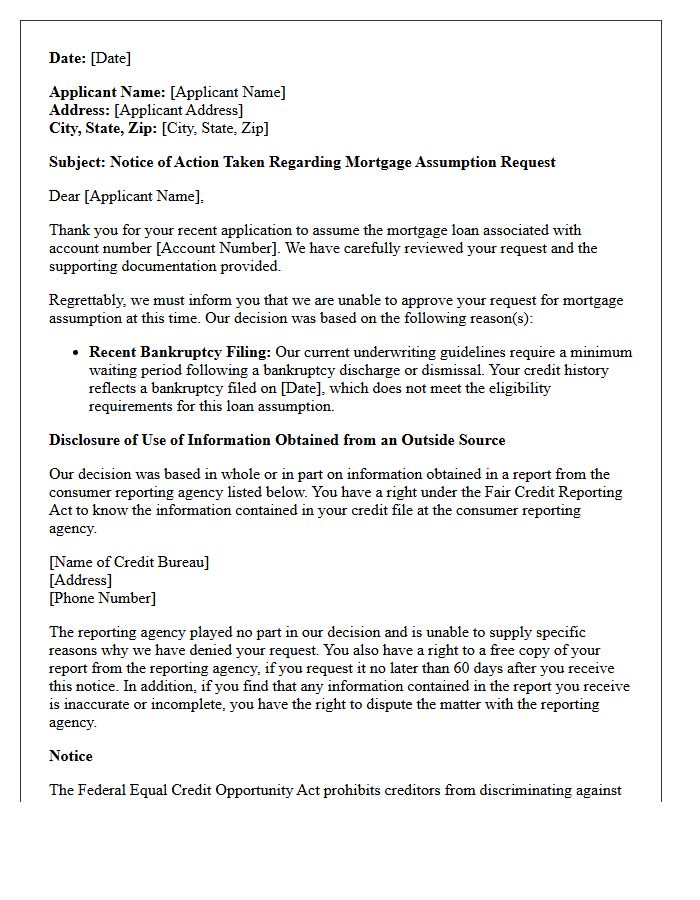

Adverse Action Letter for Mortgage Assumption Denial Regarding Recent Bankruptcy

Receiving an adverse action letter after a mortgage assumption denial is critical when a recent bankruptcy is involved. This formal notice explains why the lender rejected the request to take over a loan. Under the Equal Credit Opportunity Act, the lender must provide specific reasons, such as insufficient time since the discharge or failure to meet seasoning requirements. Reviewing this document helps you understand the impact of your credit history on eligibility and allows you to dispute inaccuracies. Timely communication with the servicer is essential to address these financial barriers effectively.

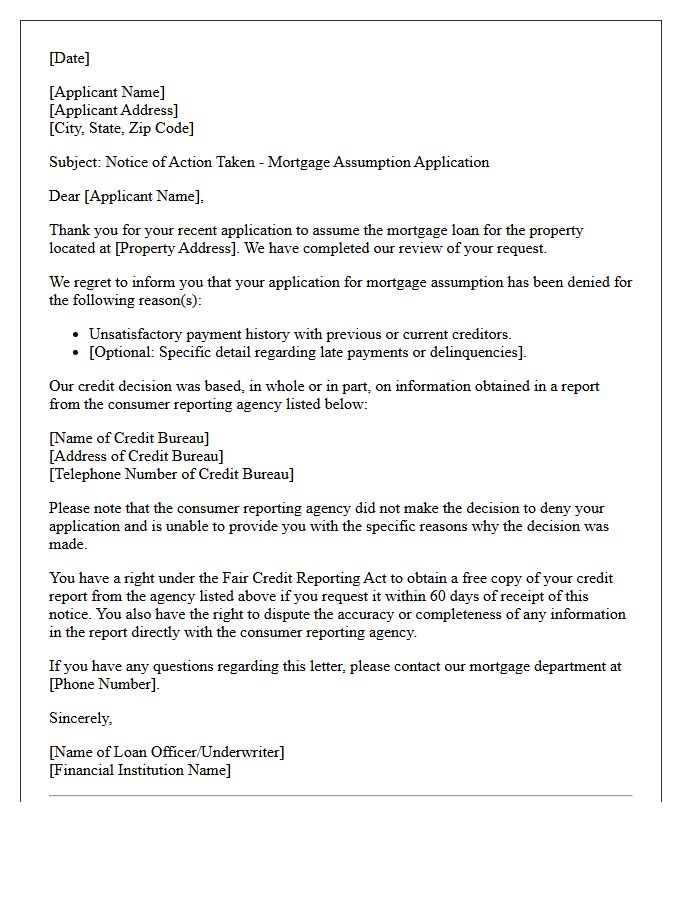

Unsatisfactory Payment History Adverse Action Letter for Mortgage Assumption

An Unsatisfactory Payment History Adverse Action Letter is a formal notice issued when a mortgage assumption request is denied due to past credit issues. It notifies the applicant that their repayment track record failed to meet underwriting standards. Under the Equal Credit Opportunity Act (ECOA), lenders must provide specific reasons for the rejection, such as late payments or delinquencies. Understanding this document is crucial for identifying credit reporting errors and taking corrective steps to improve eligibility for future financing or successful loan transfers.

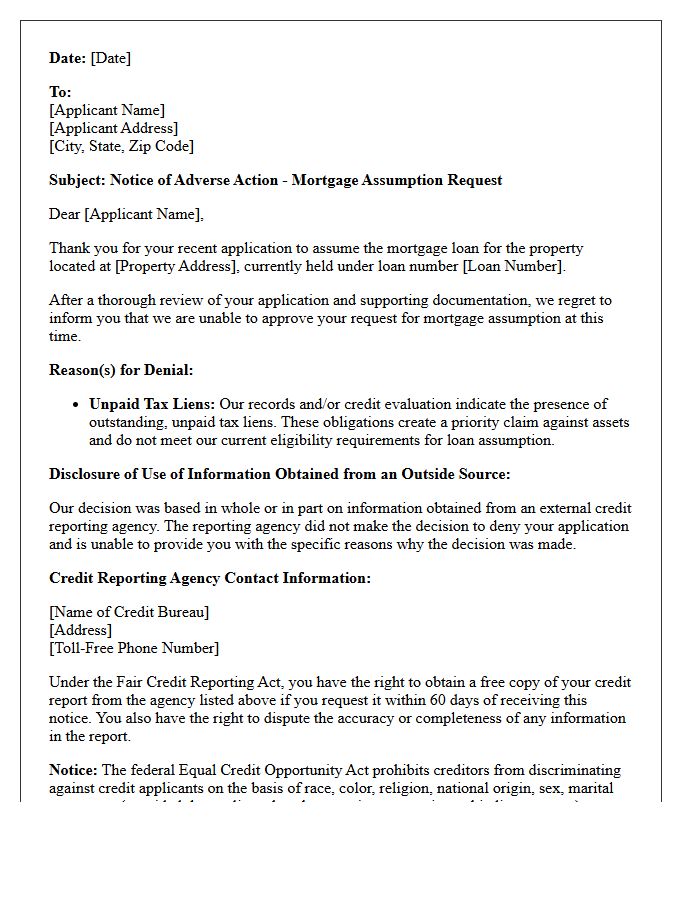

Adverse Action Letter for Mortgage Assumption Denial Due to Unpaid Tax Liens

An Adverse Action Letter is a formal notification issued when a mortgage assumption request is denied. If the rejection stems from unpaid tax liens, the lender must specify that the applicant's creditworthiness or the property's title status failed to meet underwriting standards. Under the Equal Credit Opportunity Act (ECOA), this document ensures transparency by explaining how tax liens create superior claims that jeopardize the lender's security interest. Borrowers should review the letter to identify which governmental records triggered the denial and seek professional tax resolution to clear the title.

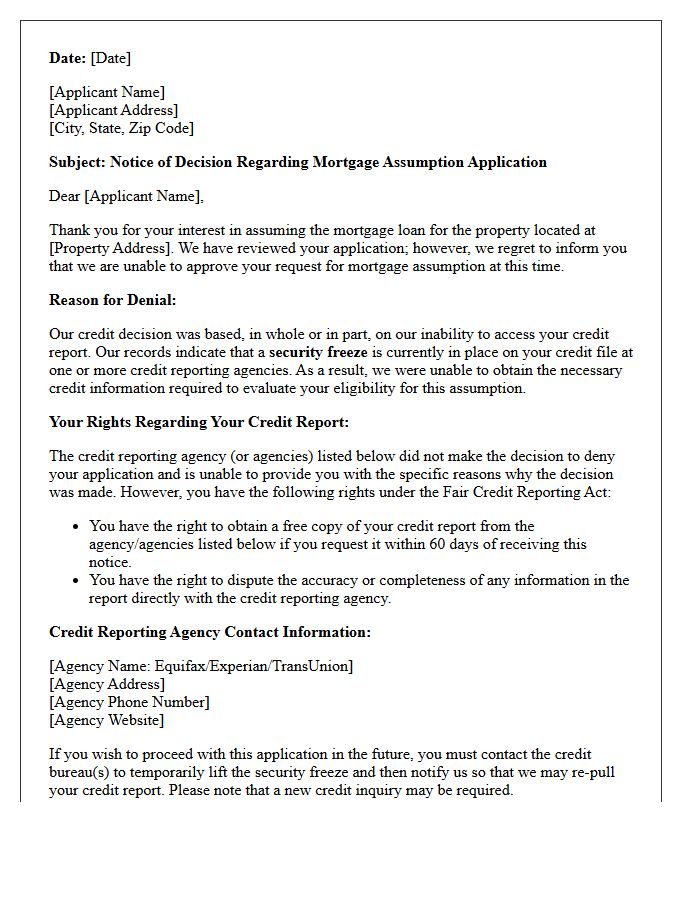

Credit Freeze Adverse Action Letter for Mortgage Assumption Denial

If you receive a Credit Freeze Adverse Action Letter after a mortgage assumption denial, it means the lender could not access your credit report due to a security freeze. Federal law requires this notice to explain why your application was halted. To proceed, you must contact the relevant credit bureaus to thaw your file, then request a re-evaluation from the lender. This letter ensures transparency under the Fair Credit Reporting Act, allowing you to address data access issues rather than a poor credit score itself.

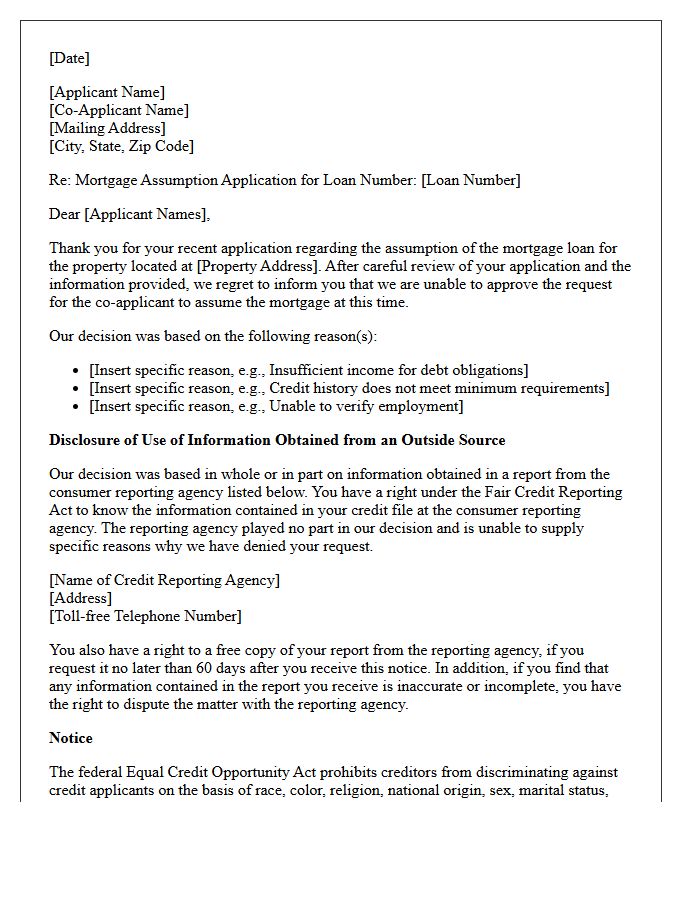

Adverse Action Letter for Co-Applicant Mortgage Assumption Denial

When a co-applicant is denied during a mortgage assumption, the lender must issue an Adverse Action Letter. This document is a legal requirement under the Equal Credit Opportunity Act. It explicitly details the specific reasons for the rejection, such as insufficient income or poor credit scores. Understanding this notice is crucial because it allows the applicant to dispute inaccuracies or improve their financial standing for future requests. Protecting your consumer rights ensures transparency throughout the mortgage assumption process, preventing arbitrary lending decisions and ensuring fair housing compliance for all parties involved.

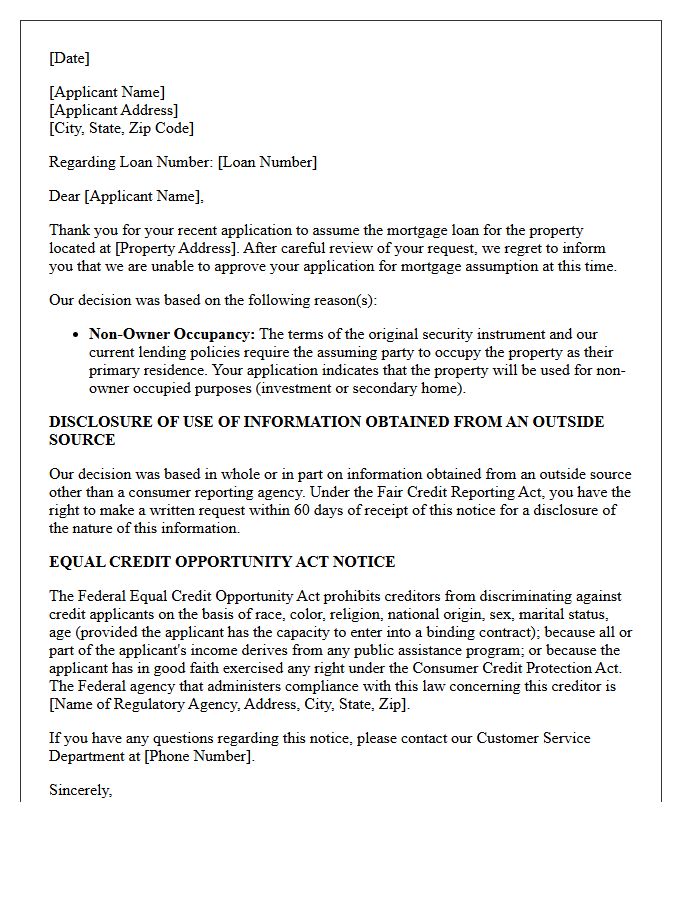

Non-Owner Occupancy Mortgage Assumption Denial Adverse Action Letter

A Non-Owner Occupancy Mortgage Assumption Denial Adverse Action Letter is a formal notice sent when a lender rejects a request to take over a loan because the applicant does not intend to live in the property. Lenders prioritize owner-occupancy to mitigate risk, as investment properties often carry higher default rates. Federal law requires this document to clearly state the specific reasons for the credit denial. Receiving this letter ensures transparency and informs the applicant of their rights to review credit reports used during the evaluation process.

What is a mortgage assumption adverse action letter?

A mortgage assumption adverse action letter is a formal written notice sent by a lender to inform an applicant that their request to take over an existing mortgage loan has been denied. This document is required by the Equal Credit Opportunity Act (ECOA) and must outline the specific reasons for the credit denial.

Why was my mortgage assumption application denied?

Common reasons for denial include a low credit score, insufficient debt-to-income (DTI) ratio, unstable employment history, or failure to meet the specific investor guidelines associated with the original loan. The adverse action letter will explicitly state the primary factors that contributed to the lender's decision.

Can I dispute the findings in a mortgage assumption denial letter?

Yes. Under the Fair Credit Reporting Act (FCRA), if your denial was based on information from a credit report, you have the right to request a free copy of that report within 60 days. If you find inaccuracies or outdated information, you can dispute those items with the credit bureau and provide corrected documentation to the lender for reconsideration.

Does a denial for a mortgage assumption affect my credit score?

The receipt of the adverse action letter itself does not impact your credit score. However, the hard credit inquiry performed by the lender during the application process may cause a temporary, minor decrease in your score, regardless of whether the assumption was approved or denied.

What are my options after receiving an adverse action letter for an assumption?

After receiving a denial, you can attempt to resolve the specific issues cited (such as paying down debt), apply with a qualified co-signer if the lender permits, or explore alternative financing options like a traditional purchase mortgage. You may also contact the lender's loss mitigation or assumption department to discuss if a different program better fits your financial profile.

Comments