Receiving an adverse action letter after a mortgage loan modification denial is a formal requirement under federal law. This notice explains the specific reasons for the rejection, ensuring transparency and protecting consumer rights during the loss mitigation process. Understanding these legal disclosures helps homeowners determine their next steps or appeal options. To assist you, below are some ready to use template.

Image cover: Navigating Mortgage Modification Denials: Adverse Action Letter Samples and Templates

Letter Samples List

- Insufficient Income Mortgage Modification Denial Letter

- Incomplete Application Adverse Action Modification Letter

- Negative Net Present Value Mortgage Modification Denial Letter

- Missing Documentation Adverse Action Modification Letter

- Maximum Modification Limit Reached Adverse Action Letter

- Non-Owner Occupied Property Modification Denial Letter

- Excessive Forbearance History Modification Denial Letter

- Minimum Credit Score Requirement Adverse Action Letter

- Lack of Imminent Default Modification Denial Letter

- Investor Guideline Restriction Adverse Action Letter

- Excessive Debt-to-Income Ratio Modification Denial Letter

- Subordinate Lien Conflict Adverse Action Modification Letter

- Standard Mortgage Loan Modification Adverse Action Letter

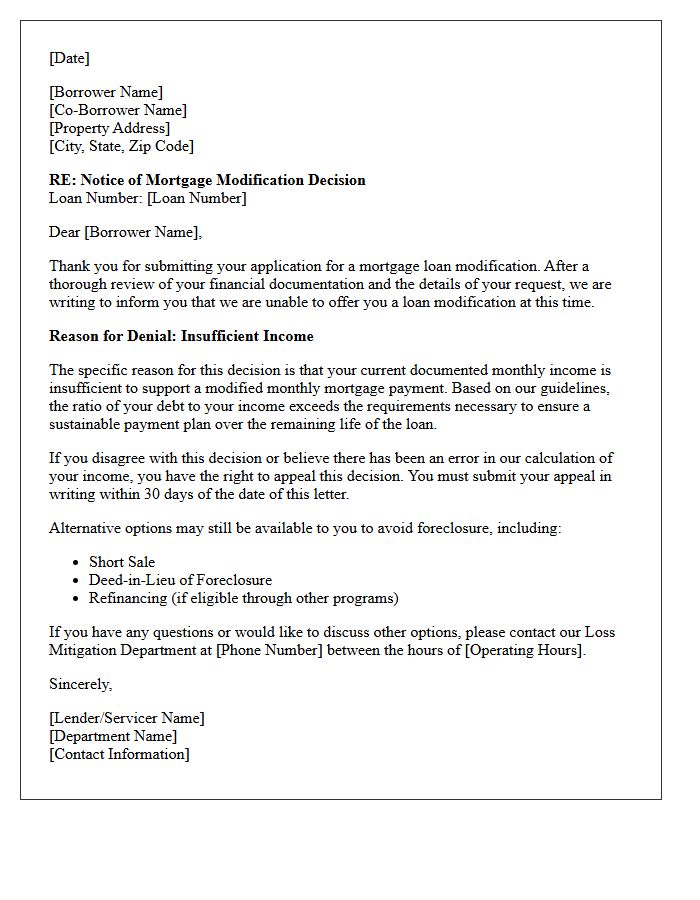

Insufficient Income Mortgage Modification Denial Letter

An Insufficient Income Mortgage Modification Denial occurs when a lender determines your monthly gross earnings cannot support a sustainable restructured payment. This NPV (Net Present Value) failure means the bank believes foreclosure is more financially viable than a loan adjustment. To challenge this, you must quickly document supplemental income or household contributions and submit a formal appeal within 30 days. Understanding your debt-to-income ratio is essential to proving you have enough stable cash flow to meet the trial period requirements and maintain long-term homeownership.

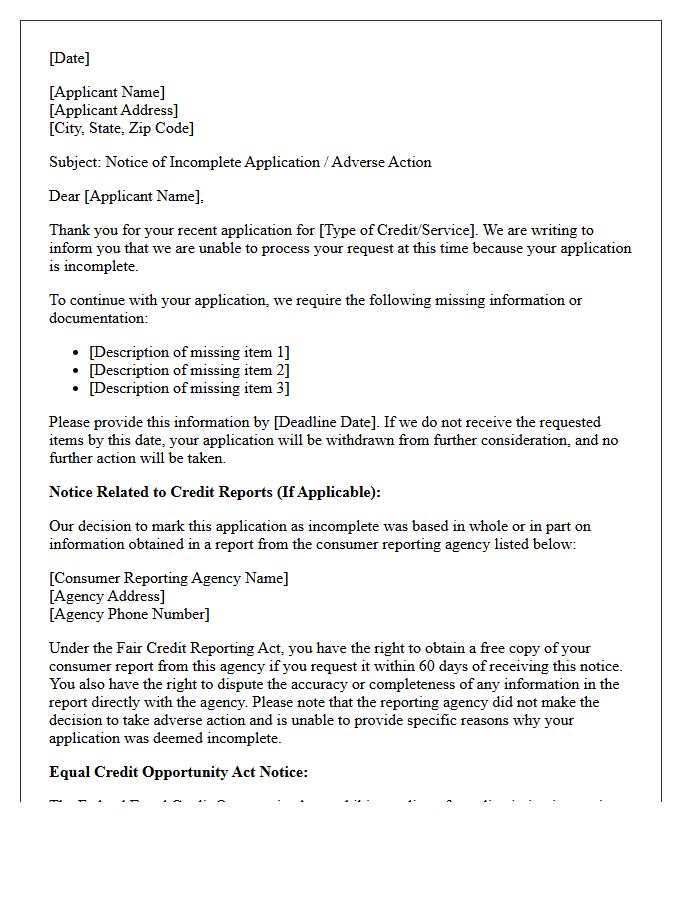

Incomplete Application Adverse Action Modification Letter

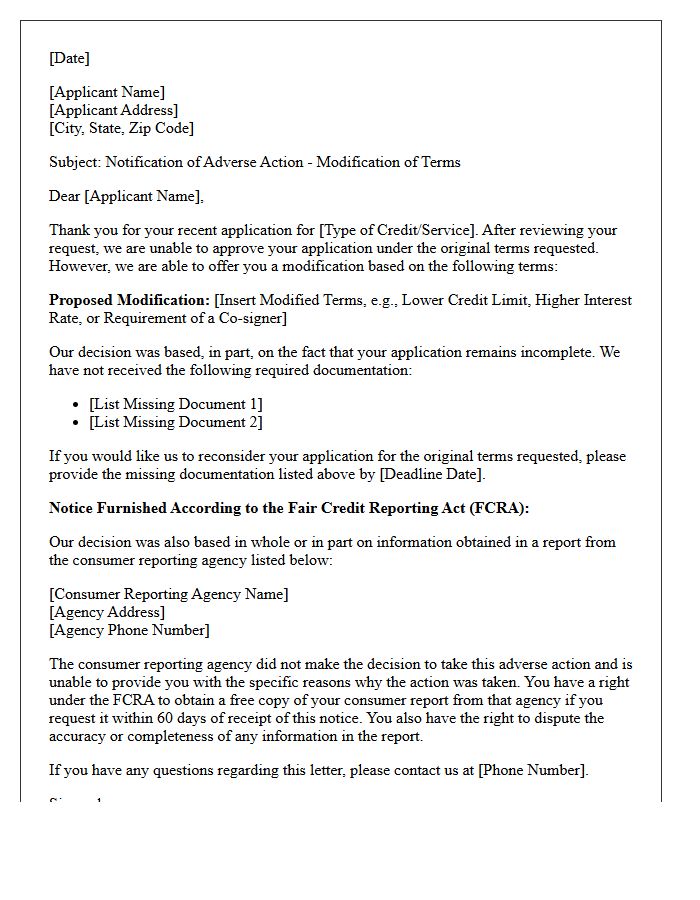

An Incomplete Application Adverse Action Modification Letter is a formal notice sent to credit applicants when a decision cannot be made due to missing information. Under the Equal Credit Opportunity Act (ECOA), lenders must provide a written explanation if they deny or modify credit terms. This specific letter acts as an adverse action notice, informing the consumer of the specific deficiencies in their file. It ensures regulatory compliance by giving the applicant a chance to provide necessary documentation before a final denial is issued, maintaining transparency throughout the lending process.

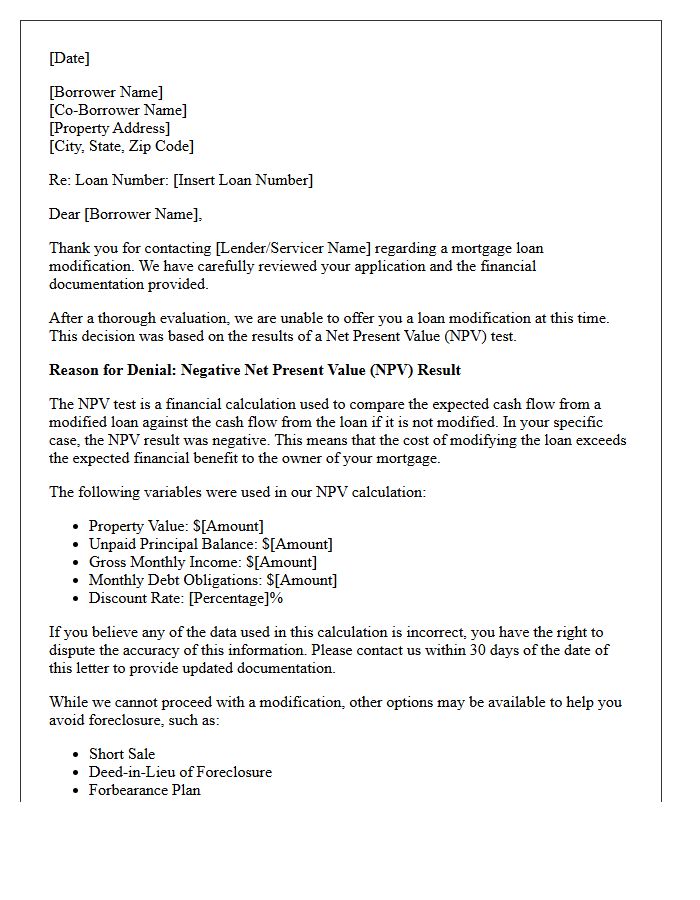

Negative Net Present Value Mortgage Modification Denial Letter

Receiving a Negative Net Present Value (NPV) denial letter means your mortgage servicer determined that foreclosing is more profitable for the investor than modifying your loan. This financial calculation compares the expected cash flows of a modified payment plan against the recovery value of a foreclosure sale. If you believe your income or property value was inaccurately reported, you have a right to appeal. Challenging the inputs used in the NPV test is the most effective way to overturn a modification denial and secure more affordable housing payments.

Missing Documentation Adverse Action Modification Letter

When issuing a Missing Documentation Adverse Action Modification Letter, creditors must clearly notify applicants that their request was denied due to an incomplete application. This legal notice is required under the Equal Credit Opportunity Act to ensure transparency. It must specify the exact missing information needed to make a decision and provide a deadline for submission. Failure to provide this written disclosure can lead to regulatory non-compliance. Always include a statement of the applicant's rights and the specific reasons for the credit denial or modification to maintain legal standards.

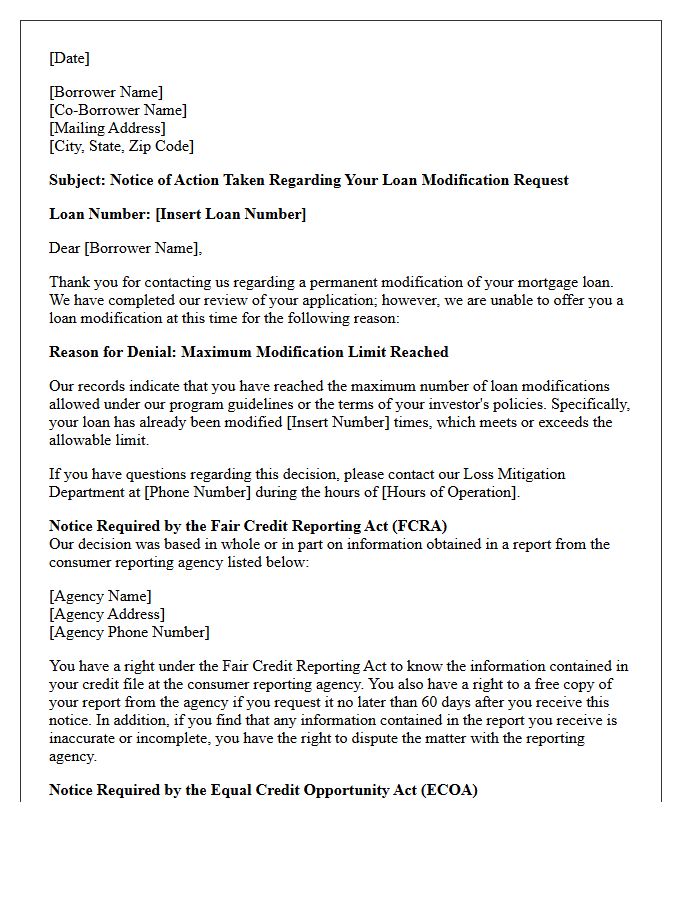

Maximum Modification Limit Reached Adverse Action Letter

A Maximum Modification Limit Reached letter is a formal adverse action notice sent when a borrower has exhausted the total number of permitted loan restructures. Lenders impose these caps to ensure financial stability and mitigate risk. Receiving this document signifies that no further loan modifications are available under current program guidelines, often leading to alternative loss mitigation options or foreclosure. It is crucial to review the letter's specific denial reasons and your right to appeal or seek independent counseling to explore remaining debt relief strategies before legal deadlines pass.

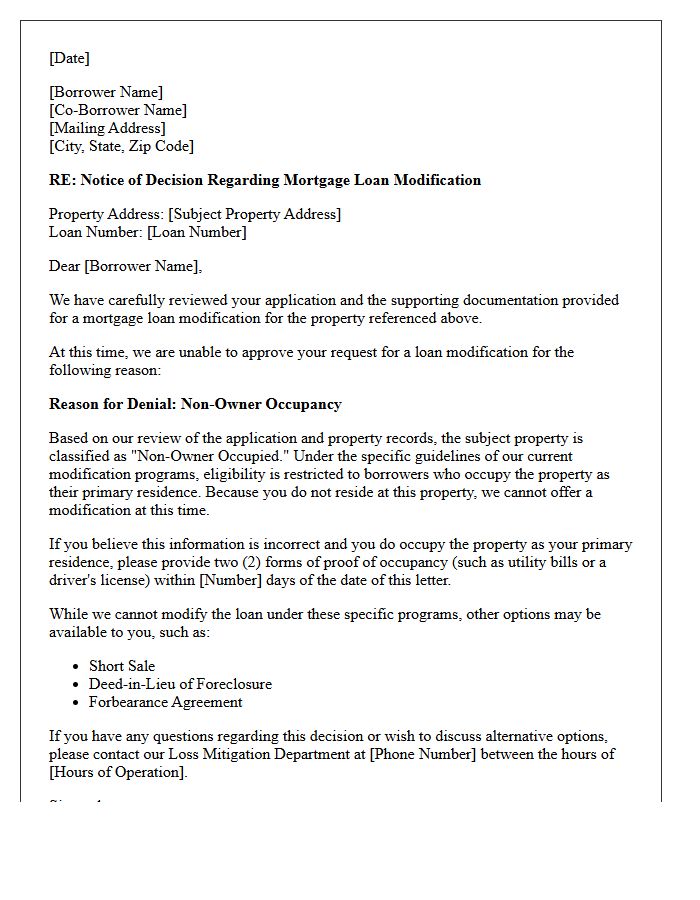

Non-Owner Occupied Property Modification Denial Letter

Receiving a Non-Owner Occupied Property Modification Denial Letter indicates your loan restructuring request was rejected because the residence is an investment property. Lenders often prioritize owner-occupied homes for loss mitigation programs like HAMP or internal flex modifications. This denial typically occurs when a occupancy verification proves the borrower does not reside on-site. To contest this, review the specific reason cited, ensure your investor guidelines allow for rental modifications, and consider alternative options like a short sale or deed-in-lieu to resolve the delinquency status effectively.

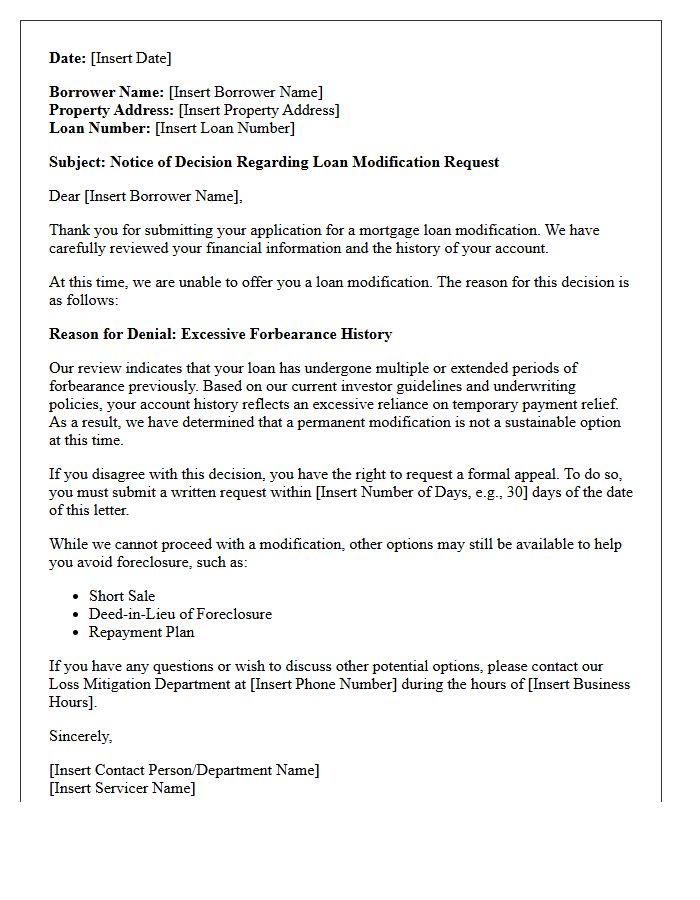

Excessive Forbearance History Modification Denial Letter

An Excessive Forbearance History Modification Denial Letter informs borrowers that their request for a loan restructuring was rejected due to prolonged non-payment periods. Lenders issue this notice when a homeowner has already exhausted the maximum allowed time in forbearance without successfully resuming regular payments. This indicates that the financial instability is viewed as permanent rather than temporary. Receiving this letter means the servicer believes further loan modifications are no longer a viable solution, potentially moving the account toward foreclosure or requiring an alternative liquidation strategy to resolve the debt.

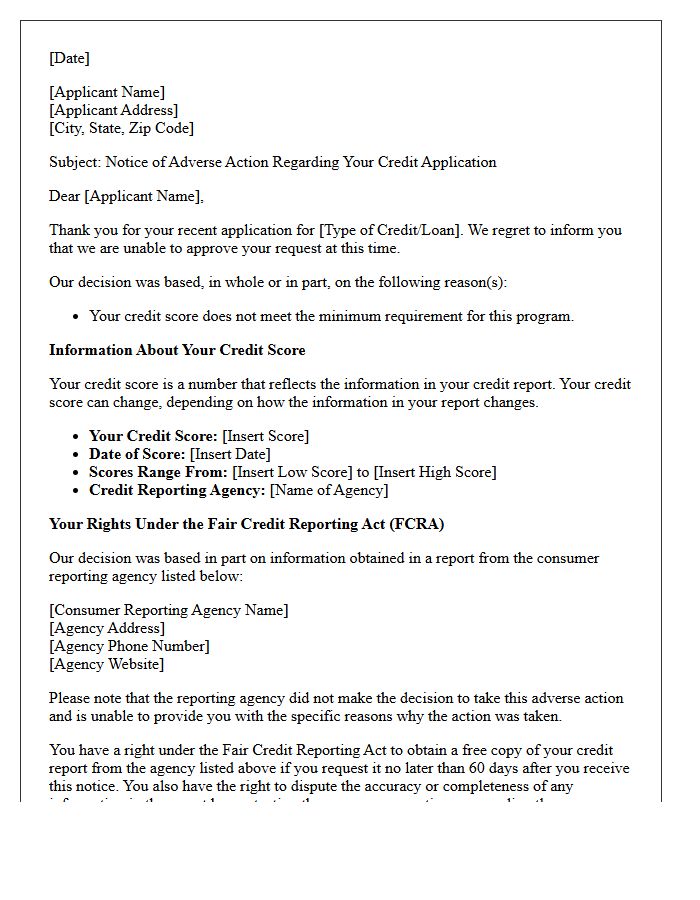

Minimum Credit Score Requirement Adverse Action Letter

An Adverse Action Letter is a formal notice sent when a lender denies your application due to a low credit score. This document is required by law and must disclose the specific minimum credit score requirement you failed to meet. It also identifies the credit bureau that provided the data and outlines your right to a free report. Understanding these reasons allows you to dispute inaccuracies or improve your financial standing for future approvals. Receiving this letter is a critical step in maintaining transparency within the lending process.

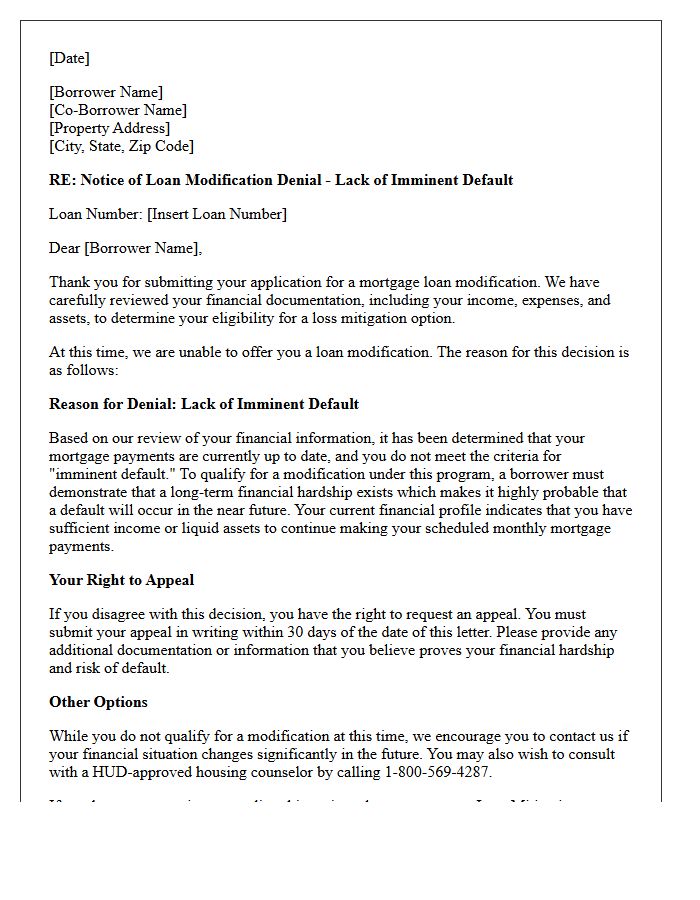

Lack of Imminent Default Modification Denial Letter

A Lack of Imminent Default Modification Denial Letter is issued when a lender determines a borrower is not yet at high risk of missing mortgage payments. This formal notice indicates that your current financial situation does not meet the hardship criteria required for a loan workout. It serves as a legal notification that your request for a proactive modification was rejected because your income or assets appear sufficient to maintain the debt. Receiving this letter means you must continue regular payments or provide additional evidence of an impending financial crisis to appeal the decision.

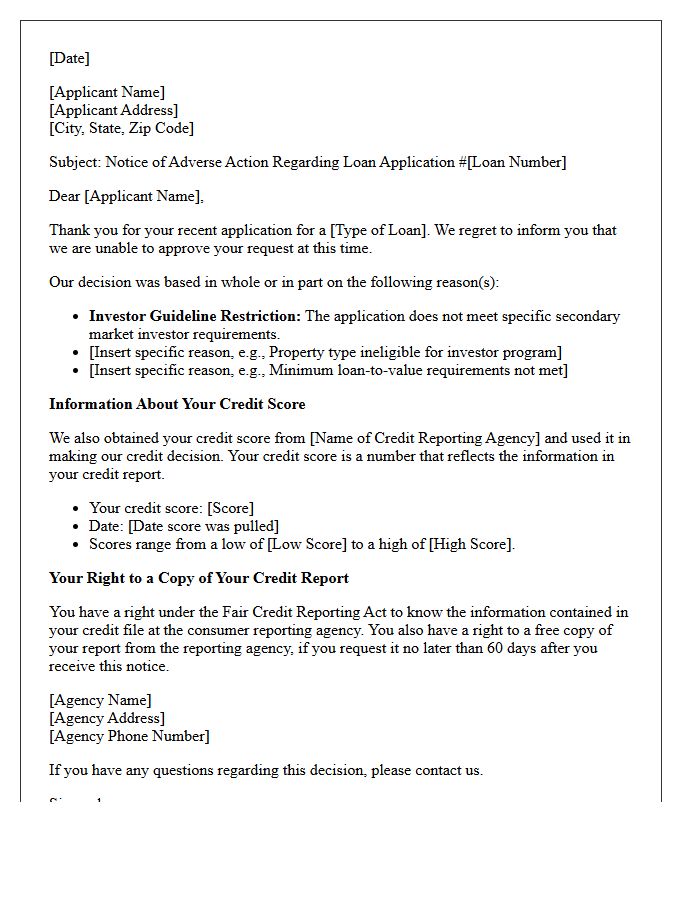

Investor Guideline Restriction Adverse Action Letter

An Adverse Action Letter is a formal notification issued when a lender denies or modifies credit based on specific investor guideline restrictions. These internal or secondary market rules often supercede standard credit scores, focusing on property types or high-risk financial profiles. Receiving this document is crucial because it legally discloses the reason for denial, allowing the applicant to dispute inaccuracies or adjust their strategy. Understanding these regulatory disclosures ensures transparency in the lending process and helps borrowers identify which specific criteria failed to meet investor requirements for loan approval.

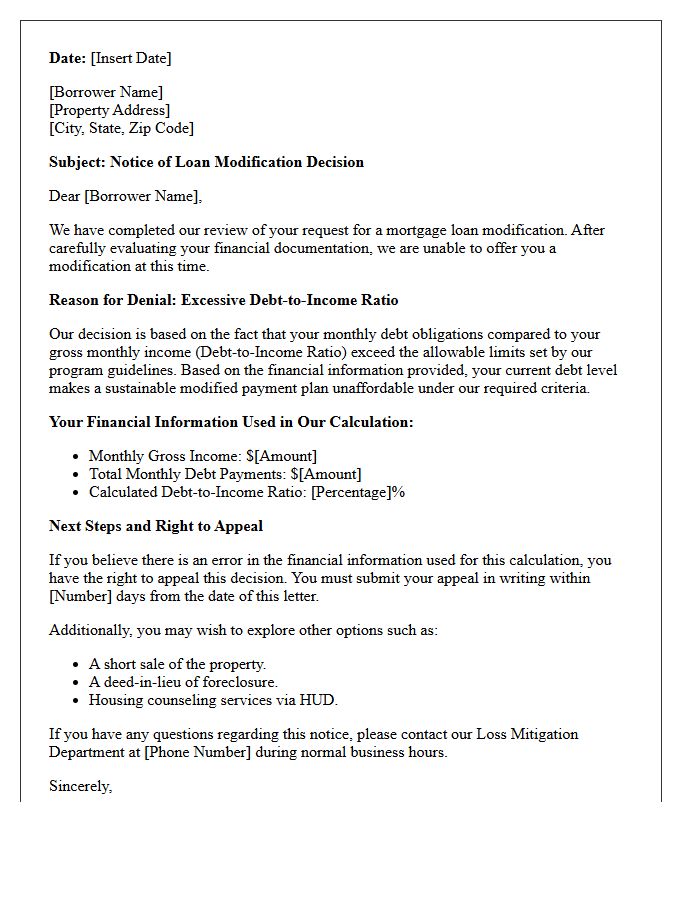

Excessive Debt-to-Income Ratio Modification Denial Letter

Receiving an Excessive Debt-to-Income Ratio Modification Denial Letter indicates that your monthly liabilities are too high relative to your gross income. Lenders use this metric to determine if a restructured mortgage remains unaffordable even after adjustments. To contest this decision, you should review your financial statement for errors, verify all income sources, and consider paying down smaller balances. Understanding this specific DTI threshold is crucial for navigating the appeals process or exploring alternative loss mitigation options to avoid foreclosure and stabilize your long-term housing affordability.

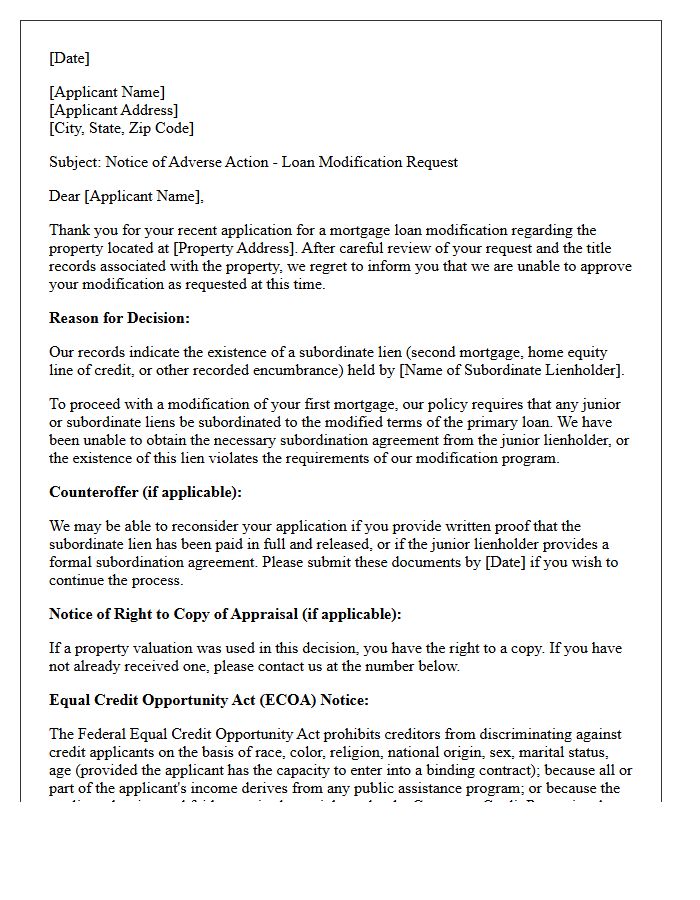

Subordinate Lien Conflict Adverse Action Modification Letter

A Subordinate Lien Conflict Adverse Action Modification Letter notifies borrowers that a requested loan modification was denied due to issues with junior security interests. This occurs when subordinate lienholders refuse to subordinate their claims or when existing terms violate the primary lender's priority requirements. Understanding this document is crucial for resolving title encumbrances that block restructuring efforts. Borrowers must negotiate with secondary lenders or satisfy outstanding debts to clear the conflict, ensuring the senior lien maintains legal precedence during the modification process.

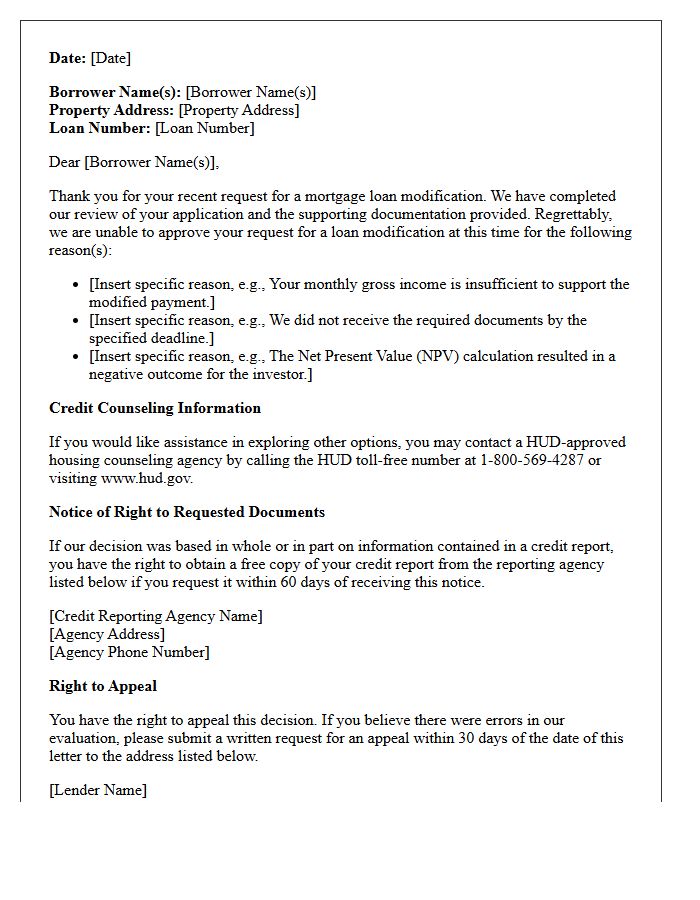

Standard Mortgage Loan Modification Adverse Action Letter

A Standard Mortgage Loan Modification Adverse Action Letter is a formal notice sent to borrowers when a lender denies a request for loan restructuring. It is a legal requirement under the Equal Credit Opportunity Act (ECOA). This document must clearly state the specific reasons for the denial, such as debt-to-income ratios or insufficient property value. Understanding this letter is crucial because it outlines your right to appeal the decision or correct errors in your credit report, providing a final opportunity to prevent potential foreclosure actions.

What is a mortgage loan modification adverse action letter?

An adverse action letter is a formal notice sent by a mortgage servicer to inform a borrower that their application for a loan modification has been denied. This document is required by the Equal Credit Opportunity Act (ECOA) to ensure transparency in lending decisions.

Why did I receive an adverse action letter for my mortgage modification?

You received this letter because your servicer determined you did not meet specific eligibility criteria. Common reasons include "excessive deficit" (insufficient income to support the new payment), "net present value" (NPV) failure, or failing to provide required financial documentation within the specified timeframe.

What information must be included in a loan modification denial notice?

Under federal law, the letter must include the specific reasons for the denial, the name and address of the federal agency that administers compliance, and a disclosure of your right to a credit report if the decision was based on your credit score.

Can I appeal a mortgage loan modification denial?

Yes, borrowers generally have 14 to 30 days to file a formal appeal if they believe the servicer made an error or if they can provide new financial information. The adverse action letter will outline the specific steps and deadlines required to contest the decision.

Does receiving an adverse action letter mean I will face foreclosure?

Not necessarily. While a denial means the specific modification was rejected, the letter may suggest other loss mitigation options such as a short sale, deed-in-lieu of foreclosure, or a repayment plan. It is critical to contact your servicer immediately to discuss these alternatives.

Comments