When a candidate rejects a proposed salary or benefit adjustment, employers must issue an Adverse Action Letter to formally withdraw the job offer. This document ensures legal compliance and clear communication when negotiations fail to reach an agreement. Understanding the regulatory requirements protects your organization during the hiring process. Below are some ready to use templates.

Image cover: Navigating Adverse Action: Templates for Declined Counteroffer Terms

Letter Samples List

- Adverse Action Letter for Unaccepted Mortgage Counteroffer

- Notice of Adverse Action Letter for Declined Loan Terms

- Unaccepted Counteroffer Adverse Action Letter for Home Buyers

- Mortgage Lender Adverse Action Letter for Expired Counteroffer

- Final Adverse Action Letter for Unaccepted Refinance Terms

- Adverse Action Letter for Rejected Loan Amount Counteroffer

- Unaccepted Interest Rate Counteroffer Adverse Action Letter

- Mortgage Application Adverse Action Letter for Declined Terms

- Compliance Adverse Action Letter for Unaccepted Mortgage Counteroffer

- Adverse Action Letter for Unaccepted Down Payment Counteroffer

- Residential Mortgage Adverse Action Letter for Refused Counteroffer

- Standard Adverse Action Letter for Unaccepted Loan Counteroffer

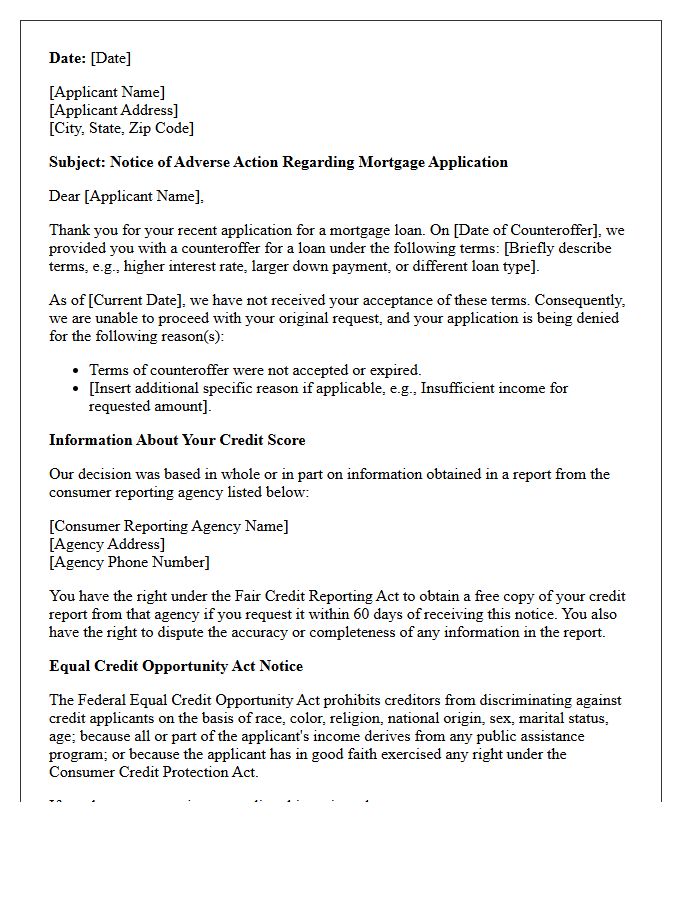

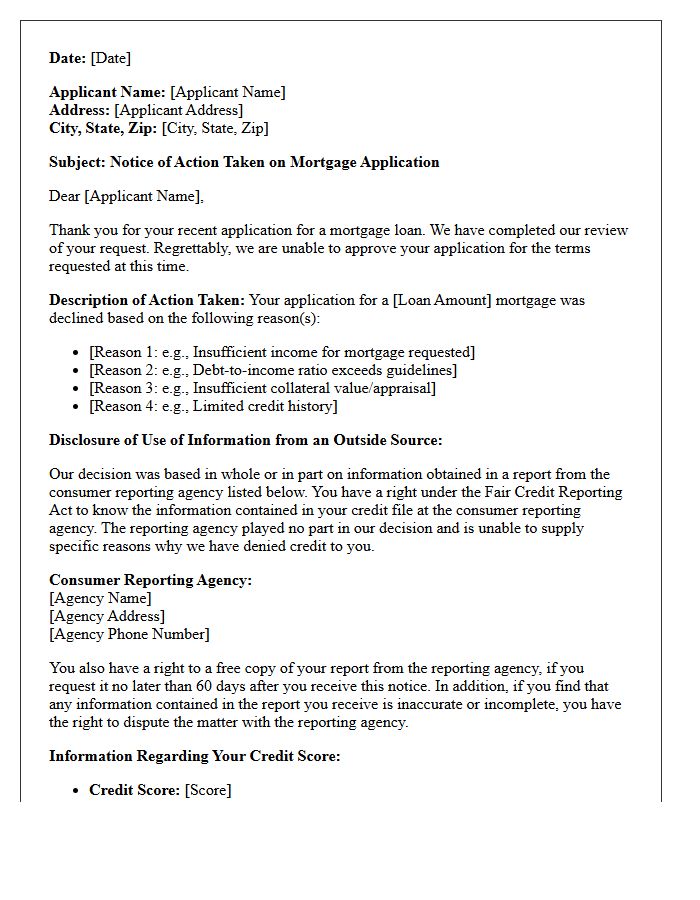

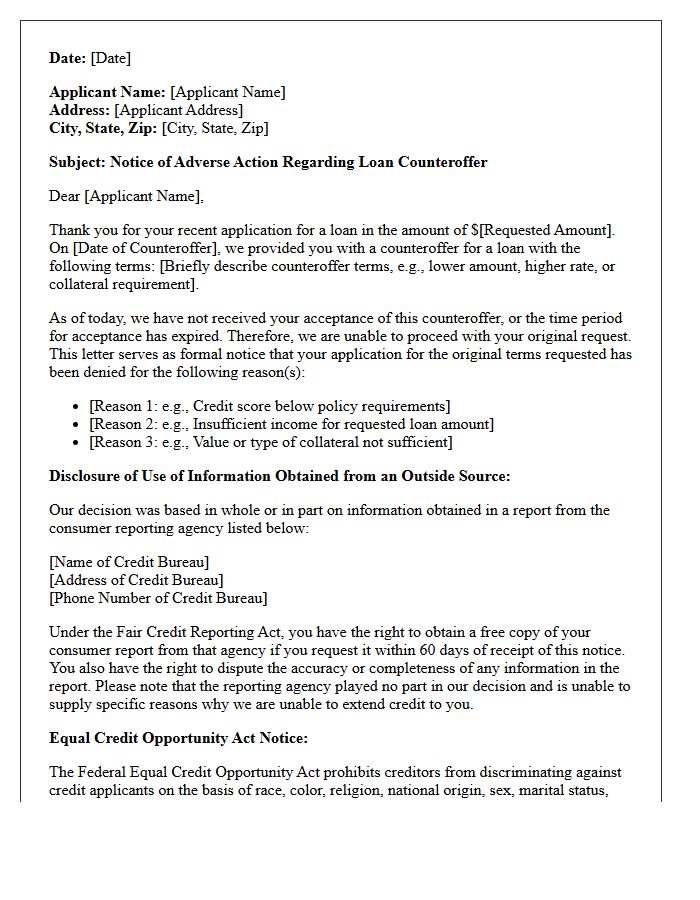

Adverse Action Letter for Unaccepted Mortgage Counteroffer

If a lender proposes a mortgage counteroffer that you do not accept, they are legally required to issue an Adverse Action Letter. Under the Equal Credit Opportunity Act, this document provides transparency by explaining the specific reasons why your original loan terms were denied. It serves as a consumer protection tool, ensuring you understand factors like credit scores or debt ratios that influenced the decision. Receiving this letter does not necessarily damage your credit, but it offers essential insights to help you improve your financial standing for future applications.

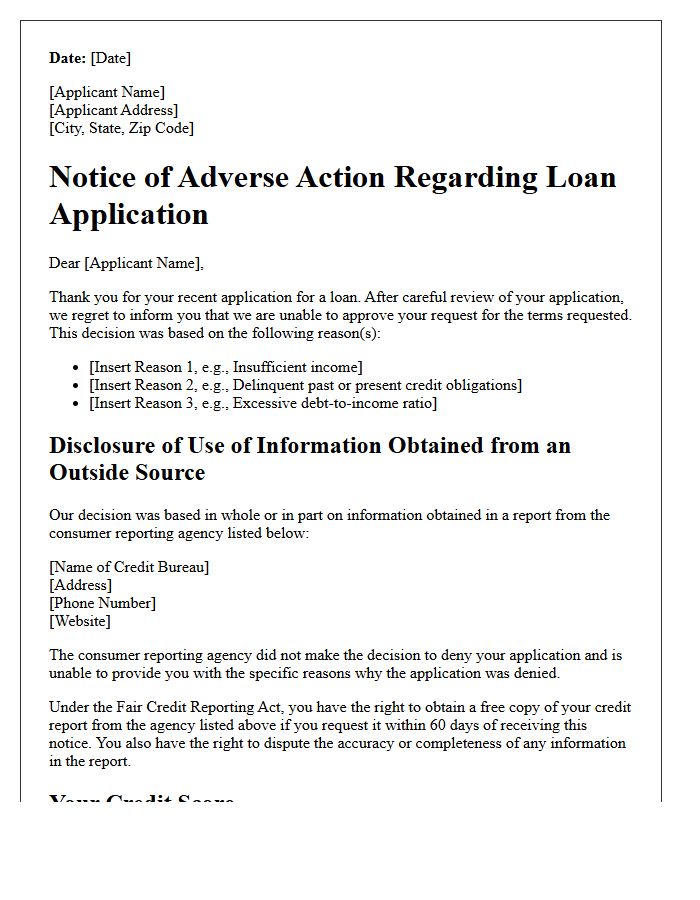

Notice of Adverse Action Letter for Declined Loan Terms

A Notice of Adverse Action is a legally required document issued when a lender denies your credit application or offers less favorable terms. It must provide specific reasons for the rejection, such as a low credit score or insufficient income. This letter ensures transparency under the Equal Credit Opportunity Act. It also grants you the right to request a free copy of your credit report from the mentioned bureau within 60 days. Reviewing this notice is essential for identifying errors and improving your financial profile for future loan approval.

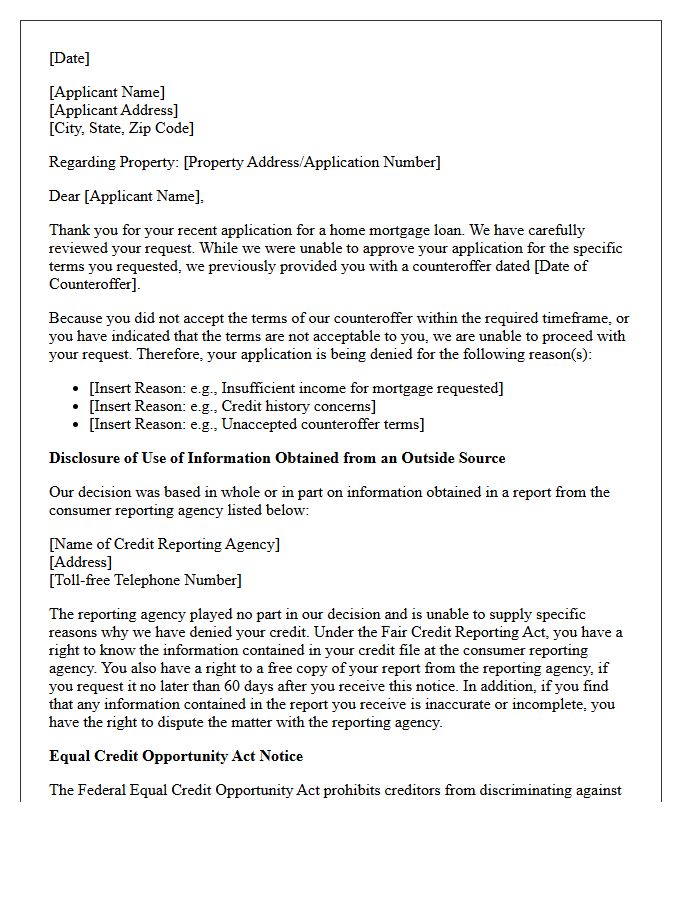

Unaccepted Counteroffer Adverse Action Letter for Home Buyers

An Adverse Action Letter is a formal notice lenders must provide when they cannot fulfill your specific loan terms. In real estate, if a lender presents a counteroffer with different rates or down payment requirements that you decline or fail to accept, they are legally required to issue this document. It outlines the specific reasons for the original denial, such as credit scores or debt ratios. Receiving this letter is a standard regulatory step under ECOA guidelines, ensuring transparency and protecting your consumer rights during the home buying process.

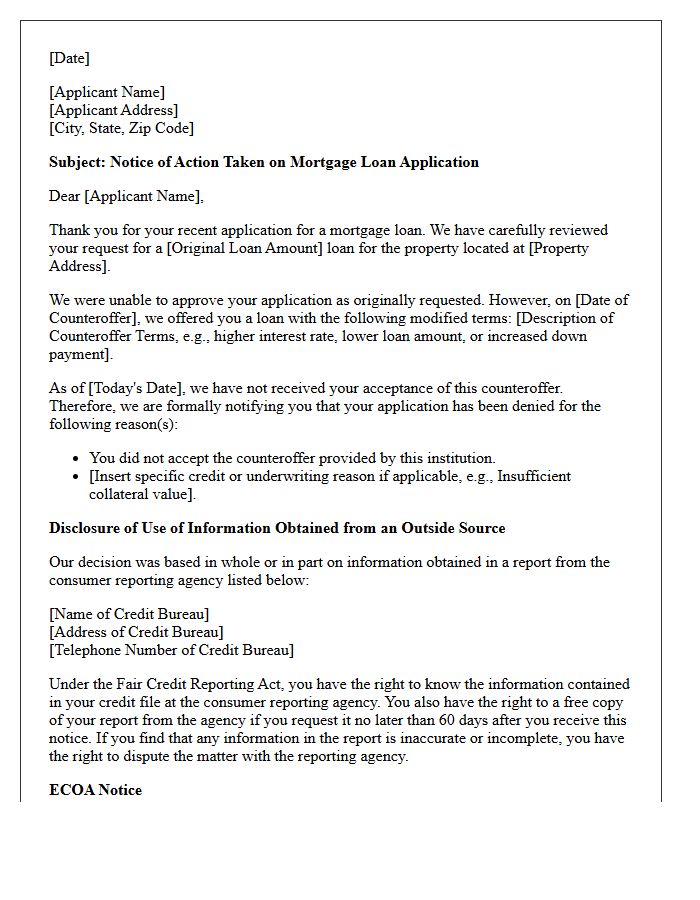

Mortgage Lender Adverse Action Letter for Expired Counteroffer

A mortgage lender issues an Adverse Action Letter when a counteroffer expires without buyer acceptance. This formal notice is legally required under the Equal Credit Opportunity Act (ECOA) to explain why the original loan terms were denied. It highlights that the lender proposed alternative financing-such as a higher interest rate or larger down payment-which the applicant failed to accept within the specified timeframe. Receiving this document signifies the formal rejection of the application, ensuring transparency regarding credit decisions and protecting consumer rights during the home financing process.

Final Adverse Action Letter for Unaccepted Refinance Terms

A Final Adverse Action Letter is a formal notice issued when a mortgage refinance application is denied because the applicant rejected the offered terms. This document is a legal requirement under the Equal Credit Opportunity Act (ECOA). It must clearly outline the specific reasons for the decision, such as insufficient income, low credit scores, or a high debt-to-income ratio. Receiving this letter is crucial for transparency, allowing borrowers to understand their financial standing and identify corrective actions needed to qualify for better loan products in the future.

Adverse Action Letter for Rejected Loan Amount Counteroffer

An Adverse Action Letter is a mandatory legal notice issued when a lender denies your original loan request. If you receive a counteroffer for a lower amount and choose to reject it, the lender must provide this document explaining the specific reasons for the denial. It typically highlights factors like credit scores or insufficient income. Reviewing this letter is essential because it grants you the right to a free credit report, allowing you to dispute inaccuracies and improve your financial standing for future applications.

Unaccepted Interest Rate Counteroffer Adverse Action Letter

An Unaccepted Interest Rate Counteroffer Adverse Action Letter is a legal notice required when a lender declines your original loan request but offers different terms. If you reject or fail to respond to this counteroffer, the lender must issue this document. It serves as a formal rejection notice under the Equal Credit Opportunity Act, explaining the specific credit reasons for the decision and providing your credit score disclosure. Receiving this letter is mandatory to ensure transparency and protect consumer rights during the lending process.

Mortgage Application Adverse Action Letter for Declined Terms

A mortgage application adverse action letter is a formal notice required by law when a lender denies credit or offers less favorable terms. This document must clearly state the specific reasons for the declined terms, such as a low credit score or insufficient income. Receiving this letter allows you to request a free copy of your credit report within sixty days to dispute inaccuracies. Reviewing these details is essential for improving your financial profile and successfully reapplying for a home loan in the future.

Compliance Adverse Action Letter for Unaccepted Mortgage Counteroffer

When a lender provides a mortgage counteroffer that the applicant does not accept, federal law requires a Compliance Adverse Action Letter. Under the Equal Credit Opportunity Act (ECOA), this notice must be sent if the borrower fails to respond or formally rejects the revised terms within 90 days. The letter must clearly state the specific reasons for the credit decision or inform the applicant of their right to request those reasons. Ensuring regulatory disclosure protects lenders from legal non-compliance and ensures transparency regarding the applicant's creditworthiness and loan status.

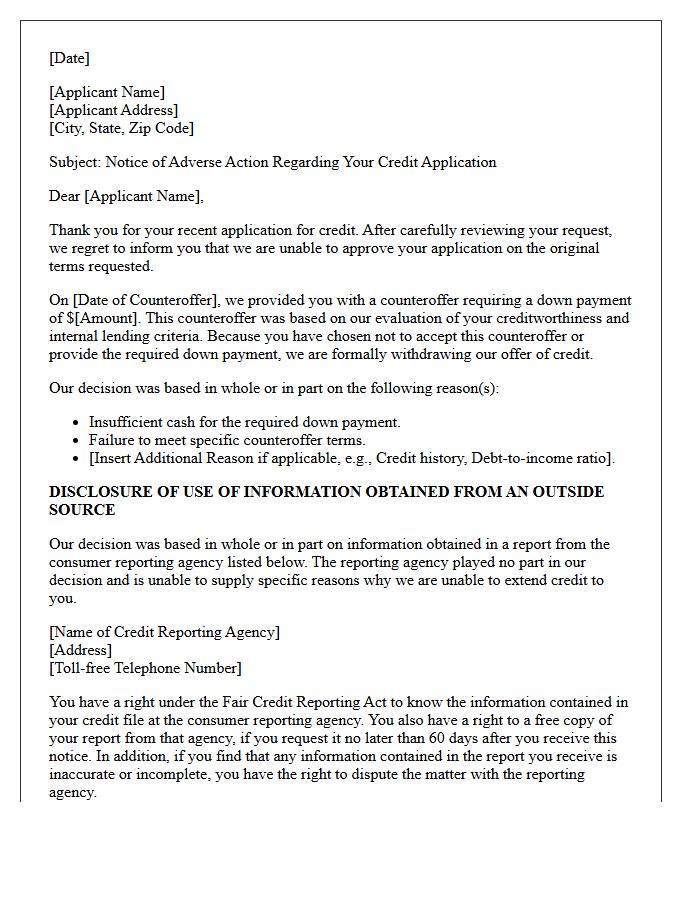

Adverse Action Letter for Unaccepted Down Payment Counteroffer

An Adverse Action Letter is a mandatory legal notice required when a lender rejects your original loan terms. If a bank issues a counteroffer requiring a higher down payment and you do not accept it, the lender must provide this formal disclosure. It explains the specific reasons for the denial, such as credit score issues or income instability. This document ensures transparency under the Equal Credit Opportunity Act, allowing you to understand why the financing was not approved as requested and how to improve your future eligibility.

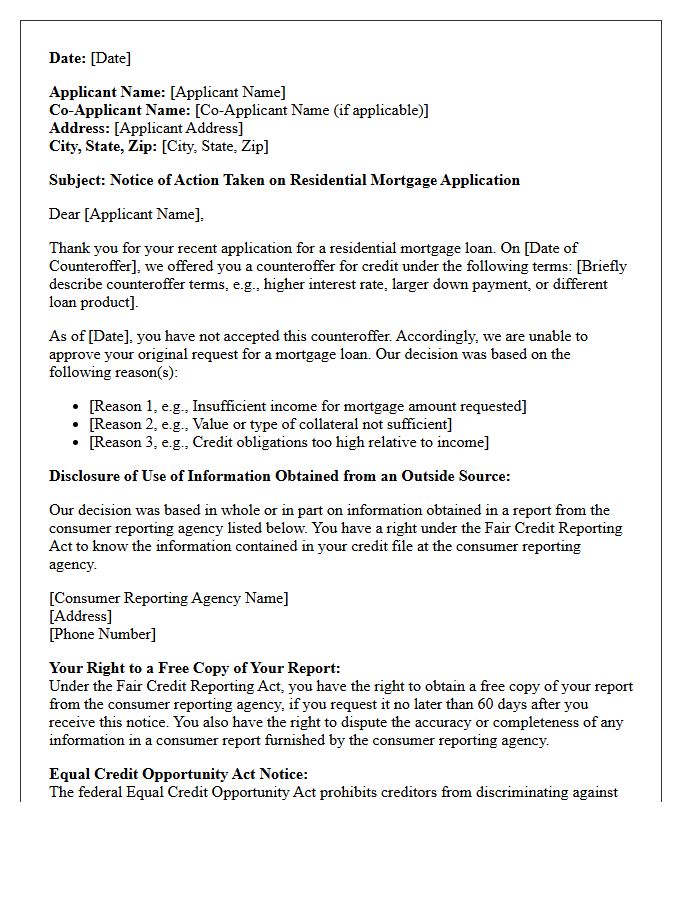

Residential Mortgage Adverse Action Letter for Refused Counteroffer

A Residential Mortgage Adverse Action Letter is a required legal notice issued when a lender denies your original loan request. If you receive a refused counteroffer notice, it means the lender proposed alternative terms-such as a higher interest rate or lower loan amount-which you declined or failed to accept. This document must clearly state the specific reasons for the denial, such as low credit scores or insufficient collateral. Under the Equal Credit Opportunity Act, this transparency ensures borrowers understand why their application was unsuccessful and allows them to dispute potential inaccuracies.

Standard Adverse Action Letter for Unaccepted Loan Counteroffer

A Standard Adverse Action Letter is a mandatory legal notice issued when a lender provides a counteroffer that the applicant chooses not to accept. Under the Equal Credit Opportunity Act (ECOA), this document ensures transparency by detailing the specific reasons for the original credit denial. It often includes information regarding the credit score used and the reporting agency involved. If a consumer ignores or rejects the modified terms, the lender must provide this formal disclosure within ninety days to remain compliant with federal consumer protection regulations.

What is an adverse action letter for an unaccepted counteroffer?

An adverse action letter is a formal notice sent to a loan applicant when a lender provides a counteroffer (such as a higher interest rate or lower loan amount) that the applicant subsequently declines or fails to accept within the required timeframe.

Is a lender required to send an adverse action notice if I reject their counteroffer?

Yes. Under the Equal Credit Opportunity Act (ECOA) and Regulation B, if a lender offers credit on terms different from those requested and the applicant does not accept them, the lender must provide a formal adverse action notice explaining the decision.

What specific information must be included in this type of adverse action letter?

The letter must include the specific reasons why the original terms were denied, the name and address of the federal agency that administers compliance, and a statement of the applicant's rights under the Fair Credit Reporting Act (FCRA) if credit data influenced the decision.

How long does a lender have to send the notice after I decline a counteroffer?

According to Regulation B, a lender generally has 90 days to provide an adverse action notice after notifying an applicant of a counteroffer that was not accepted or acted upon by the consumer.

Can an adverse action notice be delivered electronically?

Yes, lenders can deliver adverse action notices electronically, provided they comply with the requirements of the Electronic Signatures in Global and National Commerce (E-Sign) Act, which includes obtaining prior consent from the applicant.

Comments