A Conditional Approval Pending Debt Payoff Verification Letter is a formal document issued by lenders requiring proof that specific liabilities are settled before finalizing a mortgage. This step ensures your debt-to-income ratio meets underwriting guidelines for loan approval. Understanding how to document these payments is essential for a smooth closing process. To help you get started, below are some ready to use template.

Image cover: Clearing Debt for Mortgage Approval: Verification Letter Templates and Guide

Letter Samples List

- Conditional Mortgage Approval Pending Debt Payoff Letter

- Debt Payoff Verification and Conditional Approval Letter

- Conditional Loan Approval and Liability Payoff Verification Letter

- Pending Debt Clearance Conditional Approval Letter

- Mortgage Conditional Approval Subject to Debt Settlement Letter

- Credit Account Payoff Verification Conditional Approval Letter

- Conditional Financing Approval Pending Debt Closure Letter

- Debt Resolution Verification and Conditional Mortgage Letter

- Outstanding Balance Payoff Verification Conditional Approval Letter

- Conditional Commitment Pending Creditor Payoff Verification Letter

- Mortgage Underwriting Conditional Approval and Debt Payoff Letter

- Conditional Home Loan Approval Subject to Debt Payoff Letter

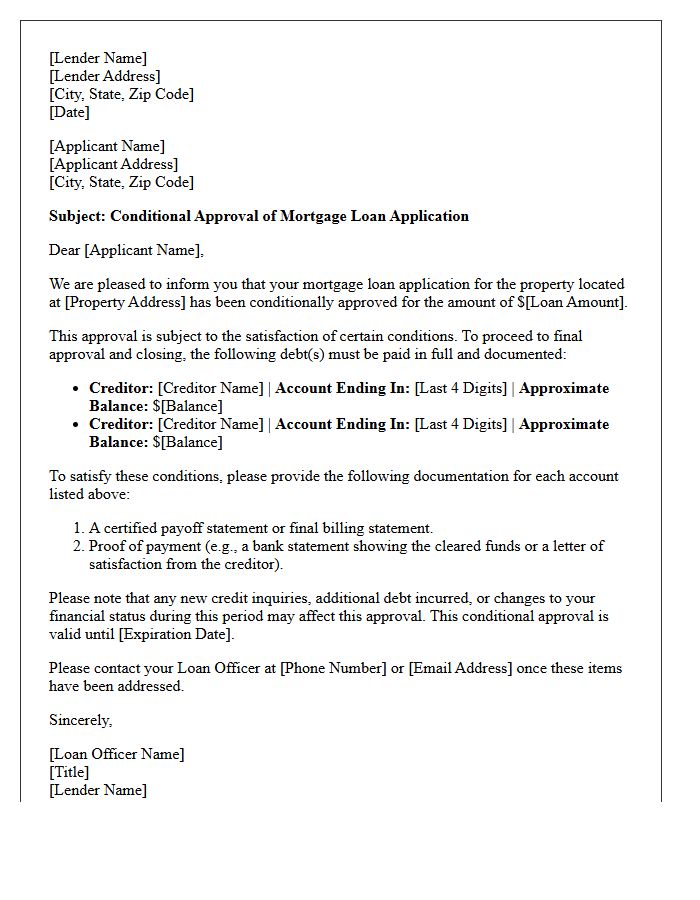

Conditional Mortgage Approval Pending Debt Payoff Letter

A conditional mortgage approval signifies a lender will grant your loan once specific criteria are met. If a debt payoff letter is required, you must provide official documentation proving a specific balance has been settled. Lenders use this to lower your debt-to-income ratio, ensuring you meet affordability guidelines. To avoid delays, ensure the letter is from the creditor on official letterhead, showing a zero balance or account closure. Do not close accounts or pay large sums without consulting your loan officer, as this can impact your credit score or cash reserves.

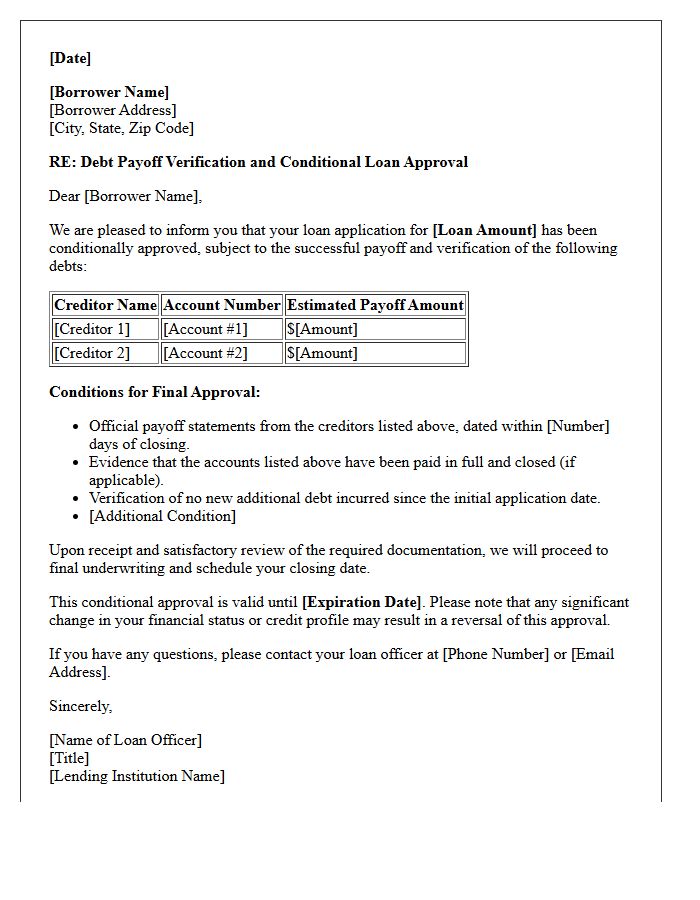

Debt Payoff Verification and Conditional Approval Letter

A Debt Payoff Verification is a crucial document confirming that a specific liability has been settled in full. Lenders require this to ensure your debt-to-income ratio qualifies for financing. Once verified, a creditor issues a Conditional Approval Letter, which outlines the remaining requirements needed for final loan authorization. This letter serves as a formal bridge, signaling that your application is approved provided you meet specific underwriting stipulations. Monitoring these documents ensures a smooth closing process and validates your financial eligibility for new credit or a mortgage.

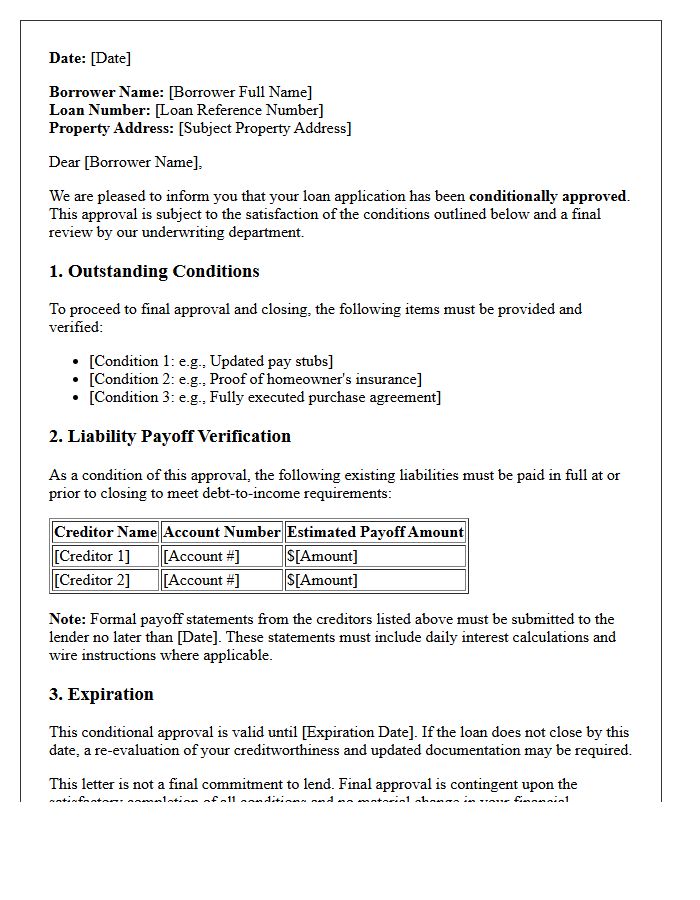

Conditional Loan Approval and Liability Payoff Verification Letter

A Conditional Loan Approval indicates a lender will provide financing provided specific criteria are met. A critical requirement is the Liability Payoff Verification Letter, which serves as official documentation confirming the exact balance needed to clear existing debts. This process ensures your debt-to-income ratio aligns with underwriting standards. To secure final approval, borrowers must provide these verified statements promptly to prove that outstanding obligations will be settled, thereby reducing financial risk and securing the new mortgage or loan agreement.

Pending Debt Clearance Conditional Approval Letter

A Pending Debt Clearance Conditional Approval Letter is a formal document indicating that a creditor or lender has agreed to clear your outstanding balance, provided specific requirements are met. It serves as a preliminary confirmation, not a final release. To secure full clearance, you must fulfill stated conditions, such as making a final payment or submitting required documentation within a set timeframe. This letter is crucial for credit repair and mortgage applications, as it demonstrates progress toward financial resolution. Always retain this document until you receive a final settlement confirmation.

Mortgage Conditional Approval Subject to Debt Settlement Letter

A mortgage conditional approval subject to a debt settlement letter means the lender has verified your application but requires proof of resolved liabilities before final funding. This condition highlights that financial risk must be mitigated by showing creditors have accepted specific payment terms to close outstanding accounts. You must provide a formal letter from the creditor confirming the settled amount and zero balance. Failing to submit this legal documentation can stall your closing process or lead to a loan denial, as it directly impacts your final debt-to-income ratio.

Credit Account Payoff Verification Conditional Approval Letter

A Credit Account Payoff Verification Conditional Approval Letter is a formal document issued by lenders during mortgage processing. It specifies that your loan is approved conditionally, provided you provide certified proof that specific debts have been paid in full. This ensures your debt-to-income ratio meets underwriting guidelines. To satisfy this requirement, you must submit an official payoff statement or a zero-balance letter from the creditor. Final funding remains contingent upon the successful verification of these balances being cleared to mitigate financial risk for the financial institution.

Conditional Financing Approval Pending Debt Closure Letter

A Conditional Financing Approval Pending Debt Closure Letter is a lender's commitment to provide funding only after specific liabilities are settled. This document ensures the borrower's debt-to-income ratio meets strict underwriting standards. It serves as a critical safeguard for financial institutions, requiring documented proof that existing balances are closed before final loan disbursement. Understanding this condition is essential for homebuyers and business owners to secure their mortgage or commercial credit by streamlining their financial obligations during the final approval phase.

Debt Resolution Verification and Conditional Mortgage Letter

A Debt Resolution Verification is a formal document confirming that previous financial obligations are settled or managed through a repayment plan. This is critical for obtaining a Conditional Mortgage Letter, which outlines the specific requirements a borrower must meet before final loan approval. Lenders use these documents to ensure debt-to-income ratios are accurate and that all credit hurdles are cleared. Providing verified proof of resolution ensures your mortgage application remains valid, helping you secure financing by demonstrating financial stability and meeting the lender's strict closing conditions.

Outstanding Balance Payoff Verification Conditional Approval Letter

An Outstanding Balance Payoff Verification Conditional Approval Letter is a formal document issued by lenders during the mortgage process. It confirms your application is approved, provided you settle specific debts and provide proof of payment. This requirement ensures your debt-to-income ratio meets lending guidelines before final funding. To satisfy this condition, you must submit an official zero-balance statement or a satisfaction letter from the creditor. Understanding this document is vital, as failing to verify the payoff can delay your loan closing or result in a final denial.

Conditional Commitment Pending Creditor Payoff Verification Letter

A Conditional Commitment Pending Creditor Payoff Verification Letter is a lender's pledge to approve a loan once debt satisfaction is confirmed. It signifies that the borrower is qualified, provided specific existing liabilities are paid in full to meet debt-to-income requirements. This document outlines the mandatory documentation needed from creditors to verify zero balances. It is a critical milestone in the underwriting process, ensuring that the borrower's financial obligations are accurately cleared before the final loan funding occurs. Proper verification protects both the lender and the applicant's closing timeline.

Mortgage Underwriting Conditional Approval and Debt Payoff Letter

Receiving a conditional approval means an underwriter has reviewed your mortgage application and will approve the loan once specific requirements are met. A frequent condition is providing a debt payoff letter. This official document from a creditor confirms the exact balance needed to close an account. Underwriters use this to ensure your debt-to-income ratio meets lending guidelines. You must provide proof that these debts were paid during or before closing to satisfy the condition. Timely submission of these documents is essential to securing final loan approval and proceeding to your scheduled closing date.

Conditional Home Loan Approval Subject to Debt Payoff Letter

A conditional home loan approval subject to a debt payoff letter requires the borrower to eliminate specific liabilities before closing. Lenders issue this condition to lower your debt-to-income ratio, ensuring you meet strict affordability guidelines. You must provide official documentation from creditors confirming the balance is paid in full. Do not close these accounts without consulting your loan officer, as it may impact your credit score. Timely submission of this letter is critical to securing final loan approval and meeting your scheduled closing date without delays.

What is a Conditional Approval Pending Debt Payoff Verification Letter?

A Conditional Approval Pending Debt Payoff Verification Letter is a document issued by a mortgage lender stating that a loan application is approved, provided the borrower pays off specific debts and submits official proof of the zero balance before closing.

Why do lenders require debt payoff verification for mortgage approval?

Lenders require this verification to ensure a borrower's Debt-to-Income (DTI) ratio meets the necessary guidelines. By paying off outstanding balances, the borrower reduces their monthly liabilities, which can lower the lender's risk and qualify the borrower for a higher loan amount.

What documents serve as valid proof for a debt payoff verification?

Valid proof typically includes a final settlement statement, a paid-in-full letter from the creditor, or a zero-balance statement. In some cases, a lender may accept a "credit supplement" where a third-party agency verifies the payoff directly with the creditor.

Can I use a credit card statement as proof of debt payoff?

A standard credit card statement showing a payment was made may not be sufficient on its own. Most lenders require a formal verification letter or an updated account statement specifically showing a $0 balance and a status of "paid" or "closed" to satisfy the condition.

How does a debt payoff verification impact my mortgage closing timeline?

Failure to provide a debt payoff verification letter promptly can delay your "Clear to Close." It is essential to settle the required accounts early in the underwriting process to allow time for the creditor to issue the letter and the lender to verify the updated financial status.

Comments