A Non-Warrantable Condominium Conditional Approval Letter outlines the specific requirements a lender needs to clear before financing a property that falls outside standard Fannie Mae or Freddie Mac guidelines. This document is essential for securing funding on unique condo projects. Understanding these conditions helps streamline the closing process for borrowers and investors. Below are some ready to use template.

Image cover: Mastering Non-Warrantable Condo Financing: Approval Letter Samples and Professional Templates

Letter Samples List

- Primary Residence Non-Warrantable Condominium Conditional Approval Letter

- Investment Property Non-Warrantable Condominium Conditional Approval Letter

- Second Home Non-Warrantable Condominium Conditional Approval Letter

- High Loan-to-Value Non-Warrantable Condominium Conditional Approval Letter

- Portfolio Mortgage Non-Warrantable Condominium Conditional Approval Letter

- Jumbo Loan Non-Warrantable Condominium Conditional Approval Letter

- Pending Litigation Exception Non-Warrantable Condominium Conditional Approval Letter

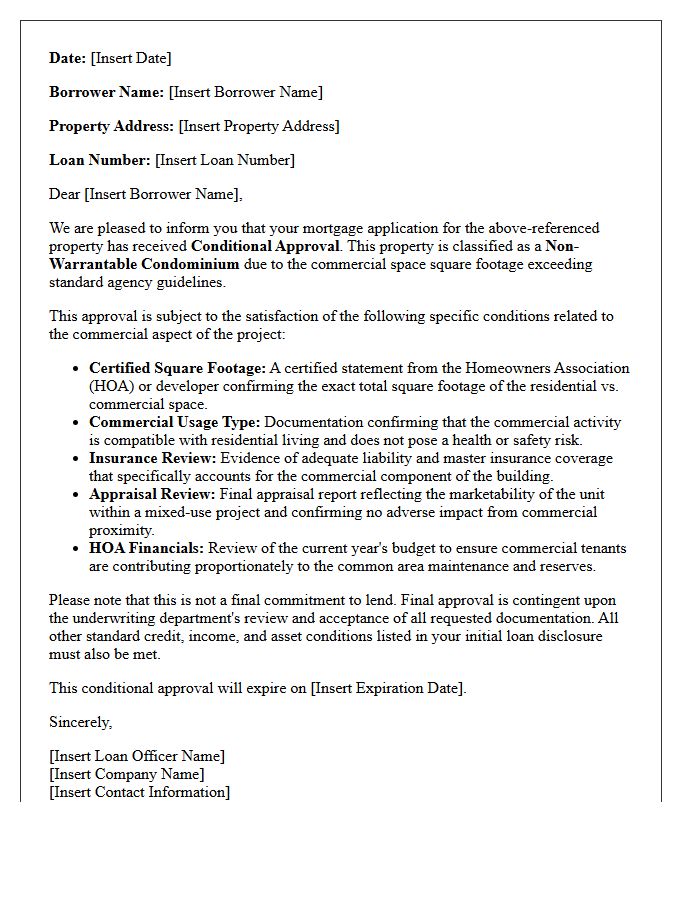

- Commercial Space Ratio Non-Warrantable Condominium Conditional Approval Letter

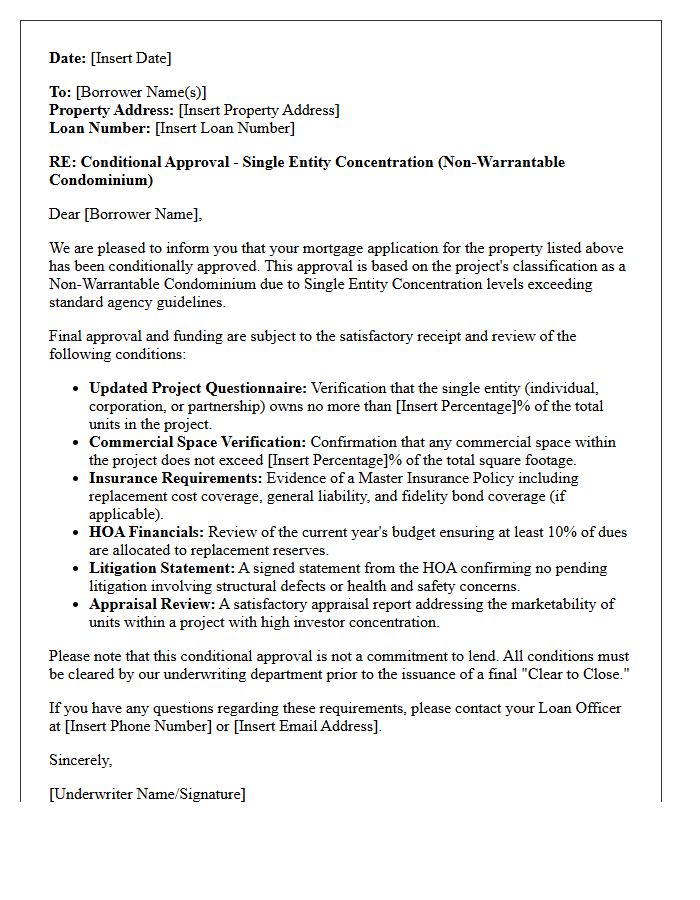

- Single Entity Concentration Non-Warrantable Condominium Conditional Approval Letter

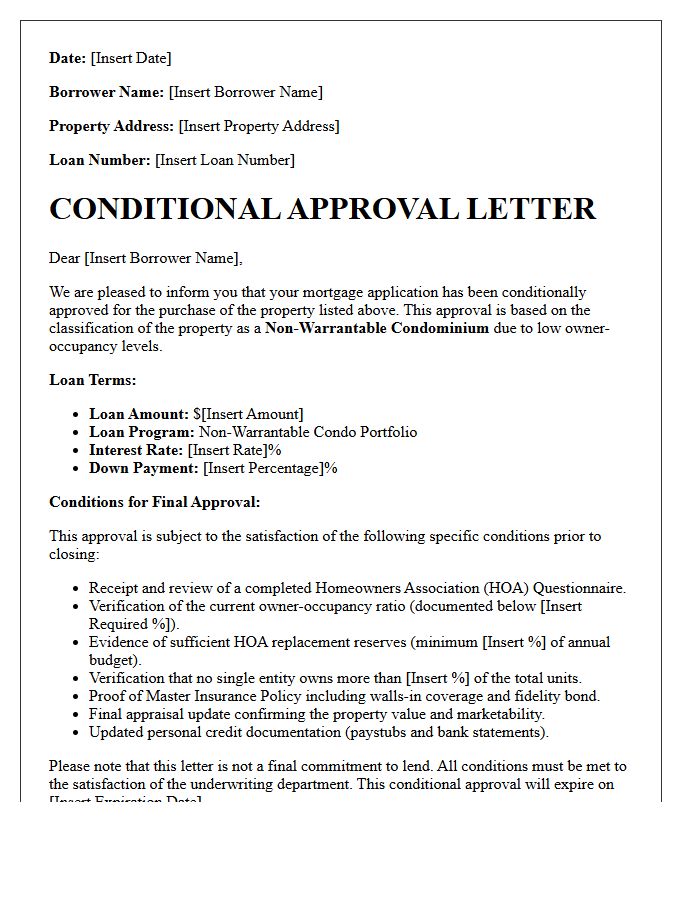

- Low Owner-Occupancy Non-Warrantable Condominium Conditional Approval Letter

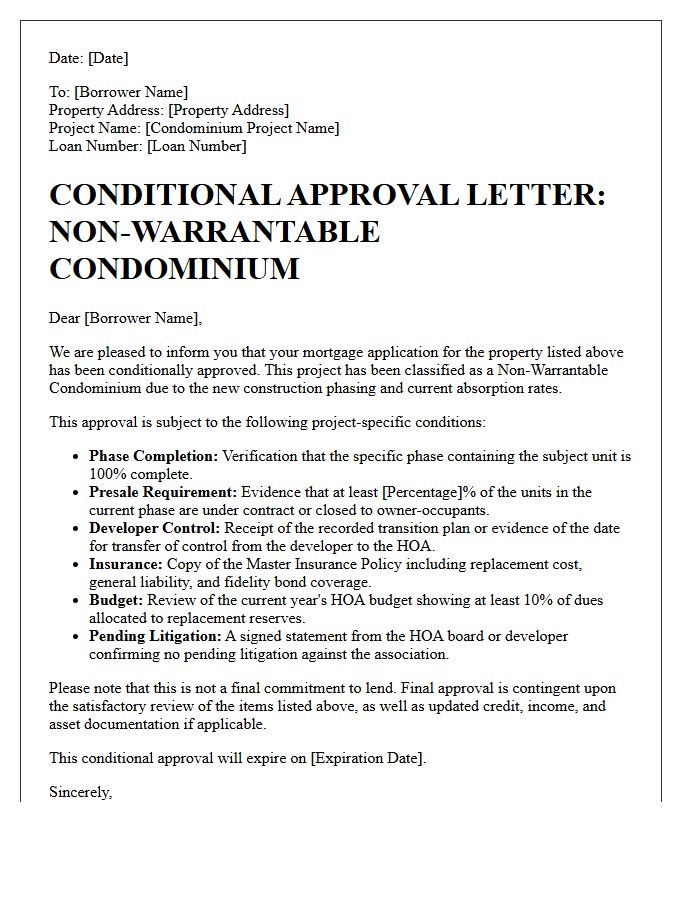

- New Construction Phasing Non-Warrantable Condominium Conditional Approval Letter

- Special Assessment Review Non-Warrantable Condominium Conditional Approval Letter

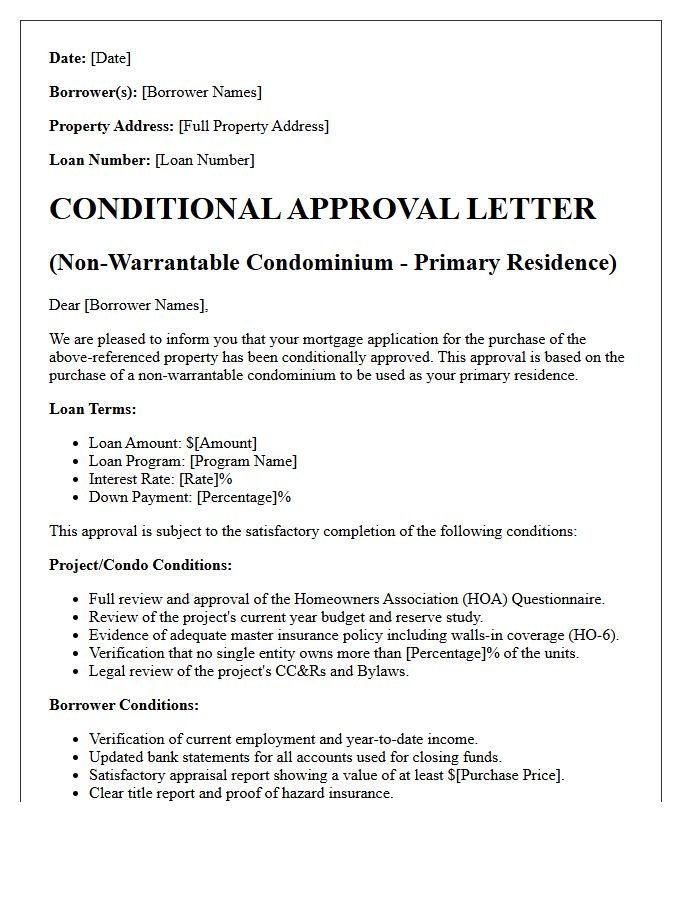

Primary Residence Non-Warrantable Condominium Conditional Approval Letter

A Primary Residence Non-Warrantable Condominium Conditional Approval Letter is a formal document issued by a lender indicating preliminary intent to finance a unit that fails to meet Fannie Mae or Freddie Mac standards. This letter outlines specific underwriting requirements, such as litigation status, high investor concentration, or budget issues, that must be resolved. It serves as critical proof for buyers and sellers that a specialized loan product is available, provided all mentioned property-specific conditions are met before the final closing process begins.

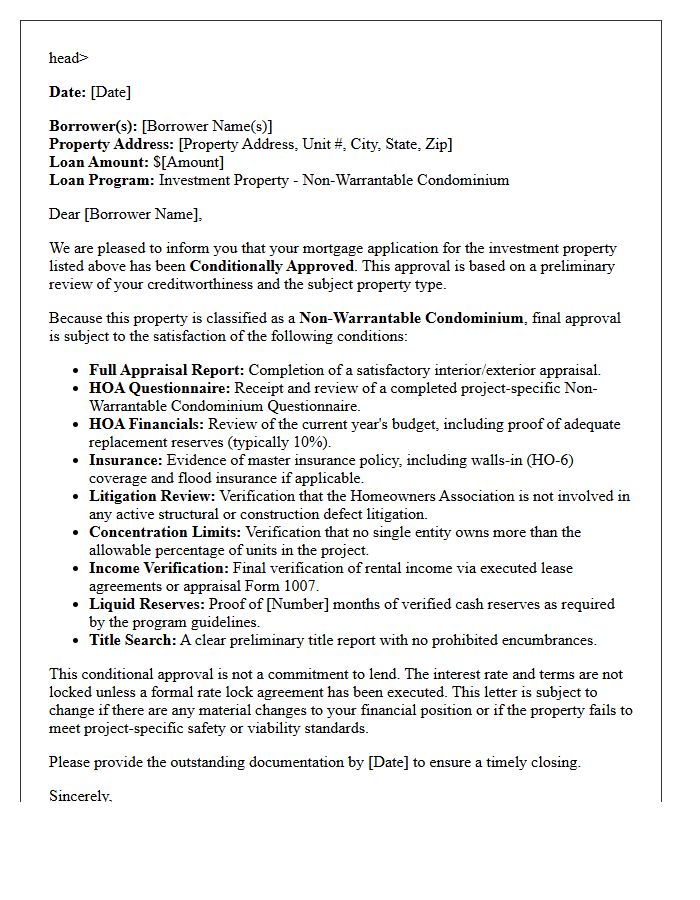

Investment Property Non-Warrantable Condominium Conditional Approval Letter

An investment property Non-Warrantable Condominium Conditional Approval Letter confirms that a lender has reviewed your financial profile and the project's status. These complexes often fail Fannie Mae or Freddie Mac standards due to high investor concentration, ongoing litigation, or commercial space. This letter specifies the requirements you must meet-such as appraisal verification or insurance compliance-before final funding. Securing this document is essential for real estate investors to demonstrate credibility and lock in financing for unique or high-risk multi-family housing units.

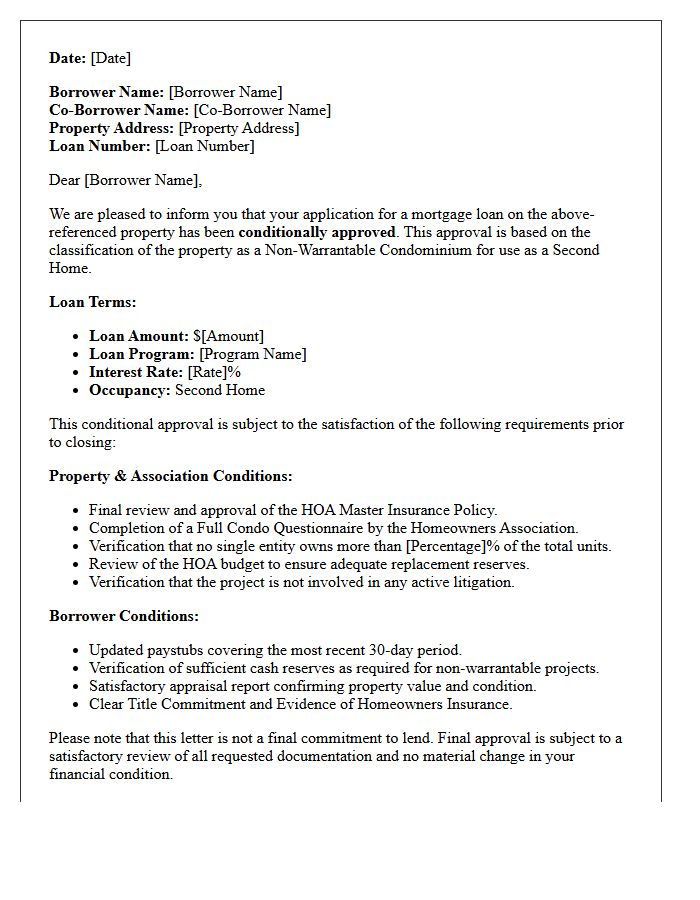

Second Home Non-Warrantable Condominium Conditional Approval Letter

A Second Home Non-Warrantable Condominium Conditional Approval Letter is a formal document issued by a lender indicating preliminary financing approval for a non-conforming property. Unlike standard units, non-warrantable condos do not meet Fannie Mae or Freddie Mac guidelines due to high investor concentration or litigation. This letter specifies the underwriting requirements and documentation needed to finalize the loan. Securing this conditional approval is essential for buyers to demonstrate financial credibility when purchasing unique secondary residences that require specialized portfolio lending solutions or private financing options.

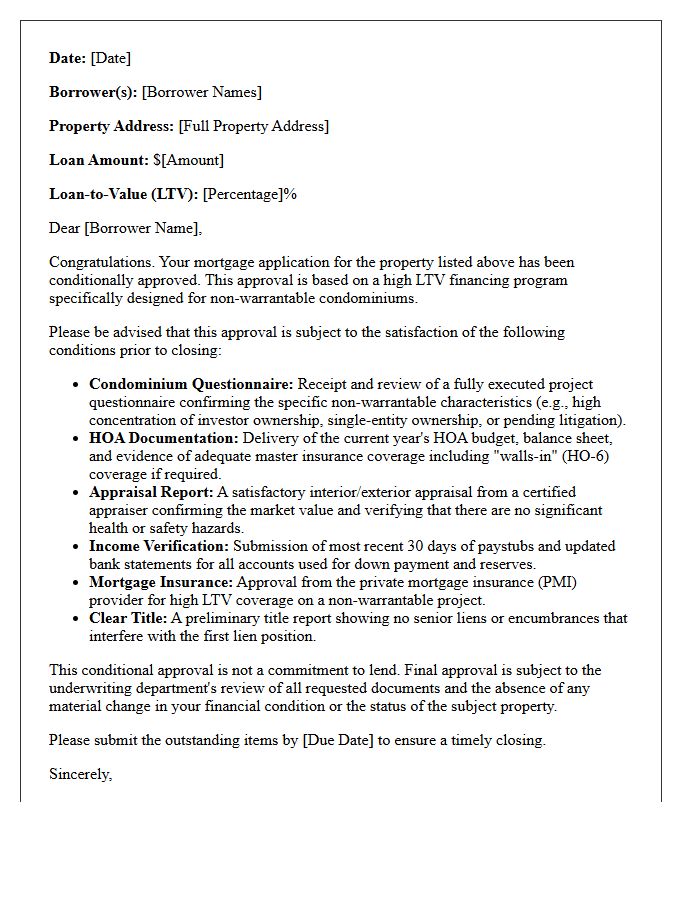

High Loan-to-Value Non-Warrantable Condominium Conditional Approval Letter

A High Loan-to-Value Non-Warrantable Condominium Conditional Approval Letter confirms a lender's intent to finance units that fail Fannie Mae or Freddie Mac standards. This document is essential for buyers seeking flexible financing despite project issues like high investor concentration or pending litigation. It outlines specific conditions, such as down payment requirements and credit scores, necessary to secure the loan. For sellers and real estate agents, this letter serves as a vital indicator of a borrower's financial credibility and the lender's specialized capability to navigate complex, non-conforming property risks effectively.

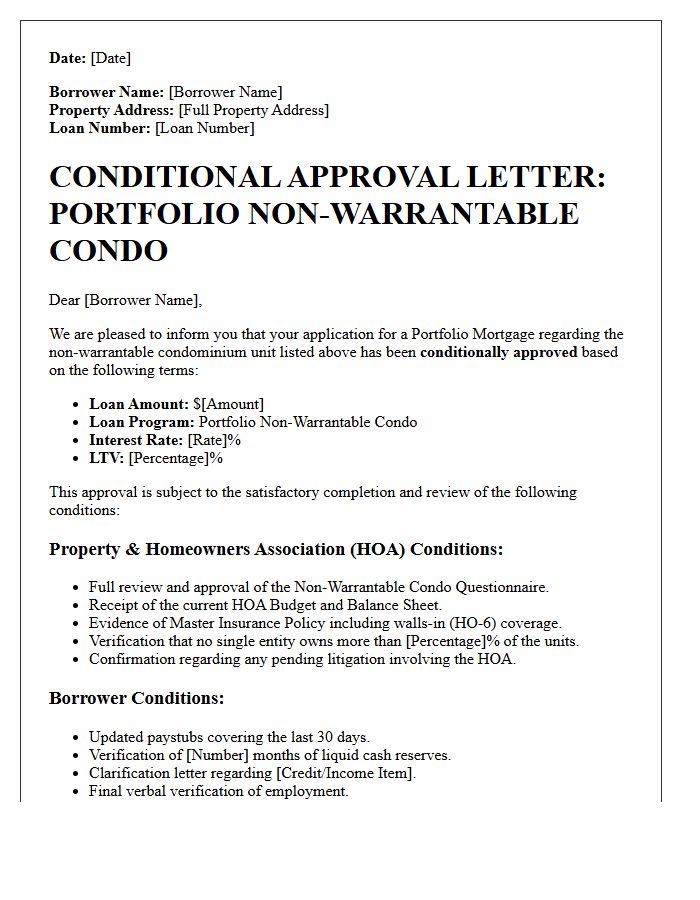

Portfolio Mortgage Non-Warrantable Condominium Conditional Approval Letter

A Portfolio Mortgage for a Non-Warrantable Condominium provides financing for units that fail to meet standard Fannie Mae or Freddie Mac guidelines. Since these loans are held internally by the lender rather than sold on the secondary market, they offer flexible underwriting for projects with high investor concentration or litigation. A Conditional Approval Letter is a critical milestone, confirming that the borrower meets credit requirements subject to specific underwriting conditions, such as final project documentation or property appraisals, ensuring the specialized loan structure is viable before closing.

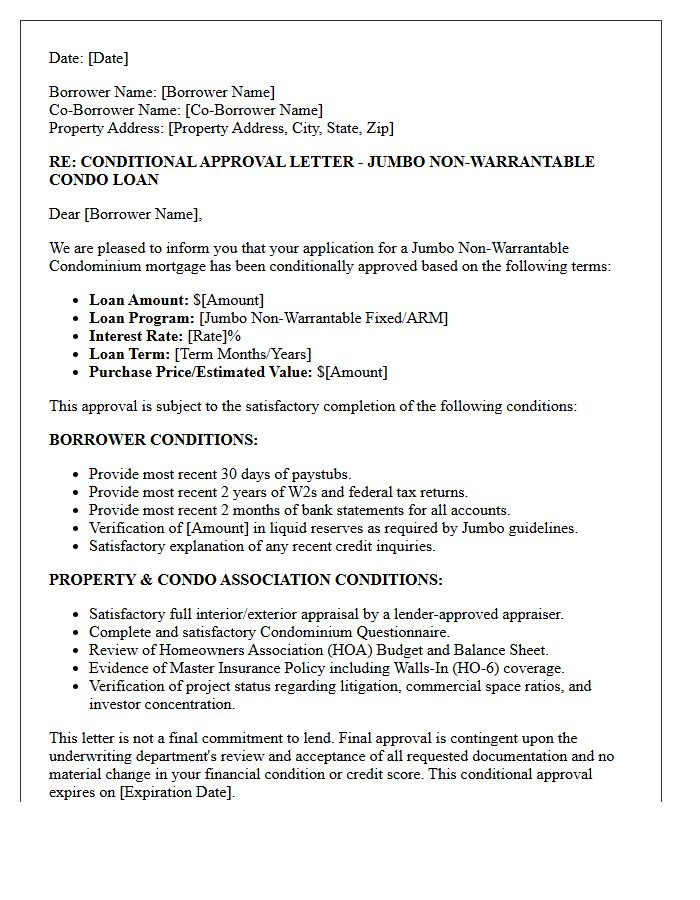

Jumbo Loan Non-Warrantable Condominium Conditional Approval Letter

A Jumbo Loan Non-Warrantable Condominium Conditional Approval Letter confirms a lender's intent to finance high-value units that fail to meet standard Fannie Mae or Freddie Mac guidelines. This document is essential for non-conforming properties, such as those with high commercial space ratios or developer control. It outlines specific underwriting conditions, including verified income, asset reserves, and building litigation reviews. Obtaining this letter proves financial readiness to sellers, demonstrating that the complex structural and financial risks associated with non-warrantable condos have been preliminary assessed for a large-scale mortgage.

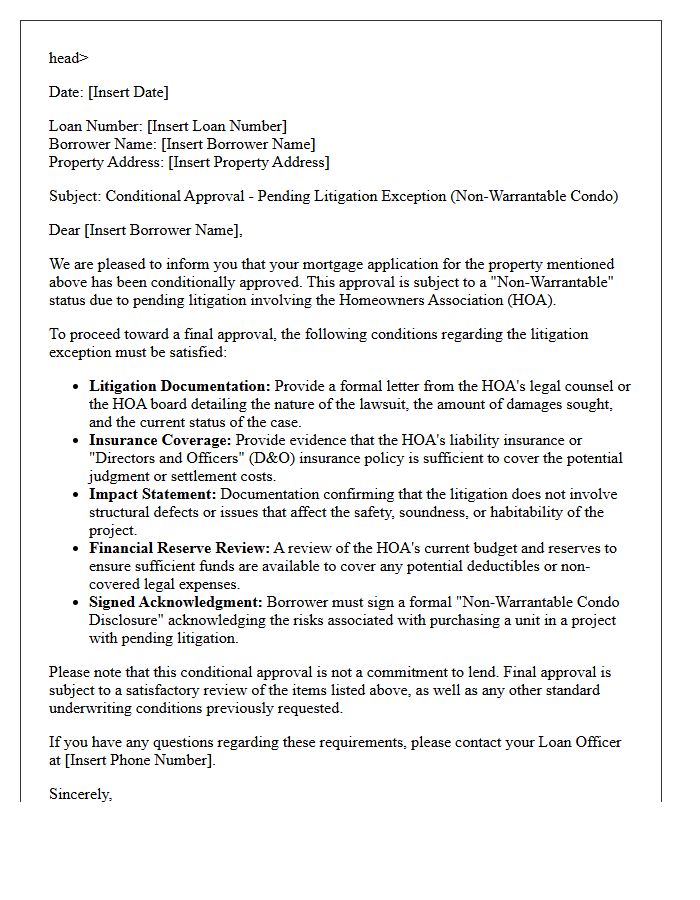

Pending Litigation Exception Non-Warrantable Condominium Conditional Approval Letter

A Pending Litigation Exception allows lenders to issue a Conditional Approval Letter for a non-warrantable condominium despite ongoing lawsuits. Typically, litigation makes a project ineligible for conventional financing; however, exceptions are granted if the legal action is minor or budget-protected. This letter outlines specific underwriting requirements and documentation needed to mitigate risk. Understanding these conditions is crucial for borrowers seeking financing in complexes facing legal disputes, as it bridges the gap between project non-compliance and final loan funding.

Commercial Space Ratio Non-Warrantable Condominium Conditional Approval Letter

A Conditional Approval Letter for a non-warrantable condominium indicates that a lender may finance a unit despite a high Commercial Space Ratio. Typically, Fannie Mae and Freddie Mac reject projects where commercial areas exceed 35% of total square footage. This letter outlines specific requirements the homeowners association or developer must meet to mitigate risk. Securing this document is vital for buyers targeting mixed-use buildings, as it confirms the lender is willing to provide specialized financing provided all structural, legal, and financial stipulations regarding the commercial usage are satisfied before closing.

Single Entity Concentration Non-Warrantable Condominium Conditional Approval Letter

A Single Entity Concentration Non-Warrantable Condominium Conditional Approval Letter is a formal document issued by a lender when one individual or company owns more than the allowed percentage of units in a complex. This concentration risk typically makes a loan ineligible for sale to Fannie Mae or Freddie Mac. The letter outlines specific financial conditions, such as higher interest rates or increased down payment requirements, that must be met to mitigate the risk of a single owner's default impacting the entire homeowners association's stability and budget.

Low Owner-Occupancy Non-Warrantable Condominium Conditional Approval Letter

A Conditional Approval Letter for a low owner-occupancy non-warrantable condominium indicates a lender's preliminary agreement to finance a unit in a building where investors outnumber primary residents. Since these properties do not meet Fannie Mae or Freddie Mac standards, this document outlines specific requirements-such as higher down payments or specialized portfolio lending criteria-that must be satisfied before final funding. It serves as a vital assurance for buyers navigating non-conforming markets, confirming that the lender accepts the project's unique risk profile pending final verification of financial stability and insurance coverage.

New Construction Phasing Non-Warrantable Condominium Conditional Approval Letter

A Conditional Approval Letter for a non-warrantable condominium indicates that a lender is willing to finance a unit despite the project's current status. In new construction phasing, a project is often deemed non-warrantable because it lacks sufficient pre-sale numbers or turned-over control required by Fannie Mae or Freddie Mac. This letter outlines specific underwriting requirements, such as minimum owner-occupancy ratios or budget reserves, that must be satisfied before final funding. It is a critical document for buyers and developers to secure specialized financing in developing communities.

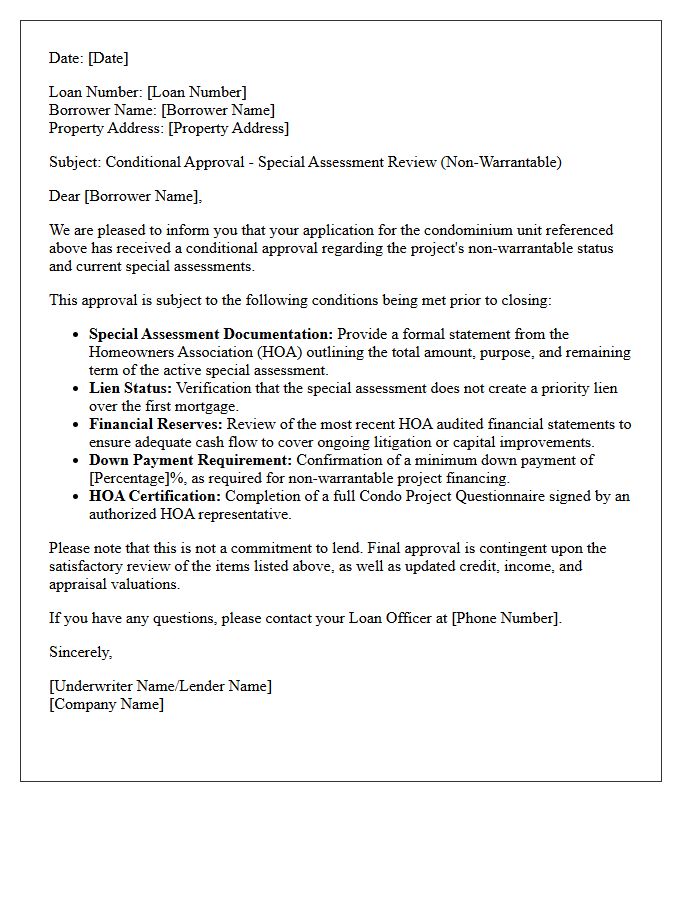

Special Assessment Review Non-Warrantable Condominium Conditional Approval Letter

A Special Assessment Review Non-Warrantable Condominium Conditional Approval Letter is a vital document in real estate financing. It signifies that a lender has conditionally approved a loan for a property that fails standard secondary market guidelines, often due to pending litigation or budget deficits. The letter outlines specific underwriting requirements, such as the satisfactory resolution of special assessments or additional financial documentation. Borrowers must meet these stipulations to secure final funding for units within complexes classified as non-warrantable, ensuring the investment risk is sufficiently mitigated for the financial institution.

What is a Non-Warrantable Condominium Conditional Approval Letter?

A Non-Warrantable Condominium Conditional Approval Letter is a document issued by a lender stating that a specific condo project and borrower have met preliminary underwriting requirements for a non-conforming loan, pending the satisfaction of remaining conditions such as a final appraisal or updated HOA documentation.

Why do I need a conditional approval letter for a non-warrantable condo?

Because non-warrantable condos do not meet Fannie Mae or Freddie Mac guidelines, lenders face higher risks. This letter serves as a formal commitment that the lender is willing to finance the property despite its non-warrantable status, provided all specific financial and legal stipulations are verified.

What are the common conditions listed in a non-warrantable condo approval letter?

Common conditions include a satisfactory "Full Condo Questionnaire," verification of the HOA's master insurance policy, evidence of adequate replacement reserves (typically 10%), confirmation that no single entity owns more than 20% of units, and proof that the project is not involved in pending litigation.

How long is a conditional approval letter valid for a non-warrantable unit?

Most conditional approval letters are valid for 30 to 60 days. Because the eligibility of a non-warrantable project can change based on budget updates or occupancy shifts, lenders require the closing to occur within this window or may demand a re-certification of the condo's status.

Does a conditional approval letter guarantee I will get the loan?

No, it is not a final guarantee. The loan will only move to "Clear to Close" once the underwriter reviews and signs off on every requirement listed in the letter, including the unit's appraisal value and the final legal review of the homeowners association (HOA) bylaws.

Comments