A Conditional Approval Subject to Subordination Agreement Letter outlines that a new loan is approved only if existing creditors agree to a lower priority rank. This legal safeguard ensures the primary lender holds first-lien position during refinancing or secondary financing. Understanding these requirements is essential for securing debt restructuring. Below are some ready to use template options to simplify your documentation process.

Image cover: Conditional Approval with Subordination Requirements: Guide and Templates

Letter Samples List

- Conditional Approval Subject To Subordination Agreement Letter

- Mortgage Refinance Conditional Approval Subject To Subordination Letter

- Second Lien Subordination Conditional Approval Letter

- Borrower Notification Of Conditional Approval Subject To Subordination Letter

- Home Equity Subordination Requirement Approval Letter

- Clear To Close Pending Subordination Agreement Letter

- Primary Lender Subordination Request And Conditional Approval Letter

- Commercial Mortgage Conditional Approval Subject To Subordination Letter

- Rate Lock And Conditional Approval Subject To Subordination Letter

- Construction Loan Conditional Approval Subject To Subordination Letter

- Government Mortgage Conditional Approval Subject To Subordination Letter

- Investment Property Conditional Approval Subject To Subordination Letter

- Third Party Subordination Condition Mortgage Approval Letter

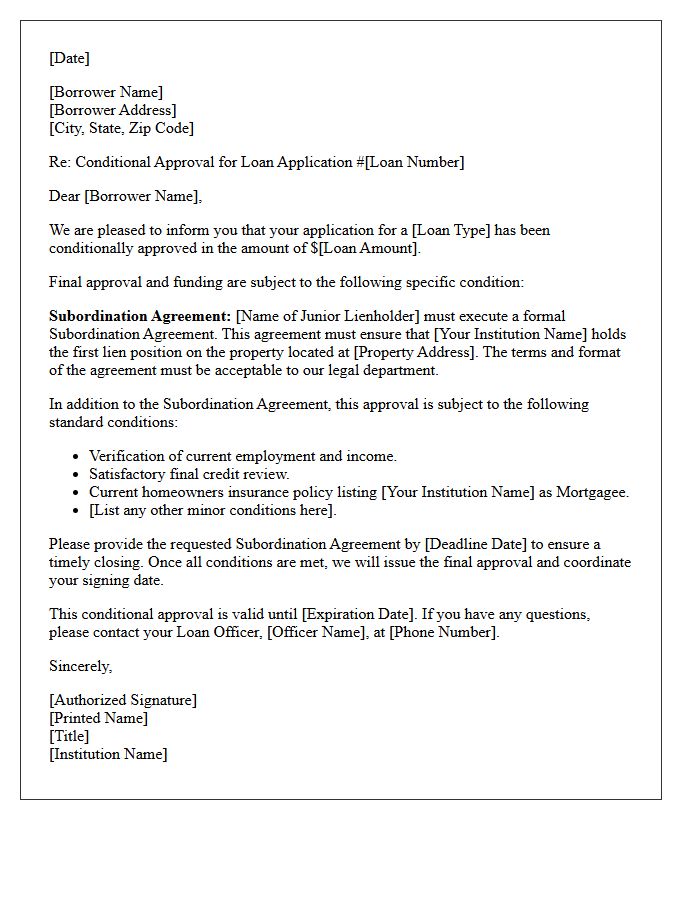

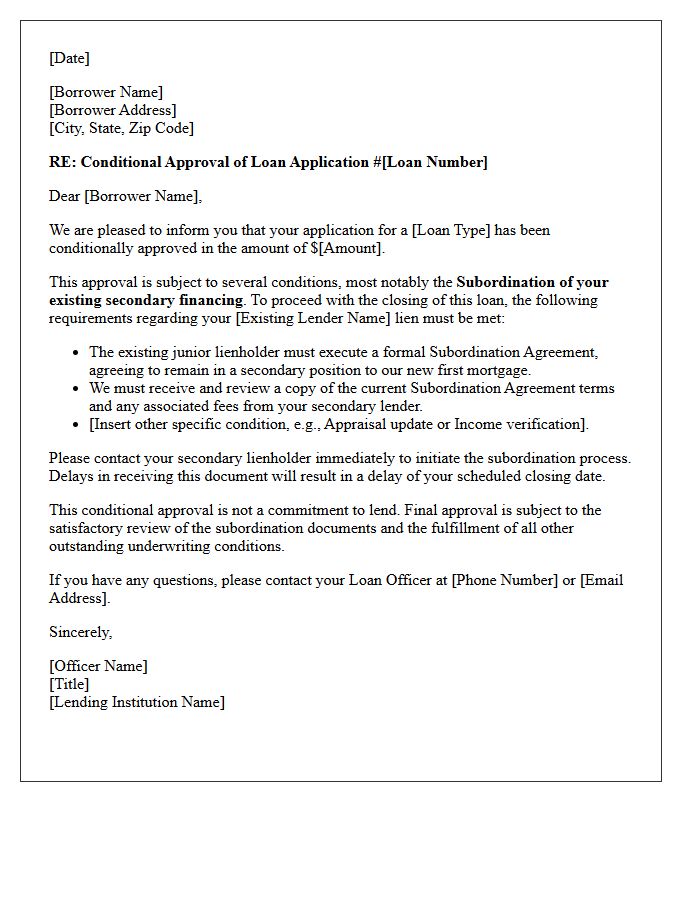

Conditional Approval Subject To Subordination Agreement Letter

A Conditional Approval Subject To Subordination Agreement Letter is a formal notice issued by a lender indicating loan approval contingent on a priority reshuffle. It requires an existing lienholder to sign a Subordination Agreement, moving their claim to a secondary position. This legal document ensures the new primary lender has first rights to the collateral if default occurs. Borrowers must coordinate between both financial institutions to finalize this legal subordination before the new financing can officially close. It is a critical step in refinancing or securing secondary lines of credit.

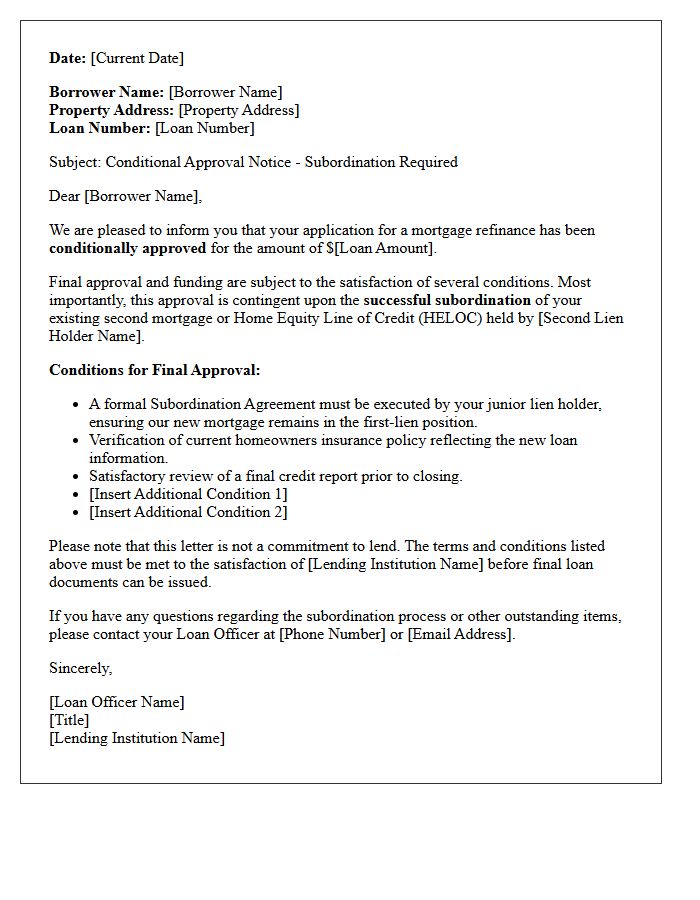

Mortgage Refinance Conditional Approval Subject To Subordination Letter

A mortgage refinance conditional approval remains pending until the lender receives a subordination letter from any existing junior lienholder. This legal document confirms that a secondary lender, such as a HELOC provider, agrees to remain in a lower priority position behind the new primary mortgage. Without this agreement, the refinance cannot close because the new lender requires a first-lien status to protect their investment. Borrowers should request this document early to avoid processing delays, as it is a critical requirement for final loan funding and title insurance clearance.

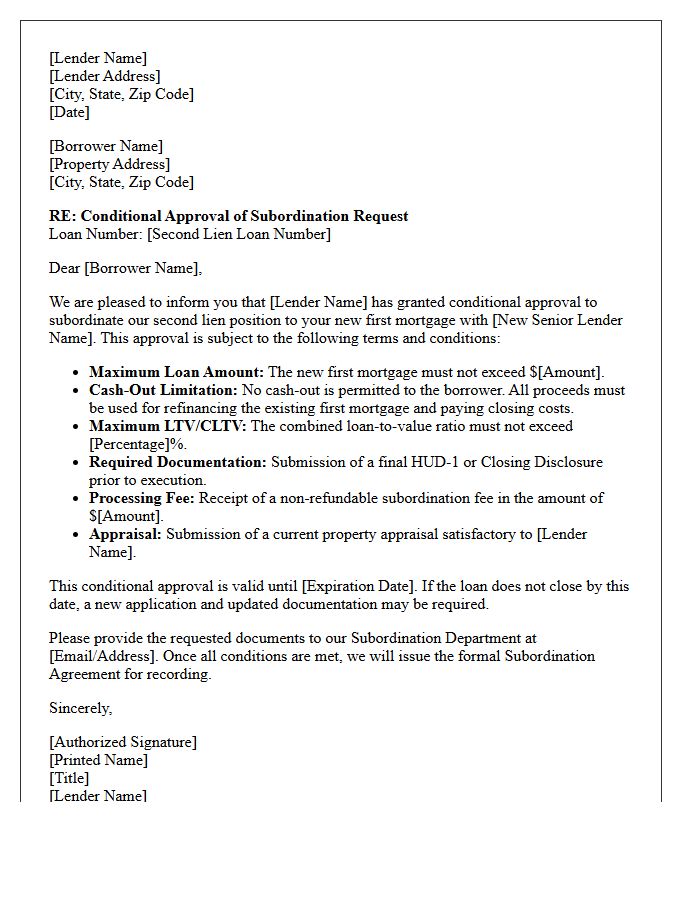

Second Lien Subordination Conditional Approval Letter

A Second Lien Subordination Conditional Approval Letter is a formal document issued by a junior lender agreeing to remain in a lower priority position. The subordination process is critical when refinancing a primary mortgage, as the secondary lender must legally consent to stay behind the new first loan. This letter outlines specific conditions, such as maximum loan-to-value ratios or administrative fees, that must be met before final authorization. Understanding these requirements is essential for ensuring a smooth closing and maintaining the established lien priority during debt restructuring.

Borrower Notification Of Conditional Approval Subject To Subordination Letter

A Borrower Notification of Conditional Approval Subject to Subordination Letter informs a homeowner that their new financing is approved, provided the existing junior lienholder agrees to remain in a second position. The subordination agreement is the critical requirement, as the primary lender needs to ensure their first-lien priority is protected. This document outlines specific conditions the borrower must meet before final funding occurs. It serves as a formal notice that the loan process is progressing but remains contingent upon the legal cooperation of all current mortgage holders to secure the lender's financial interest.

Home Equity Subordination Requirement Approval Letter

A Home Equity Subordination Requirement Approval Letter is a critical document used when refinancing a primary mortgage while keeping an existing home equity line or loan. This letter confirms that the junior lender agrees to remain in second lien position, allowing the new primary mortgage to take legal priority. Without this formal subordination agreement, the refinancing process cannot close. Homeowners must proactively request this approval from their equity lender, as processing times vary and specific eligibility criteria regarding credit scores and loan-to-value ratios must be met to secure the approval.

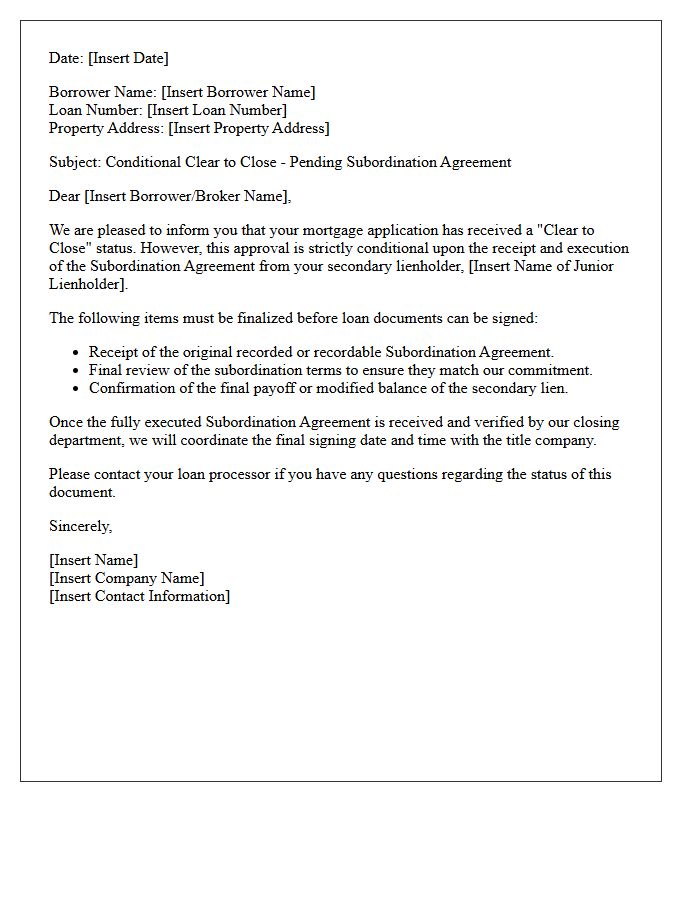

Clear To Close Pending Subordination Agreement Letter

A Clear To Close with a pending subordination agreement occurs when a secondary lienholder must legally agree to remain in a subordinate position behind a new primary mortgage. This document is essential for final loan approval, as the lender requires guaranteed priority status. Borrowers should monitor this process closely, as delays in receiving the signed agreement from the second lender can postpone the closing date. Finalizing this paperwork ensures the title is clear and the new financing is secured according to underwriting guidelines.

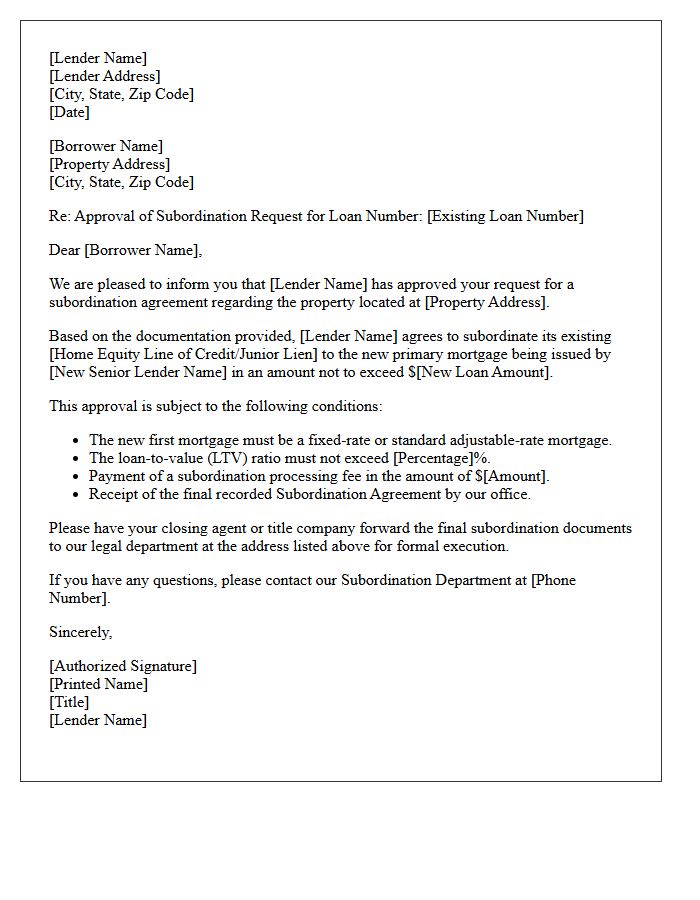

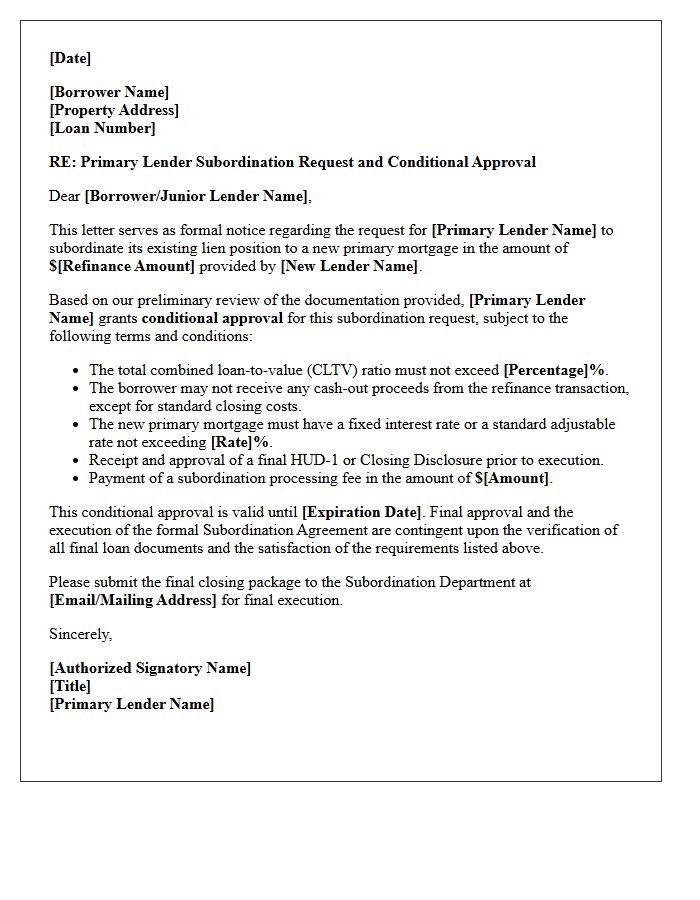

Primary Lender Subordination Request And Conditional Approval Letter

A Primary Lender Subordination Request is a formal application where a secondary lienholder asks a senior creditor to maintain a lower priority position during refinancing. The resulting Conditional Approval Letter outlines specific requirements, such as maximum loan-to-value ratios or debt limits, that must be met to finalize the agreement. Understanding these documents is essential for homeowners seeking to restructure debt without losing their existing secondary financing. This process ensures legal clarity regarding lien priority and protects the primary lender's security interest in the underlying collateral.

Commercial Mortgage Conditional Approval Subject To Subordination Letter

A commercial mortgage conditional approval subject to a subordination letter requires existing lienholders to legally rank their debt priority below the new lender. This process ensures the primary financier holds first-lien position, securing their collateral interest. The approval remains contingent until all secondary creditors sign an agreement to defer their repayment claims. Obtaining this document is critical for final funding, as it mitigates risk for the lead bank. Borrowers must coordinate with current lenders early to avoid closing delays caused by these priority negotiations.

Rate Lock And Conditional Approval Subject To Subordination Letter

A rate lock guarantees your interest rate for a specific period, protecting you from market fluctuations. When combined with a conditional approval, the lender agrees to fund your loan provided you meet specific requirements, such as obtaining a subordination letter. This document is essential when refinancing a primary mortgage while keeping a secondary lien, like a HELOC, in place. It ensures the new primary lender retains first-priority status. Without a timely subordination agreement, your rate lock may expire, potentially increasing your long-term borrowing costs.

Construction Loan Conditional Approval Subject To Subordination Letter

A construction loan conditional approval subject to a subordination letter means your lender requires a subordination agreement from an existing lienholder. This legal document ensures the new construction loan takes primary lien position, prioritizing it for repayment over existing debt, such as a land loan or second mortgage. Securing this letter is a critical funding condition; without it, the lender faces higher risk, which may stall your project. Borrowers must coordinate between lenders early to ensure the junior lienholder agrees to remain in a secondary position during the build process.

Government Mortgage Conditional Approval Subject To Subordination Letter

A government mortgage conditional approval subject to a subordination letter occurs during refinancing when a homeowner has an existing second lien, such as a HELOC or down payment assistance loan. The primary lender requires the junior lienholder to formally agree to remain in a secondary position. This legal document is critical for ensuring the new first mortgage maintains priority status. Processing this request can delay closing, so homeowners must coordinate early with their secondary lender to secure the necessary approval and meet all underwriting conditions efficiently.

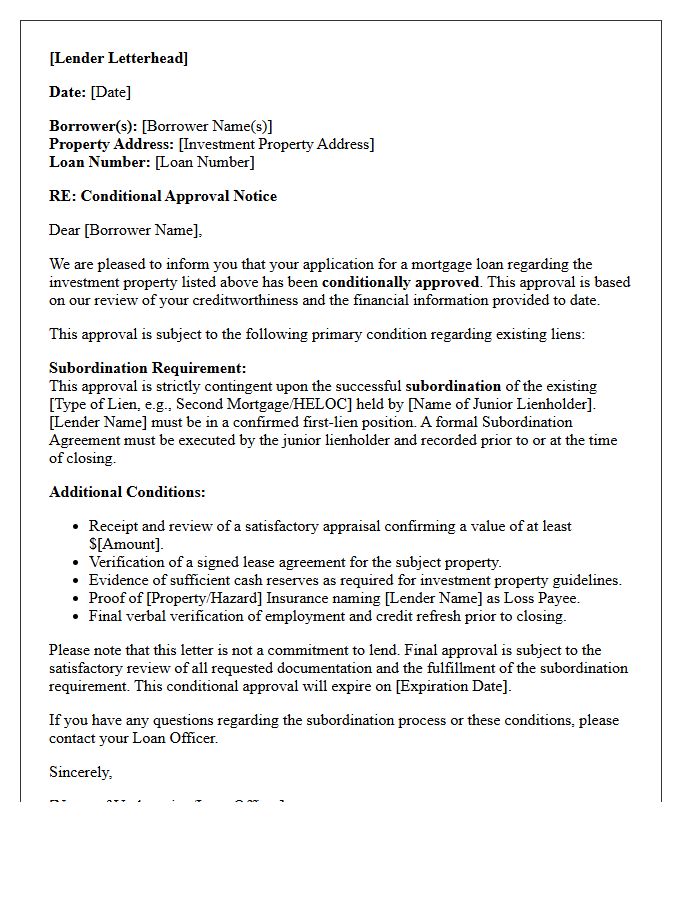

Investment Property Conditional Approval Subject To Subordination Letter

A conditional approval for an investment property subject to a subordination letter occurs when a secondary lender agrees to maintain a lower priority position. This document is crucial because primary lenders require their lien to be paid first during a default. The borrower must ensure the junior lienholder signs this agreement to finalize the refinance or purchase. Without this legal priority restructuring, the primary loan cannot close. Ensuring all parties understand lien priority is the most important step in securing financing for leveraged real estate assets.

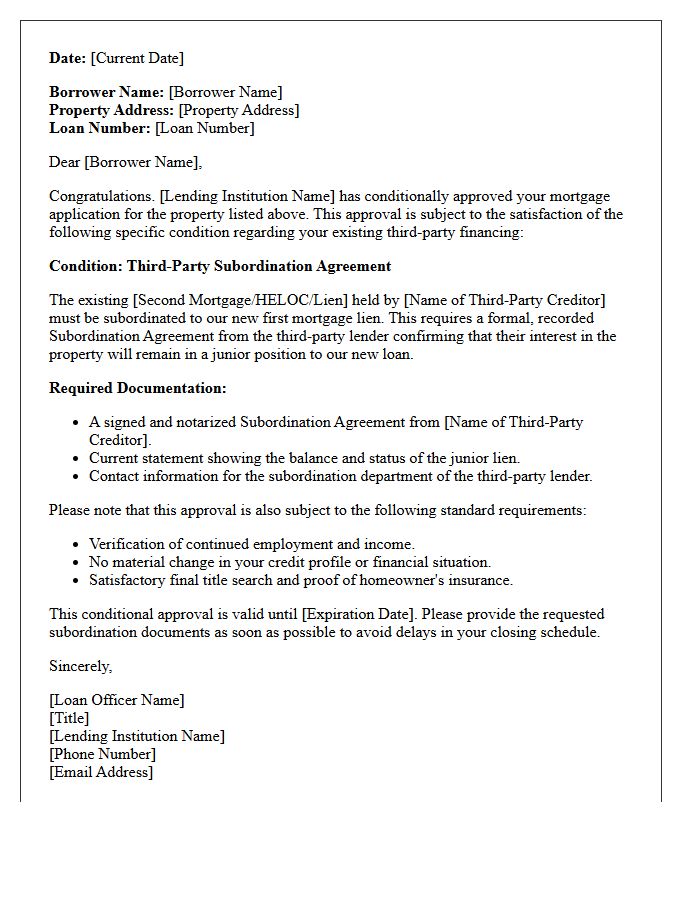

Third Party Subordination Condition Mortgage Approval Letter

A Third Party Subordination Condition in a mortgage approval letter signifies that the lender requires a subordination agreement from an existing junior lienholder. This legal document ensures the new primary mortgage maintains first-priority status, even if it was recorded after a current second mortgage or HELOC. Borrowers must coordinate with their secondary lenders early, as approval is not guaranteed and delays in obtaining these signed forms can significantly postpone or jeopardize the final closing process. Understanding this condition is essential for successful refinancing or securing additional financing on encumbered property.

What is a Conditional Approval Subject to Subordination Agreement Letter?

A Conditional Approval Subject to Subordination Agreement Letter is a formal document issued by a lender stating that a new loan application is approved, provided that an existing lienholder agrees to remain in a secondary position behind the new mortgage.

Why do lenders require a subordination agreement for loan approval?

Lenders require a subordination agreement to ensure they hold the first lien position on a property's title. This protects the lender's interest by ensuring their debt is prioritized for repayment before other existing junior liens in the event of a foreclosure.

What happens if a junior lienholder refuses to sign the subordination agreement?

If a junior lienholder refuses to sign, the conditional approval remains unsatisfied. In this scenario, the borrower may be unable to close the new loan unless the existing junior lien is paid off in full or the new lender agrees to waive the requirement, which is rare.

Who is responsible for obtaining the signed subordination agreement?

While the new lender or title company typically initiates the request, the borrower is ultimately responsible for ensuring the junior lienholder receives the necessary documentation and follows through with the subordination process to meet the loan conditions.

How long does it take to process a subordination agreement during refinancing?

The processing time for a subordination agreement typically ranges from two to four weeks, depending on the requirements and responsiveness of the current junior lienholder. It is recommended to start this process early to avoid delays in the final loan closing.

Comments