A Revision of Conditional Approval Terms Letter is a formal request to modify specific requirements set by a lender or authority. This document clarifies why certain conditions are unattainable and proposes feasible alternatives to secure final authorization. Understanding how to structure this request is essential for successful negotiations. To assist your drafting process, below are some ready to use templates.

Image cover: Mastering the Amendment of Conditional Approval Terms: Professional Letter Templates and Samples

Letter Samples List

- Income Adjustment Conditional Approval Revision Letter

- Appraisal Shortfall Term Modification Letter

- Interest Rate Expiration Term Revision Letter

- Down Payment Requirement Adjustment Letter

- Debt-to-Income Ratio Recalculation Revision Letter

- Loan Program Conversion Conditional Approval Letter

- Credit Profile Fluctuation Term Revision Letter

- Co-Borrower Addition Conditional Approval Letter

- Property Condition Repair Escrow Revision Letter

- Principal Loan Amount Reduction Revision Letter

- Closing Cost Seller Concession Modification Letter

- Employment Verification Condition Revision Letter

- Private Mortgage Insurance Term Adjustment Letter

Income Adjustment Conditional Approval Revision Letter

An Income Adjustment Conditional Approval Revision Letter signifies a secondary review of your financial aid status. It updates a previously issued decision based on new documentation or verified changes in your economic circumstances. This document is essential because it outlines your revised Expected Family Contribution (EFC) or Student Aid Index (SAI). Recipients must carefully review the terms and conditions specified to ensure all requirements are met for the final disbursement of adjusted funds. Failure to provide requested evidence can result in the reversal of your financial aid award.

Appraisal Shortfall Term Modification Letter

An Appraisal Shortfall Term Modification Letter is a formal document used when a property's appraised value is lower than the agreed purchase price. This amendment typically outlines how the buyer and seller will address the financial gap. It may specify that the buyer will cover the difference with cash, the seller will reduce the sales price, or both parties will compromise. Ensuring this legal addendum is clearly drafted is essential for securing financing and preventing the real estate transaction from collapsing due to a valuation discrepancy.

Interest Rate Expiration Term Revision Letter

An Interest Rate Expiration Term Revision Letter is a formal notice sent by lenders to modify the deadline of a previously locked mortgage rate. This document is critical because it extends or adjusts the timeframe during which a borrower can secure a specific percentage. If the revision is not acknowledged, the rate may expire, potentially leading to higher monthly payments. Borrowers must review the new expiration date and any associated extension fees to ensure their financing remains stable until the loan closing is finalized.

Down Payment Requirement Adjustment Letter

A Down Payment Requirement Adjustment Letter is a formal notification from a lender informing a borrower of changes to their upfront equity commitment. This document typically outlines modified loan-to-value (LTV) ratios based on updated credit risk assessments or property appraisals. Understanding this letter is crucial, as it directly impacts your closing costs and monthly mortgage obligations. Carefully review the stated adjustments to ensure your financing strategy remains viable before proceeding with the real estate transaction.

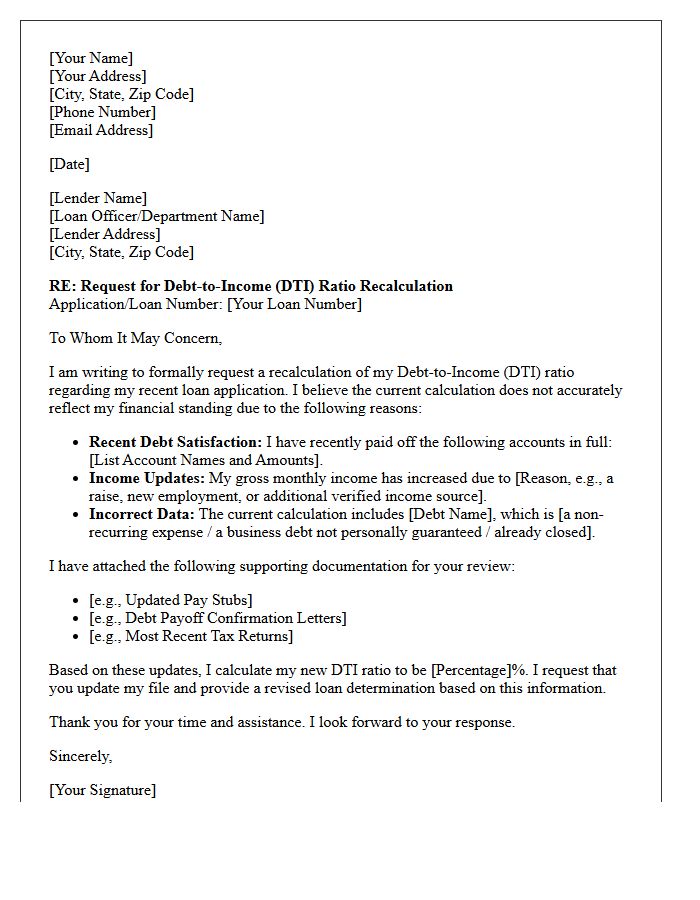

Debt-to-Income Ratio Recalculation Revision Letter

A Debt-to-Income Ratio Recalculation Revision Letter is a formal document sent to lenders to correct inaccuracies in financial assessments. It is essential when original calculations overlook stable income sources or include disputed debts that inflate the ratio. Providing verifiable evidence, such as updated pay stubs or debt discharge notices, helps justify a lower DTI. This revision is crucial for borrowers seeking mortgage approval or better loan terms, as it ensures the lender evaluates your true repayment capacity based on precise, updated financial data.

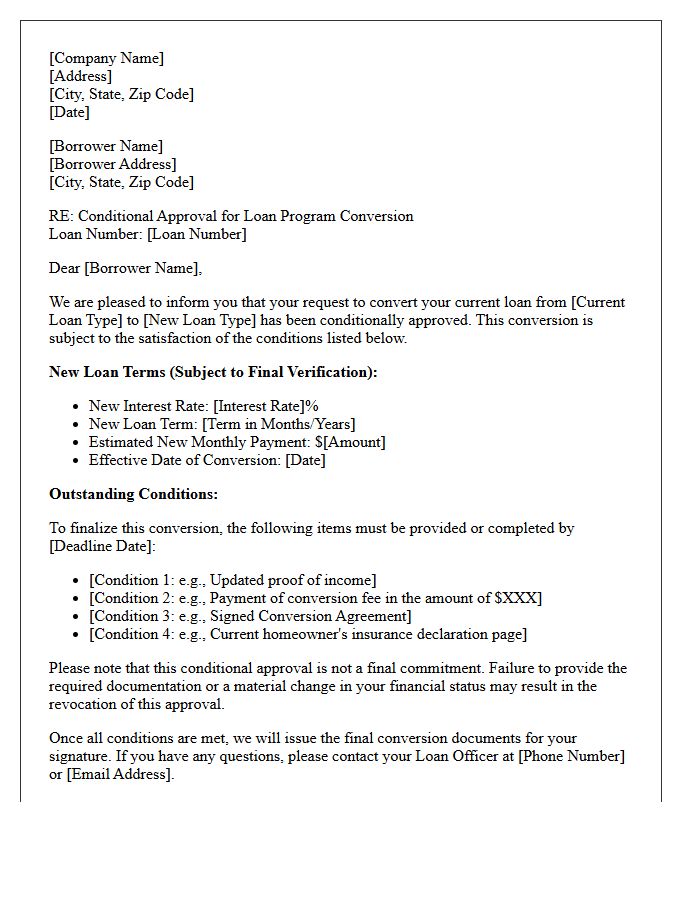

Loan Program Conversion Conditional Approval Letter

A Loan Program Conversion Conditional Approval Letter confirms that a lender has reviewed your request to switch mortgage types. This document outlines specific underwriting requirements that must be satisfied before final funding. It is crucial to understand that program conversion may alter your interest rate, monthly payments, or down payment obligations. Borrowers must submit all outstanding documentation promptly to maintain their conditional status. Receiving this letter indicates progress, but it is not a guaranteed commitment until all stated contingencies are cleared by the financial institution.

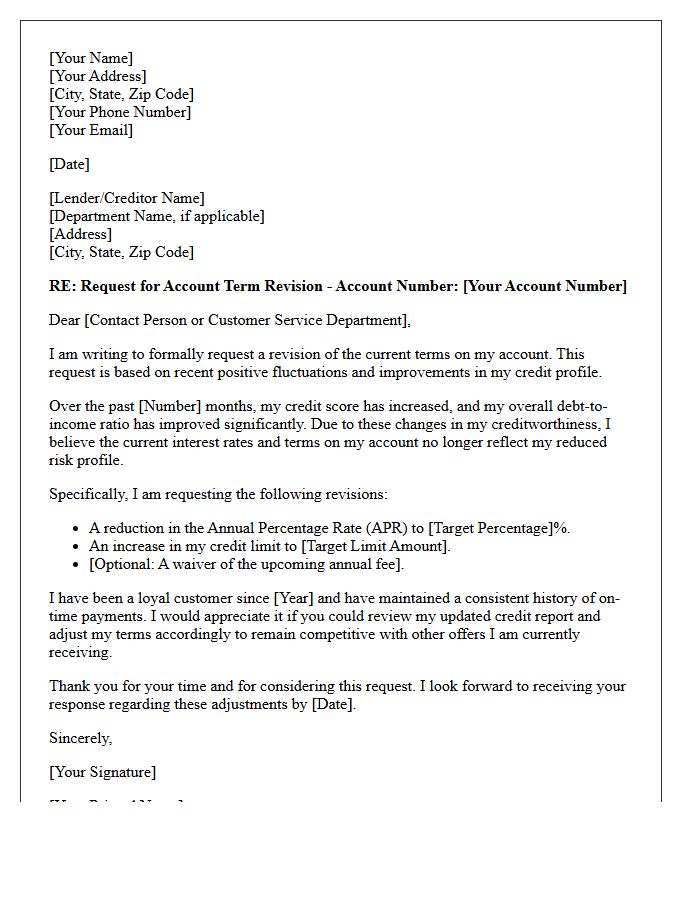

Credit Profile Fluctuation Term Revision Letter

A Credit Profile Fluctuation Term Revision Letter is a formal notification from a lender adjusting your borrowing terms based on changes in your financial behavior. This document typically outlines modifications to interest rates, credit limits, or repayment conditions triggered by shifts in your credit score. It is essential to review these letters immediately to understand how your repayment obligations have evolved. Timely action and maintaining a stable credit profile are crucial to preventing unfavorable adjustments and ensuring long-term financial stability with your creditors.

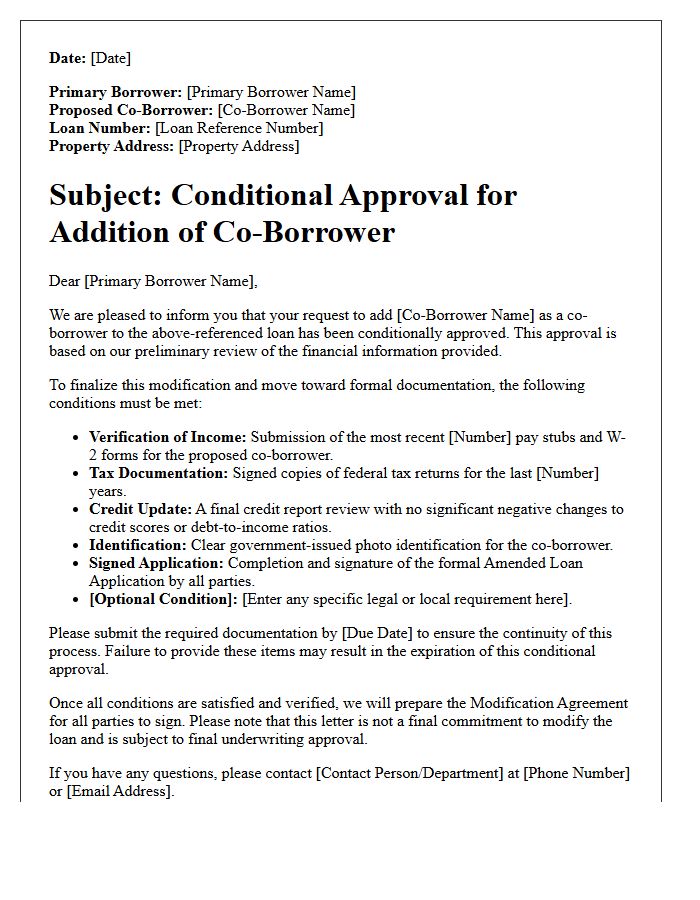

Co-Borrower Addition Conditional Approval Letter

A Co-Borrower Addition Conditional Approval Letter is a formal document issued by a lender during the mortgage process. It signifies that adding a second applicant to the loan is tentatively approved, provided specific underwriting conditions are met. This letter outlines requirements such as updated credit checks, income verification, and debt-to-income assessments for both parties. Receiving this status means the lender is willing to proceed, but the final loan commitment remains contingent upon the successful submission and verification of all requested financial documentation to mitigate lending risk.

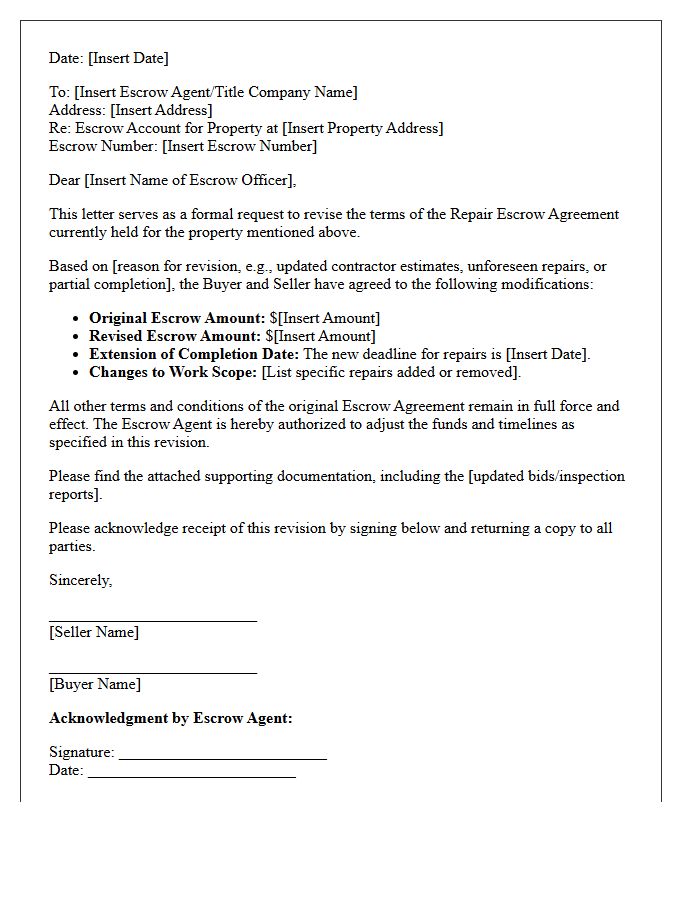

Property Condition Repair Escrow Revision Letter

A Property Condition Repair Escrow Revision Letter is a formal document used to modify original escrow agreements during real estate transactions. It specifically outlines changes to repair obligations, adjusted cost estimates, or extended deadlines for property improvements. This letter ensures that both buyers and sellers agree to updated terms regarding funds held in reserve. It serves as a vital legal amendment to protect parties if unexpected issues arise during the restoration process, maintaining financial transparency until the lender requirements or safety standards are fully met before final fund release.

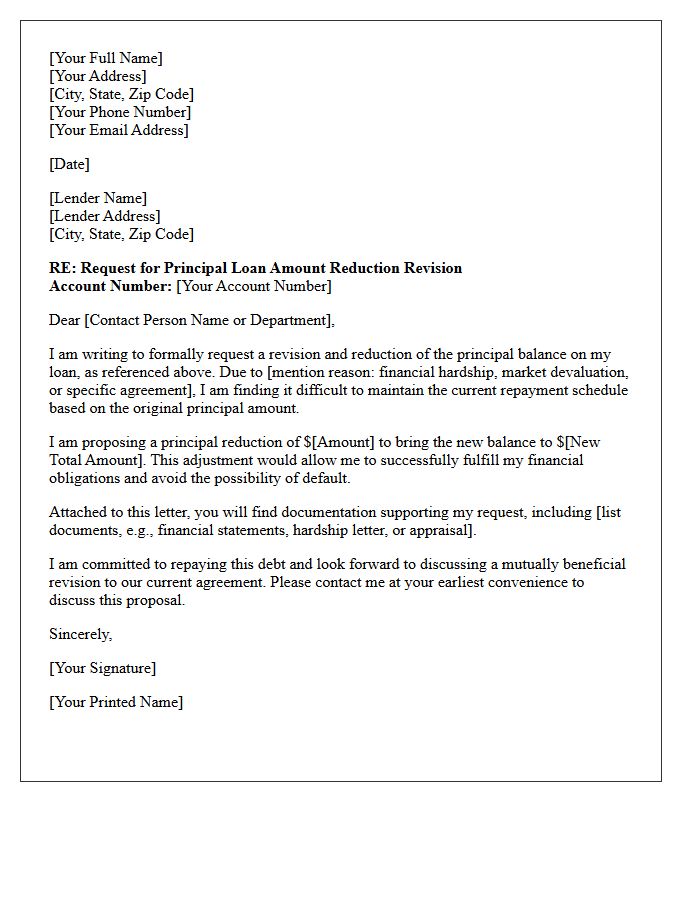

Principal Loan Amount Reduction Revision Letter

A Principal Loan Amount Reduction Revision Letter is a formal document issued by a lender to confirm a permanent decrease in your total outstanding debt. This revision typically occurs after a successful loan modification, a lump-sum payment, or a principal curtailment agreement. It serves as legal evidence that your mortgage balance has been adjusted downward, potentially lowering your monthly interest charges. Homeowners must verify the new balance accuracy and retain this letter for financial records to ensure the servicer correctly applies the reduction to the loan account.

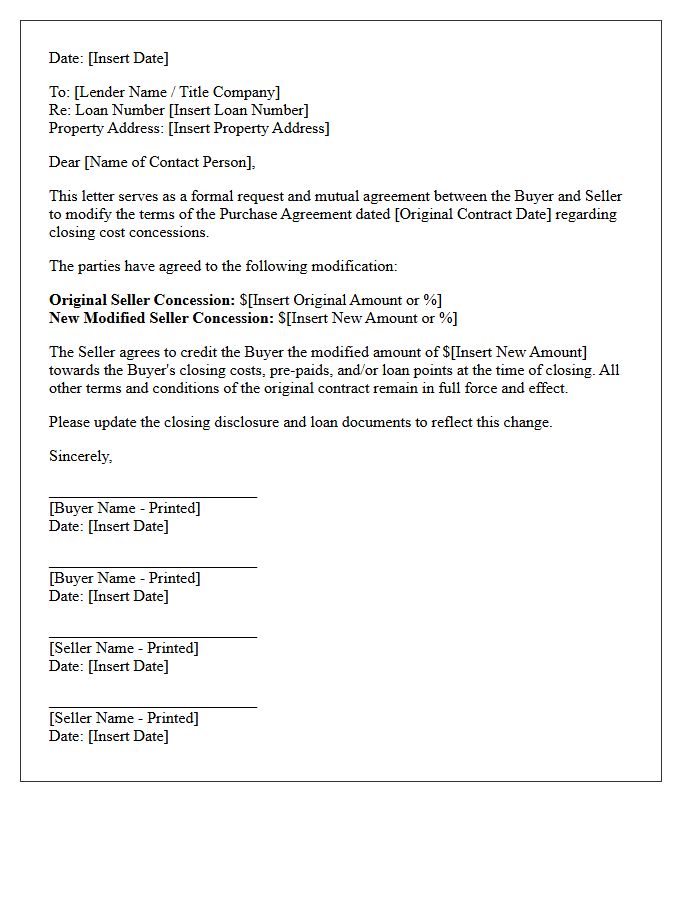

Closing Cost Seller Concession Modification Letter

A Closing Cost Seller Concession Modification Letter is a formal document used to amend the original purchase agreement when the parties agree to change the amount a seller contributes toward the buyer's closing expenses. This amendment is essential for lenders to update the loan estimate and ensure compliance with maximum contribution limits. It serves as a legal record of the revised financial terms, preventing delays during the final underwriting process by clearly documenting any shifts in credits or sales price before the transaction concludes.

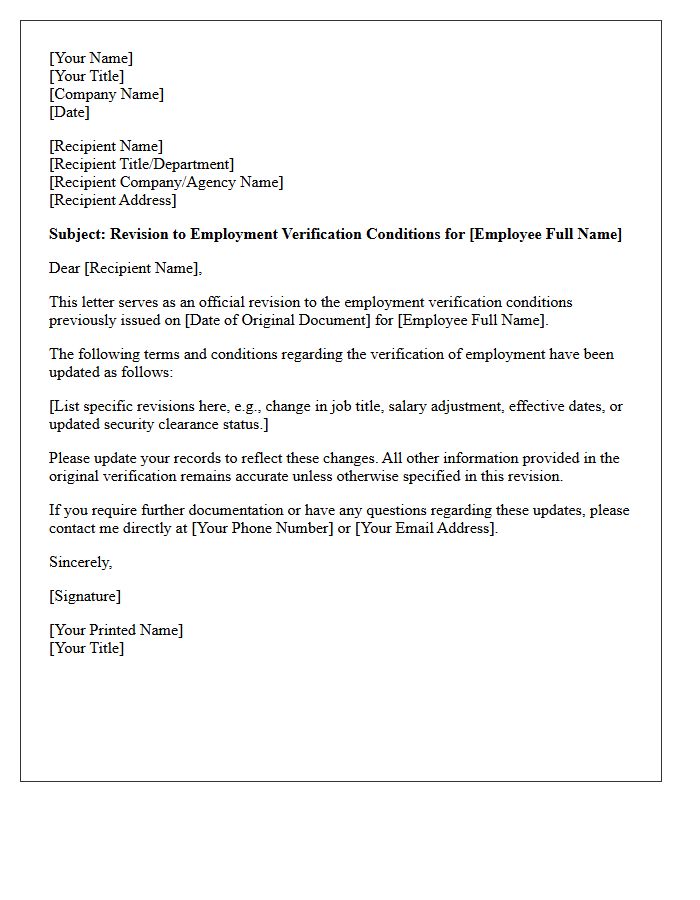

Employment Verification Condition Revision Letter

An Employment Verification Condition Revision Letter is a formal document used to update or correct previously submitted job information during a background check or loan application. It clarifies discrepancies regarding job titles, start dates, or salary details to ensure compliance with underwriting standards. Providing this amended statement promptly is essential for maintaining transparency and resolving potential red flags. Employers issue this revision to confirm verified data accuracy, helping candidates secure final approvals for legal, financial, or professional onboarding processes without further administrative delays.

Private Mortgage Insurance Term Adjustment Letter

A Private Mortgage Insurance (PMI) Term Adjustment Letter is a formal notification from your lender regarding changes to your PMI cancellation date. This document is essential because it updates the projected timeline for reaching the 80% loan-to-value ratio required to stop payments. Receiving this letter often signifies that your scheduled termination has been recalculated based on your payment history or additional principal payments. Reviewing this adjustment ensures you do not overpay for insurance once you have gained sufficient home equity to satisfy federal requirements for removal.

What is a Revision of Conditional Approval Terms Letter?

A Revision of Conditional Approval Terms Letter is a formal document issued by a lender to notify a borrower of changes to the original requirements or contingencies that must be met before a loan receives final approval.

Why did my conditional approval terms change?

Terms are typically revised due to new information discovered during the underwriting process, such as updated credit report data, changes in employment status, property appraisal discrepancies, or shifts in debt-to-income ratios.

How do I respond to a revised conditional approval letter?

To move forward, you should carefully review the new conditions, sign the acknowledgment if required, and promptly provide any additional documentation requested to satisfy the updated requirements.

Can a revision of terms lead to a loan denial?

Yes, if the revised terms include conditions that the borrower cannot meet-such as requiring a higher down payment or a lower debt level-the loan may be denied if the borrower fails to satisfy those new criteria.

Does a revision of terms restart the entire mortgage process?

No, it does not restart the entire process, but it may add time to the closing timeline as the underwriter must verify the newly requested documents and ensure the file complies with the updated terms.

Comments