A Notice of Default and Demand for Payment is a formal legal document issued when a borrower fails to meet loan obligations. It serves as an official warning to settle outstanding debts before further legal action or foreclosure begins. Understanding your rights and responsibilities during this process is essential for debt resolution. To assist you, below are some ready to use template.

Image cover: Professional Notice of Default and Demand for Payment Templates

Letter Samples List

- Standard Mortgage Notice of Default and Demand for Payment Letter

- First Warning Notice of Default and Demand for Payment Letter

- Second Warning Notice of Default and Demand for Payment Letter

- Final Pre-Foreclosure Notice of Default and Demand for Payment Letter

- Commercial Mortgage Notice of Default and Demand for Payment Letter

- Residential Mortgage Notice of Default and Demand for Payment Letter

- Escrow Deficiency Notice of Default and Demand for Payment Letter

- Balloon Payment Notice of Default and Demand for Payment Letter

- Maturity Date Notice of Default and Demand for Payment Letter

- Property Tax Delinquency Notice of Default and Demand for Payment Letter

- Breach of Covenant Notice of Default and Demand for Payment Letter

- Cure Period Notice of Default and Demand for Payment Letter

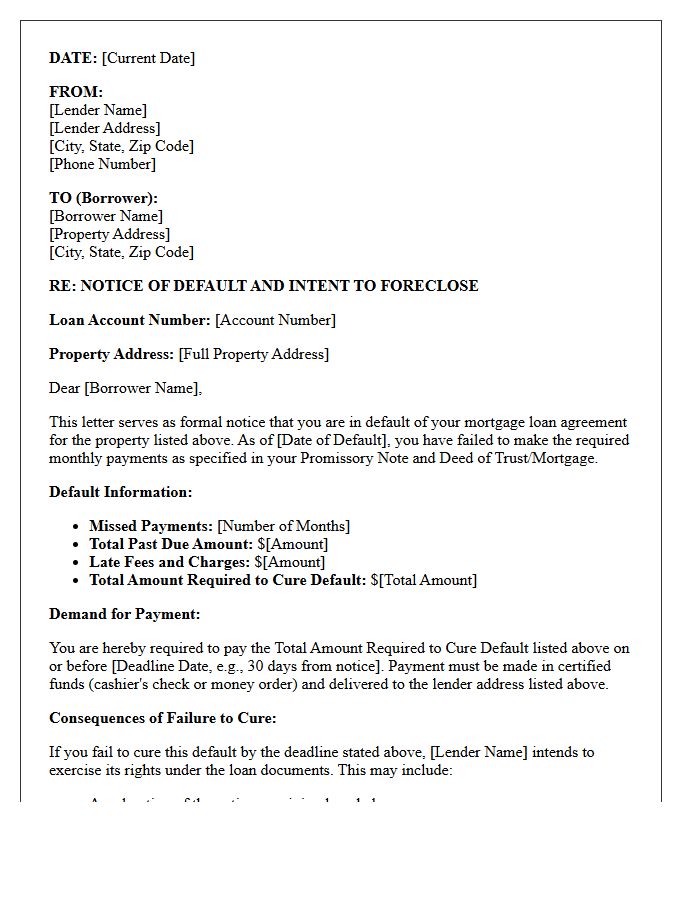

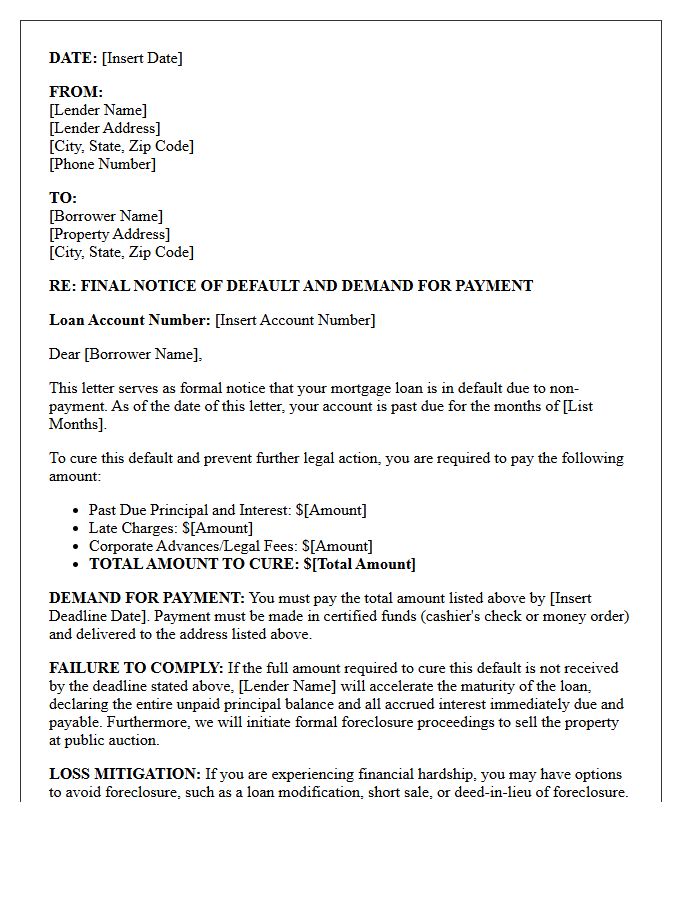

Standard Mortgage Notice of Default and Demand for Payment Letter

A Notice of Default and Demand for Payment is a formal legal document issued by a lender when a borrower breaches the loan agreement. It serves as the official initiation of the foreclosure process. The letter specifies the total arrears, including late fees and interest, required to cure the default. Borrowers are typically given a strictly defined grace period to pay the outstanding balance. Failing to resolve the debt within this timeframe allows the creditor to accelerate the loan and legally seize the property to recover the investment.

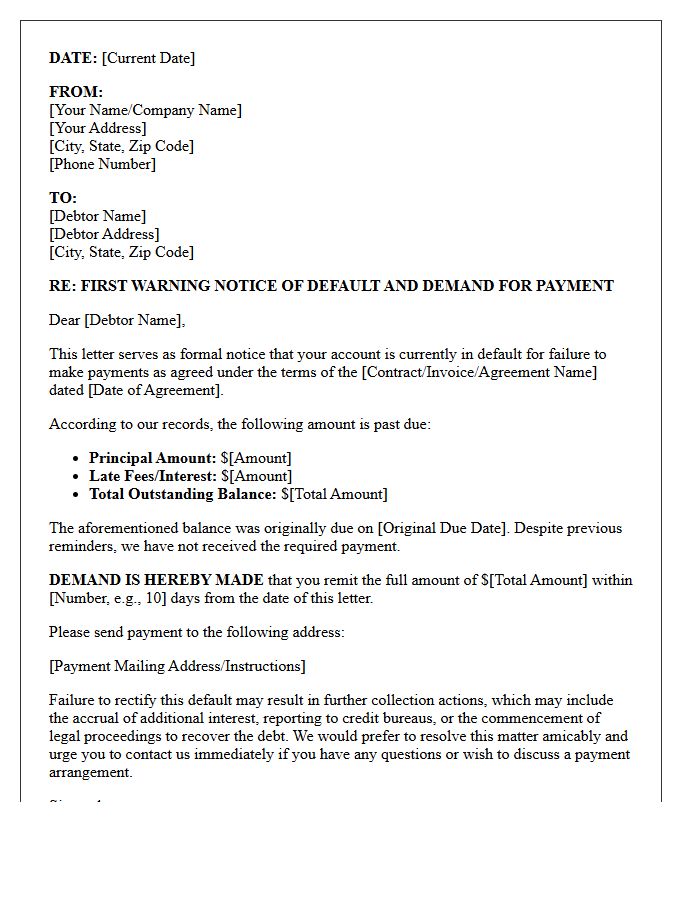

First Warning Notice of Default and Demand for Payment Letter

A First Warning Notice of Default and Demand for Payment Letter is a critical legal document informing a debtor of a breach of contract due to missed payments. This formal notification serves as a final opportunity to resolve outstanding debts before escalating to legal action or asset repossession. It outlines the specific amount owed, applicable late fees, and a strict deadline for compliance. Receiving this letter indicates that the creditor is initiating the acceleration clause, making the entire balance due immediately if the default is not rectified promptly.

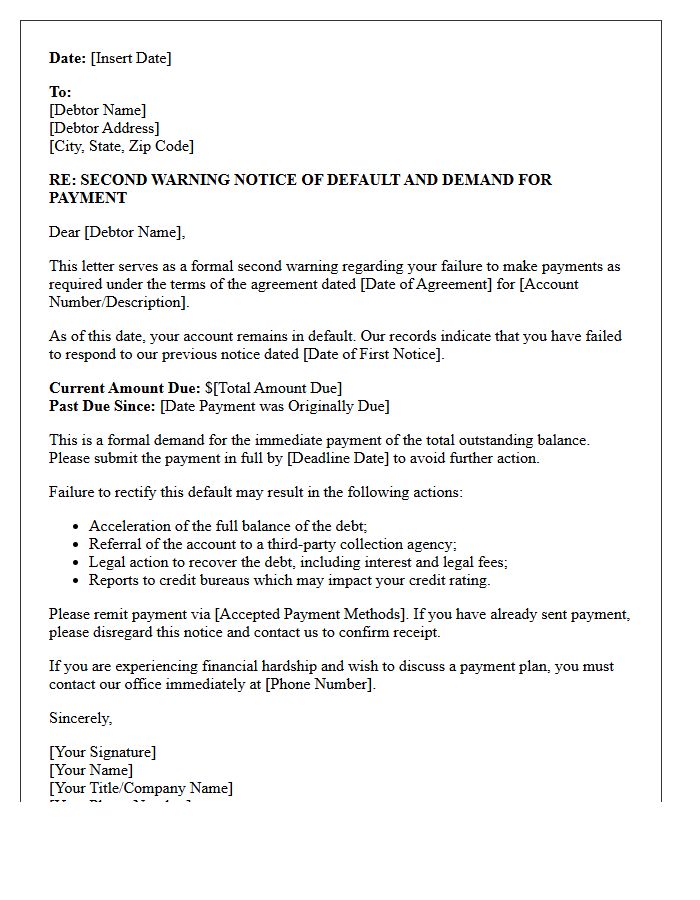

Second Warning Notice of Default and Demand for Payment Letter

A Second Warning Notice of Default and Demand for Payment is a formal legal document issued when a debtor fails to resolve arrears following an initial alert. It serves as a final opportunity to settle outstanding debts before the creditor initiates aggressive legal action or repossession. This letter explicitly states the total amount due, includes late fees, and sets a strict deadline for payment. Ignoring this notice typically results in credit score damage and potential litigation, making immediate communication or full payment essential to avoid further financial penalties.

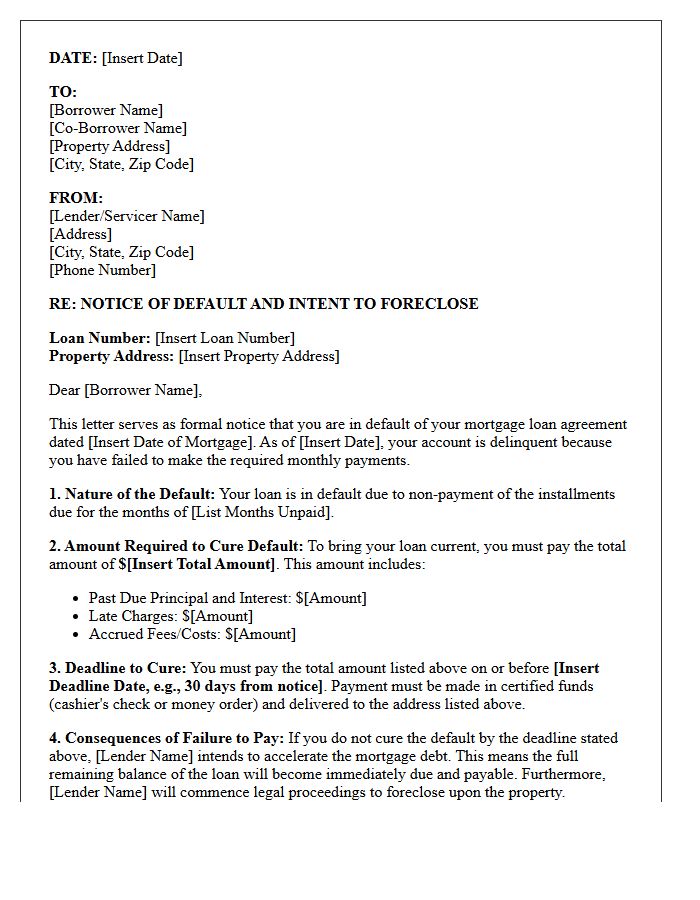

Final Pre-Foreclosure Notice of Default and Demand for Payment Letter

A Final Pre-Foreclosure Notice of Default and Demand for Payment Letter is a critical legal warning sent by lenders when a mortgage is severely delinquent. This formal document serves as the final opportunity to resolve unpaid debts before the lender initiates formal foreclosure proceedings. It outlines the total amount due, includes late fees, and provides a strict deadline for payment. Ignoring this notice results in the loss of property rights, making it essential to contact your servicer immediately to explore loss mitigation options or loan reinstatement to save your home.

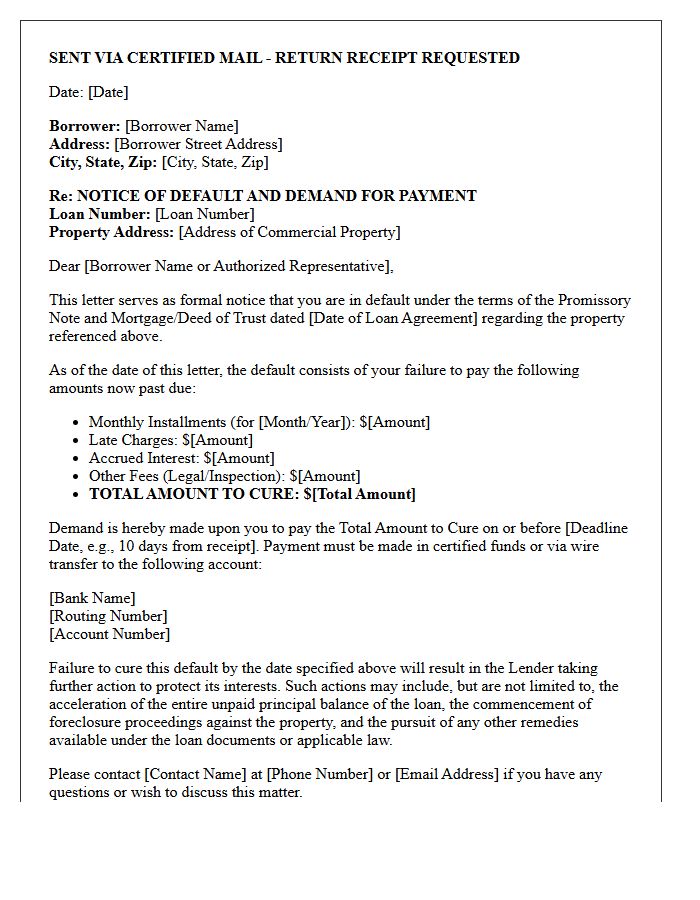

Commercial Mortgage Notice of Default and Demand for Payment Letter

A Commercial Mortgage Notice of Default and Demand for Payment is a critical legal document issued by a lender when a borrower breaches loan terms. It serves as formal notice that the loan is in default due to missed payments or covenant violations. This letter triggers a specific "cure period," allowing the borrower to rectify the debt before foreclosure proceedings begin. Receiving this demand requires immediate action to negotiate a workout agreement or payment plan, as it represents the final warning before the lender exercises acceleration of the entire loan balance.

Residential Mortgage Notice of Default and Demand for Payment Letter

A residential mortgage Notice of Default is a formal legal document issued by a lender when a borrower breaches their loan contract, typically through missed payments. This letter serves as the final warning before the foreclosure process begins. It outlines the specific arrears owed, including late fees and interest, and provides a strict deadline for payment. To prevent the loss of the property, the homeowner must satisfy the Demand for Payment within the specified timeframe to reinstate the loan and successfully avoid formal legal proceedings.

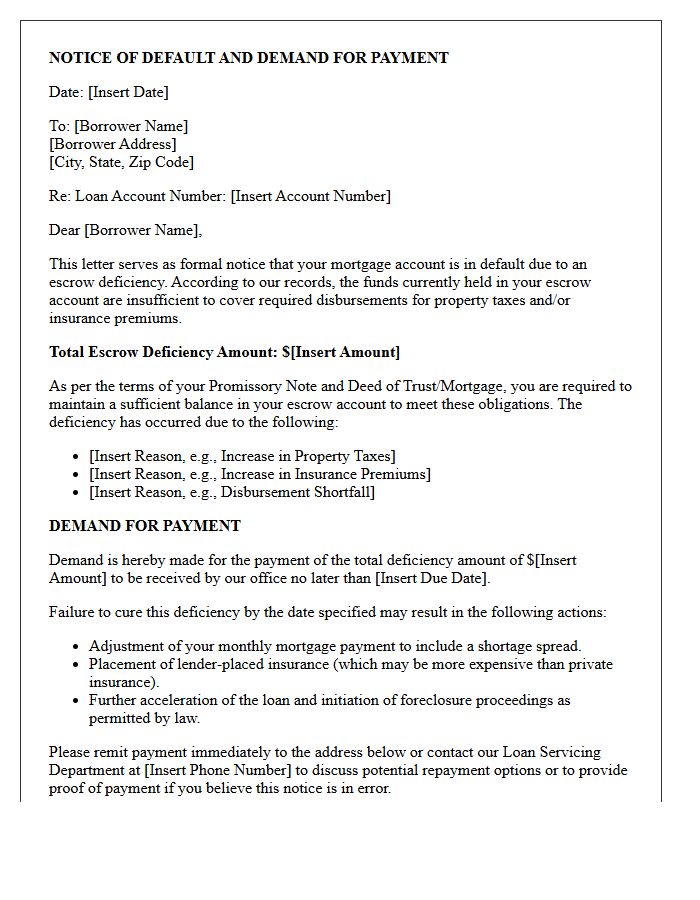

Escrow Deficiency Notice of Default and Demand for Payment Letter

An Escrow Deficiency Notice of Default is a formal legal demand issued when a mortgage account lacks sufficient funds to cover property taxes or insurance premiums. Receiving this letter indicates a breach of contract, requiring the borrower to replenish the escrow balance immediately. Failure to resolve the shortage can lead to foreclosure proceedings or the implementation of costly lender-placed insurance. It is critical to review the provided escrow analysis, verify the calculations for accuracy, and submit the requested payment by the specified deadline to maintain loan compliance and protect property ownership.

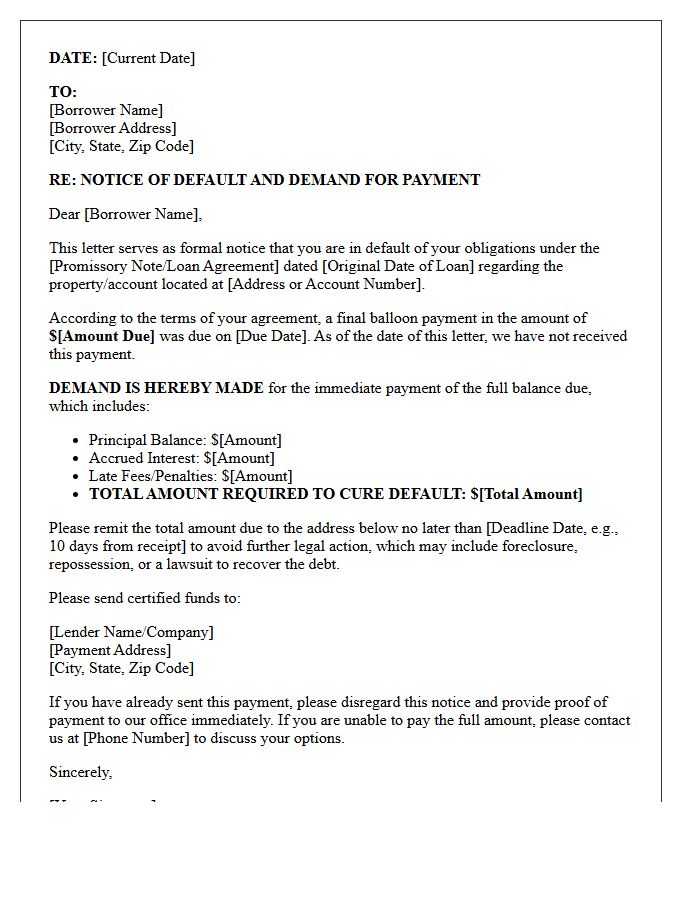

Balloon Payment Notice of Default and Demand for Payment Letter

A Balloon Payment Notice of Default is a formal legal notification issued when a borrower fails to pay the final large lump sum due at the end of a loan term. This Demand for Payment Letter serves as a final warning, accelerating the debt and initiating the foreclosure or repossession process. It outlines the total outstanding balance, including accrued interest and late fees, providing a strict deadline for remediation. Understanding this document is critical for homeowners or business owners to avoid immediate foreclosure and protect their financial equity through urgent refinancing or legal intervention.

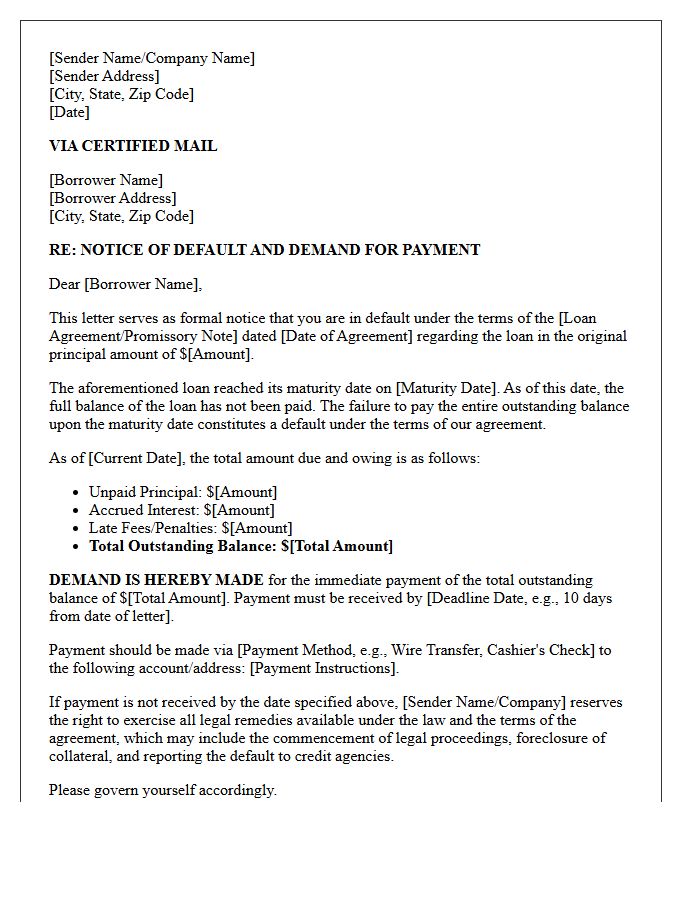

Maturity Date Notice of Default and Demand for Payment Letter

A Maturity Date Notice of Default and Demand for Payment Letter is a formal legal notification sent when a loan reaches its final due date without full repayment. This document serves as an official declaration that the borrower is in breach of contract. It strictly demands the immediate settlement of the remaining principal, accrued interest, and late fees. Receiving this letter is critical, as it often acts as the final prerequisite before a lender initiates foreclosure or legal debt collection proceedings to recover the outstanding balance.

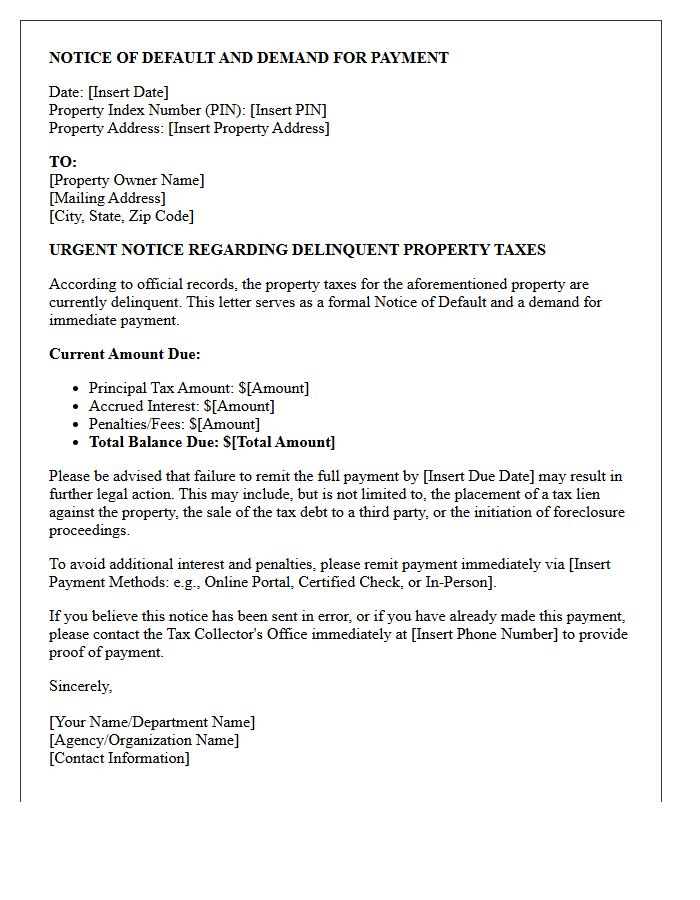

Property Tax Delinquency Notice of Default and Demand for Payment Letter

A property tax delinquency notice serves as a formal legal warning that your real estate taxes are past due. This critical document acts as a Notice of Default, informing the owner that the government has initiated a lien against the property. The letter includes a formal Demand for Payment, outlining the total balance, accrued interest, and strict deadlines. Ignoring this notice can lead to severe consequences, including significant financial penalties or even a tax foreclosure. Promptly addressing the debt is essential to protect your legal ownership rights and prevent a public auction of the asset.

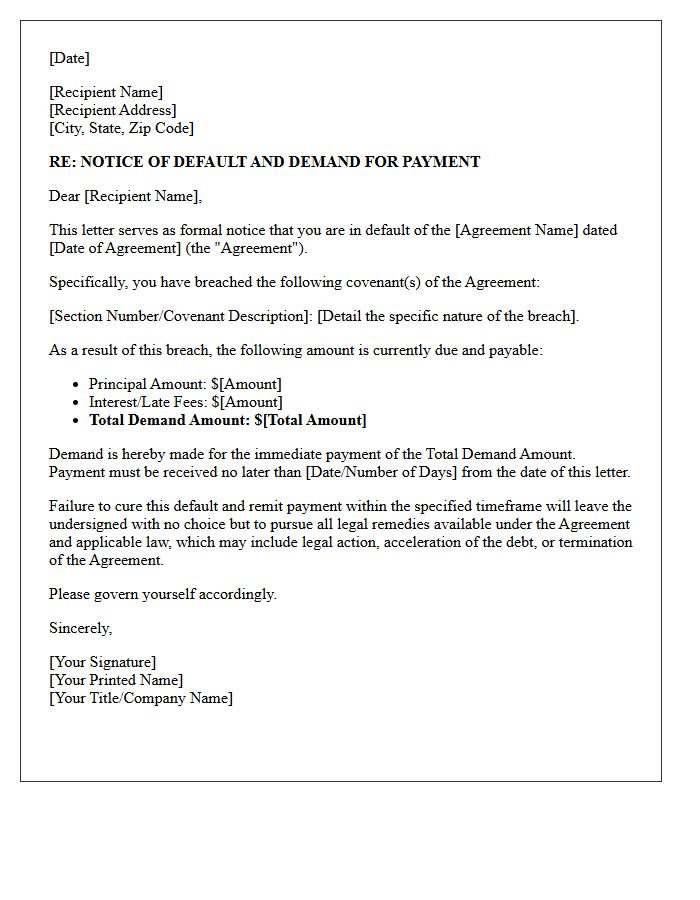

Breach of Covenant Notice of Default and Demand for Payment Letter

A Breach of Covenant Notice of Default is a formal legal document issued when a borrower violates specific loan conditions. It serves as a mandatory warning that contractual promises, such as maintaining insurance or financial ratios, have been broken. This letter includes a Demand for Payment, requiring the recipient to cure the default within a set timeframe or face immediate acceleration of the entire debt. Timely response is critical to avoid foreclosure, asset seizure, or legal action. Understanding your rights and obligations during this grace period is essential for financial protection.

Cure Period Notice of Default and Demand for Payment Letter

A Cure Period Notice of Default and Demand for Payment Letter is a formal legal notification sent to a party in breach of contract. It identifies specific violations, typically unpaid debts, and grants a mandatory grace period to rectify the issue. This document serves as an essential procedural prerequisite before a creditor can accelerate debt or initiate litigation. To avoid legal consequences or contract termination, the recipient must provide full payment or correct the default within the specified cure timeframe, effectively restoring the original contractual agreement.

What is a Notice of Default and Demand for Payment?

A Notice of Default and Demand for Payment is a formal legal document issued by a lender to a borrower stating that the borrower has failed to meet the contractual obligations of a loan, typically through missed payments. It serves as an official warning that legal action or foreclosure may commence if the outstanding debt is not paid within a specific timeframe.

What information must be included in a Notice of Default?

The notice must clearly state the total amount past due, including late fees and interest, the specific nature of the default, the deadline to cure the default, and the contact information for the lender. It also outlines the specific actions the lender will take, such as acceleration of the loan or repossession of collateral, if the demand is not met.

How long do I have to respond after receiving a Demand for Payment?

The timeframe to "cure" the default varies by state law and the terms of your original contract, but it is typically between 15 and 30 days. Failure to provide the required funds or reach an agreement with the lender by the deadline specified in the notice can result in the immediate acceleration of the entire loan balance.

Can a Notice of Default be rescinded or canceled?

Yes, a Notice of Default can be rescinded if the borrower pays the full amount demanded, including any associated legal fees and penalties, before the deadline. Alternatively, a lender may agree to cancel the notice if both parties successfully negotiate a loan modification, forbearance agreement, or a repayment plan.

What are the legal consequences of ignoring a Notice of Default and Demand for Payment?

Ignoring the notice typically leads to the acceleration of the debt, meaning the entire remaining balance becomes due immediately. This process often transitions into a formal foreclosure proceeding for real estate or the repossession of personal property, and it will significantly damage the borrower's credit score.

Comments