An Initial Escrow Account Disclosure Statement provides a detailed breakdown of estimated taxes, insurance premiums, and other charges your lender expects to pay from your escrow account during the first year of your mortgage. This transparency ensures you understand your monthly payment obligations and required reserves. To simplify your documentation process, below are some ready to use templates.

Image cover: Essential Templates and Samples for Your Initial Escrow Account Disclosure Statement

Letter Samples List

- Initial Escrow Account Disclosure Statement Cover Letter

- Revised Initial Escrow Account Disclosure Statement Letter

- Escrow Account Setup and Initial Disclosure Confirmation Letter

- Initial Escrow Account Breakdown and Payment Explanation Letter

- Notice of Escrow Account Funding and Initial Disclosure Letter

- Initial Escrow Account Tax and Insurance Allocation Letter

- Supplemental Initial Escrow Account Disclosure Information Letter

- Initial Escrow Account Disclosure Statement Acknowledgement Letter

- Post-Closing Initial Escrow Account Disclosure Verification Letter

- Initial Escrow Account Cushion Requirement Explanation Letter

- Mortgage Servicing Initial Escrow Account Disclosure Transmittal Letter

- Initial Escrow Account Disclosure Statement Correction Letter

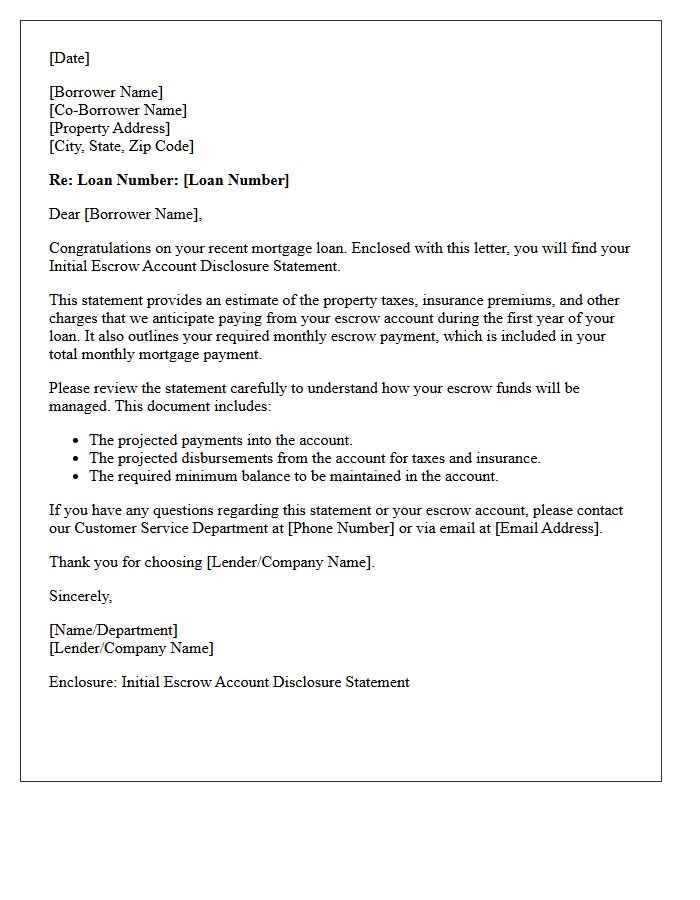

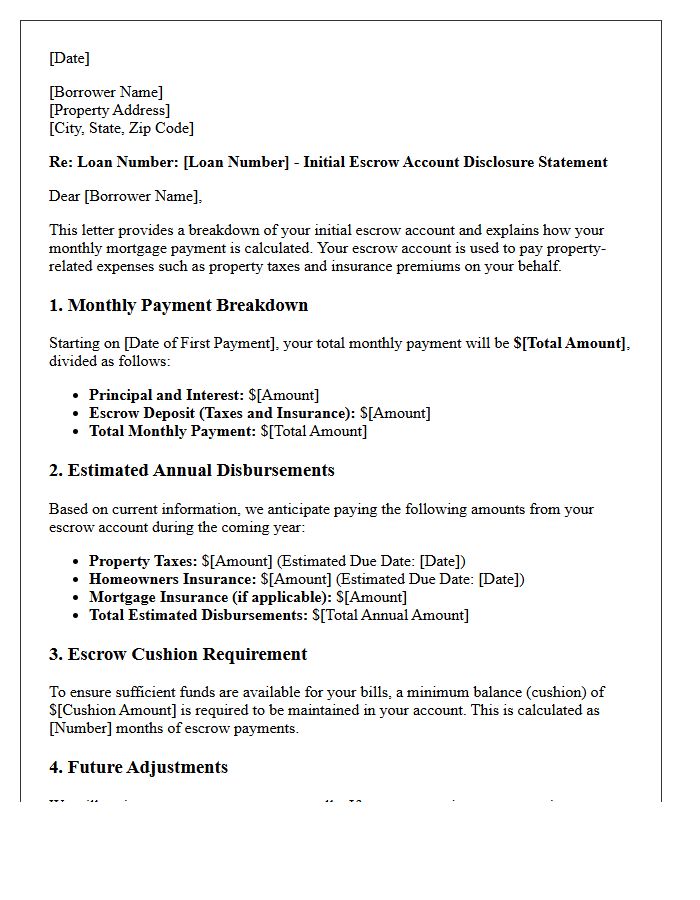

Initial Escrow Account Disclosure Statement Cover Letter

An Initial Escrow Account Disclosure Statement Cover Letter is a vital document sent by lenders at closing or within 45 days of establishing an escrow account. It formally introduces the projected payments for property taxes and insurance premiums over the next year. This letter helps homeowners understand their monthly mortgage breakdown and the required minimum cushion to prevent account shortfalls. Reviewing this statement is essential for tracking how your funds are managed and ensuring all escrow disbursements are accurately scheduled to maintain your home's financial security.

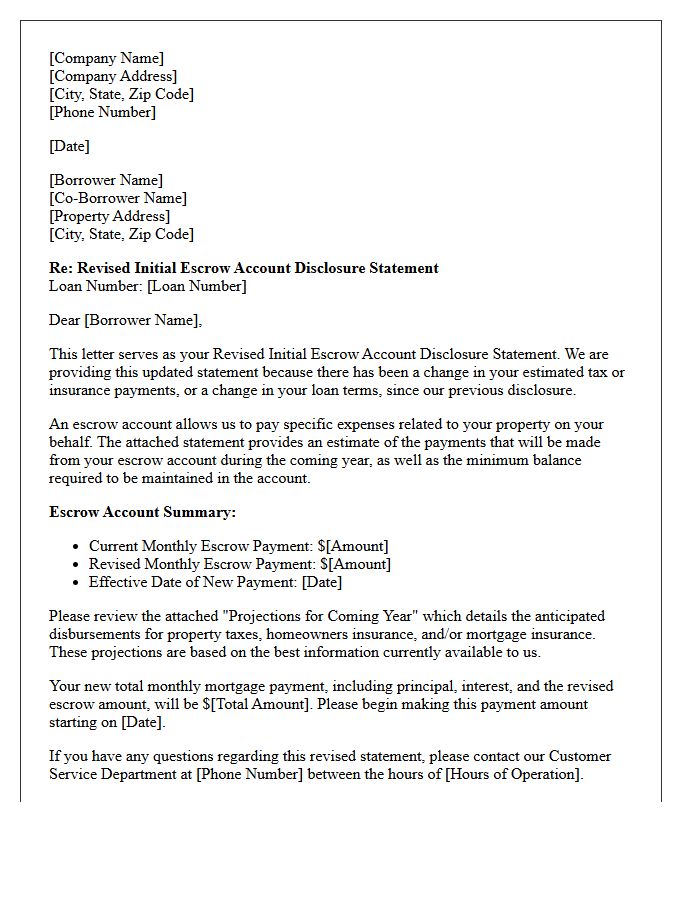

Revised Initial Escrow Account Disclosure Statement Letter

A Revised Initial Escrow Account Disclosure Statement is a critical document issued when changes occur to your mortgage escrow requirements. It provides an updated estimate of your property taxes, insurance premiums, and necessary monthly escrow payments. Lenders must provide this statement if your loan terms or payment amounts shift shortly after closing. Reviewing this document is essential to understand your new monthly obligation, ensure adequate funding for future disbursements, and avoid unexpected shortages or payment shocks during your loan's first year.

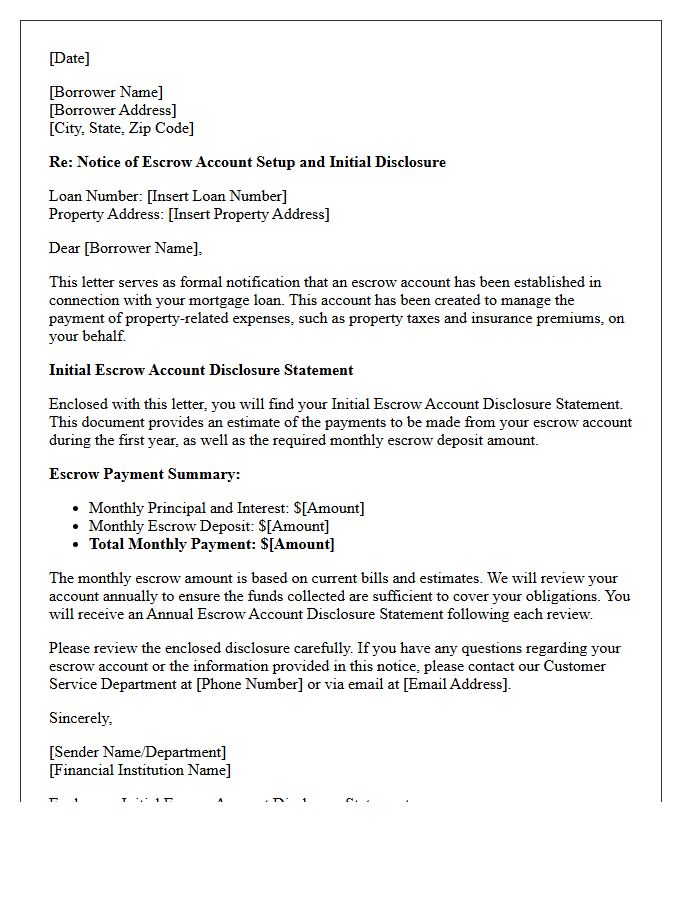

Escrow Account Setup and Initial Disclosure Confirmation Letter

The Escrow Account Setup and Initial Disclosure Confirmation Letter is a vital document provided by mortgage lenders during closing. It confirms the establishment of your escrow account, which manages property taxes and insurance payments. This letter provides an itemized initial escrow statement, detailing your monthly contributions and the projected disbursements for the year. It ensures transparency regarding your total monthly payment and outlines the required minimum cushion to prevent future shortages. Reviewing this document is essential to verify that all tax and insurance obligations are accurately calculated from the start.

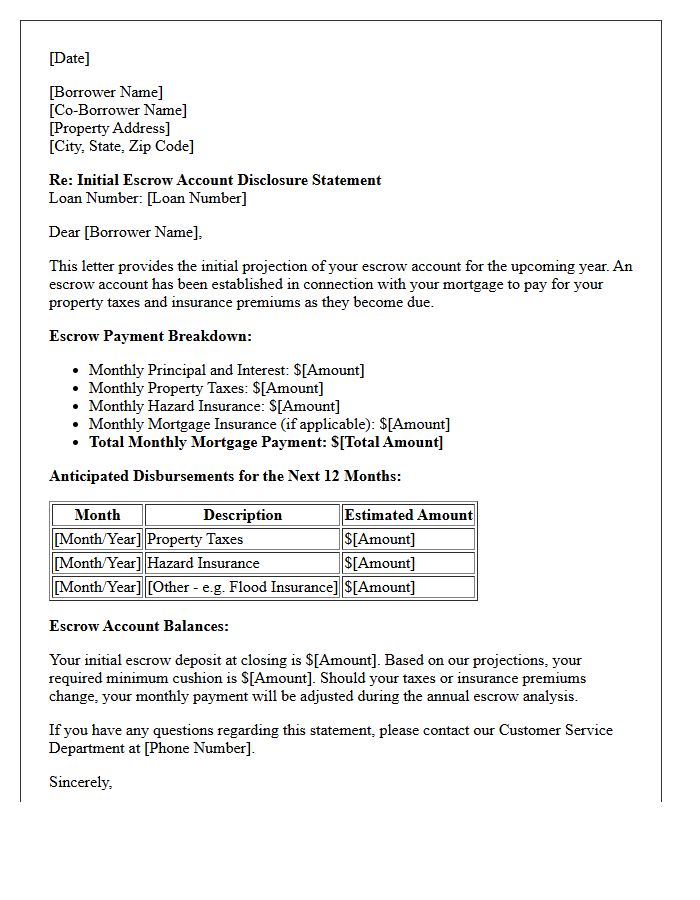

Initial Escrow Account Breakdown and Payment Explanation Letter

An Initial Escrow Account Breakdown provides a detailed 12-month projection of property taxes and insurance payments. This disclosure statement explains how your monthly mortgage payment is calculated and ensures sufficient funds cover future obligations. It tracks your starting balance, anticipated disbursements, and the required cushion to prevent shortages. Reviewing the Payment Explanation Letter is essential to understand any adjustments to your total monthly obligation and to verify that all escrowed items are accurately estimated for the upcoming year.

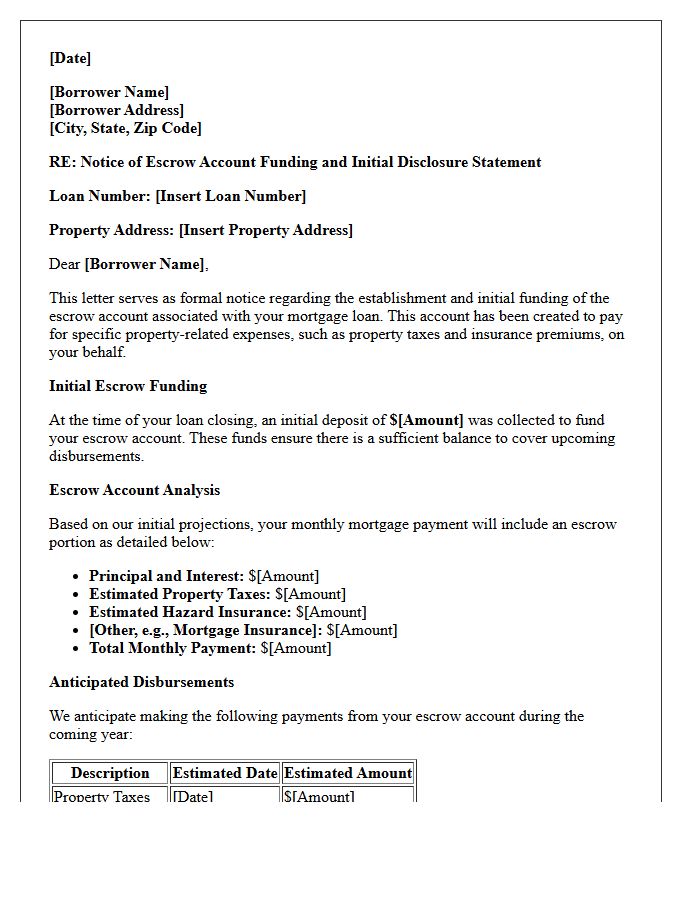

Notice of Escrow Account Funding and Initial Disclosure Letter

A Notice of Escrow Account Funding and Initial Disclosure Letter provide a detailed breakdown of your mortgage impound account. This essential document outlines the exact amount required at closing to establish your reserves for property taxes and insurance. It also provides a projected payment schedule for the upcoming year, ensuring transparency regarding your monthly housing costs. Reviewing this statement helps homeowners understand how their escrow payments are calculated and confirms that sufficient funds are set aside to cover mandatory third-party obligations without unexpected shortages.

Initial Escrow Account Tax and Insurance Allocation Letter

An Initial Escrow Account Tax and Insurance Allocation Letter is a mandatory disclosure provided at closing. It details the specific monthly amounts collected for property taxes and homeowners insurance premiums. This document ensures your escrow account maintains a sufficient balance to cover these future liabilities. It serves as a financial roadmap, highlighting your initial deposit and projected disbursements for the first year. Reviewing this letter is essential to understand how your total mortgage payment is distributed to prevent unexpected shortages or payment fluctuations.

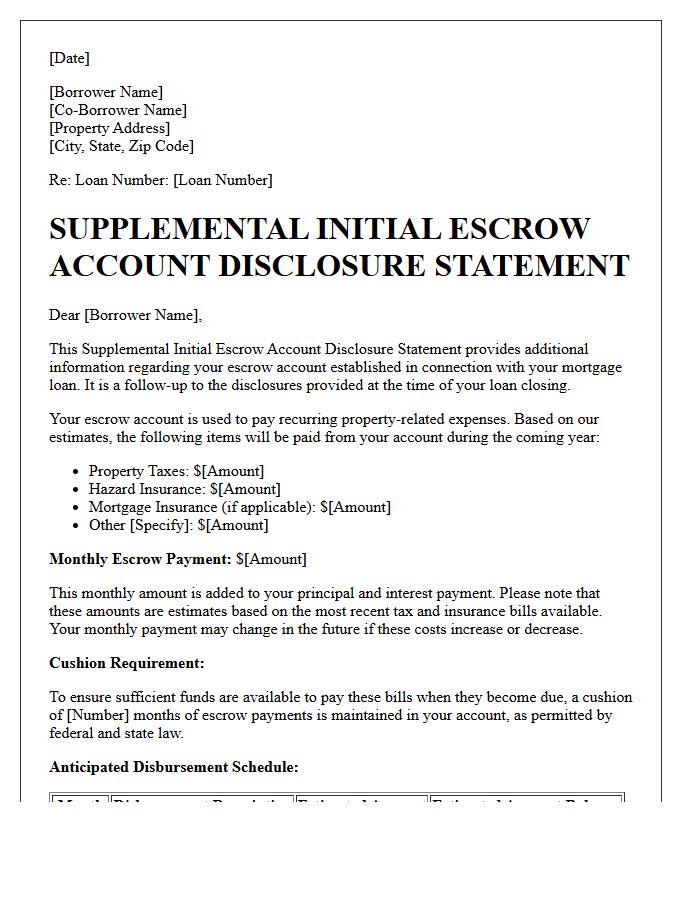

Supplemental Initial Escrow Account Disclosure Information Letter

The Supplemental Initial Escrow Account Disclosure Information Letter is a critical document provided during the mortgage closing process. It details the estimated property taxes and insurance premiums your lender will collect and pay on your behalf during the first year. This statement establishes your monthly escrow payment amount and ensures the account maintains a required minimum cushion to prevent future shortages. Reviewing this letter helps homeowners understand their total monthly financial commitment beyond just the principal and interest of the loan.

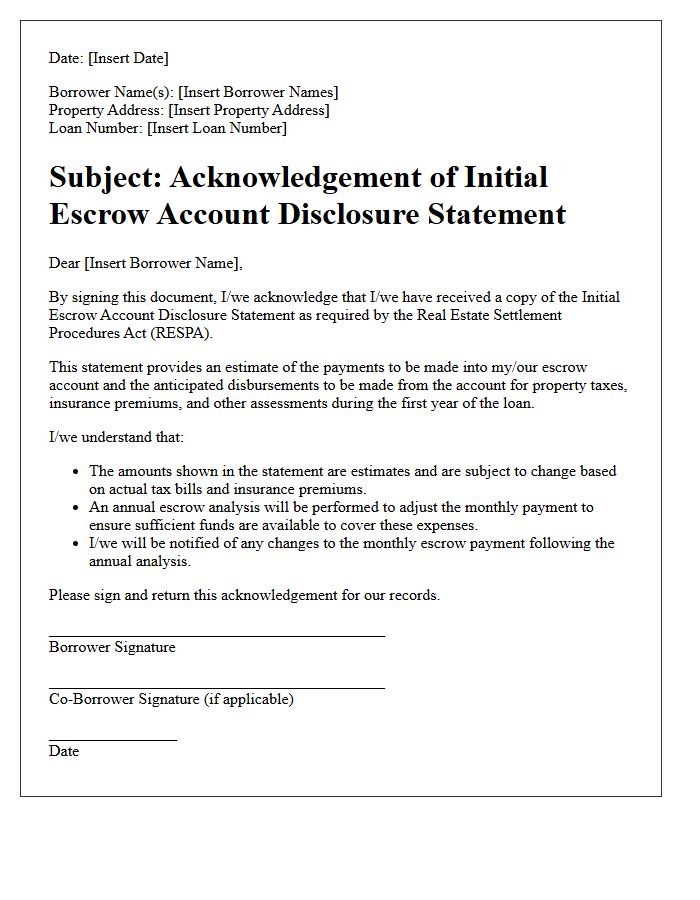

Initial Escrow Account Disclosure Statement Acknowledgement Letter

The Initial Escrow Account Disclosure Statement Acknowledgement Letter is a critical document confirming you received a detailed breakdown of your escrow payments. It outlines the estimated taxes, insurance premiums, and other charges your lender will pay on your behalf during the first year. By signing, you acknowledge the projected monthly escrow deposit and the required cushion amount. This ensures transparency regarding your total monthly mortgage obligation and prevents surprises during future escrow analysis updates. Reviewing this statement helps homeowners track how their funds are managed for essential property expenses.

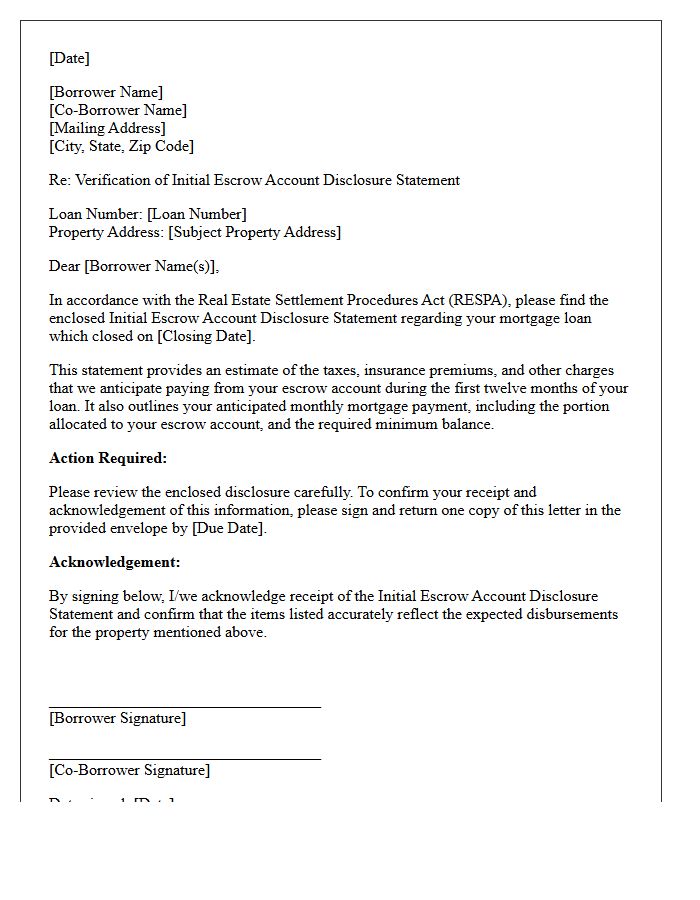

Post-Closing Initial Escrow Account Disclosure Verification Letter

A Post-Closing Initial Escrow Account Disclosure Verification Letter is a critical document used to confirm the accuracy of impound account calculations after a real estate closing. It ensures that the borrower's monthly payments for taxes and insurance align with the legal requirements of the Real Estate Settlement Procedures Act (RESPA). Lenders use this verification to prevent escrow shortages or surpluses, providing transparency regarding the projected disbursement schedule. Reviewing this letter helps homeowners understand their total housing expenses and ensures the lender maintains a proper cushion for future bills.

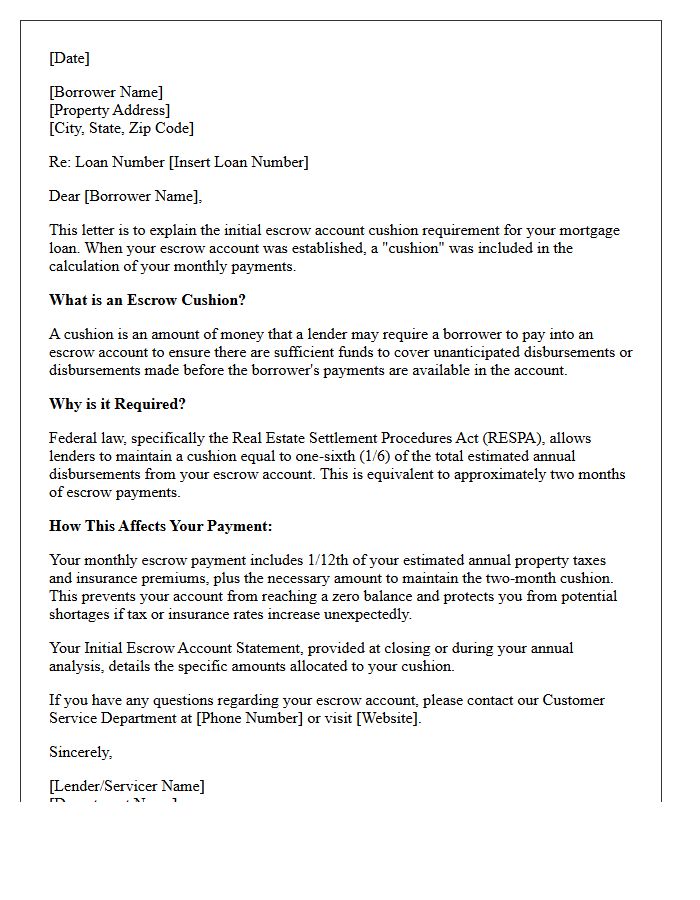

Initial Escrow Account Cushion Requirement Explanation Letter

An Initial Escrow Account Cushion explanation letter clarifies the reserve funds lenders collect to prevent account shortages. Federal law under RESPA allows lenders to maintain a cushion of up to two months of estimated annual disbursements for taxes and insurance. This buffer ensures sufficient capital remains in the account during payment fluctuations. Homeowners should review this document to understand their total monthly mortgage obligation and how the lender calculates the minimum balance required to protect against unexpected increases in property levies or premiums.

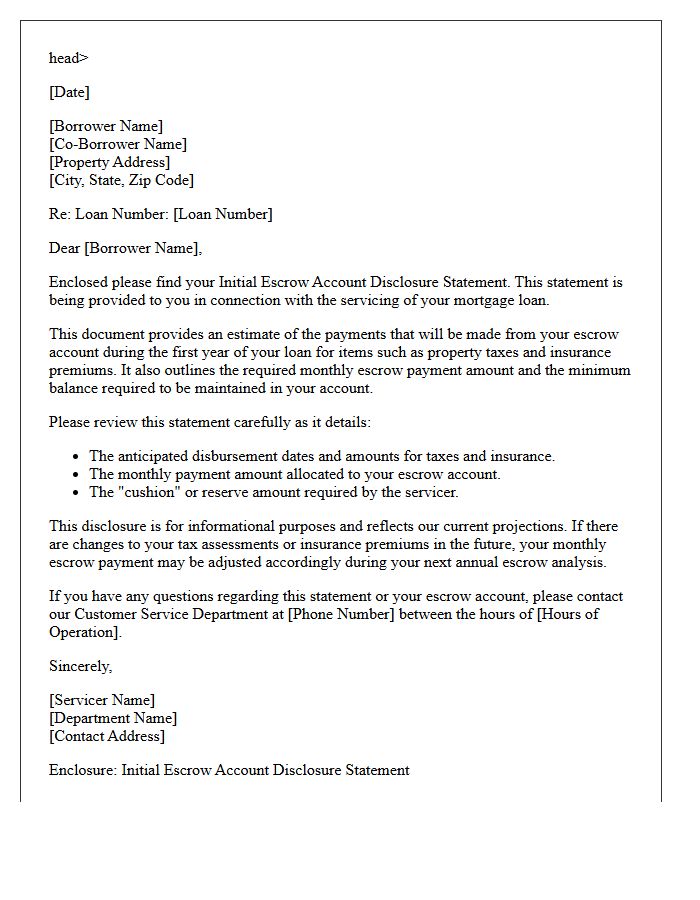

Mortgage Servicing Initial Escrow Account Disclosure Transmittal Letter

The Mortgage Servicing Initial Escrow Account Disclosure Transmittal Letter is a mandatory document provided at closing or within 45 days of establishing an escrow account. It outlines the estimated property taxes and insurance premiums the lender expects to pay on your behalf during the first year. This statement is essential for understanding your total monthly payment, as it details the escrow deposit requirements and provides a projection of the account balance to ensure no funding shortages occur during the annual cycle.

Initial Escrow Account Disclosure Statement Correction Letter

An Initial Escrow Account Disclosure Statement Correction Letter is a formal notice issued by a mortgage servicer to rectify inaccuracies in a previous escrow analysis. This document ensures compliance with RESPA guidelines by updating projected property tax or insurance payments. Homeowners must review this letter carefully, as it often results in a payment adjustment to their monthly mortgage bill. Promptly addressing these corrections helps prevent unexpected escrow shortages or surpluses, maintaining the financial accuracy of your housing account throughout the fiscal year.

What is an Initial Escrow Account Disclosure Statement?

An Initial Escrow Account Disclosure Statement is a document provided by your lender that outlines the estimated taxes, insurance premiums, and other charges expected to be paid from your escrow account during the first twelve months of your mortgage.

When is the lender required to provide the Initial Escrow Statement?

Under RESPA guidelines, lenders must provide this statement at closing or within 45 days of establishing the escrow account. It serves as the baseline for future annual escrow analyses.

What specific information is included in the Initial Escrow Disclosure?

The statement includes your monthly mortgage payment breakdown, the specific amounts allocated for property taxes and homeowners insurance, the anticipated dates of disbursements, and the required minimum cushion or reserve balance.

Why is there a "cushion" requirement in my escrow disclosure?

Lenders typically require a "cushion" of up to two months of escrow payments to cover unexpected increases in tax assessments or insurance premiums, ensuring the account does not fall into a negative balance.

How does the Initial Escrow Statement differ from the Annual Escrow Analysis?

The Initial Escrow Statement is a projection for the first year of the loan, while the Annual Escrow Analysis is a retrospective review performed every year to adjust your monthly payments based on actual taxes and insurance costs paid.

Comments