A Notice of Escrow Account Deficiency occurs when your account balance falls short of the required minimum to cover upcoming property taxes and insurance premiums. This shortage typically results from rising tax assessments or insurance rate hikes. To help you address this financial shortfall professionally, below are some ready to use template options for your correspondence.

Image cover: Essential Guide to Escrow Account Deficiency Notices: Official Templates and Communication Samples

Letter Samples List

- Standard Notice of Escrow Account Deficiency Letter

- Annual Mortgage Escrow Account Deficiency Letter

- Urgent Notice of Escrow Account Deficiency Letter

- Post-Disbursement Escrow Account Deficiency Letter

- Property Tax Increase Escrow Account Deficiency Letter

- Homeowners Insurance Premium Escrow Account Deficiency Letter

- Escrow Account Deficiency and Payment Adjustment Letter

- Delinquent Escrow Account Deficiency Warning Letter

- Escrow Account Deficiency Repayment Option Letter

- Final Notice of Escrow Account Deficiency Letter

- Shortage and Escrow Account Deficiency Disclosure Letter

- Mid-Year Escrow Account Deficiency Evaluation Letter

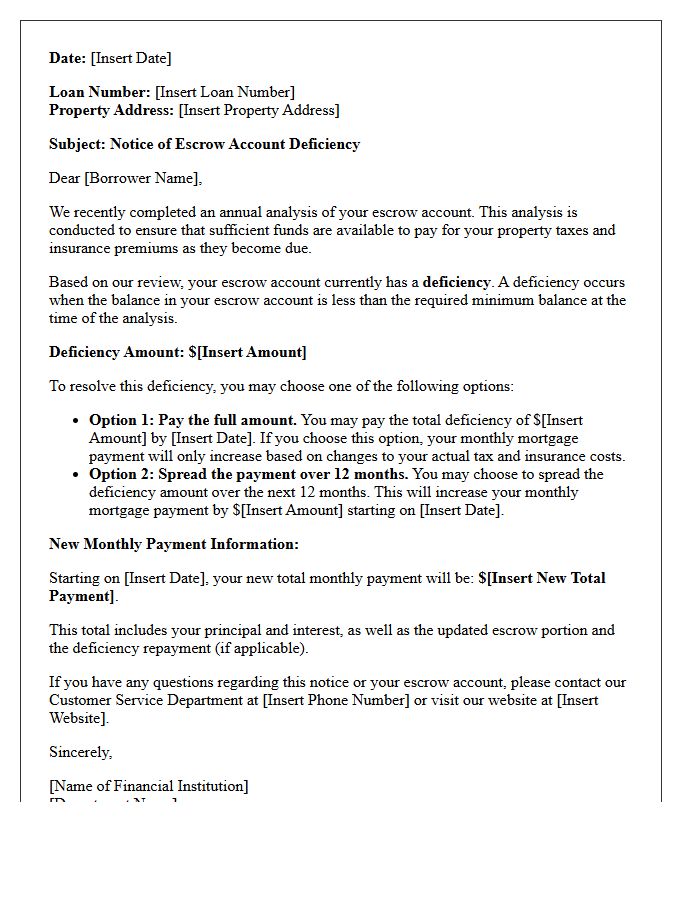

Standard Notice of Escrow Account Deficiency Letter

A Standard Notice of Escrow Account Deficiency occurs when your account balance falls below the required minimum due to increased tax or insurance costs. This letter serves as a formal notification that your current monthly payments are insufficient to cover future disbursements. Homeowners typically have options to pay the shortage as a one-time lump sum or spread the cost across future monthly mortgage payments. Timely action is essential to avoid significant payment spikes or potential escrow shortages that could impact your overall loan stability and household budgeting.

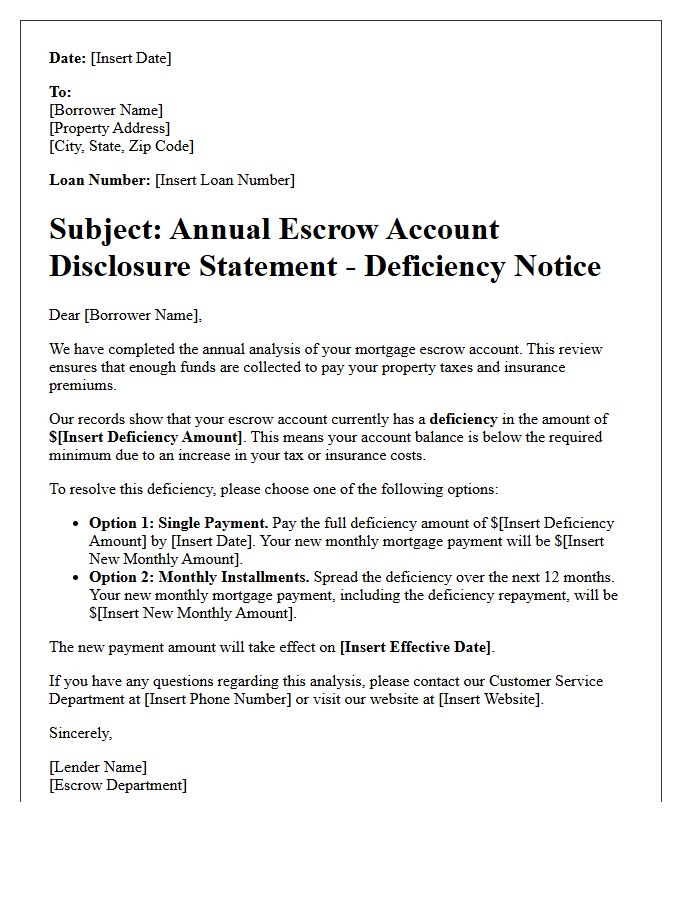

Annual Mortgage Escrow Account Deficiency Letter

An Annual Mortgage Escrow Account Deficiency Letter informs you that your escrow balance is insufficient to cover upcoming property taxes and insurance premiums. This occurs when escrow disbursements exceed the funds collected monthly. To resolve this, lenders typically offer options: paying the shortage as a one-time lump sum or spreading the cost across future monthly payments, which increases your total mortgage bill. Reviewing your annual escrow analysis statement is crucial to verify tax assessment changes or insurance rate hikes that triggered the shortfall and ensure your account remains current.

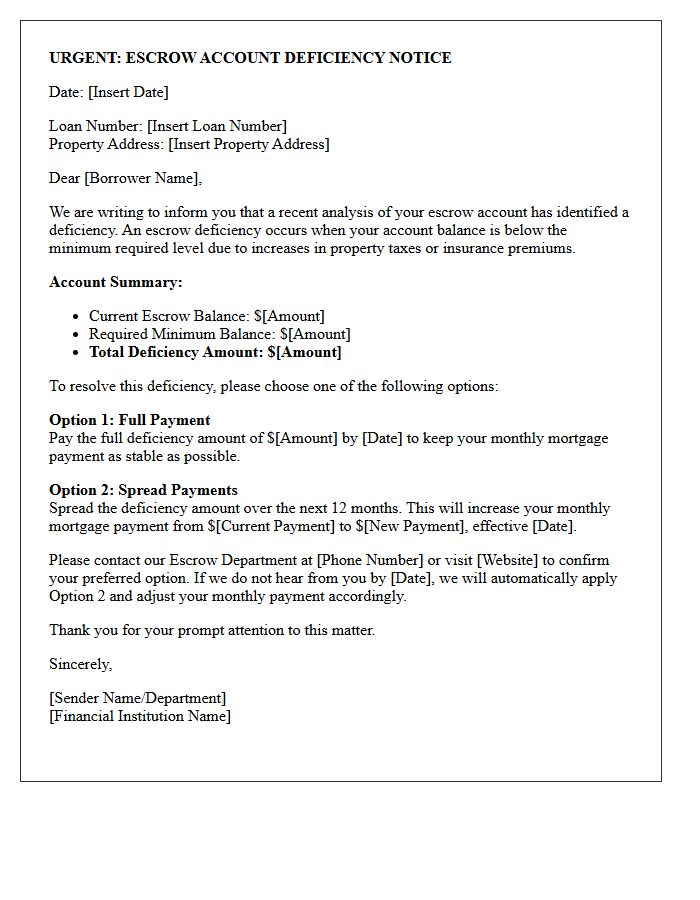

Urgent Notice of Escrow Account Deficiency Letter

An Urgent Notice of Escrow Account Deficiency indicates that your mortgage impound account has insufficient funds to cover rising property taxes or insurance premiums. Receiving this letter means your monthly mortgage payment will likely increase to rectify the shortage and maintain the required minimum balance. It is critical to review the provided escrow analysis immediately to understand your repayment options, such as making a one-time payment or spreading the cost over the next year, to avoid potential delinquency or financial penalties on your home loan.

Post-Disbursement Escrow Account Deficiency Letter

A post-disbursement escrow account deficiency letter notifies a homeowner that their escrow balance is insufficient to cover projected taxes or insurance premiums. This occurs when actual costs exceed previous estimates. To resolve this shortage, lenders typically offer options: paying the total amount upfront or spreading the deficiency over future monthly installments. Addressing this promptly is essential to avoid significant increases in your mortgage payment and ensure continuous coverage of your property obligations. Reviewing your annual escrow analysis helps verify these adjustments against actual billing statements.

Property Tax Increase Escrow Account Deficiency Letter

Receiving an escrow deficiency letter means your monthly mortgage payment will likely rise. When property taxes increase, your lender must cover the shortfall to pay the county, resulting in a negative escrow balance. You typically have two options: pay the entire shortage upfront to keep your principal payment stable, or spread the deficit over the next year. It is vital to review your annual escrow analysis to understand how higher assessments or tax rates directly impact your total monthly housing costs and future financial obligations.

Homeowners Insurance Premium Escrow Account Deficiency Letter

A homeowners insurance premium escrow account deficiency letter informs you that your escrow balance is insufficient to cover rising insurance costs. This usually occurs after a premium increase from your insurer. To resolve the shortage, lenders typically offer two options: making a one-time payment to cover the deficit or increasing your monthly mortgage payment to spread the cost over the coming year. It is vital to review your annual escrow analysis immediately to ensure your property taxes and insurance are correctly calculated to avoid future financial surprises.

Escrow Account Deficiency and Payment Adjustment Letter

An escrow account deficiency occurs when your account balance falls below the required minimum due to increased property taxes or insurance premiums. When this happens, your mortgage servicer sends a payment adjustment letter outlining the shortage. You typically have two options: pay the entire deficiency as a one-time lump sum or spread the cost across your monthly mortgage payments. Failure to address this escrow shortfall will result in a mandatory increase in your total monthly housing expense to ensure future obligations are fully funded.

Delinquent Escrow Account Deficiency Warning Letter

A Delinquent Escrow Account Deficiency Warning Letter is a formal notice from your mortgage servicer indicating your escrow account has a negative balance. This occurs when property taxes or insurance premiums exceed the funds collected. The letter outlines your repayment options, such as a one-time payment or increased monthly installments. Ignoring this notice can lead to significant monthly payment hikes or potential default. It is crucial to review your annual escrow analysis statement to understand the underlying shortage and ensure your home remains protected without financial strain.

Escrow Account Deficiency Repayment Option Letter

An Escrow Account Deficiency Repayment Option Letter notifies a homeowner that their escrow balance has fallen below the required minimum. This shortfall occurs when property taxes or insurance premiums exceed previous estimates. To resolve the deficiency, lenders typically offer three choices: paying the full amount upfront, spreading the cost over the next twelve monthly mortgage payments, or a combination of both. Carefully reviewing these options is essential to understand how your future monthly mortgage payment will be adjusted to maintain a federally mandated cushion.

Final Notice of Escrow Account Deficiency Letter

A Final Notice of Escrow Account Deficiency warns homeowners that their escrow balance is insufficient to cover projected property taxes or insurance premiums. This legal notification requires immediate action to rectify the shortfall. Failure to pay the specified amount or adjust monthly mortgage payments can lead to financial penalties or a lapse in coverage. Homeowners should carefully review the detailed breakdown provided by the lender to understand the cause of the underfunding and ensure their property remains protected and compliant with loan agreements.

Shortage and Escrow Account Deficiency Disclosure Letter

A Shortage and Escrow Account Deficiency Disclosure Letter notifies homeowners when their property tax or insurance payments exceed the funds available in their escrow account. This document outlines the escrow shortage, which occurs when the current balance is too low, and a deficiency, which happens when the balance is negative. To resolve this imbalance, lenders typically offer options: paying the total shortfall upfront or increasing monthly mortgage payments. Timely review is essential to avoid unexpected payment increases and ensure all escrow obligations are met for the upcoming year.

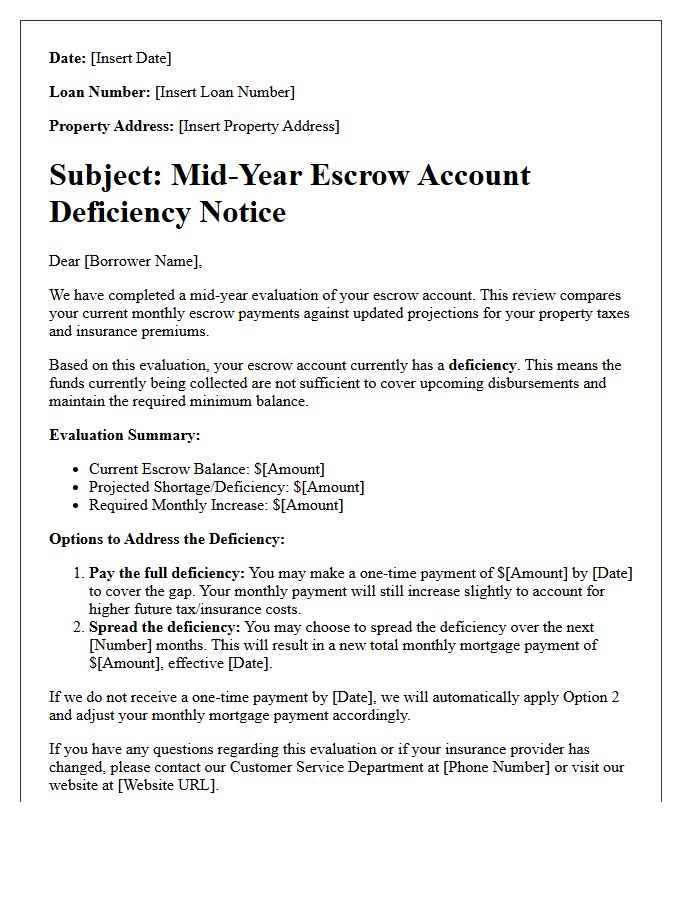

Mid-Year Escrow Account Deficiency Evaluation Letter

A Mid-Year Escrow Account Deficiency Evaluation Letter notifies homeowners that their escrow balance is insufficient to cover projected property taxes and insurance. This occurs when disbursements exceed initial estimates, often due to rising tax rates. Receiving this letter means you may face an underage, requiring a one-time payment or increased monthly mortgage installments to rebalance the account. Proactively reviewing this evaluation helps prevent significant payment spikes at year-end, ensuring your loan remains in good standing while covering essential homeownership obligations through your lender's dedicated holding account.

What is a Notice of Escrow Account Deficiency?

A Notice of Escrow Account Deficiency is a formal communication from your mortgage lender informing you that your escrow account balance is currently positive but falls below the minimum required reserve amount mandated by federal law or your loan agreement.

How does an escrow deficiency differ from an escrow shortage?

An escrow shortage occurs when the account balance is negative or insufficient to cover upcoming bills, whereas a deficiency occurs when the account has enough money to pay bills but does not maintain the required two-month "cushion" or reserve balance.

What causes a deficiency in an escrow account?

Escrow deficiencies are typically caused by an increase in property taxes or homeowners insurance premiums. When these costs rise, the minimum reserve amount required to be held in the account also increases proportionately.

What are my options for paying an escrow deficiency?

Lenders typically offer two options: you can pay the entire deficiency amount in a single lump-sum payment, or you can spread the repayment over a 12-month period, which will result in an increase to your monthly mortgage payment.

Will my monthly mortgage payment change after receiving this notice?

Yes, your monthly payment will likely increase. Even if you pay the deficiency in full, your monthly payment will rise to account for the higher cost of taxes and insurance moving forward to prevent future shortages.

Comments