The RESPA Escrow Cushion Disclosure Letter is a vital notification sent to borrowers regarding their mortgage impound accounts. Under Federal law, lenders may maintain a reserve to prevent shortages, but it cannot exceed two months of escrow payments. This document ensures transparency in account balancing and regulatory compliance. To assist your process, below are some ready to use templates.

Image cover: Mastering Your RESPA Escrow Cushion Disclosure: Professional Templates and Samples

Letter Samples List

- Initial RESPA Escrow Cushion Disclosure Letter

- Annual RESPA Escrow Cushion Analysis Letter

- Escrow Cushion Shortage and Deficiency Disclosure Letter

- RESPA Escrow Cushion Surplus Refund Letter

- Revised RESPA Escrow Cushion Disclosure Letter

- New Mortgage Escrow Cushion Establishment Letter

- Escrow Cushion Adjustment Notification Letter

- RESPA Compliant Escrow Cushion Summary Letter

- Mortgage Lender Escrow Cushion Policy Letter

- Escrow Cushion Voluntary Overpayment Acknowledgement Letter

- Aggregate Accounting Escrow Cushion Disclosure Letter

- Post Closing Escrow Cushion Verification Letter

- RESPA Escrow Cushion Limit Explanation Letter

- Transfer of Servicing Escrow Cushion Disclosure Letter

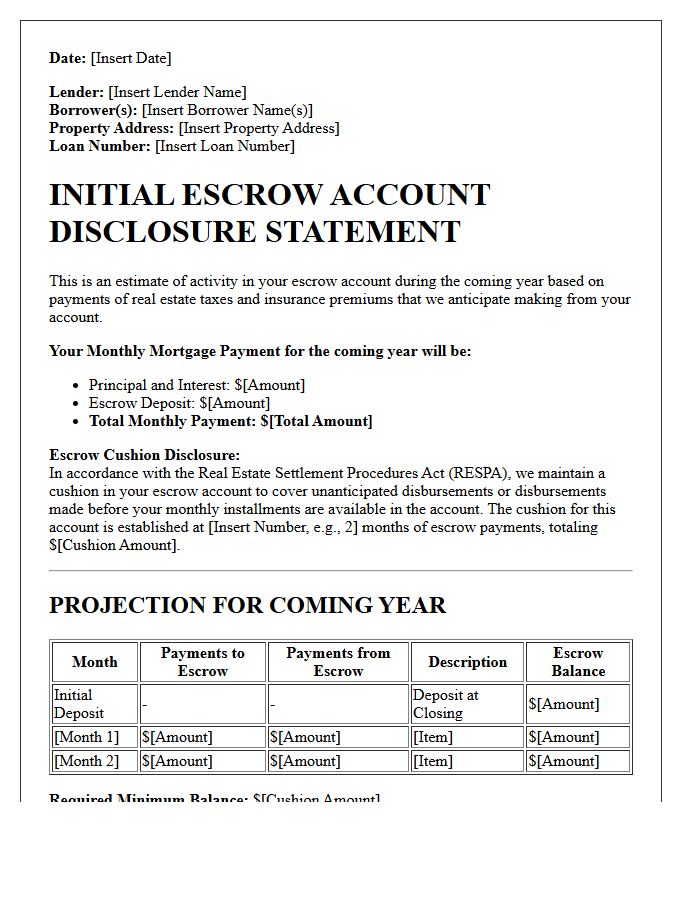

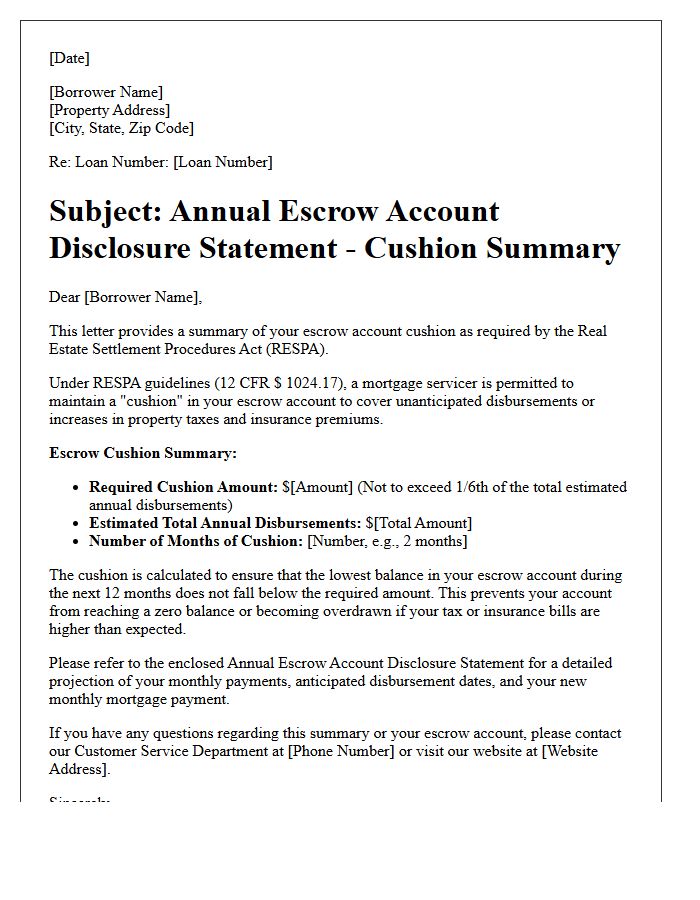

Initial RESPA Escrow Cushion Disclosure Letter

The Initial RESPA Escrow Cushion Disclosure Letter is a mandatory document provided at closing to ensure transparency regarding your mortgage account. Under the Real Estate Settlement Procedures Act, lenders are permitted to maintain a financial buffer, typically equal to two months of escrow payments. This cushion protects against fluctuations in property taxes or insurance premiums. Reviewing this statement is essential to understand your projected disbursements and verify that your prepaid expenses align with federal requirements, preventing unexpected shortages in your monthly mortgage obligations.

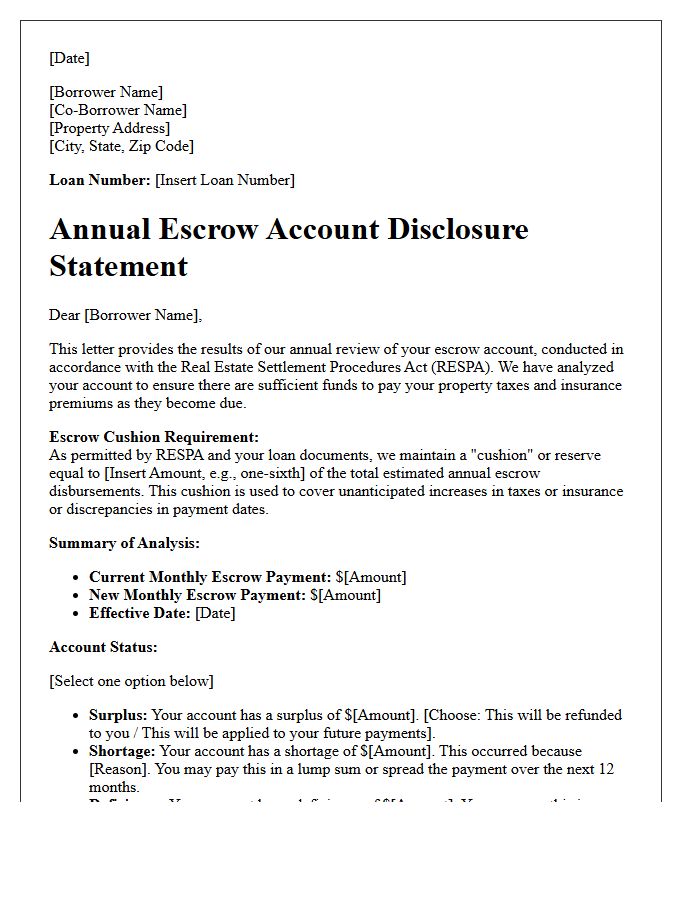

Annual RESPA Escrow Cushion Analysis Letter

The Annual RESPA Escrow Analysis is a mandatory review ensuring your account maintains a legal cushion. Lenders evaluate your property taxes and insurance premiums to prevent shortages. Federal law under RESPA limits this reserve to two months of estimated disbursements. If your costs fluctuate, your monthly mortgage payment will adjust accordingly. You will receive an annual statement detailing any surplus, which may be refunded, or a deficiency, requiring additional payments. Monitoring this letter is essential for managing your long-term homeownership costs and avoiding unexpected financial gaps.

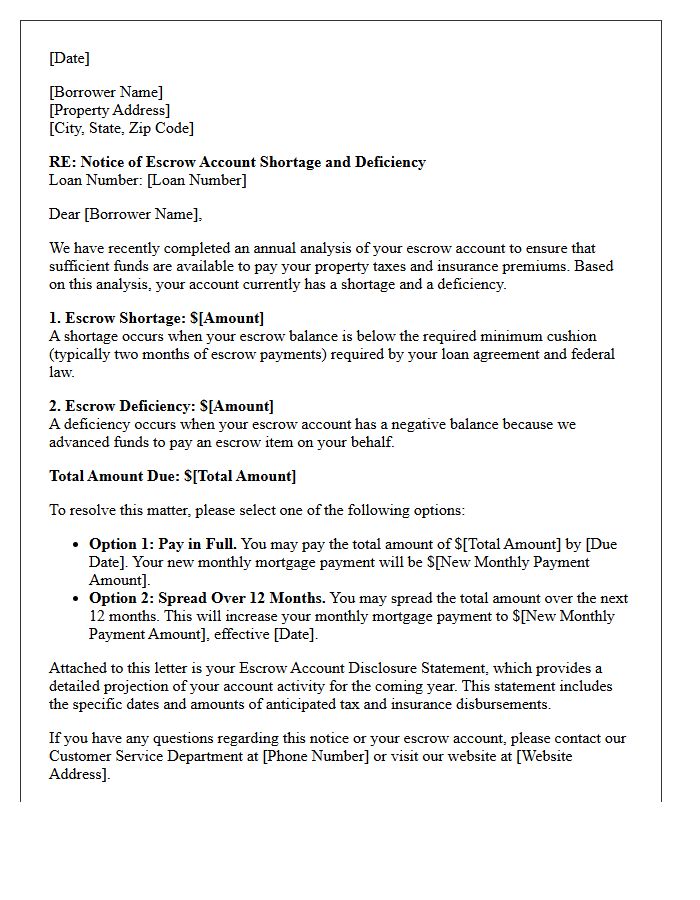

Escrow Cushion Shortage and Deficiency Disclosure Letter

An Escrow Cushion Shortage and Deficiency Disclosure Letter informs homeowners that their account lacks sufficient funds to cover rising property taxes or insurance. A shortage occurs when the balance falls below the required minimum cushion, while a deficiency happens when the account is negative. Lenders issue these notices after an annual escrow analysis to adjust monthly mortgage payments. To resolve these gaps, borrowers typically choose between making a one-time lump-sum payment or spreading the increased costs over the following year to maintain a healthy escrow balance.

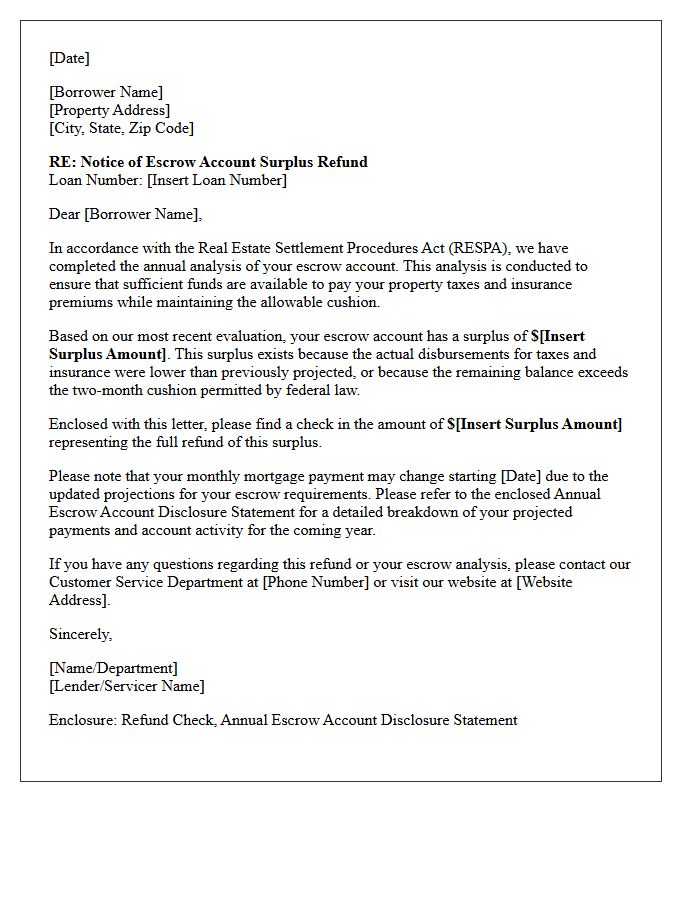

RESPA Escrow Cushion Surplus Refund Letter

A RESPA Escrow Cushion Surplus Refund Letter informs homeowners of an excess balance discovered during an annual escrow analysis. Under federal RESPA guidelines, lenders are prohibited from holding more than a two-month "cushion" of estimated tax and insurance payments. If your account exceeds this limit by fifty dollars or more, the servicer must issue a surplus refund within thirty days. Receiving this letter typically indicates that your property taxes or insurance premiums decreased, resulting in a mandatory reimbursement of your overpaid funds.

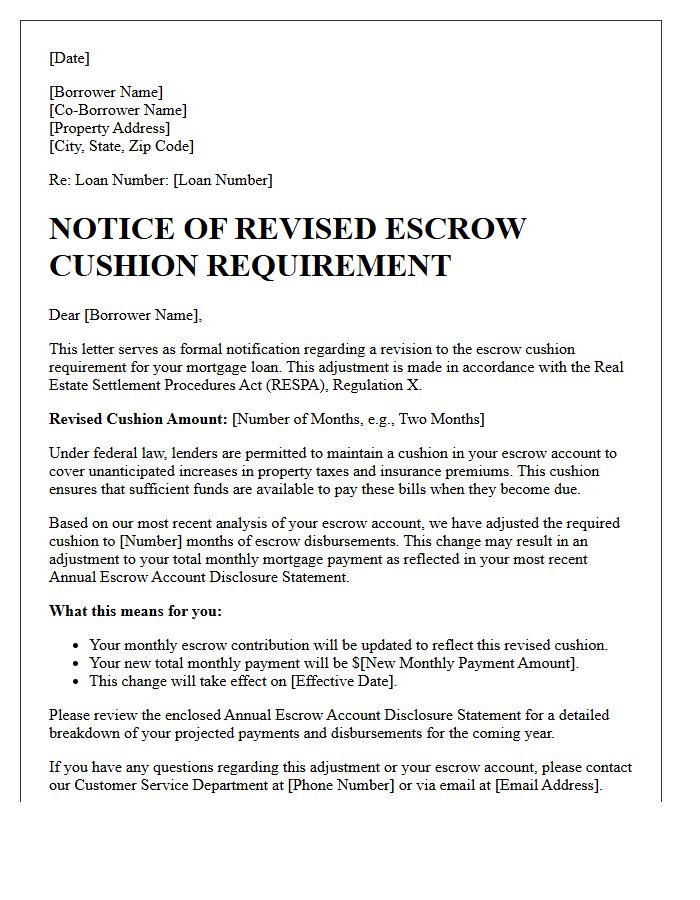

Revised RESPA Escrow Cushion Disclosure Letter

The Revised RESPA Escrow Cushion Disclosure Letter is a critical notification informing borrowers about changes in their mortgage impound accounts. Under Regulation X, lenders may maintain a cushion limited to one-sixth of the total annual disbursements to prevent account deficiencies. This revised letter details adjusted monthly payments based on updated tax and insurance projections. Homeowners must review these disclosures to understand how escrow analysis impacts their total housing costs and ensures compliance with federal consumer protection laws regarding surplus or shortage resolutions.

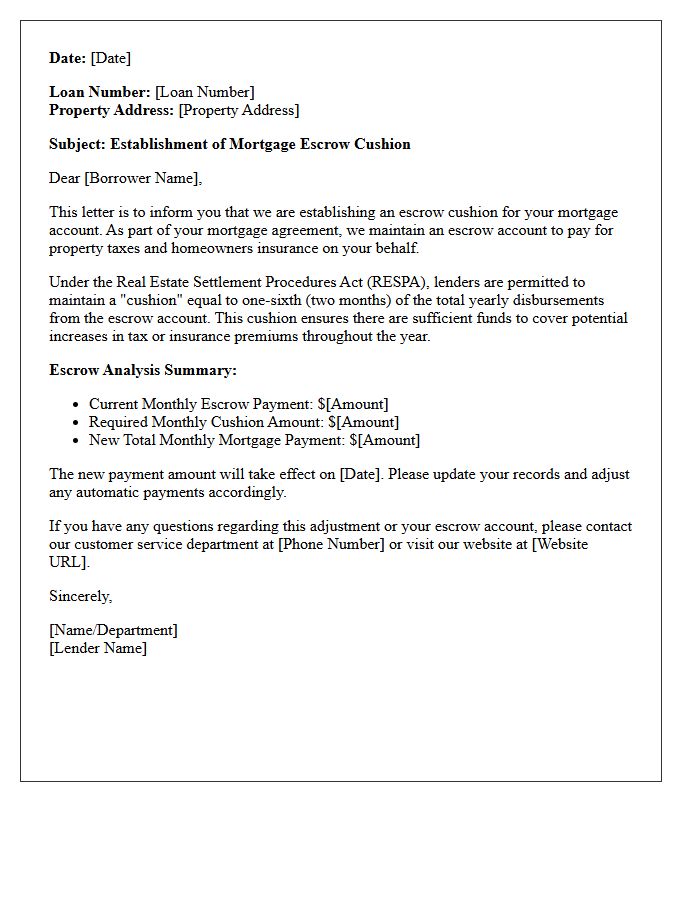

New Mortgage Escrow Cushion Establishment Letter

A New Mortgage Escrow Cushion Establishment Letter notifies homeowners of a required reserve fund maintained by lenders to prevent account shortages. This escrow cushion typically covers up to two months of projected property taxes and insurance premiums. It serves as a financial safety net against rising costs, ensuring timely payments even if tax rates fluctuate. Understanding this document is vital because it explains potential monthly payment adjustments and the initial funding needed at closing to stabilize your impound account throughout the year.

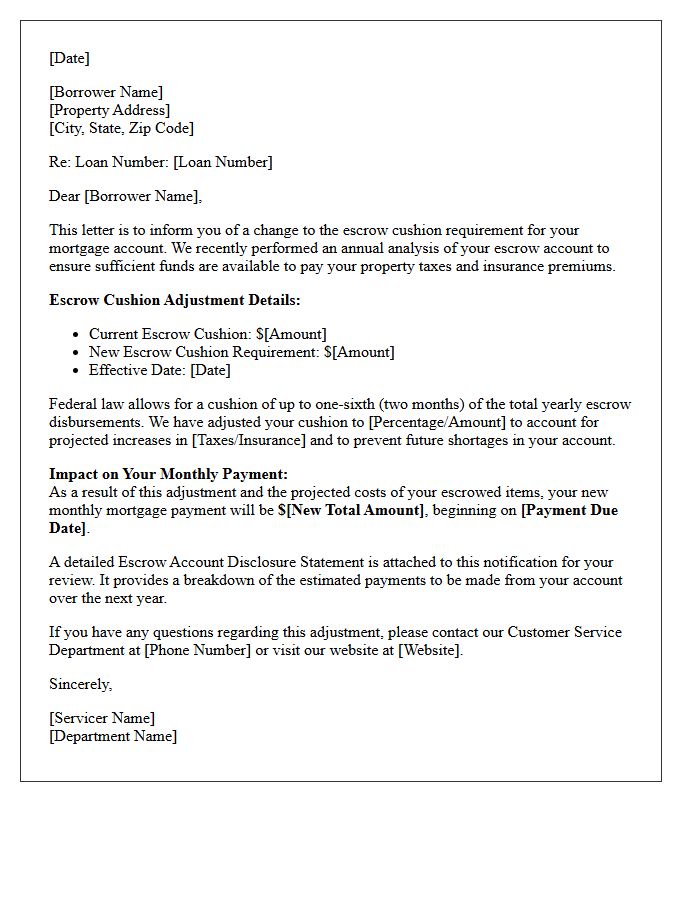

Escrow Cushion Adjustment Notification Letter

An Escrow Cushion Adjustment Notification Letter informs homeowners about changes to their monthly mortgage payments due to fluctuations in property taxes or insurance premiums. Federal law allows lenders to maintain a contingency reserve, typically equal to two months of escrow payments, to cover unexpected cost increases. This notice details whether you have a surplus to be refunded or a shortage requiring a higher monthly contribution. Reviewing this document is essential for maintaining accurate financial planning and ensuring your escrow account remains fully funded to prevent potential payment defaults or future spikes.

RESPA Compliant Escrow Cushion Summary Letter

A RESPA Compliant Escrow Cushion Summary Letter provides a clear breakdown of your mortgage impound account to ensure transparency. Under federal law, lenders are permitted to maintain a cushion equivalent to two months of estimated annual disbursements. This document verifies that your escrow reserves do not exceed legal limits, helping to prevent excessive overages. Reviewing this summary is essential for understanding your monthly payment adjustments and ensuring your servicer adheres to Regulation X guidelines regarding the management of property taxes and insurance funds.

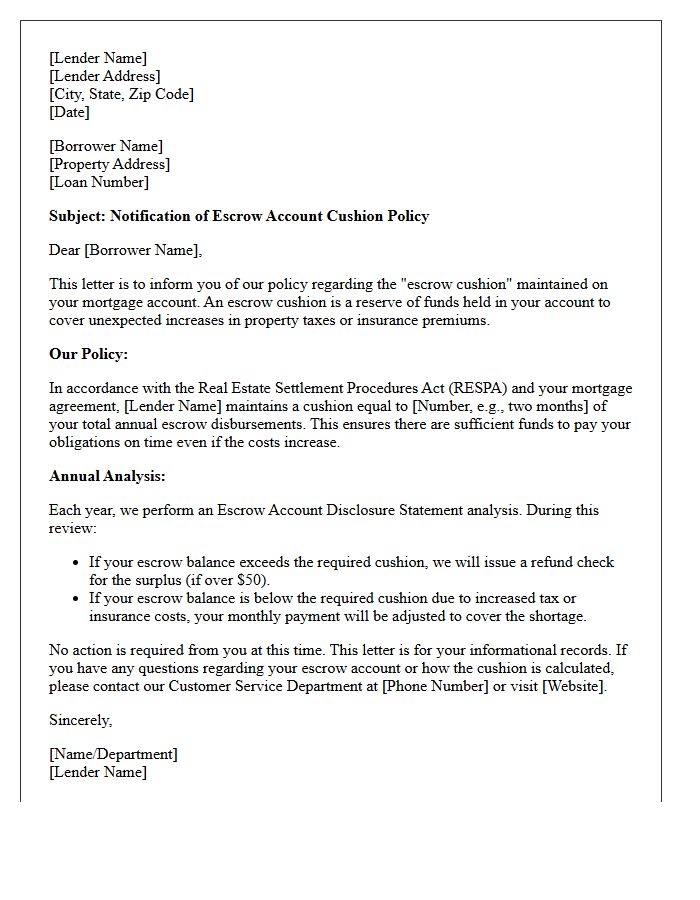

Mortgage Lender Escrow Cushion Policy Letter

A mortgage lender escrow cushion policy letter explains the reserve requirement maintained in your impound account. Federal law under RESPA allows lenders to hold a cushion of up to two months of estimated taxes and insurance payments. This financial buffer protects the servicer against cost increases or late disbursements. Reviewing this letter is essential for understanding your monthly payment adjustments and ensuring your escrow analysis reflects accurate tax assessments, preventing unexpected shortages or surplus refunds during the annual review process.

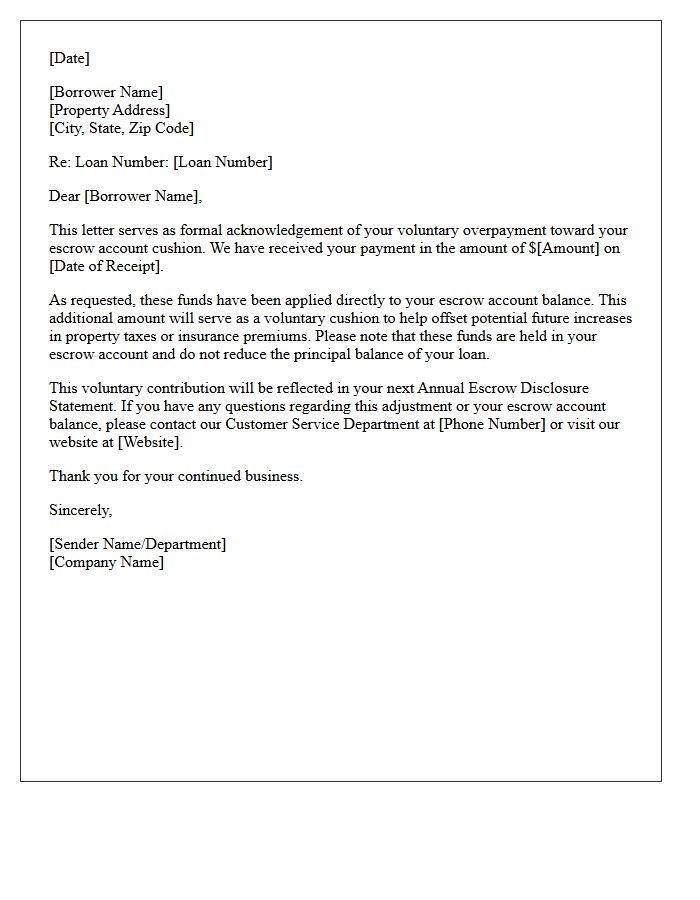

Escrow Cushion Voluntary Overpayment Acknowledgement Letter

The Escrow Cushion Voluntary Overpayment Acknowledgement Letter is a formal document confirming a homeowner's decision to maintain a higher reserve balance in their mortgage account. By signing, you authorize the lender to keep extra funds beyond the legal minimum to prevent future payment spikes or escrow shortages. This voluntary buffer acts as a financial safeguard against rising property taxes or insurance premiums. It ensures monthly stability but requires your written consent, as these surplus funds would otherwise be refunded to you during the annual analysis period.

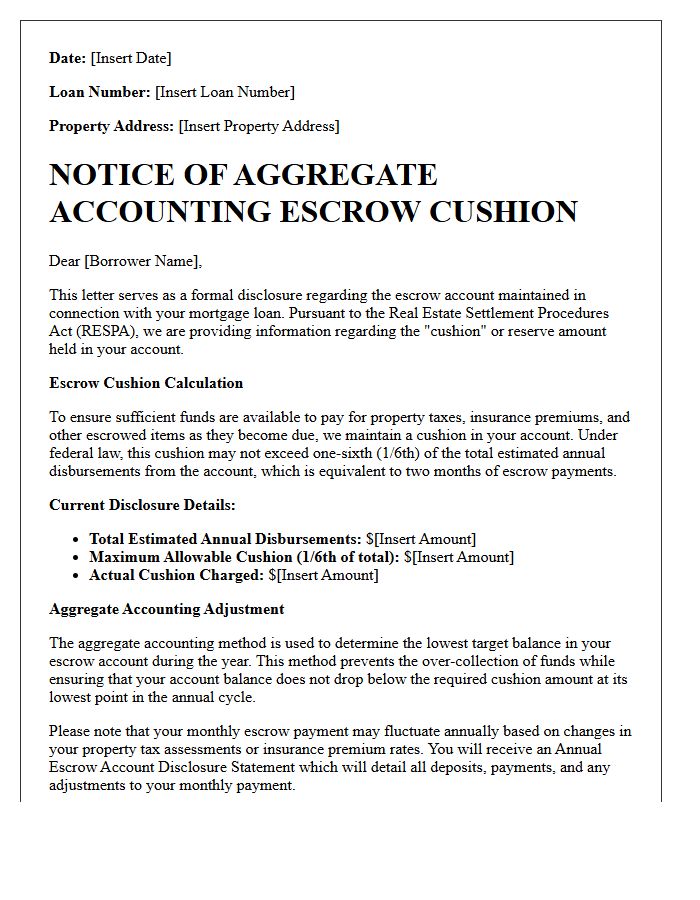

Aggregate Accounting Escrow Cushion Disclosure Letter

The Aggregate Accounting Escrow Cushion Disclosure Letter is a mandatory document that explains how lenders calculate reserve funds for taxes and insurance. This notice ensures transparency by detailing the escrow cushion, which is the extra amount held to prevent account shortages. Under federal law, this cushion cannot exceed two months of estimated annual disbursements. Understanding this statement helps homeowners verify that their monthly mortgage payments are accurate and that the lender is not overfunding the account beyond legal limits. Reviewing this disclosure is essential for effective personal financial management.

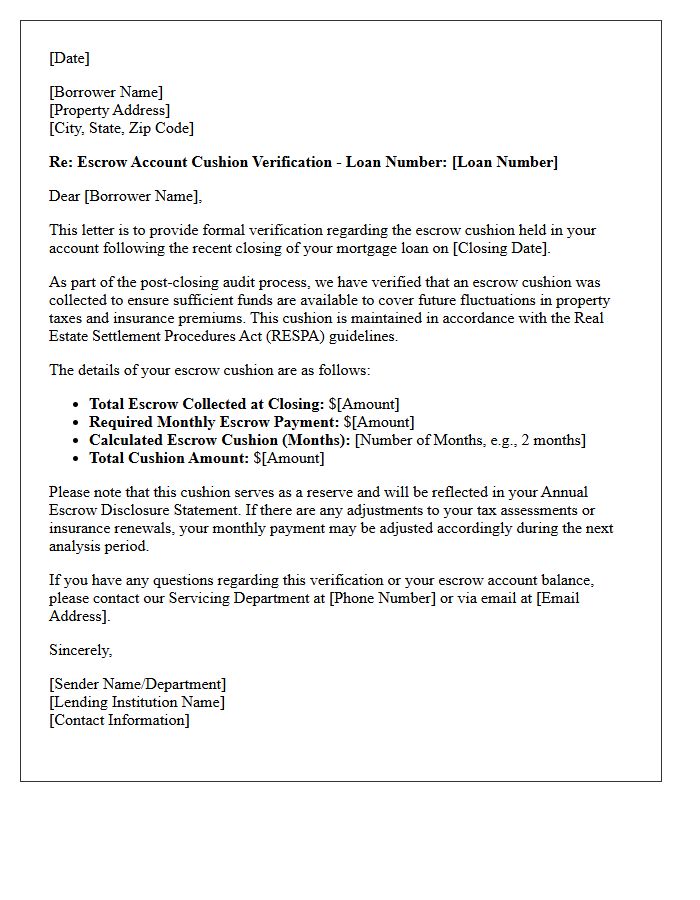

Post Closing Escrow Cushion Verification Letter

A Post Closing Escrow Cushion Verification Letter is a critical document used to confirm that mortgage escrow accounts maintain a legal reserve. After a home sale, lenders perform an analysis to ensure sufficient funds exist for property taxes and insurance premiums. This letter verifies that the cushion amount complies with RESPA guidelines, typically preventing more than two months of prepayments. Borrowers should review this to identify potential escrow shortages or to claim a refund check if the account holds excess surplus funds after the final closing adjustment.

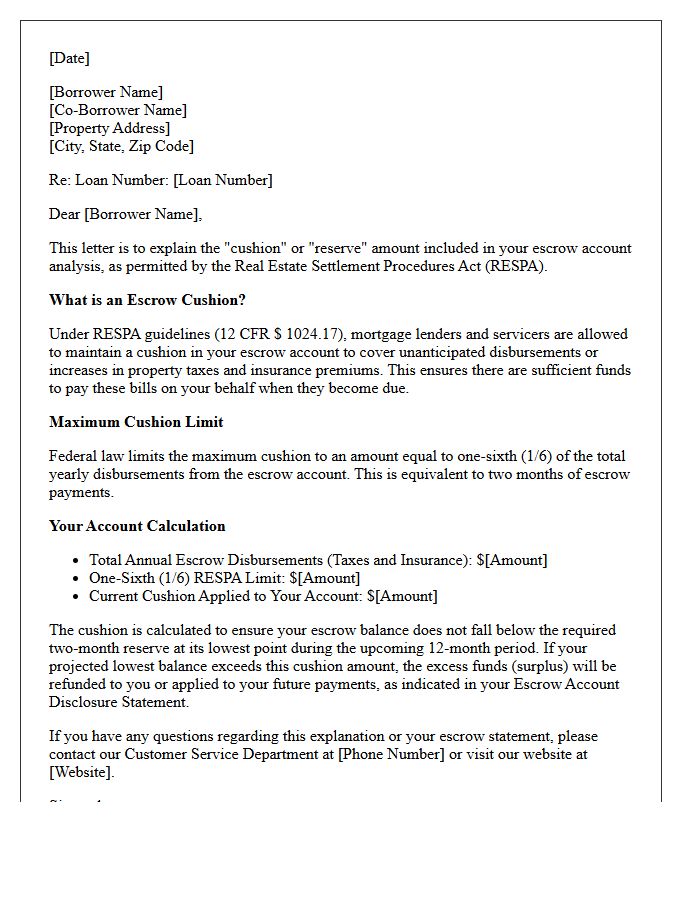

RESPA Escrow Cushion Limit Explanation Letter

A RESPA Escrow Cushion Limit Explanation Letter informs borrowers that lenders may maintain a reserve to cover unforeseen tax or insurance increases. Under federal law, this escrow cushion is strictly limited to one-sixth of the total annual estimated disbursements, equivalent to two months of payments. This document ensures transparency during annual escrow analysis, explaining how the surplus or shortage was calculated. Understanding these limits protects homeowners from excessive overfunding while ensuring the lender has sufficient liquid funds to pay critical property obligations on time.

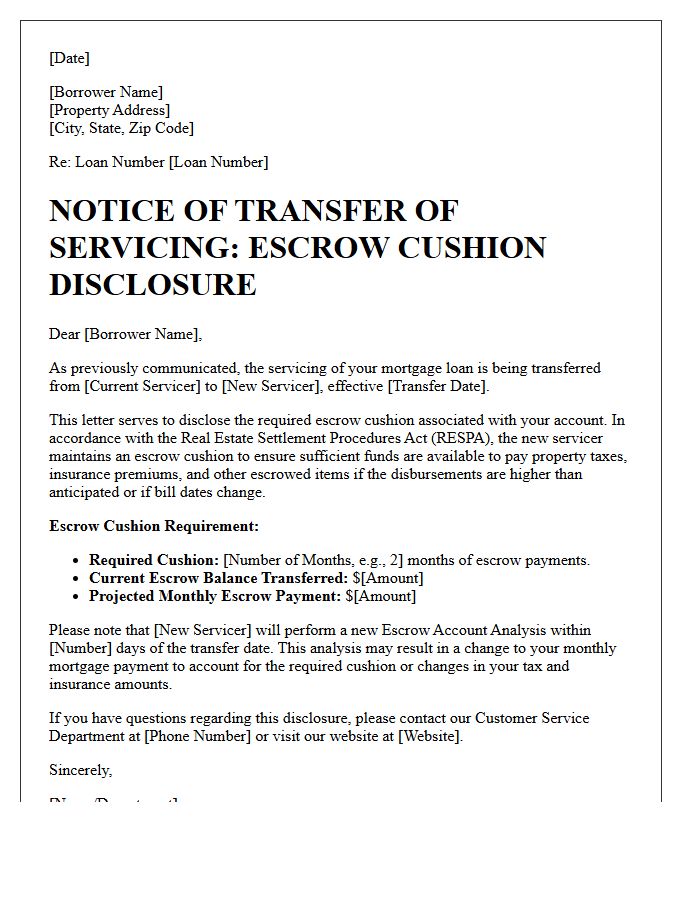

Transfer of Servicing Escrow Cushion Disclosure Letter

A Transfer of Servicing Escrow Cushion Disclosure Letter informs homeowners when their mortgage lender changes. This document specifies the minimum balance required in your escrow account to cover property taxes and insurance premiums. It ensures a financial buffer, or cushion, is maintained during the transition to the new servicer. Reviewing this letter is essential to understand potential changes in your monthly mortgage payments and to verify that your funds were transferred accurately without causing an unexpected escrow shortage.

What is a RESPA Escrow Cushion and why is it required?

A RESPA escrow cushion is a reserve of funds, equal to a maximum of two months of estimated annual disbursements, that lenders are permitted to hold in your escrow account. Under the Real Estate Settlement Procedures Act (RESPA), this cushion protects the lender against unexpected increases in property taxes or insurance premiums, ensuring there are sufficient funds to cover these obligations.

What is a RESPA Escrow Cushion Disclosure Letter?

The RESPA Escrow Cushion Disclosure Letter is a formal document provided by mortgage servicers that outlines how your escrow account is managed. It details the specific amount being held as a reserve, explains the federal guidelines governing the two-month cushion limit, and provides a breakdown of how your monthly escrow payments are calculated based on projected expenses.

How is the maximum allowable escrow cushion calculated?

Under Section 10 of RESPA, the maximum allowable cushion is one-sixth (1/6th) of the total anticipated annual disbursements from the escrow account. This equates to two months of escrow payments. If your annual tax and insurance total is $3,600, your maximum allowable cushion would be $600 ($300 per month x 2).

What happens if my escrow cushion exceeds the RESPA limit?

If a required annual escrow analysis reveals that your account balance exceeds the 1/6th cushion limit by $50 or more, the lender is legally obligated to issue an escrow refund (surplus) to the borrower. This surplus must be returned within 30 days of the analysis, provided the mortgage is current at the time of the review.

Why did my monthly payment change according to my Escrow Disclosure?

Your monthly payment may change if there is a shift in your property tax assessment or insurance premiums, or if the escrow analysis identifies a "shortage" or "deficiency." If your account falls below the required two-month cushion, the disclosure letter will outline a repayment plan to restore the cushion to the maximum level permitted by RESPA.

Comments