A Notice of Forbearance Plan Approval confirms that your mortgage lender has granted a temporary pause or reduction in monthly payments. This formal document outlines the specific duration of the assistance and the repayment terms required once the period ends. Reviewing these details ensures financial stability during hardships. To help you communicate effectively with your servicer, below are some ready to use template.

Image cover: Official Approval Templates for Your Mortgage Forbearance Plan

Letter Samples List

- Date of Official Letter

- Mortgage Lender Contact Information

- Borrower Name and Property Address

- Mortgage Loan Account Reference Number

- Notice of Forbearance Plan Approval

- Effective Dates of the Forbearance Period

- Approved Temporary Monthly Payment Amount

- Treatment of Taxes and Escrow Accounts

- Accrual of Deferred Mortgage Interest

- Post-Forbearance Repayment Plan Options

- Credit Bureau Reporting Disclosure

- Borrower Acknowledgment and Signature Line

- Authorized Mortgage Lender Representative

Date of Official Letter

The Date of Official Letter is the most critical element for establishing legal validity and chronological record-keeping. It typically appears at the top right or left, indicating exactly when the document was drafted or issued. This date serves as the official reference point for deadlines, contractual obligations, and archival filing. Ensuring the date is accurate is essential for professional accountability and tracking the timeline of formal correspondence between parties.

Mortgage Lender Contact Information

Keeping your mortgage lender contact information readily accessible is essential for successful homeownership. This data typically includes your servicer's phone number, email address, and official mailing address for payments. You must verify these details through your monthly billing statement to avoid sophisticated phishing scams. Having direct access allows you to discuss payment options, update insurance records, or request payoff statements efficiently. Always ensure you are communicating with an authorized representative to protect your financial security and maintain your loan account accurately.

Borrower Name and Property Address

Accurate Borrower Name and Property Address details are essential for legal validity in real estate contracts. The name must match official government identification to ensure enforceable ownership rights and precise credit reporting. Simultaneously, the address serves as the legal situs, uniquely identifying the collateral for the mortgage. Any discrepancies in these identifiers can lead to significant processing delays, title insurance issues, or potential loan rejection. Verifying these core elements early maintains the integrity of the financial transaction and secures the legal record.

Mortgage Loan Account Reference Number

A Mortgage Loan Account Reference Number is a unique identifier assigned by your lender to track your specific debt obligation. This alphanumeric code is essential for making payments, setting up online banking, and verifying your identity during customer service inquiries. It distinguishes your loan from others and must be included in all official correspondence. Keeping this number secure and accessible ensures accurate financial reporting and helps prevent processing errors during your mortgage repayment journey.

Notice of Forbearance Plan Approval

A Notice of Forbearance Plan Approval is a formal agreement where your mortgage lender grants a temporary pause or reduction in monthly payments due to financial hardship. It is crucial to understand that this is not debt forgiveness; the deferred amount must be repaid later. Review the specific repayment options, such as a deferral or loan modification, to avoid future default. Keep this document for your records, as it outlines the effective dates and your obligations to maintain the property during the forbearance period.

Effective Dates of the Forbearance Period

The effective date of a forbearance period marks the official commencement of temporary payment relief. Borrowers must confirm the start date specified in their formal agreement to ensure protection against late fees and credit reporting penalties. This timeline dictates when scheduled installments are paused or reduced, and it typically concludes on a predetermined expiration date unless an extension is granted. Understanding these precise dates is essential for managing mortgage obligations and coordinating with loan servicers to avoid unintentional defaults during the adjusted repayment window.

Approved Temporary Monthly Payment Amount

The Approved Temporary Monthly Payment Amount is a short-term, reduced billing figure granted by lenders during financial hardship. This adjustment allows borrowers to maintain account standing while seeking a permanent loan modification. It is critical to understand that this amount is often a trial period payment rather than a final agreement. Consistent on-time payments during this phase are essential to demonstrate eligibility for long-term debt restructuring or forbearance relief, helping to prevent potential foreclosure or default proceedings while your financial situation stabilizes.

Treatment of Taxes and Escrow Accounts

When managing a mortgage, the escrow account acts as a dedicated holding area for property-related expenses. Lenders typically collect monthly payments to cover property taxes and homeowners insurance, ensuring these critical bills are paid on time. An annual escrow analysis is performed to adjust for tax fluctuations or insurance premium changes. If your account has a deficit, your monthly payment may increase to recover the shortage. Proper management prevents tax liens and ensures continuous insurance coverage, protecting both the homeowner's equity and the lender's collateral interest.

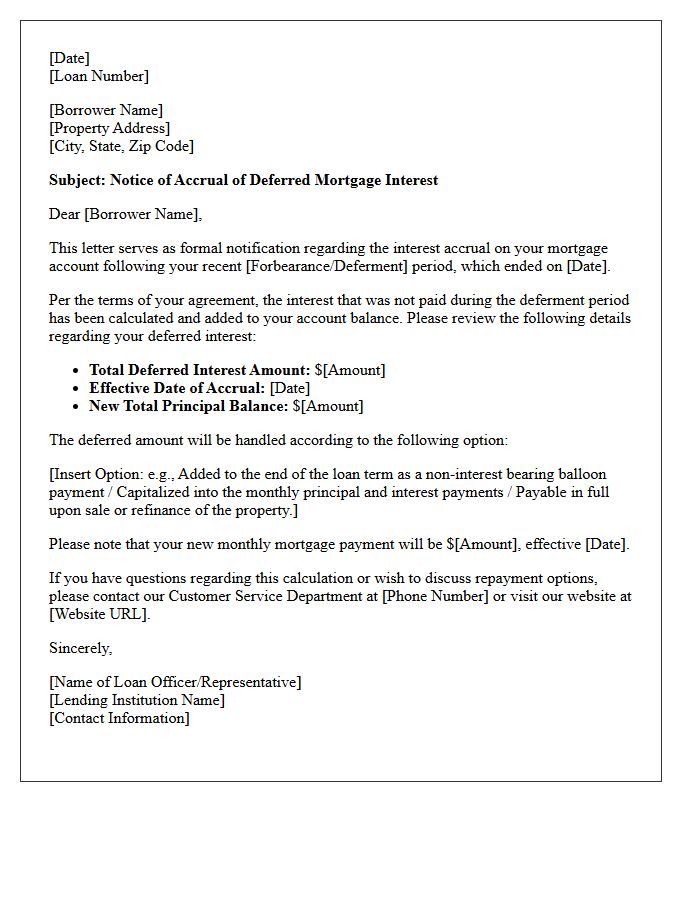

Accrual of Deferred Mortgage Interest

Accrual of deferred mortgage interest occurs when the monthly payment does not cover the full interest due. This unpaid amount is added to the principal balance, leading to negative amortization. Over time, this increases the total debt owed, meaning you may eventually owe more than the original loan amount. It is essential to monitor these balances closely, as compounding interest on a growing principal can significantly escalate long-term borrowing costs and reduce home equity.

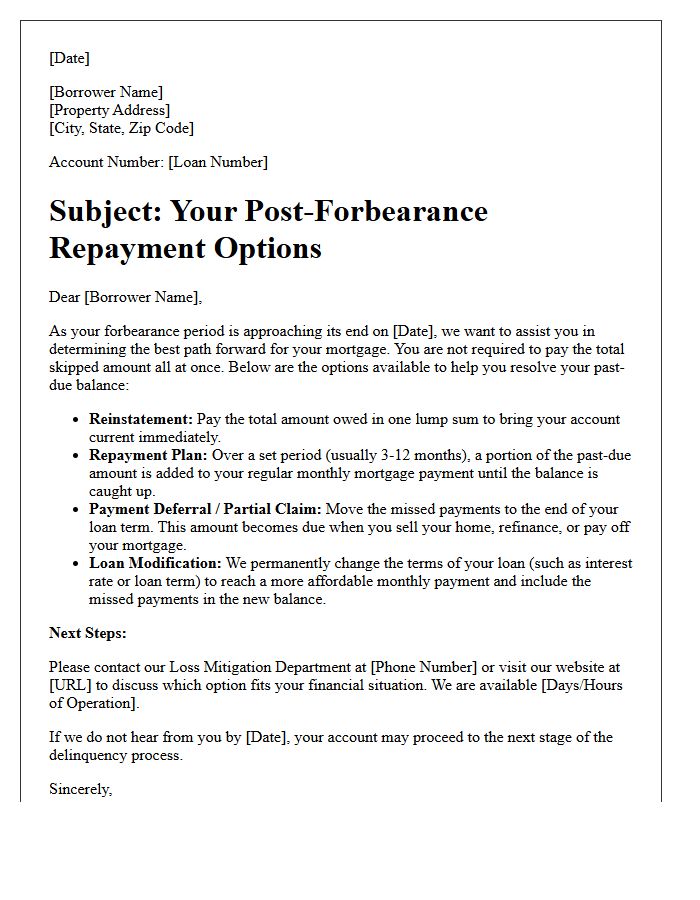

Post-Forbearance Repayment Plan Options

When exiting a pandemic-related pause, understanding Post-Forbearance Repayment Plan Options is crucial for financial stability. Borrowers typically choose between a reinstatement, which requires a lump-sum payment, or a repayment plan that spreads missed amounts over several months alongside regular installments. Alternatively, a deferral or partial claim moves arrears to the end of the loan term. For those facing long-term hardship, a loan modification may permanently adjust interest rates or terms to ensure monthly payments remain affordable. Always contact your loan servicer early to evaluate eligibility and avoid foreclosure.

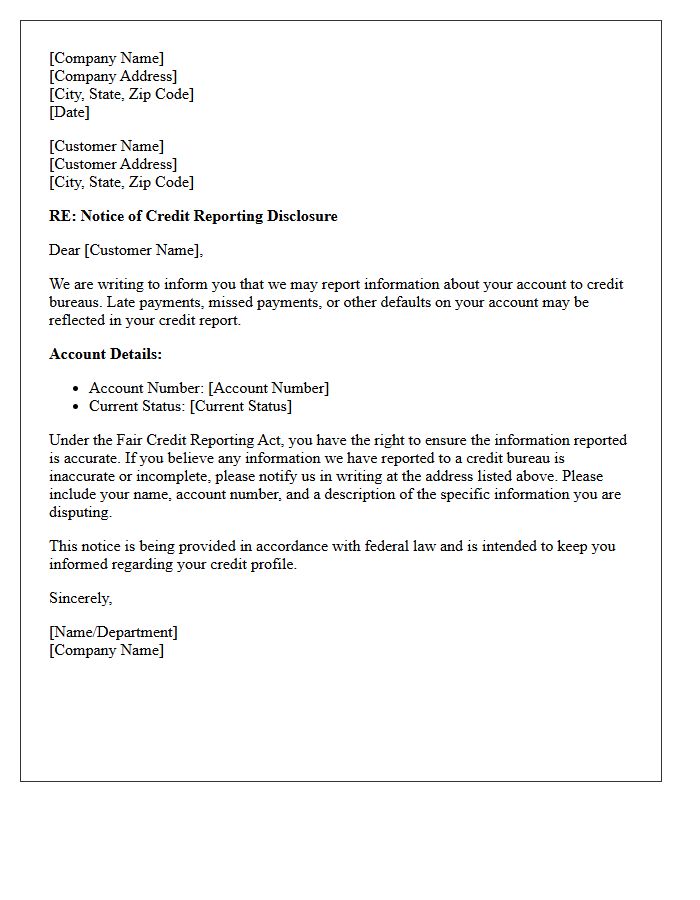

Credit Bureau Reporting Disclosure

A Credit Bureau Reporting Disclosure is a legal notification informing consumers that their payment history and financial behavior will be reported to national credit agencies. This document ensures transparency by explaining how data impacts your credit score. It is essential to review these disclosures to understand your rights regarding dispute resolution and accuracy. Lenders must provide this notice before sharing negative information, allowing you to maintain credit health and monitor for potential errors or identity theft within your official financial records.

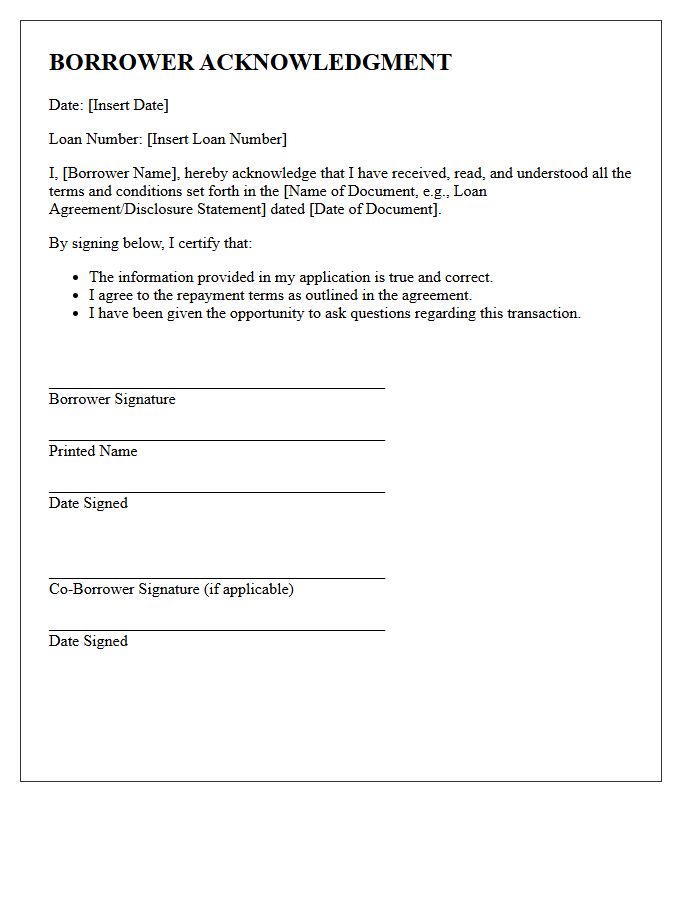

Borrower Acknowledgment and Signature Line

The Borrower Acknowledgment and Signature Line is a critical legal element in loan documentation. By signing, the borrower confirms they have read, understood, and accepted all contractual terms and disclosure requirements. This signature transforms the document into a legally binding agreement, affirming the accuracy of the provided information. It serves as formal consent to the repayment schedule and interest rates. Always ensure all blanks are filled before signing, as this line represents your legal commitment to the financial obligations outlined in the credit agreement.

Authorized Mortgage Lender Representative

An Authorized Mortgage Lender Representative is a licensed professional qualified to facilitate home financing on behalf of a financial institution. Their primary role is to evaluate borrower eligibility, manage loan applications, and ensure compliance with federal lending regulations. Understanding their credentials is crucial because they act as the direct link between homebuyers and capital providers. They provide essential guidance on interest rates, loan structures, and closing requirements, helping clients navigate the complexities of debt obligations while protecting the lender's financial interests throughout the mortgage origination process.

What is a Notice of Forbearance Plan Approval?

A Notice of Forbearance Plan Approval is an official document from your mortgage servicer confirming that your request to temporarily suspend or reduce your monthly mortgage payments has been accepted due to financial hardship.

How long does a typical mortgage forbearance plan last?

The duration of a forbearance plan varies depending on your loan type and specific situation, but they are typically approved in increments of 3 to 6 months, with the possibility of an extension if the hardship persists.

Do I still have to pay back the missed payments after the forbearance period ends?

Yes, forbearance is not debt forgiveness. All skipped or reduced payments must be repaid. You will work with your servicer to determine a repayment option, such as a repayment plan, payment deferral, or loan modification.

Will being on a forbearance plan negatively impact my credit score?

Under most federal guidelines and the CARES Act, if you were current before the forbearance, your servicer must continue to report you as current. However, the account may be noted as "active forbearance" on your credit report.

What should I do if my financial hardship continues after the initial plan expires?

If you are nearing the end of your approved period and cannot resume payments, you must contact your mortgage servicer immediately to request an extension or discuss long-term loss mitigation options to avoid foreclosure.

Comments