An Imminent Default Loss Mitigation Letter is a formal request sent to lenders by homeowners facing unavoidable financial hardship. This proactive communication outlines your situation to seek alternatives like loan modification or forbearance before a payment is missed. Acting early can help preserve your credit and prevent foreclosure. To help you draft a professional request, below are some ready to use template.

Image cover: Proactive Mortgage Relief: Imminent Default Loss Mitigation Letter Templates

Letter Samples List

- Imminent Default Hardship Evaluation Letter

- Loss Mitigation Options Notification Letter

- Mortgage Assistance Application Request Letter

- Trial Period Plan Offer Letter

- Forbearance Agreement Approval Letter

- Repayment Plan Terms Notification Letter

- Payment Deferral Option Offer Letter

- Short Sale Intent to Proceed Letter

- Deed in Lieu Eligibility Notice Letter

- Loss Mitigation Missing Documents Letter

- Home Retention Assistance Approval Letter

- Imminent Default Modification Agreement Letter

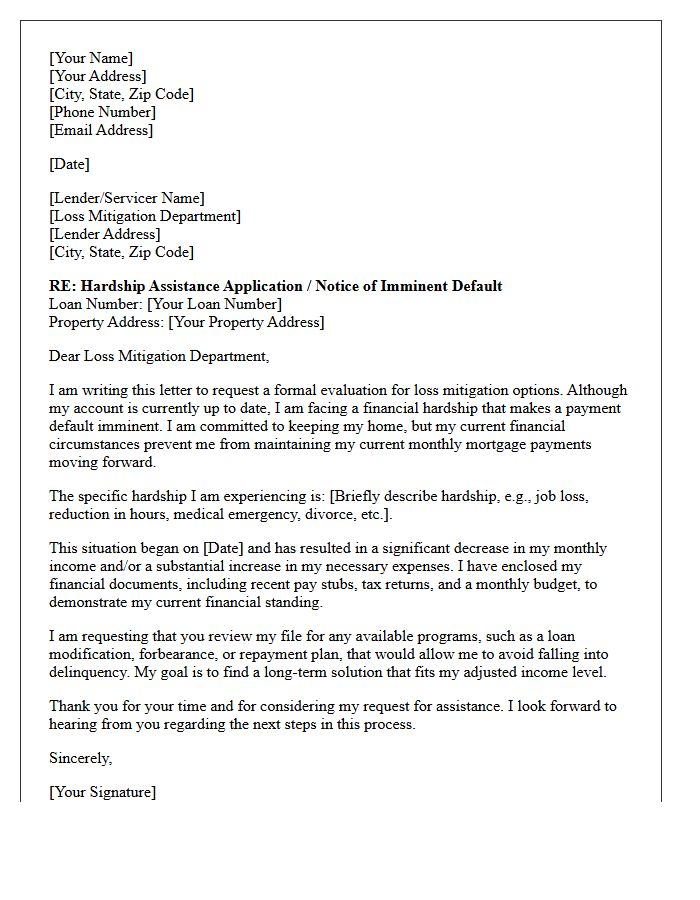

Imminent Default Hardship Evaluation Letter

An Imminent Default Hardship Evaluation Letter is a formal document used by homeowners to prove financial distress before missing a mortgage payment. It serves as a proactive request for loss mitigation options, such as loan modification or forbearance. To be effective, the letter must clearly document qualifying circumstances like job loss, illness, or divorce. Providing detailed financial evidence helps lenders assess your eligibility for assistance programs, potentially preventing foreclosure and protecting your credit score before a formal default occurs.

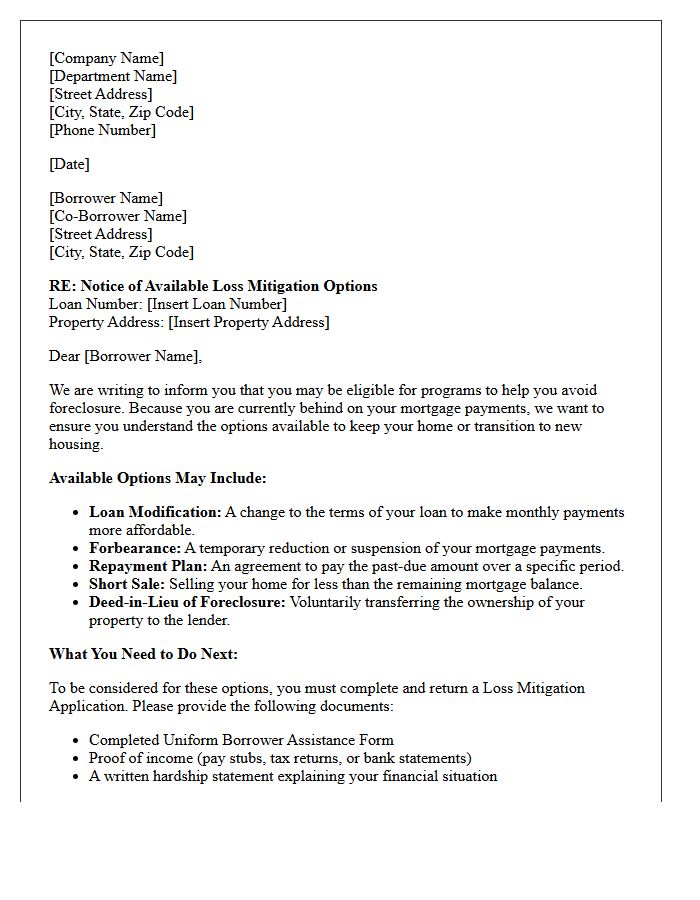

Loss Mitigation Options Notification Letter

A Loss Mitigation Options Notification Letter is a formal document sent by mortgage servicers to borrowers facing financial hardship. It outlines available foreclosure alternatives, such as loan modifications, short sales, or repayment plans. This notice is a critical step in the home retention process, providing specific deadlines and required documentation to evaluate your eligibility for relief. Reviewing this letter promptly is essential to understand your legal rights and prevent property loss through proactive communication with your lender.

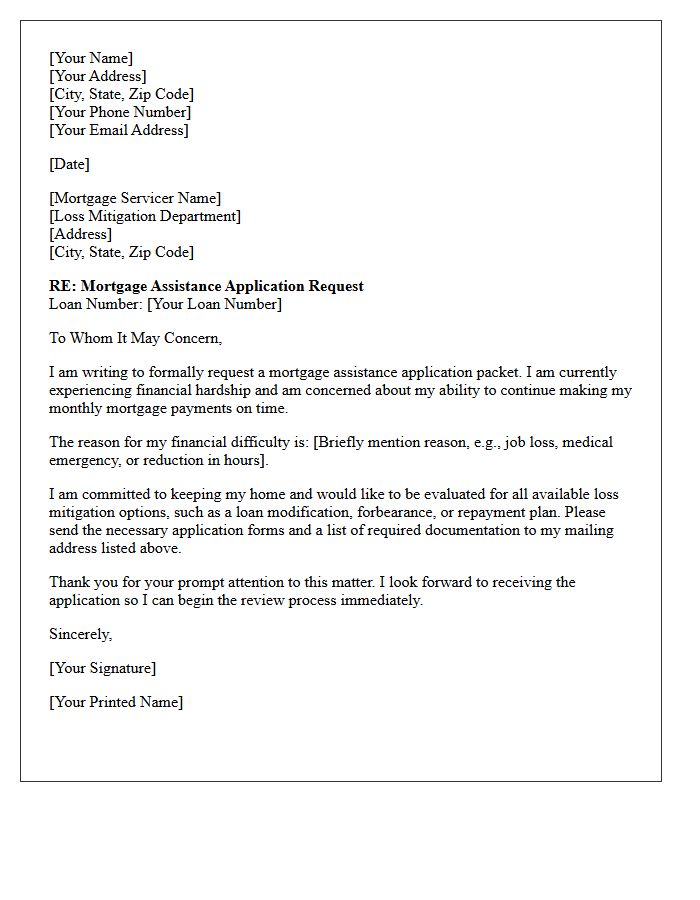

Mortgage Assistance Application Request Letter

A Mortgage Assistance Application Request Letter is a formal document sent to your loan servicer to initiate a hardship review. It serves as an official request for loss mitigation options like loan modification or forbearance. The letter should clearly explain your financial setbacks, such as job loss or medical emergencies, while demonstrating your intent to resolve delinquency. Providing concise details and supporting documentation is essential for a successful evaluation. This letter is the critical first step in protecting your home from foreclosure and establishing a sustainable repayment plan with your lender.

Trial Period Plan Offer Letter

A Trial Period Plan Offer Letter is a formal document outlining the terms of a temporary employment or mortgage modification phase. It specifies the duration of the trial, performance expectations, and compensation details. This legal agreement serves as a preliminary step before permanent status is granted. Candidates must review the eligibility criteria and deadlines carefully, as successful completion is mandatory for a final contract. Understanding these conditional terms ensures both parties align on goals and responsibilities during this evaluative timeframe.

Forbearance Agreement Approval Letter

A Forbearance Agreement Approval Letter is a formal document from a lender confirming a temporary pause or reduction in mortgage payments. It outlines the specific repayment terms and the duration of the relief period. Crucially, this letter is not a loan waiver; skipped payments are deferred, not forgiven. Borrowers must strictly adhere to the reinstatement plan or modification terms specified to avoid foreclosure. Always verify the effective dates and impact on credit reporting to ensure long-term financial stability while managing temporary hardship.

Repayment Plan Terms Notification Letter

A Repayment Plan Terms Notification Letter is a formal document outlining the specific repayment schedule agreed upon between a lender and borrower. It details critical information such as the installment amounts, due dates, and interest rates applied to the balance. Receiving this letter confirms that your request for a structured payment strategy has been approved. It is essential to review the terms and conditions carefully to ensure compliance and avoid potential default. Keep this record as official verification of your financial commitment and the revised obligations required to settle your outstanding debt effectively.

Payment Deferral Option Offer Letter

A Payment Deferral Option Offer Letter is a formal document from a lender allowing borrowers to postpone monthly installments due to temporary financial hardship. This agreement moves missed payments to the end of the loan term without changing the interest rate. It is legally binding, so you must review the specific terms, duration, and any potential impact on your credit score before signing. Accepting this offer provides immediate liquidity relief while preventing default, ensuring your account remains in good standing during difficult periods.

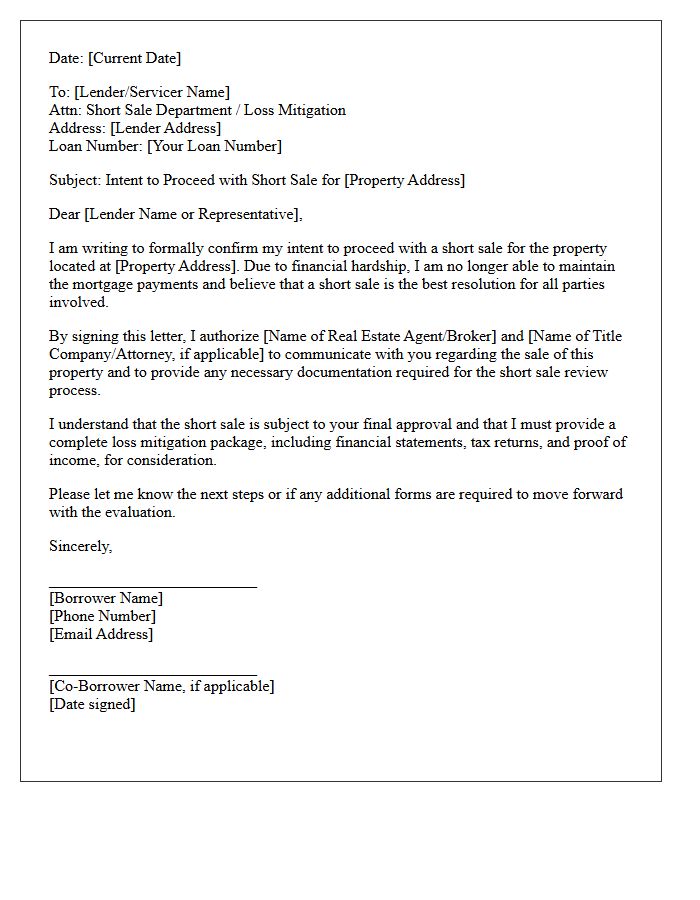

Short Sale Intent to Proceed Letter

A Short Sale Intent to Proceed Letter is a formal document where a homeowner notifies their lender of their voluntary agreement to sell the property for less than the remaining mortgage balance. This letter is crucial for initiating the mitigation process and demonstrates the seller's commitment to avoiding foreclosure. It typically accompanies a financial hardship package, providing the lender with the necessary written consent to evaluate the transaction. Submitting this document promptly ensures the bank begins reviewing the offer, helping to streamline the complex short sale approval timeline.

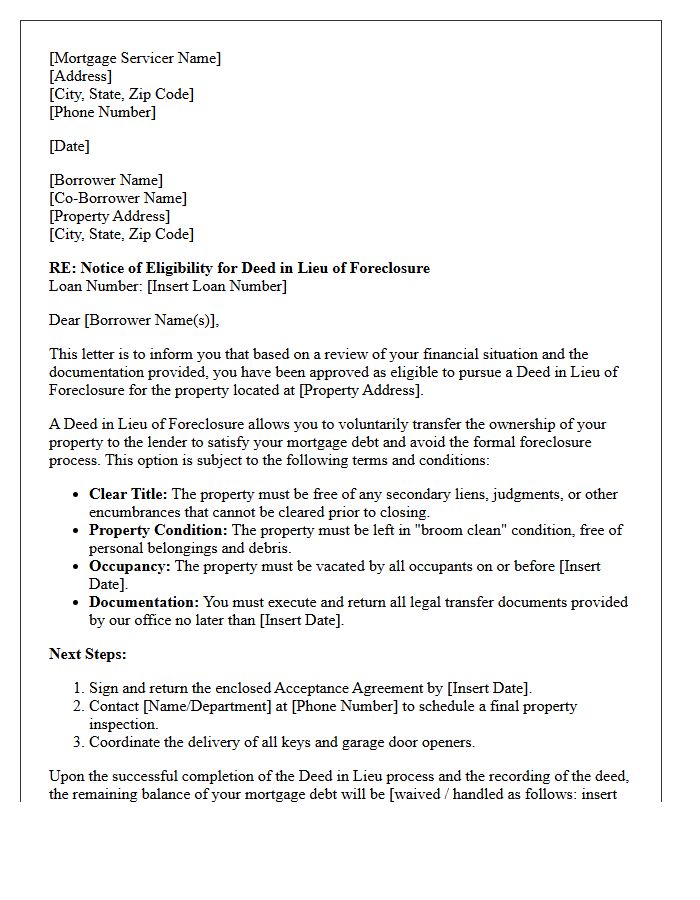

Deed in Lieu Eligibility Notice Letter

A Deed in Lieu Eligibility Notice Letter is a formal notification from a mortgage servicer informing a homeowner that they qualify for a deed in lieu of foreclosure. This document outlines the requirements to voluntarily transfer the property title to the lender to satisfy the debt. It is a critical alternative for borrowers facing financial hardship who cannot sell through a short sale. Receiving this letter indicates that the lender has reviewed your financial eligibility and is willing to bypass the traditional foreclosure process to mitigate losses for both parties.

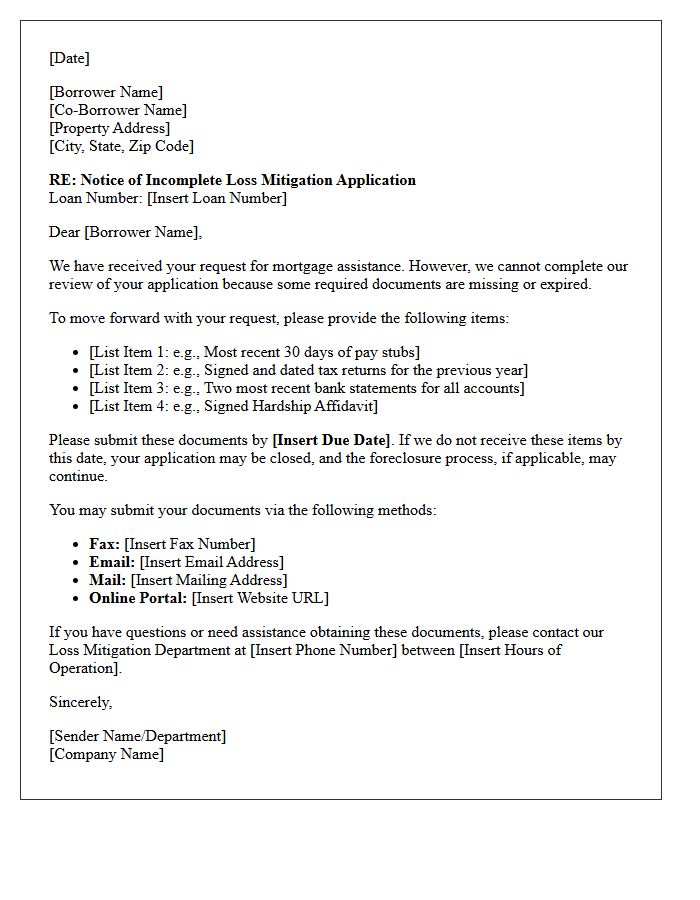

Loss Mitigation Missing Documents Letter

A Loss Mitigation Missing Documents Letter is a formal notice from your mortgage servicer indicating that your application for foreclosure alternatives is incomplete. This critical document lists the specific financial records or forms required to proceed with a loan workout. Failing to provide these items within the strict deadline can lead to an automatic denial of your request. Homeowners must respond promptly and ensure every requested document is legible and current to maintain their legal protections and pause potential foreclosure proceedings during the review period.

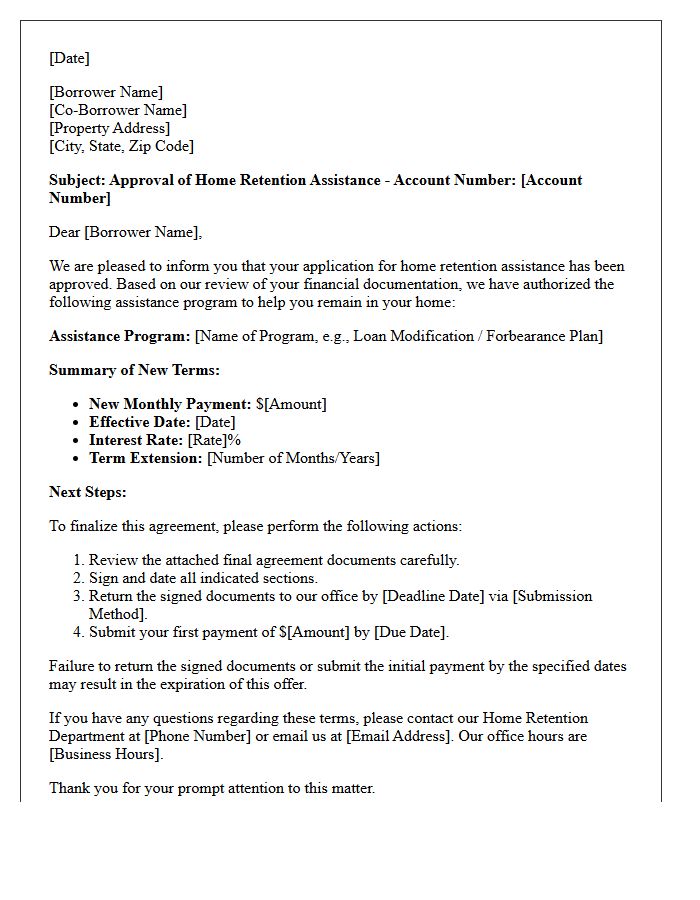

Home Retention Assistance Approval Letter

A Home Retention Assistance Approval Letter is a formal document confirming that your mortgage servicer has authorized a loan modification or repayment plan to prevent foreclosure. This critical notice outlines your new payment terms, adjusted interest rates, and the specific effective date of the agreement. It is essential to review the compliance requirements carefully, as missing a trial payment can void the offer. Retaining this letter is vital for legal protection and serves as official proof that you have successfully secured homeownership stability through an approved loss mitigation program.

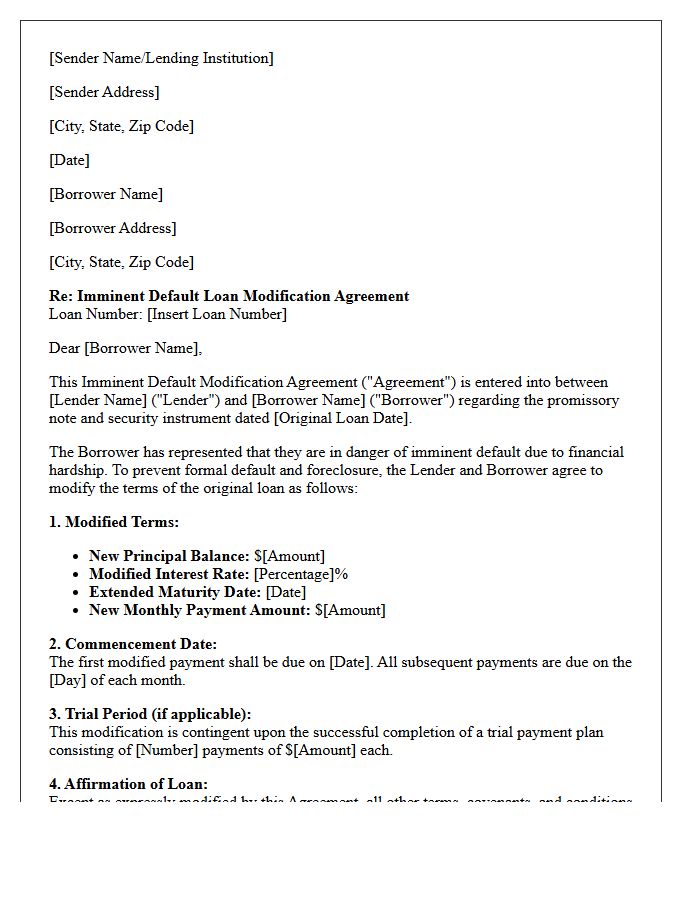

Imminent Default Modification Agreement Letter

An Imminent Default Modification Agreement Letter is a formal document issued when a borrower anticipates missing future payments due to financial hardship. This proactive tool allows lenders to restructure mortgage terms before a formal default occurs. By adjusting interest rates or extending loan durations, the agreement aims to prevent foreclosure and stabilize the borrower's credit. Receiving this letter signifies a critical opportunity to negotiate a permanent loan modification, ensuring the home remains secure while establishing a more manageable repayment schedule tailored to the borrower's current financial capacity.

What is an Imminent Default Loss Mitigation Letter?

An Imminent Default Loss Mitigation Letter is a formal notification sent by a borrower to their mortgage servicer explaining that, while they are currently up to date on payments, financial hardship makes a future default unavoidable. This letter initiates the application process for foreclosure prevention options like loan modifications or short sales.

When should I send an Imminent Default Loss Mitigation Letter?

You should send this letter as soon as you realize a significant financial change-such as job loss, medical emergency, or divorce-will prevent you from making your next mortgage payment. Acting before you actually miss a payment allows you to qualify for "imminent default" status under specific federal and investor guidelines.

What documentation must accompany a loss mitigation request?

To support your letter, you must typically provide a complete loss mitigation package including recent pay stubs, bank statements, tax returns, and a detailed Hardship Affidavit. Providing these documents alongside your letter helps the servicer evaluate your eligibility for programs like the Flex Modification or a Deed-in-Lieu of Foreclosure.

Can I get a loan modification if I am not yet behind on payments?

Yes, many mortgage investors, including Fannie Mae and Freddie Mac, allow for loan modifications due to imminent default. If you can prove that your financial hardship is permanent and that default is certain without assistance, the servicer can restructure your loan terms before your credit score is impacted by missed payments.

How does a servicer determine "Imminent Default" eligibility?

Servicers determine eligibility by evaluating your debt-to-income ratio, total liquid assets, and the nature of your hardship. If your monthly expenses exceed your verifiable income and your savings are insufficient to cover the deficit, the servicer may officially designate your account as being in imminent default, triggering access to loss mitigation workouts.

Comments