A Loss Mitigation Solicitation Letter is a formal outreach sent by mortgage servicers to homeowners facing financial hardship. This crucial document outlines available alternatives to foreclosure, such as loan modifications or short sales, helping borrowers regain financial stability. Understanding how to structure this communication is essential for effective loss recovery. To help you get started, below are some ready to use template.

Image cover: Effective Loss Mitigation Solicitation Letter Samples and Templates

Letter Samples List

- Initial Loss Mitigation Solicitation Letter

- Second Request Loss Mitigation Solicitation Letter

- Final Warning Loss Mitigation Solicitation Letter

- Loan Modification Assistance Solicitation Letter

- Short Sale Option Solicitation Letter

- Deed-In-Lieu Of Foreclosure Solicitation Letter

- Forbearance Plan Solicitation Letter

- Repayment Agreement Solicitation Letter

- Early Intervention Loss Mitigation Letter

- Post-Forbearance Loss Mitigation Solicitation Letter

- Imminent Default Loss Mitigation Solicitation Letter

- Mortgage Hardship Assistance Solicitation Letter

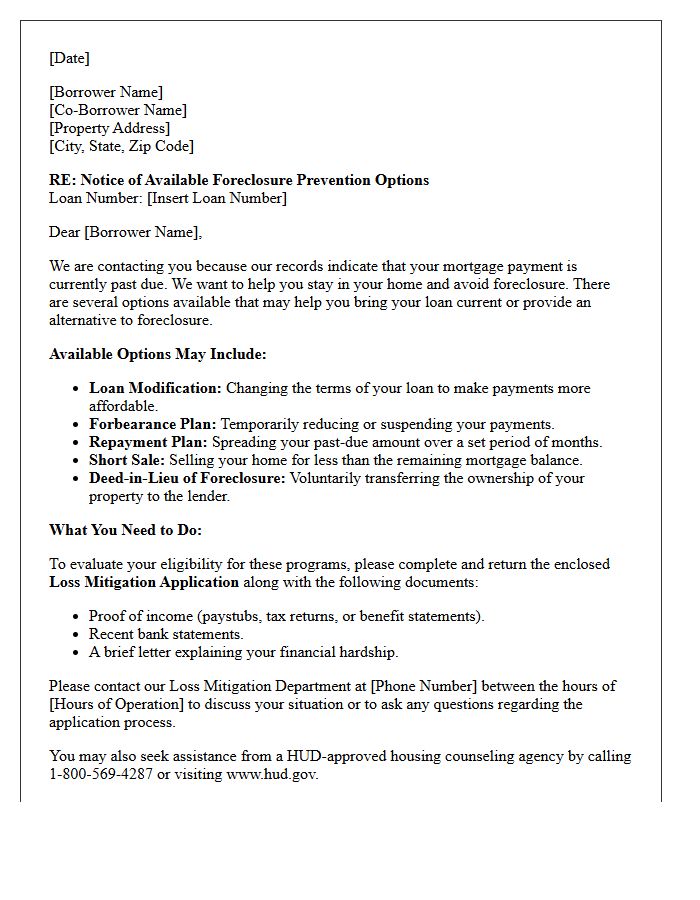

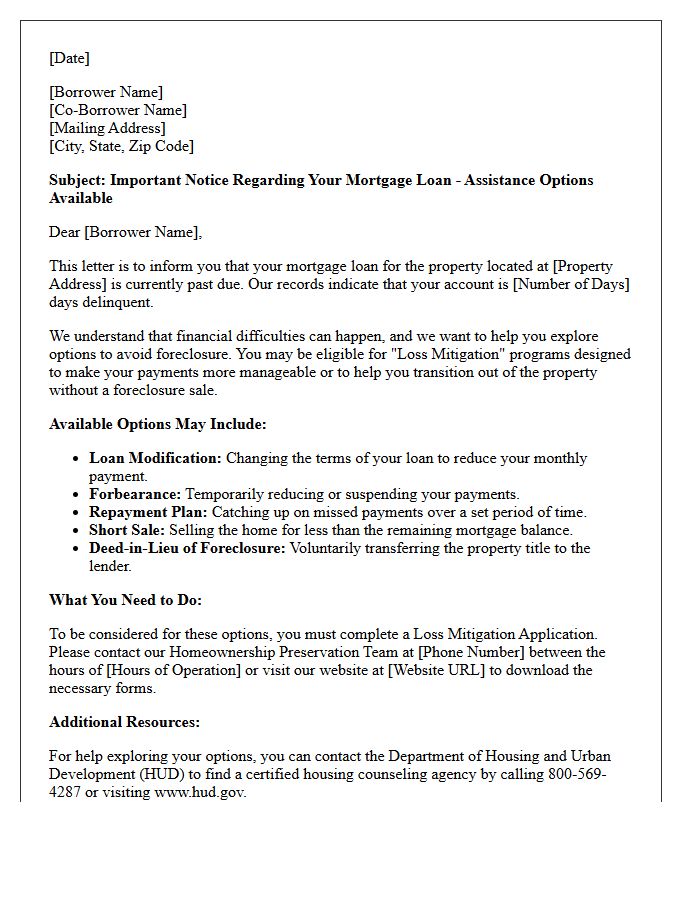

Initial Loss Mitigation Solicitation Letter

An Initial Loss Mitigation Solicitation Letter is a mandatory notice sent by mortgage servicers to borrowers entering delinquency. This document serves as a critical outreach requirement under federal law, informing homeowners of available alternatives to foreclosure. It typically outlines specific assistance programs, such as loan modifications, repayment plans, or short sales. Borrowers must act quickly upon receipt, as the letter provides a timeline and a list of necessary financial documentation required to evaluate eligibility for foreclosure prevention options and maintain homeownership stability.

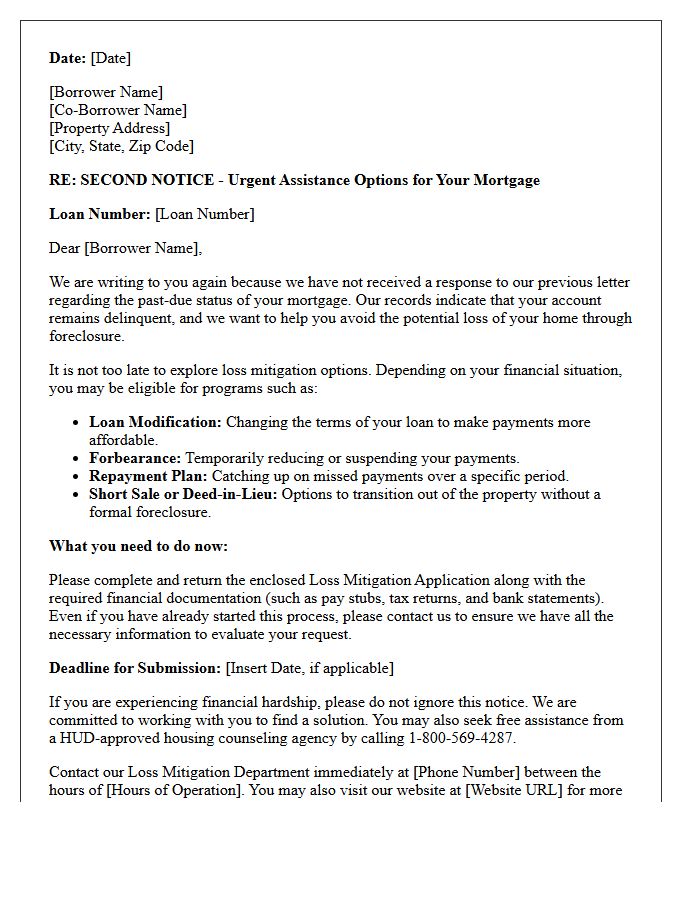

Second Request Loss Mitigation Solicitation Letter

A Second Request Loss Mitigation Solicitation Letter is a critical notice sent by mortgage servicers when a homeowner's initial application is incomplete. This document identifies missing information or documents required to evaluate foreclosure alternatives. To avoid foreclosure, borrowers must respond by the specified deadline to maintain their legal protections. Promptly submitting the requested paperwork allows the lender to finalize a review for options like loan modifications, short sales, or deeds-in-lieu, ensuring the mitigation process continues without further delays or loss of homeownership rights.

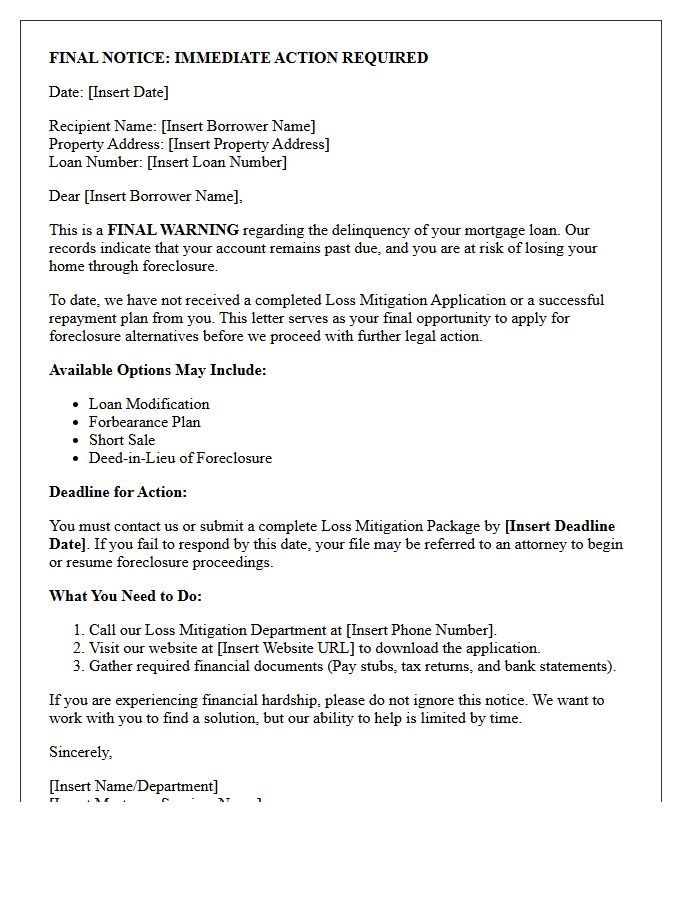

Final Warning Loss Mitigation Solicitation Letter

A Final Warning Loss Mitigation Solicitation Letter is a critical notice from your mortgage servicer indicating the last opportunity to avoid foreclosure. It outlines available alternatives, such as loan modifications, short sales, or deeds-in-lieu, to resolve payment delinquencies. Ignoring this document typically triggers immediate legal action. Homeowners must submit a complete loss mitigation application before the stated deadline to stay proceedings. Reviewing these options promptly is essential for preserving homeownership and protecting your credit score during financial hardship.

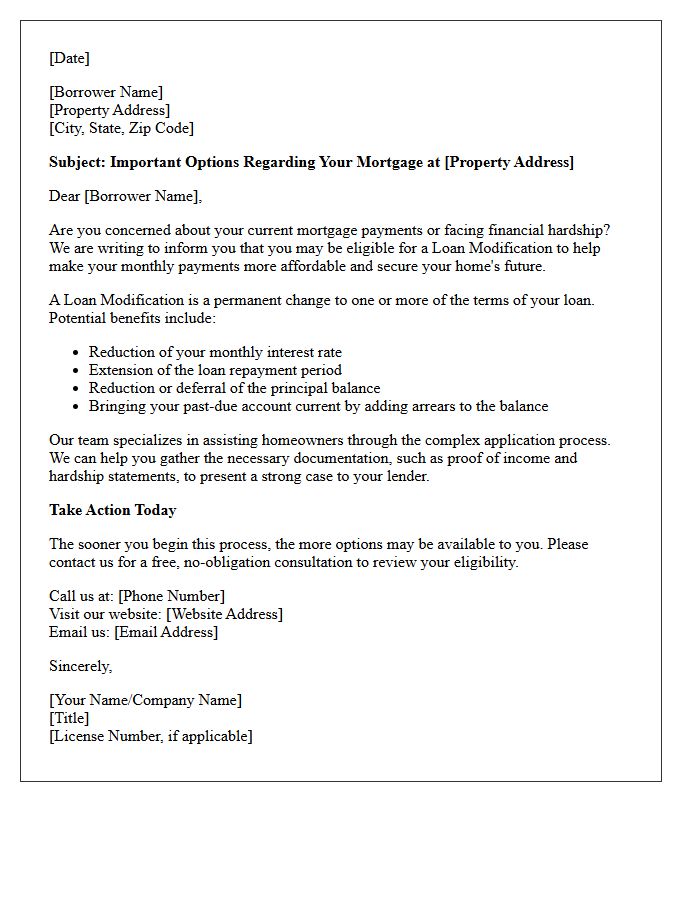

Loan Modification Assistance Solicitation Letter

A loan modification assistance solicitation letter is a marketing document from private companies offering to negotiate mortgage terms with your lender. It is crucial to understand that many of these solicitations are scams charging illegal upfront fees for services your loan servicer provides for free. Always verify the sender's legitimacy through the HUD website or a certified housing counselor. Legitimate help never guarantees a specific outcome or instructs you to stop communicating with your bank. Protecting your financial information from predatory third-party entities is essential to avoiding foreclosure fraud.

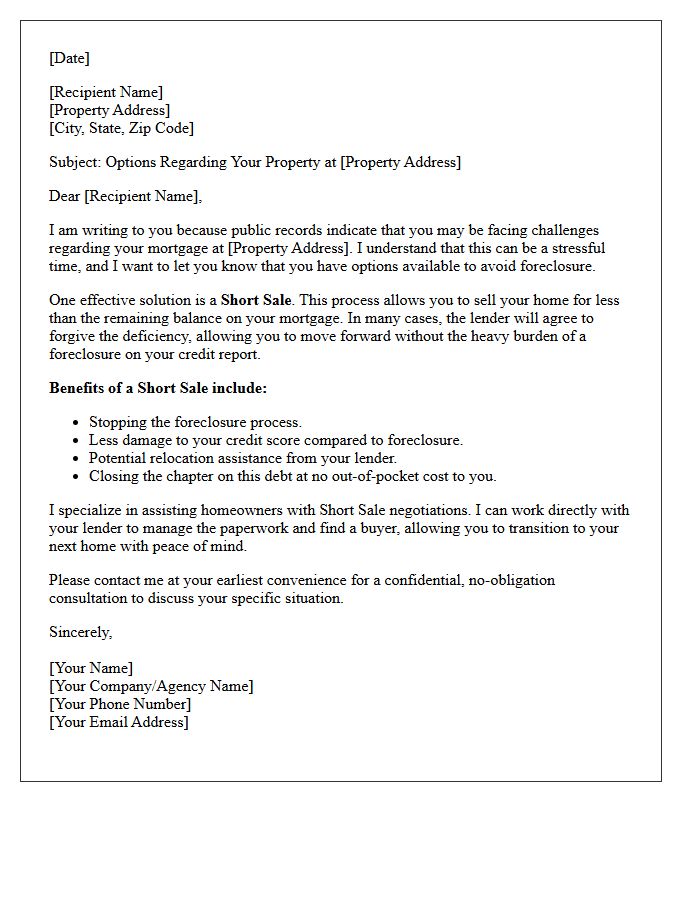

Short Sale Option Solicitation Letter

A Short Sale Option Solicitation Letter is a formal notification from a mortgage servicer inviting homeowners in financial distress to consider a short sale rather than facing foreclosure. This document outlines the potential benefits, such as deficiency waivers and relocation assistance incentives. It serves as a critical opportunity for borrowers to settle their debt by selling the property for less than the outstanding loan balance. Reviewing the terms carefully is essential to understand how it impacts your credit score and future mortgage eligibility.

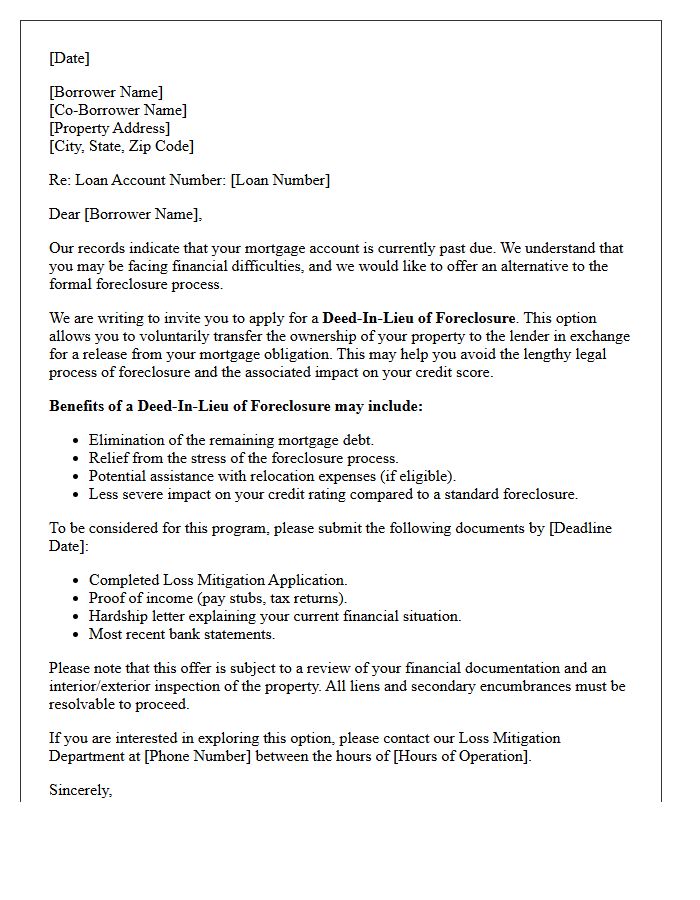

Deed-In-Lieu Of Foreclosure Solicitation Letter

A Deed-In-Lieu of Foreclosure solicitation letter is a formal invitation from a mortgage servicer to a homeowner in default. It proposes voluntarily transferring property ownership to the lender to satisfy the debt and avoid a formal foreclosure sale. This document outlines potential benefits, such as deficiency waivers or relocation assistance, often called "cash for keys." Borrowers must carefully review the terms to ensure the lender releases them from all future liability. Responding to this solicitation can mitigate credit score damage compared to a traditional foreclosure proceeding.

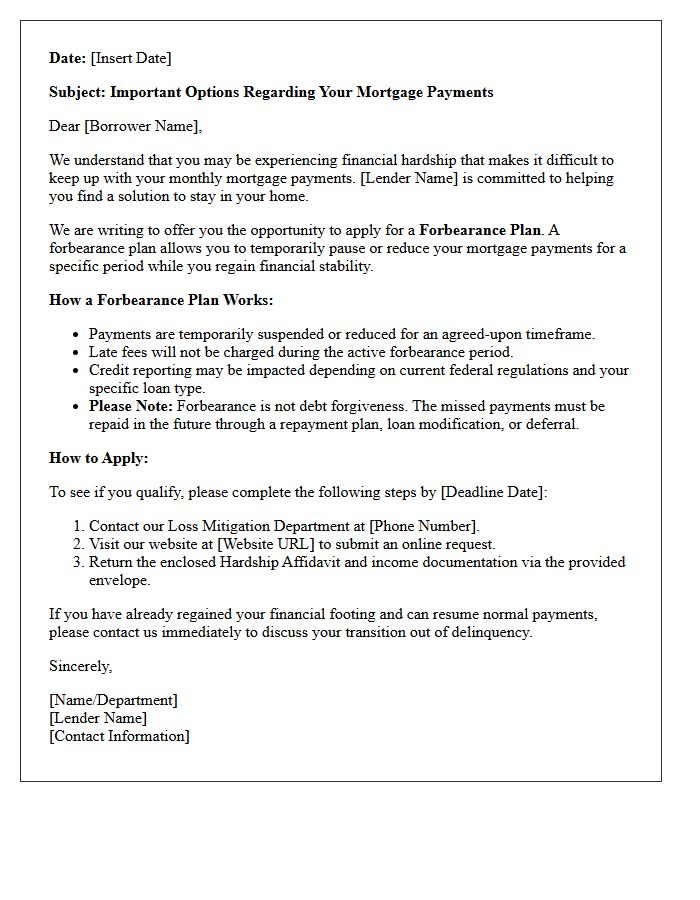

Forbearance Plan Solicitation Letter

A Forbearance Plan Solicitation Letter is a formal notice from a mortgage servicer offering temporary payment relief to borrowers facing financial hardship. This document outlines options to suspend or reduce monthly payments for a specific period. It is crucial to understand that forbearance is not debt forgiveness; skipped amounts must eventually be repaid. Reviewing the repayment terms and eligibility requirements immediately is essential to avoid foreclosure. Always contact your lender directly to verify the letter's authenticity and discuss long-term loss mitigation strategies to protect your home equity.

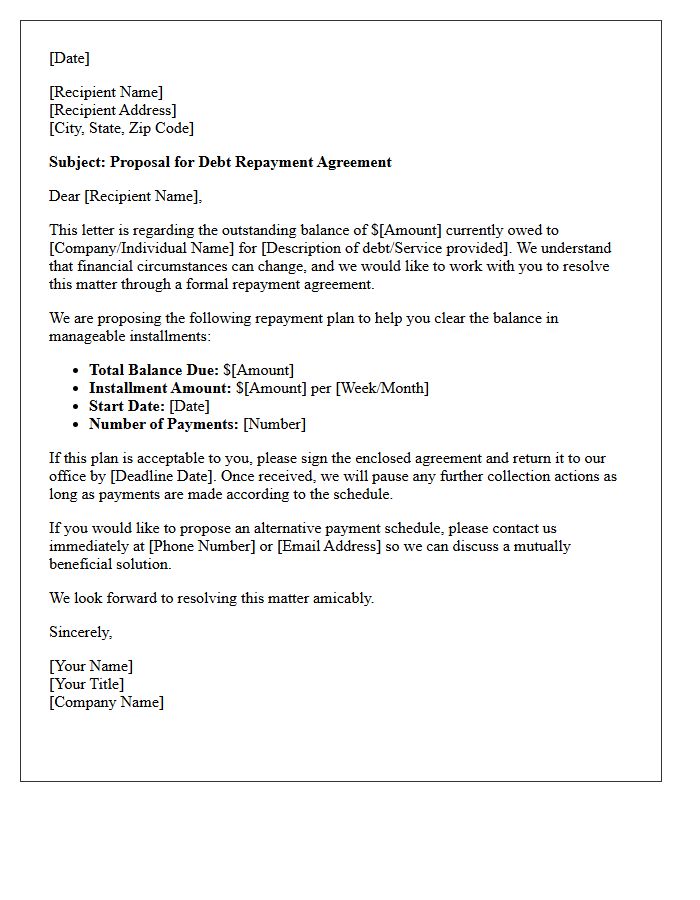

Repayment Agreement Solicitation Letter

A Repayment Agreement Solicitation Letter is a formal proposal sent by a creditor or collection agency to a debtor. It aims to restructure outstanding debt through a manageable installment plan rather than demanding an immediate lump-sum payment. Recipients should carefully review the terms and conditions, including interest rates and payment schedules, before signing. Acknowledging this letter can restart the statute of limitations on debt, so it is crucial to verify the debt's validity and seek legal advice to ensure the agreement is fair and protects your financial rights.

Early Intervention Loss Mitigation Letter

An Early Intervention Loss Mitigation Letter is a formal notice sent by mortgage servicers when a borrower misses payments. This federally mandated document provides essential homeownership preservation options to prevent foreclosure. It details available assistance programs, such as loan modifications or repayment plans, and lists contact information for housing counselors. Receiving this letter is a critical opportunity to communicate with your lender. Acting quickly upon receipt allows homeowners to explore legal protections and foreclosure alternatives to stabilize their financial situation and retain their property.

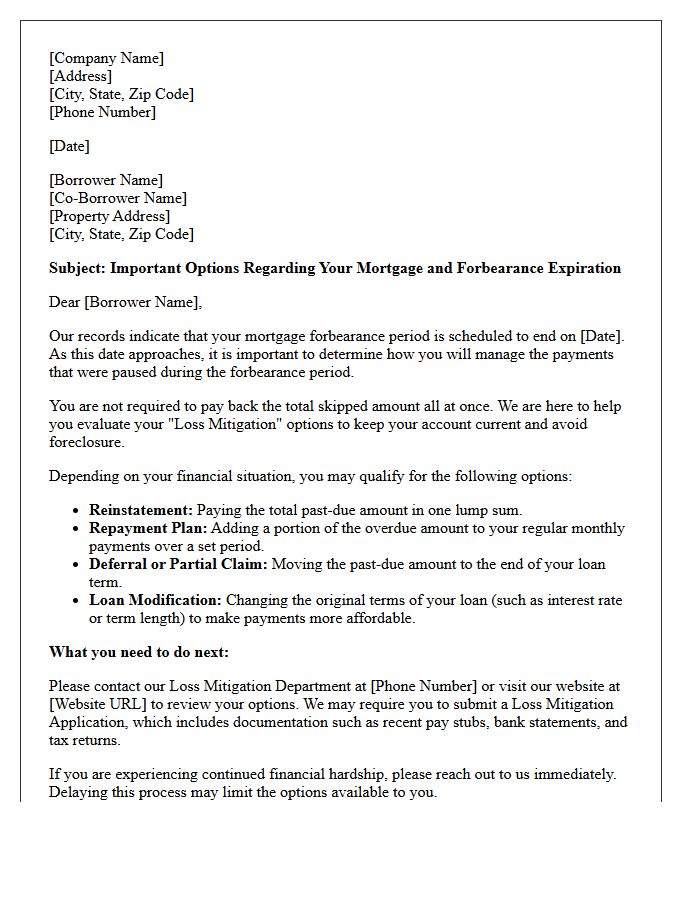

Post-Forbearance Loss Mitigation Solicitation Letter

A Post-Forbearance Loss Mitigation Solicitation Letter is a critical notice sent by mortgage servicers as a payment pause ends. It outlines available repayment options to prevent foreclosure, such as loan modifications, payment deferrals, or repayment plans. Homeowners must respond promptly to these documents to evaluate their financial eligibility for various workout solutions. Reviewing this letter is essential for maintaining homeownership and understanding your rights under federal servicing guidelines. Ignoring this solicitation can lead to delinquency and legal action against your property title.

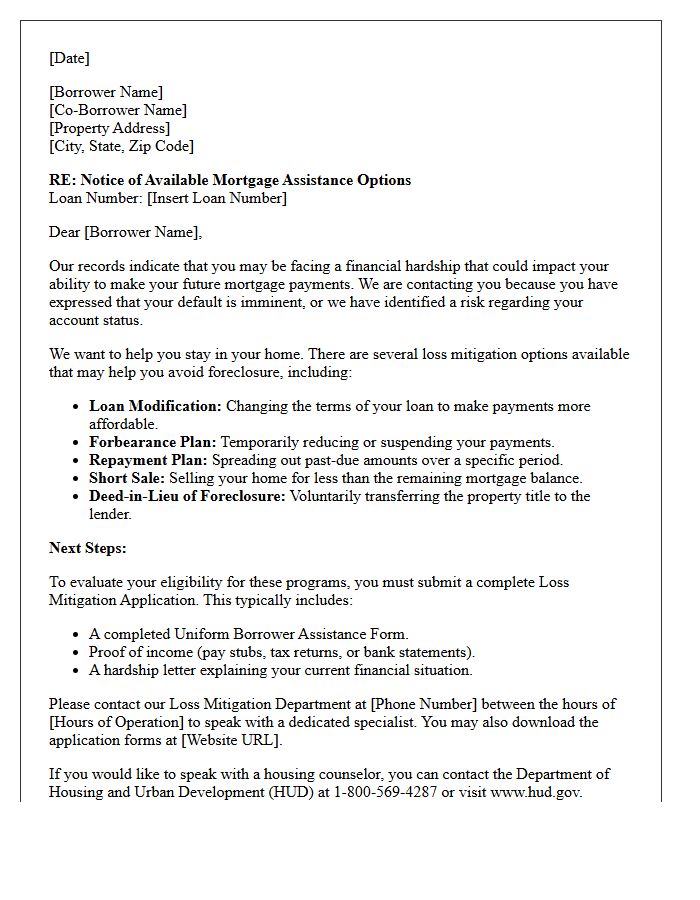

Imminent Default Loss Mitigation Solicitation Letter

An Imminent Default Loss Mitigation Solicitation Letter is a critical formal notice sent by mortgage servicers to homeowners at risk of missing payments. This document outlines available foreclosure prevention options, such as loan modifications, repayment plans, or short sales. Receiving this letter indicates that the lender is willing to negotiate to avoid legal action. To protect your home, you must respond promptly with the required financial documentation to undergo a eligibility review. Acting quickly during this pre-default phase provides the best opportunity to secure affordable terms and ensure long-term housing stability.

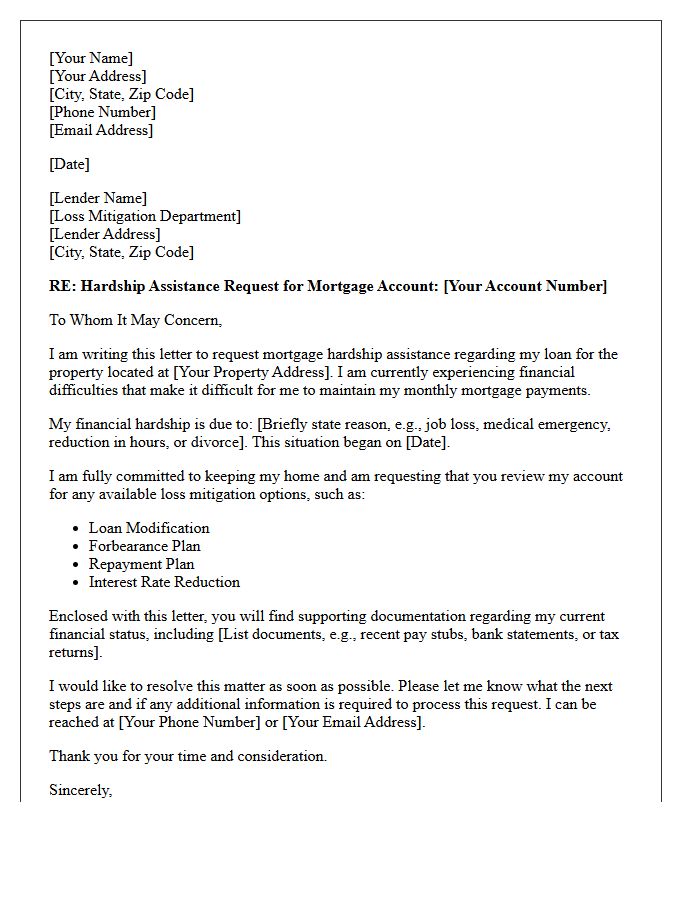

Mortgage Hardship Assistance Solicitation Letter

A Mortgage Hardship Assistance Solicitation Letter is a formal request sent to lenders to initiate loss mitigation. It serves as a vital document explaining the financial challenges, such as job loss or illness, that prevent timely payments. To be effective, the letter must clearly outline the hardship, provide a timeline of events, and propose a specific solution like loan modification or forbearance. Including supporting financial documentation is essential to demonstrate a sincere intent to resolve delinquency and avoid foreclosure proceedings while protecting your long-term housing stability.

What is a Loss Mitigation Solicitation Letter?

A Loss Mitigation Solicitation Letter is a formal notice sent by a mortgage servicer to a borrower who is delinquent or at risk of default. It outlines available options to avoid foreclosure, such as loan modifications, short sales, or repayment plans, and invites the borrower to apply for these alternatives.

What should I do if I receive a Loss Mitigation Solicitation Letter?

You should respond immediately by contacting your mortgage servicer or a HUD-approved housing counselor. The letter usually includes a deadline and a list of required financial documents-such as tax returns and pay stubs-needed to evaluate your eligibility for foreclosure prevention options.

What are the common foreclosure alternatives mentioned in these letters?

Common options include a loan modification to lower monthly payments, a forbearance plan to temporarily pause payments, a repayment plan to catch up on arrears, a short sale, or a deed-in-lieu of foreclosure. The specific options available depend on your investor's guidelines and your financial situation.

Will applying for loss mitigation stop the foreclosure process?

In many cases, yes. Under federal CFPB rules, "dual tracking" is restricted, meaning a servicer generally cannot move forward with a foreclosure sale if a complete loss mitigation application is submitted and under review within specific timeframes. However, you must submit all requested documents promptly to ensure protection.

What documents are required for a loss mitigation application?

Servicers typically require a completed Request for Mortgage Assistance (RMA) form, recent pay stubs or profit/loss statements, the last two years of federal tax returns, recent bank statements, and a hardship letter explaining why you are unable to make your current mortgage payments.

Comments