A Notice of Default and Demand for Guarantor Performance is a formal legal document issued when a primary borrower fails to meet their loan obligations. It officially notifies the guarantor of the breach and demands immediate payment or fulfillment of the guaranteed debt. Understanding this process is vital for protecting creditor rights. To assist your legal documentation, below are some ready to use template.

Image cover: Official Notice of Default and Guarantor Demand Templates

Letter Samples List

- First Notice of Default and Demand for Guarantor Performance Letter

- Final Notice of Default and Guarantor Demand Letter

- Commercial Mortgage Default Notice and Guarantor Demand Letter

- Residential Mortgage Default and Guarantor Performance Letter

- Notice of Default and Demand for Payment Guarantor Letter

- Notice of Default and Demand for Corporate Guarantor Performance Letter

- Notice of Default and Demand for Individual Guarantor Performance Letter

- Pre-Foreclosure Notice of Default and Guarantor Demand Letter

- Notice of Loan Default and Guarantor Acceleration Letter

- Mortgage Arrears Default Notice and Guarantor Demand Letter

- Notice of Material Default and Guarantor Performance Letter

- Notice of Default and Guarantor Cure Period Expiration Letter

- Notice of Default and Demand for Joint Guarantor Performance Letter

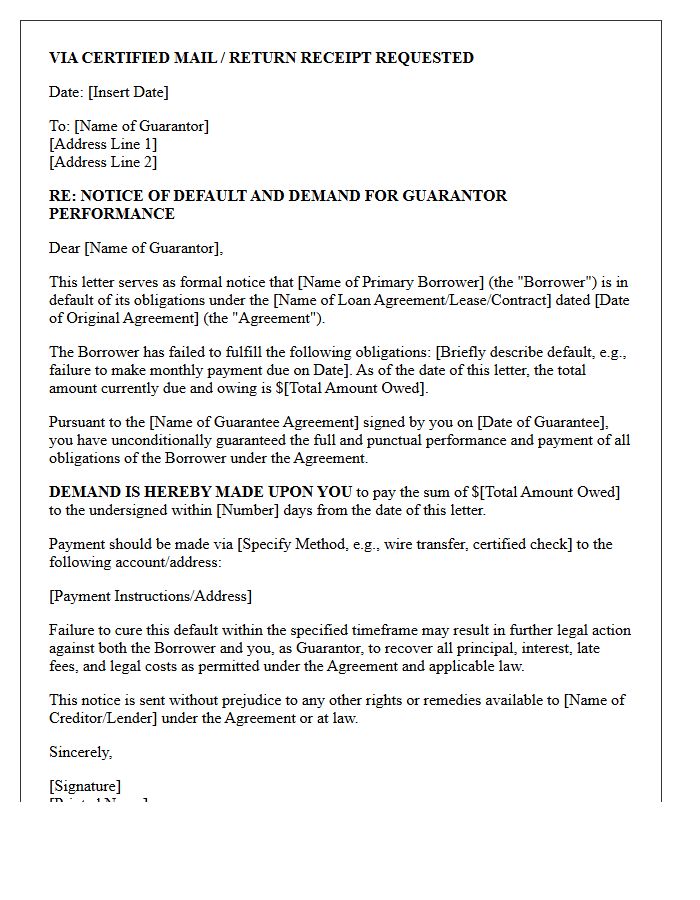

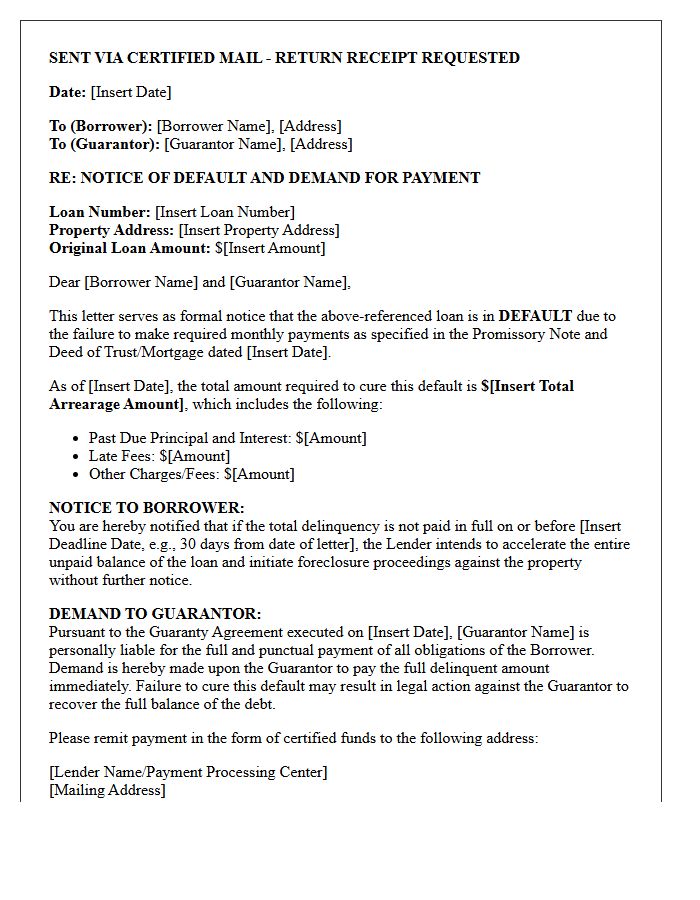

First Notice of Default and Demand for Guarantor Performance Letter

A First Notice of Default and Demand for Guarantor Performance is a critical legal document issued by a lender when a borrower breaches loan terms. It serves as a formal notification that the primary debtor has defaulted, triggering the guarantor's obligatory liability to fulfill the debt. This letter demands immediate payment or performance as outlined in the guaranty agreement. Receiving this notice is a serious escalation, indicating that the lender is moving toward legal recovery and potentially seizing assets or initiating litigation against the guarantor to satisfy the outstanding obligation.

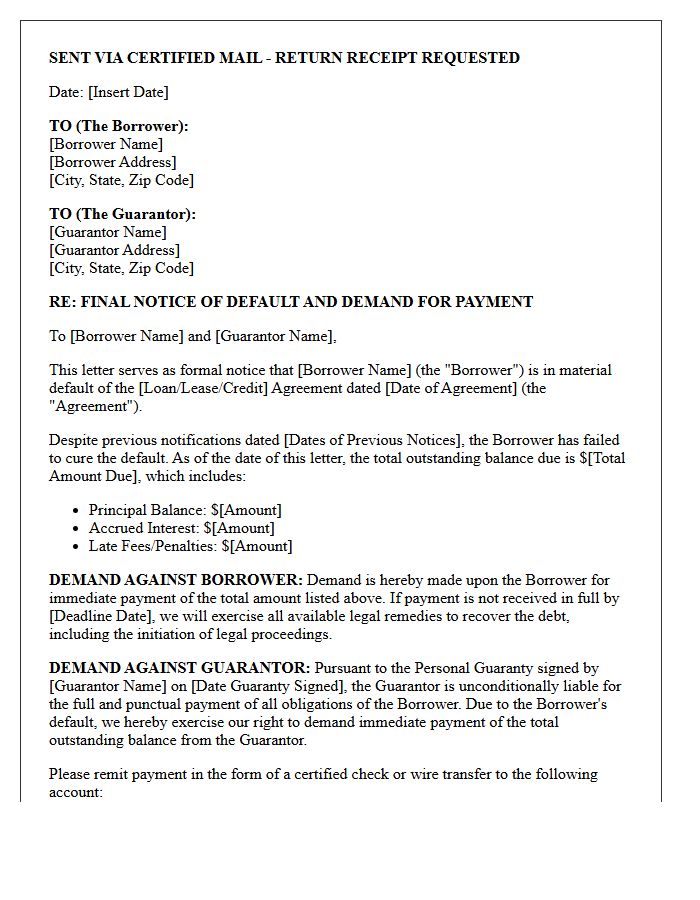

Final Notice of Default and Guarantor Demand Letter

A Final Notice of Default and Guarantor Demand Letter is a critical legal document signaling the final stage before litigation or foreclosure. It formally notifies the primary borrower of a breach of contract and demands immediate repayment of the outstanding debt. Simultaneously, it invokes the guarantor's liability, holding them personally responsible for the balance. Receiving this letter indicates that all previous cure periods have expired, making it the last opportunity to resolve the delinquency before the creditor initiates aggressive legal recovery actions against all involved parties.

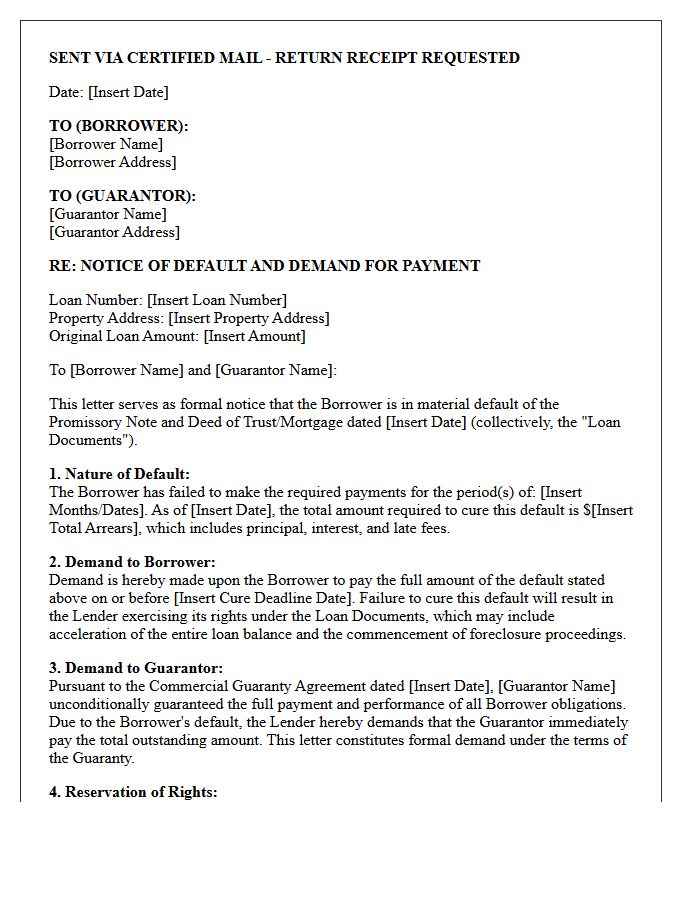

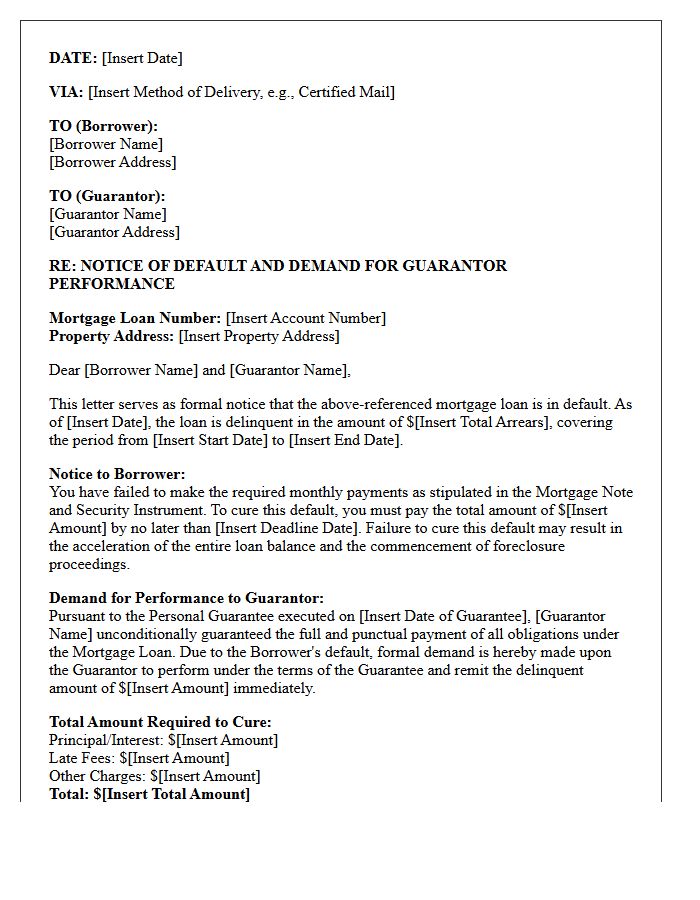

Commercial Mortgage Default Notice and Guarantor Demand Letter

A Commercial Mortgage Default Notice officially notifies a borrower of a contractual breach, such as missed payments. This formal document triggers the acceleration clause, making the full loan balance due immediately. Simultaneously, a Guarantor Demand Letter targets individuals who backed the debt, holding them personally liable for the deficiency. Receiving these notices marks the start of potential foreclosure or litigation. It is critical to review cure periods and seek legal counsel to negotiate a forbearance agreement or restructuring before the lender pursues asset seizure or a deficiency judgment.

Residential Mortgage Default and Guarantor Performance Letter

A Residential Mortgage Default and Guarantor Performance Letter is a formal legal notice issued when a borrower fails to meet repayment obligations. This document serves as a notice of default, officially informing both the primary borrower and the guarantor of the breach of contract. It demands immediate rectification of the arrears and outlines the guarantor's liability to cover the outstanding debt. Understanding this letter is crucial, as it marks the final step before a lender initiates foreclosure proceedings or pursues legal action against the guarantor's personal assets to satisfy the loan.

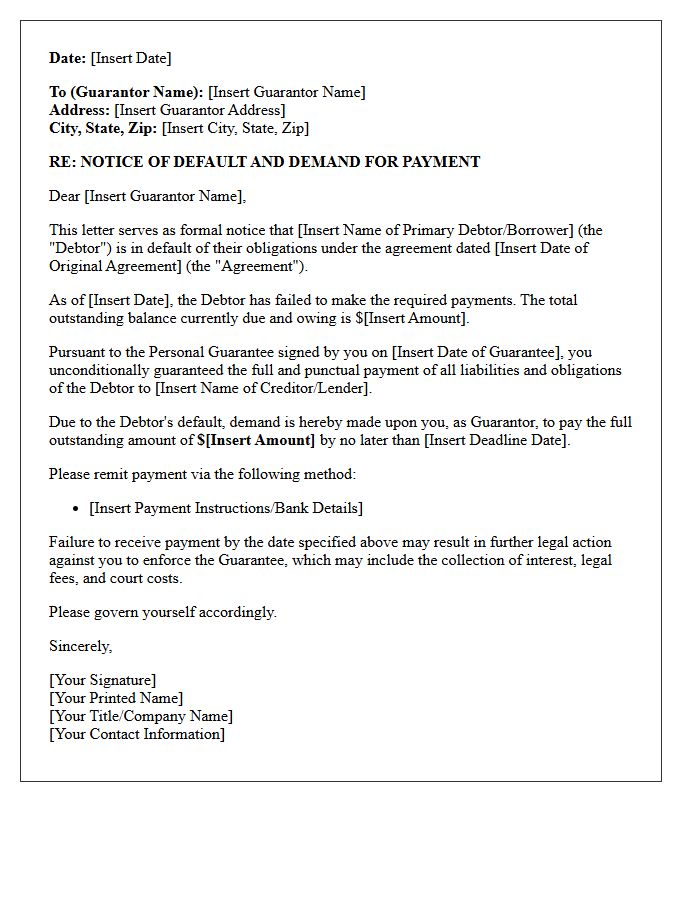

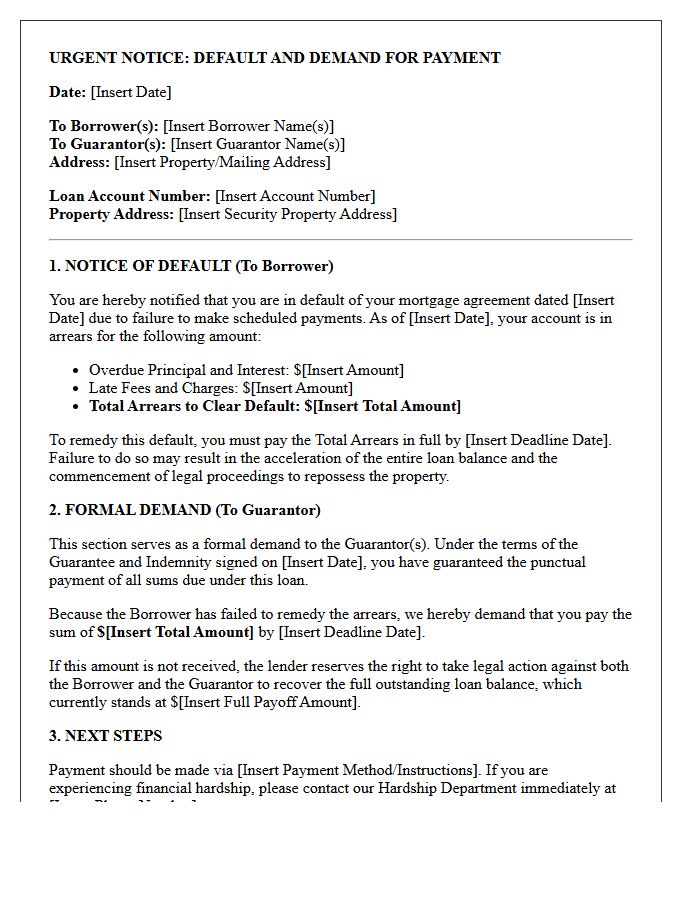

Notice of Default and Demand for Payment Guarantor Letter

A Notice of Default and Demand for Payment Guarantor Letter is a formal legal document issued when a primary borrower breaches their loan agreement. This notice officially informs the guarantor that they are now legally obligated to repay the outstanding debt immediately. It serves as a final demand before the lender pursues aggressive collection actions or litigation against the guarantor's personal assets. Understanding this notice is critical, as it signifies that the lender is exercising their right to recover funds from the secondary party due to the primary borrower's insolvency or non-payment.

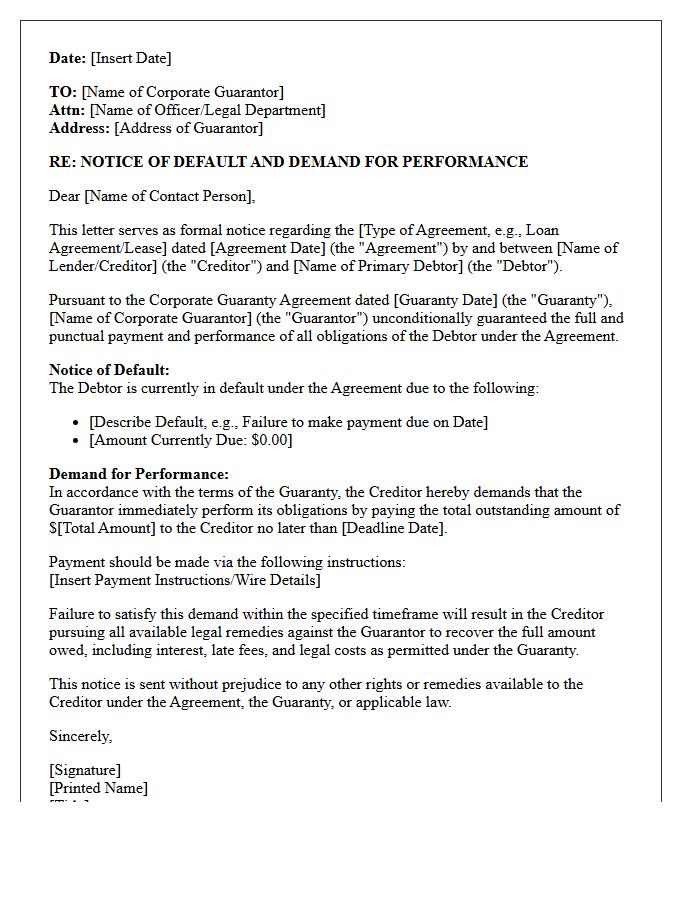

Notice of Default and Demand for Corporate Guarantor Performance Letter

A Notice of Default and Demand for Corporate Guarantor Performance Letter is a formal legal notification sent when a primary borrower fails to meet their obligations. This document informs the corporate guarantor that they are now legally required to fulfill the debt or performance duties outlined in the guarantee agreement. It serves as a critical legal prerequisite before initiating litigation or collection actions. Timely response is essential to mitigate additional interest penalties, legal fees, and potential damage to the guarantor's credit standing or corporate reputation.

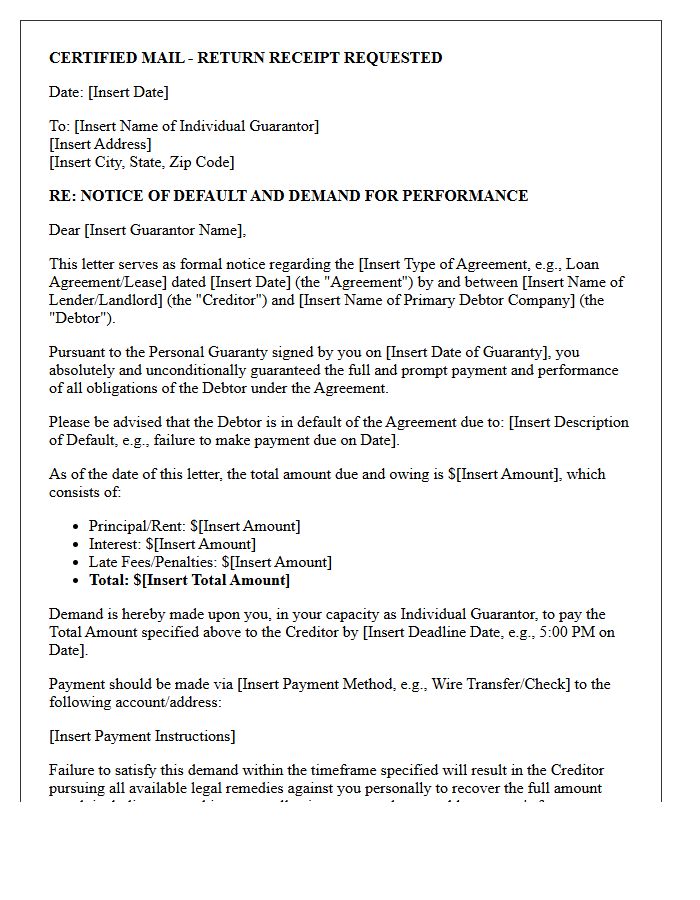

Notice of Default and Demand for Individual Guarantor Performance Letter

A Notice of Default and Demand for Individual Guarantor Performance is a formal legal document issued when a primary borrower fails to meet loan obligations. It serves as an official acceleration notice, informing the guarantor that they are now personally liable for the outstanding debt. This letter demands immediate payment or performance as outlined in the guaranty agreement. Receiving this notice is critical, as it precedes potential litigation or asset seizure. Understanding your legal defenses and the specific cure period is essential to mitigating personal financial risk and avoiding further legal escalation.

Pre-Foreclosure Notice of Default and Guarantor Demand Letter

A Pre-Foreclosure Notice of Default is a formal legal warning issued when a borrower misses multiple mortgage payments, officially starting the foreclosure process. This document provides a final opportunity to cure the reinstatement amount before the property is seized. Simultaneously, a Guarantor Demand Letter targets third parties who backed the loan, legally requiring them to fulfill the debt obligation immediately. Understanding these notices is critical for homeowners and co-signers to explore loss mitigation, negotiate settlements, or seek legal counsel to prevent total asset loss and severe credit damage.

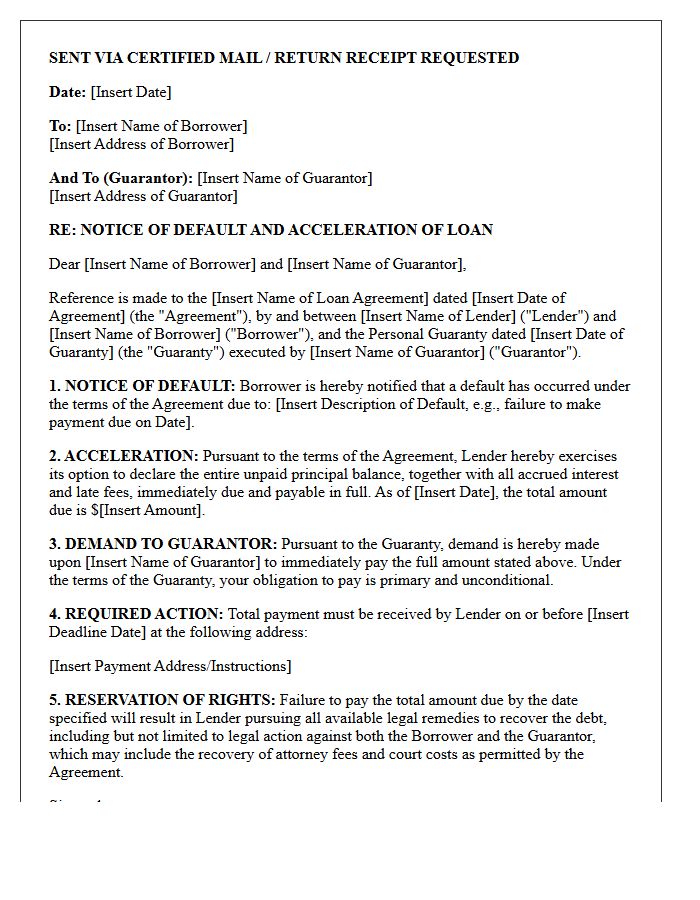

Notice of Loan Default and Guarantor Acceleration Letter

A Notice of Loan Default is a formal legal document issued when a borrower fails to meet repayment obligations. This notice officially triggers the Guarantor Acceleration Letter, which demands immediate full payment of the outstanding debt from the guarantor rather than following the original installment schedule. It signifies the end of the grace period and initiates potential legal action or asset seizure. Understanding these documents is critical, as they represent the final stage before litigation, holding the guarantor fully liable for the entire balance plus accrued interest and fees.

Mortgage Arrears Default Notice and Guarantor Demand Letter

Receiving a Mortgage Arrears Default Notice is a critical legal warning that your home loan is overdue. This document outlines the total debt and provides a specific rectification period to pay the balance before foreclosure begins. If the loan is secured by a third party, a Guarantor Demand Letter will be issued simultaneously, holding them legally responsible for the full debt. It is vital to seek immediate legal or financial advice to negotiate a hardship variation or repayment plan to protect your credit rating and prevent the loss of property ownership.

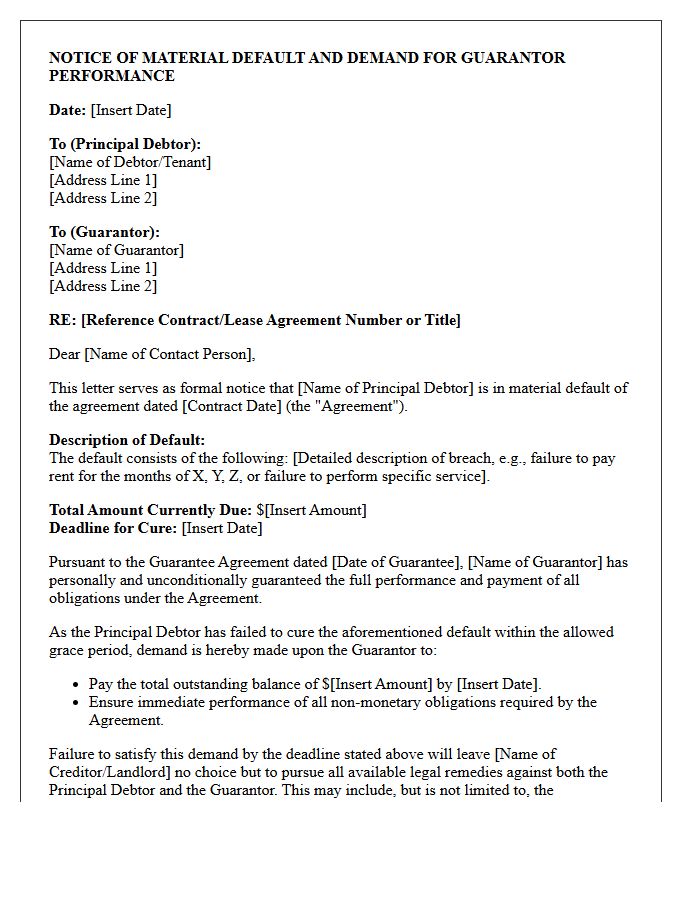

Notice of Material Default and Guarantor Performance Letter

A Notice of Material Default and Guarantor Performance Letter is a formal legal notification issued when a borrower breaches core contract terms. The notice alerts the guarantor that the primary party has failed to meet obligations, triggering the guarantor's legal liability to fulfill the debt or performance requirements. Timely response is critical, as this document often serves as a final warning before litigation or asset seizure. Understanding the specific cure period and the scope of the guarantee is essential for protecting financial interests and mitigating further legal consequences.

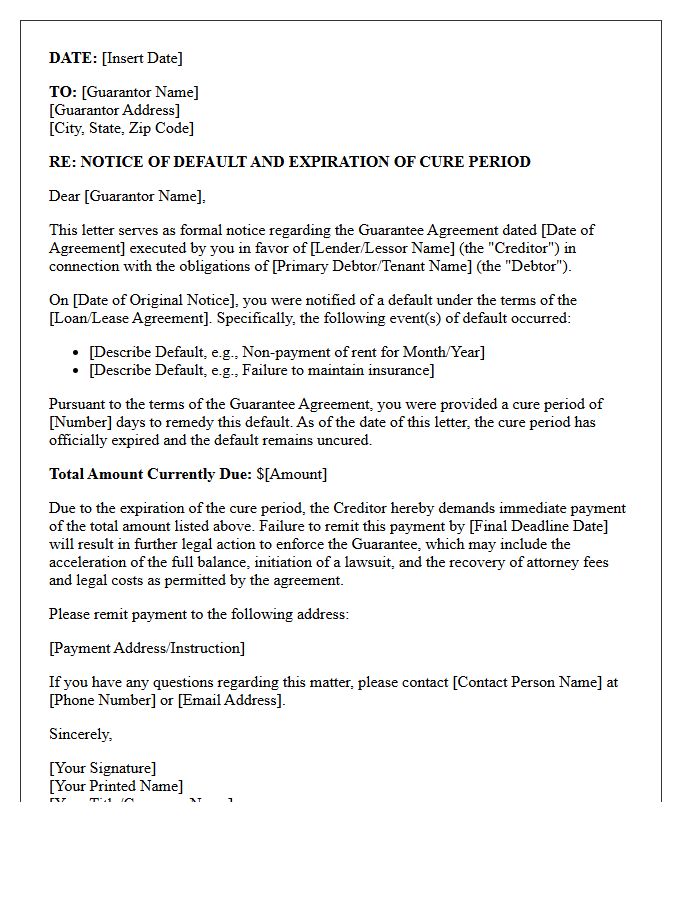

Notice of Default and Guarantor Cure Period Expiration Letter

A Notice of Default and Guarantor Cure Period Expiration Letter serves as a formal legal warning. It notifies a guarantor that the primary borrower has breached the contract and the allotted cure period-the timeframe to rectify the debt-is ending. Failure to resolve the balance before this deadline triggers the guarantor's personal liability. Once expired, the lender may initiate foreclosure or legal action to seize assets. Understanding this timeline is critical for mitigating financial risk and preventing immediate legal acceleration of the total outstanding debt amount.

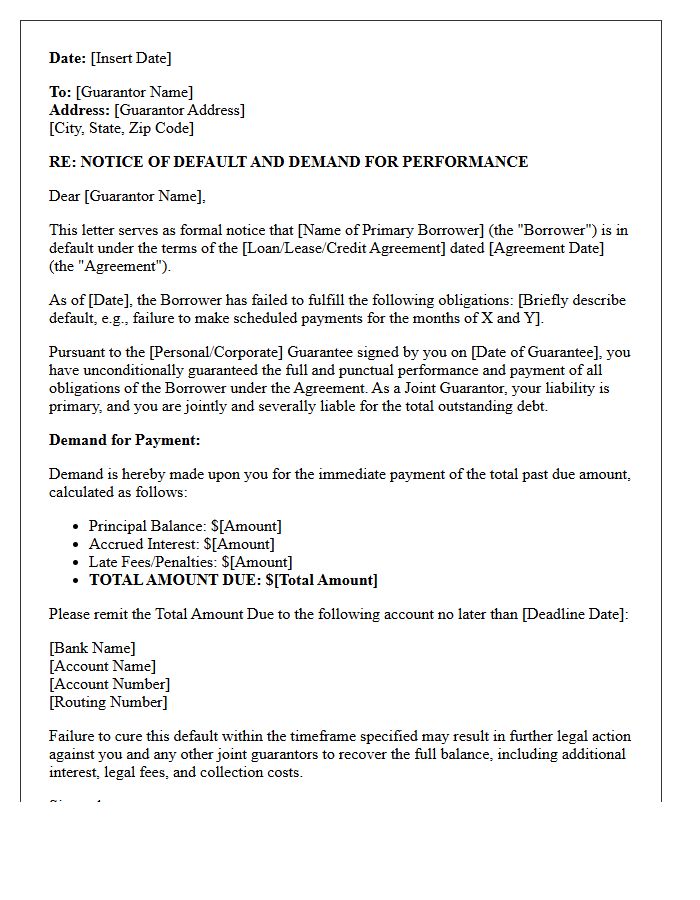

Notice of Default and Demand for Joint Guarantor Performance Letter

A Notice of Default and Demand for Joint Guarantor Performance is a formal legal document issued when a primary borrower breaches loan terms. This notice notifies the co-guarantors that they are now legally obligated to fulfill the outstanding debt obligations. Under joint and several liability, the lender can demand the full balance from any individual guarantor or all of them collectively. It serves as a final demand for payment before the creditor initiates formal litigation or asset seizure to recover the remaining balance and associated penalties.

What is a Notice of Default and Demand for Guarantor Performance?

A Notice of Default and Demand for Guarantor Performance is a formal legal communication sent to an individual or entity that has guaranteed a loan or contract. It officially notifies the guarantor that the primary borrower has defaulted and demands that the guarantor fulfill their contractual obligation to repay the debt or remedy the breach.

What triggers a demand for performance from a guarantor?

The demand is triggered when the primary borrower fails to meet specific obligations outlined in the loan agreement, such as missing scheduled payments, violating financial covenants, or filing for bankruptcy. Once a default occurs and remains uncured, the lender invokes the "guaranty" clause to seek payment directly from the guarantor.

Is a guarantor liable for the full amount of the debt?

The extent of liability depends on whether the guaranty is "unlimited" or "limited." An unlimited guaranty holds the guarantor responsible for the entire outstanding debt, including interest and legal fees. A limited guaranty restricts the guarantor's liability to a specific dollar amount or a certain percentage of the total obligation.

What happens if a guarantor ignores a Notice of Default?

If a guarantor fails to respond or perform after receiving a formal demand, the lender typically initiates legal action to enforce the guaranty. This can lead to a court judgment, wage garnishment, bank account levies, or the seizure of personal assets pledged as collateral for the guaranty.

Can a guarantor contest a Demand for Guarantor Performance?

Yes, a guarantor may contest the demand if there are valid legal defenses. Common defenses include proving the primary debt was already satisfied, demonstrating that the underlying contract was materially altered without the guarantor's consent, or identifying procedural errors in how the notice was served.

Comments