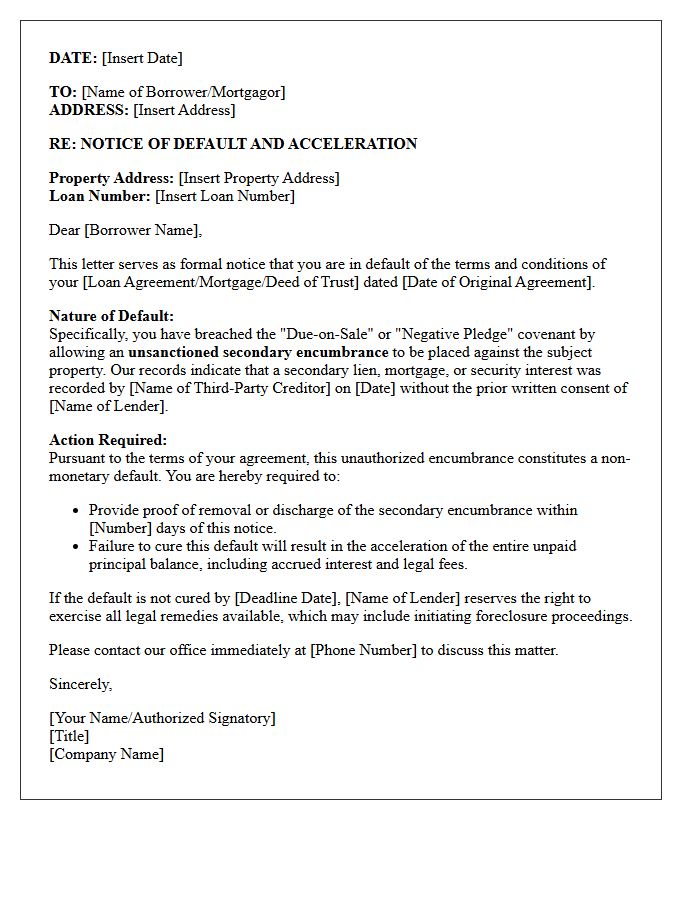

A Notice of Default for Unauthorized Secondary Financing is a legal warning issued when a borrower secures additional loans against a property without the primary lender's consent. This violation of "due-on-sale" or "anti-encumbrance" clauses can trigger immediate foreclosure proceedings. Protecting your lien priority is essential for risk management. To assist your legal notification process, below are some ready to use template.

Image cover: Official Notice of Default: Unauthorized Secondary Financing Templates and Samples

Letter Samples List

- Initial Notice of Default for Unauthorized Secondary Financing Letter

- Urgent Warning Letter Regarding Unauthorized Subordinate Liens

- Notice of Default and Intent to Accelerate Due to Secondary Financing Letter

- Commercial Mortgage Default Letter for Unapproved Junior Financing

- Final Demand Letter for Cure of Unauthorized Secondary Mortgage

- Residential Loan Breach Letter for Undisclosed Secondary Financing

- Notice of Covenant Violation Letter for Unauthorized Junior Debt

- Legal Counsel Notice Letter for Unauthorized Secondary Financing Default

- Immediate Cease and Desist Letter for Unapproved Secondary Lien Default

- Pre-Foreclosure Notice Letter for Unauthorized Subordinate Financing

- Borrower Cure Notice Letter for Breach of Secondary Financing Clause

- Default Declaration Letter for Unsanctioned Secondary Encumbrance

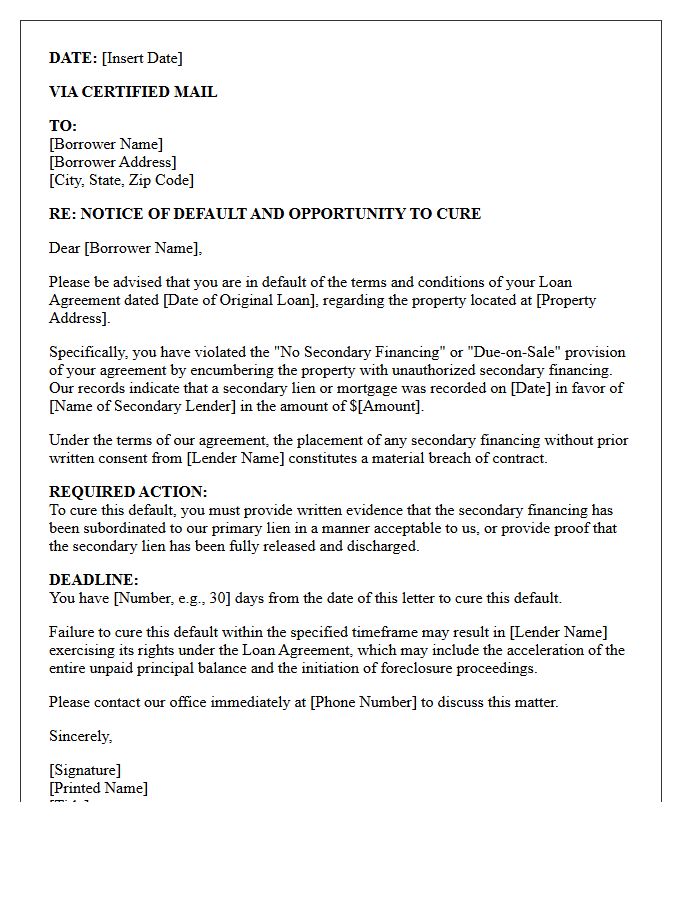

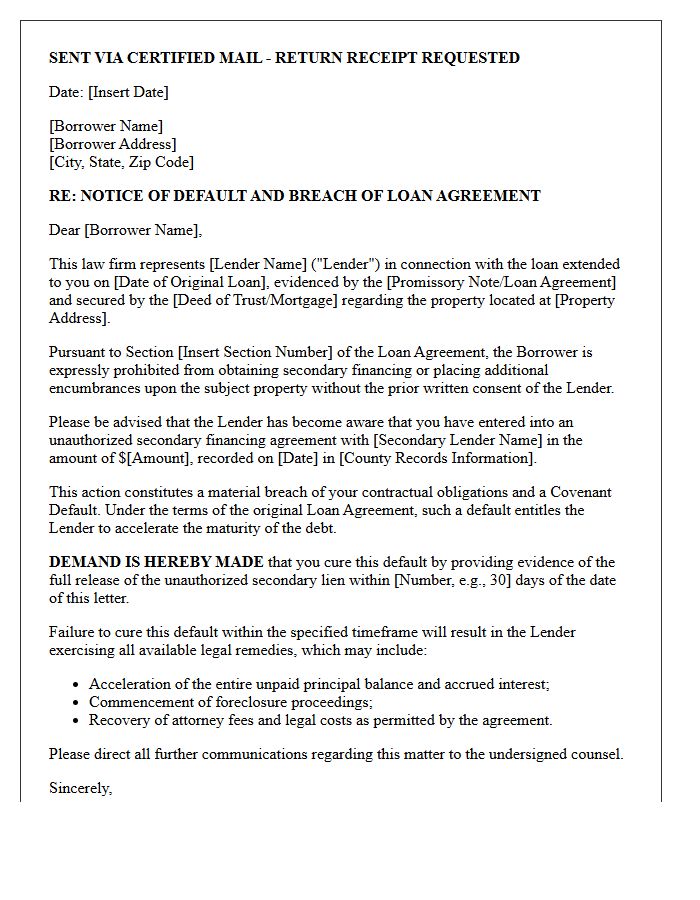

Initial Notice of Default for Unauthorized Secondary Financing Letter

An Initial Notice of Default for Unauthorized Secondary Financing is a formal legal warning issued when a borrower secures additional loans without the primary lender's consent. This action typically violates the due-on-sale or anti-encumbrance clauses within the original mortgage agreement. Receiving this letter indicates that the senior lienholder may accelerate the debt, demanding full repayment immediately. It is crucial to address this breach promptly to prevent foreclosure proceedings. Borrowers must either subordinate the junior lien or remove the unauthorized financing to restore the loan to good standing and protect their equity.

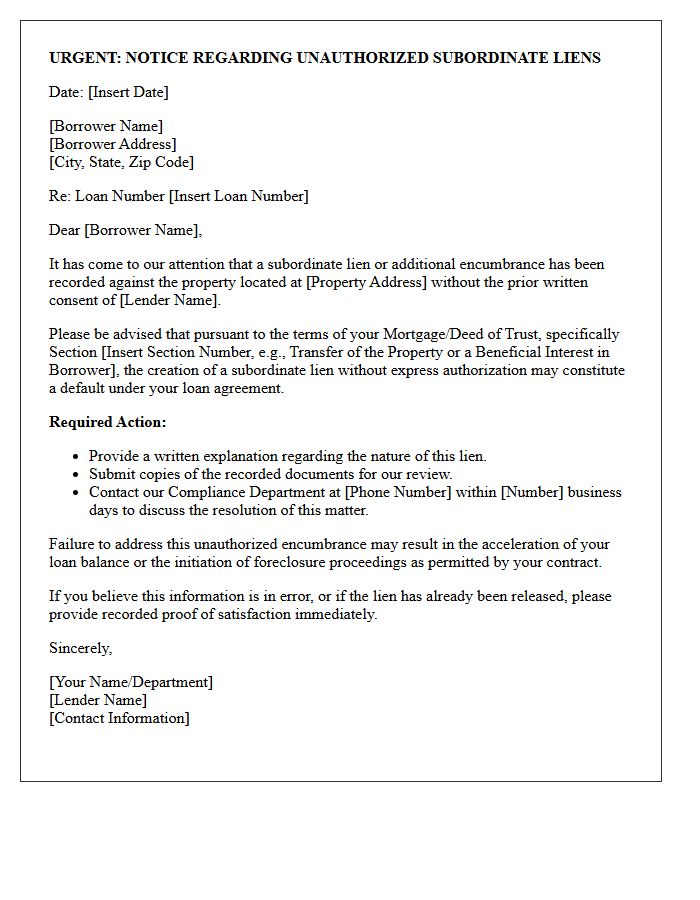

Urgent Warning Letter Regarding Unauthorized Subordinate Liens

An Urgent Warning Letter Regarding Unauthorized Subordinate Liens serves as a critical notice to property owners about junior security interests placed on a title without lender consent. These secondary debts violate due-on-sale clauses or existing loan covenants, potentially triggering a default or foreclosure. It is essential to address these unauthorized encumbrances immediately to maintain legal compliance and protect your home equity. Failure to resolve these liens can jeopardize your primary financing and overall financial stability. Act quickly to rectify any title discrepancies mentioned in the correspondence.

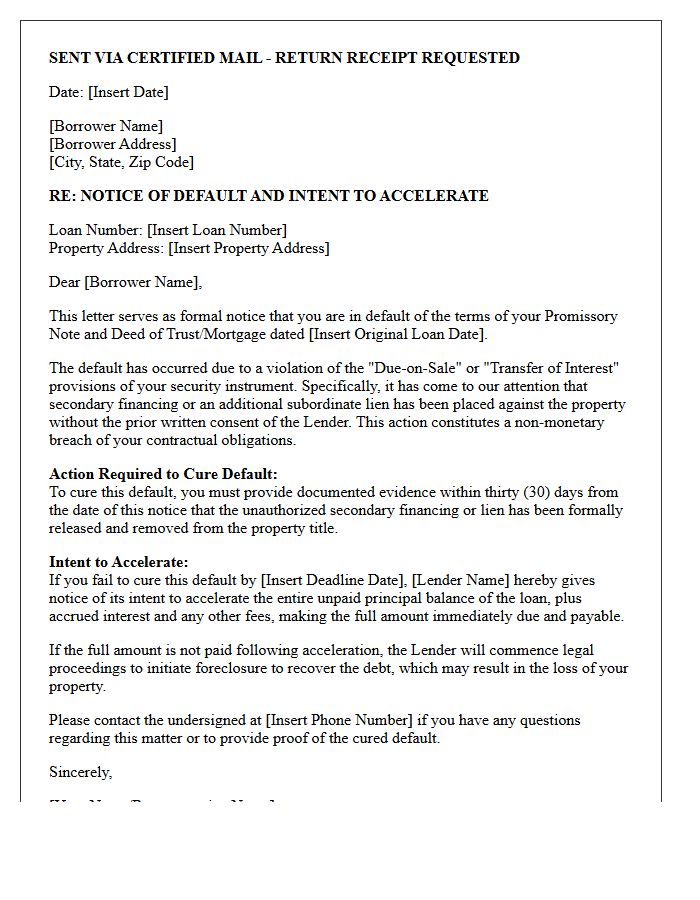

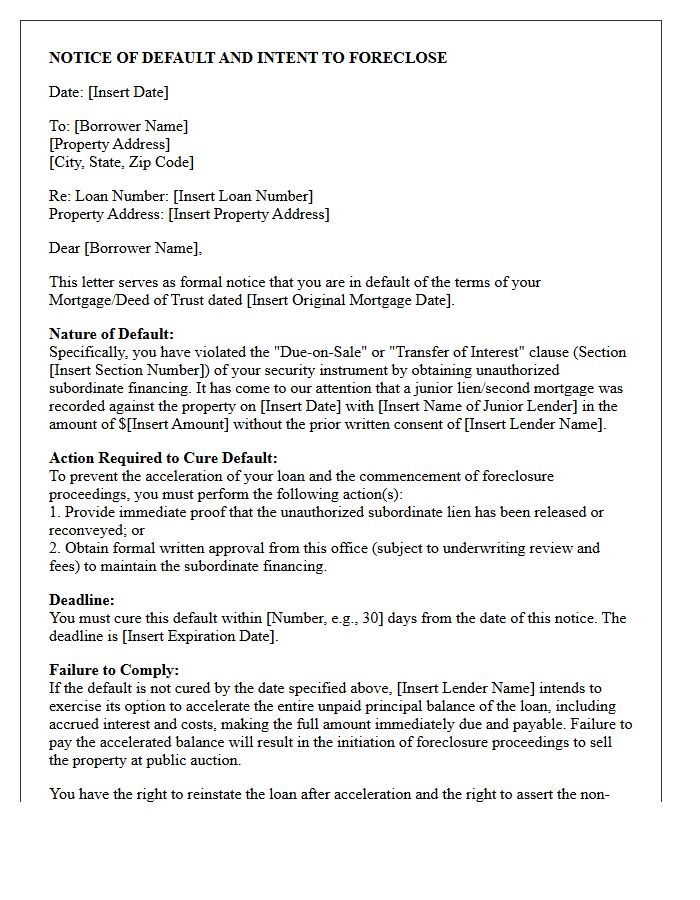

Notice of Default and Intent to Accelerate Due to Secondary Financing Letter

A Notice of Default and Intent to Accelerate Due to Secondary Financing is a formal warning from a senior lender. It states that the borrower has violated a due-on-sale clause by securing an unauthorized second mortgage or junior lien against the property. This action triggers a default, giving the lender the right to accelerate the debt, making the entire loan balance due immediately. To avoid foreclosure, the borrower must typically remove the secondary financing or obtain a formal subordination agreement within the specified cure period.

Commercial Mortgage Default Letter for Unapproved Junior Financing

A commercial mortgage default letter for unapproved junior financing notifies a borrower of a material breach of contract. Most loan agreements contain a due-on-encumbrance clause prohibiting secondary liens without lender consent. This additional debt increases financial risk and reduces equity cushions. Receipt of this formal Notice of Default typically triggers a cure period, during which the borrower must remove the unauthorized lien. Failure to resolve the violation allows the senior lender to accelerate the loan, demand full repayment, or initiate foreclosure proceedings to protect their primary security interest.

Final Demand Letter for Cure of Unauthorized Secondary Mortgage

A final demand letter for the cure of an unauthorized secondary mortgage is a legal notice issued when a borrower violates a due-on-sale clause. This document formally notifies the homeowner that securing a second loan without lender consent constitutes a contractual default. It specifies a strict cure period to resolve the breach, typically by accelerating the debt or removing the lien. Failure to address this demand allows the primary lienholder to initiate foreclosure proceedings to protect their priority interest and mitigate financial risk under the original deed of trust.

Residential Loan Breach Letter for Undisclosed Secondary Financing

A residential loan breach letter for undisclosed secondary financing notifies a borrower they have violated their mortgage contract. Lenders issue this formal notice because hidden subordinate debt increases credit risk and alters the property's loan-to-value ratio. This action often triggers a default provision, potentially leading to acceleration of the full debt. Borrowers must act quickly to resolve the discrepancy or provide proof of compliance. Understanding these legal notices is critical to preventing foreclosure proceedings initiated by the primary lienholder due to non-disclosure of additional property encumbrances.

Notice of Covenant Violation Letter for Unauthorized Junior Debt

A Notice of Covenant Violation for unauthorized junior debt is a formal legal warning issued by a senior lender when a borrower secures additional loans without prior consent. This breach often triggers a default, as secondary financing can dilute the collateral value and jeopardize the primary lender's repayment priority. Receiving this notice is a critical event that may lead to loan acceleration or foreclosure. Borrowers must immediately review their intercreditor agreements and seek a waiver or debt restructuring to resolve the non-compliance and maintain their primary financing relationship.

Legal Counsel Notice Letter for Unauthorized Secondary Financing Default

A Legal Counsel Notice Letter for Unauthorized Secondary Financing Default is a formal demand sent when a borrower secures junior liens without the primary lender's consent. This action typically violates due-on-encumbrance clauses, triggering a technical default. The letter serves as legal notification that the borrower must remedy the breach or face acceleration of the debt. It outlines specific contractual violations and sets a strict deadline for resolution. Understanding this notice is crucial for protecting collateral priority and ensuring compliance with original loan covenants to avoid potential foreclosure proceedings.

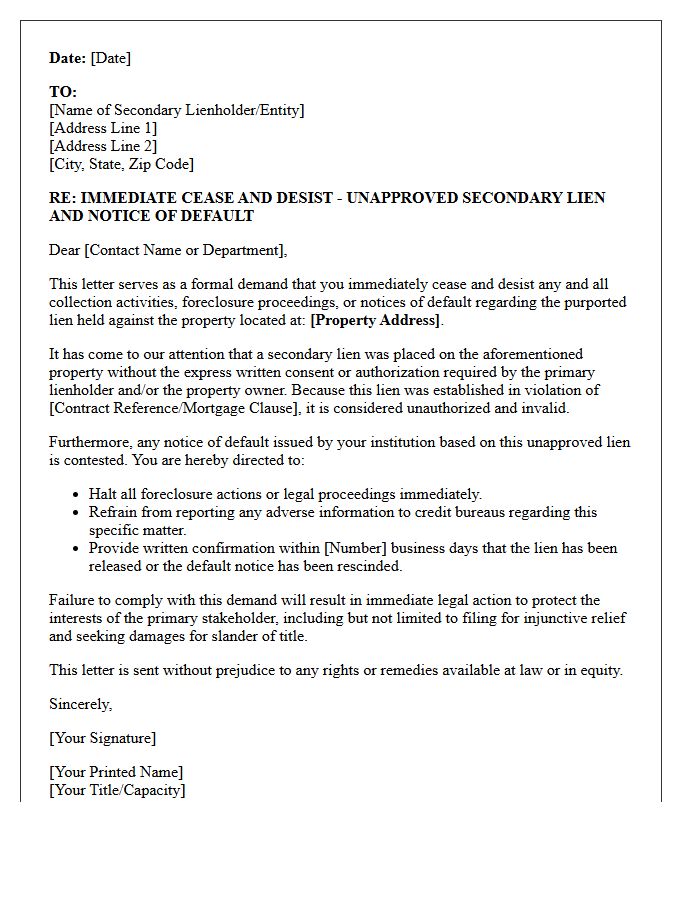

Immediate Cease and Desist Letter for Unapproved Secondary Lien Default

An Immediate Cease and Desist Letter for an unapproved secondary lien default is a critical legal notice. It formally demands the termination of unauthorized subordinate financing that violates original loan covenants. This document serves as a formal warning to junior lienholders or borrowers, asserting that the secondary encumbrance jeopardizes the primary lender's priority. Issuing this letter is a vital step to mitigate risk, prevent further contract breaches, and establish a paper trail for potential foreclosure or legal enforcement actions regarding unauthorized debt.

Pre-Foreclosure Notice Letter for Unauthorized Subordinate Financing

A pre-foreclosure notice for unauthorized subordinate financing is issued when a homeowner takes out a second mortgage or lien without the primary lender's consent. This action typically violates the due-on-sale clause found in most security instruments. Because the secondary debt increases financial risk and jeopardizes the priority of the original lien, the lender may accelerate the loan. To avoid foreclosure, borrowers must often satisfy the subordinate debt or obtain a formal subordination agreement. Promptly addressing this notice of default is essential to maintaining homeownership and protecting your credit rating.

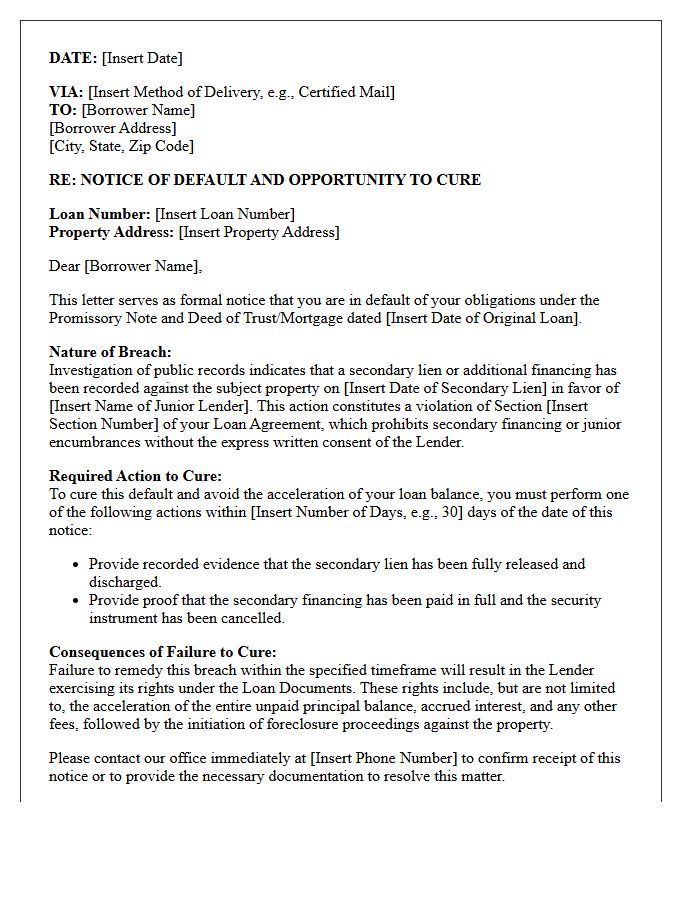

Borrower Cure Notice Letter for Breach of Secondary Financing Clause

A borrower cure notice for breaching a secondary financing clause is a formal legal warning issued when a debtor obtains unauthorized additional debt secured by the same property. This action violates the original loan agreement, potentially jeopardizing the primary lender's security interest. The notice provides a specific remedy period for the borrower to rectify the default, typically by discharging the junior lien. Failure to address this breach can lead to loan acceleration or foreclosure, as secondary financing often triggers "due-on-sale" or "anti-encumbrance" provisions designed to protect the senior creditor's priority status.

Default Declaration Letter for Unsanctioned Secondary Encumbrance

A Default Declaration Letter for Unsanctioned Secondary Encumbrance is a formal notice issued by a lender when a borrower secures additional financing against a property without prior consent. This action typically violates loan covenants, triggering a technical default. The letter informs the borrower of the breach and outlines required remedial actions to avoid foreclosure. It serves as a legal prerequisite for accelerating the debt or pursuing litigation, protecting the primary lender's priority position and ensuring the security interest remains uncompromised by unauthorized subordinate liens or junior debt obligations.

What is a Notice of Default for Unauthorized Secondary Financing?

A Notice of Default for Unauthorized Secondary Financing is a formal legal notification sent by a senior lender to a borrower when a secondary loan (such as a second mortgage or HELOC) has been secured against the property without the primary lender's prior written consent, violating the original loan agreement.

Why is secondary financing prohibited without lender consent?

Lenders prohibit unauthorized secondary financing through "Due-on-Sale" or "Anti-Encumbrance" clauses because additional debt increases the risk of foreclosure. It reduces the borrower's equity stake and creates a competing lien that can complicate the primary lender's ability to recover funds during a default.

What are the consequences of receiving a Notice of Default for an unapproved junior lien?

If a borrower fails to remedy the unauthorized financing, the primary lender can exercise the "Acceleration Clause." This demands the immediate payment of the entire remaining mortgage balance in full. Failure to pay or resolve the lien can lead to a formal foreclosure proceeding against the property.

How can a borrower cure a default caused by unauthorized secondary financing?

To cure the default, the borrower must typically pay off the secondary loan and record a release of the lien to restore the original equity position. Alternatively, the borrower can attempt to negotiate a retroactive subordination agreement where the primary lender formally approves the secondary debt, though this is at the lender's discretion.

Does a "Notice of Default" mean the property is in foreclosure?

The Notice of Default is the first public step in the legal foreclosure process, but it does not mean the property has been lost. It serves as a final warning period (reinstatement period) during which the borrower has a specific timeframe to resolve the unauthorized financing issue before the lender schedules a foreclosure sale.

Comments