Failing to address mandated property maintenance can lead to a formal Notice of Default, jeopardizing your legal standing and ownership rights. This document serves as an official warning that repair obligations have been breached, requiring immediate corrective action to avoid foreclosure or litigation. Understanding your responsibilities is essential to protecting your investment. Below are some ready to use templates.

Image cover: Formal Notice of Default: Failure to Complete Mandatory Property Repairs

Letter Samples List

- Mortgage Lender Contact Information And Date

- Borrower Name And Secured Property Address

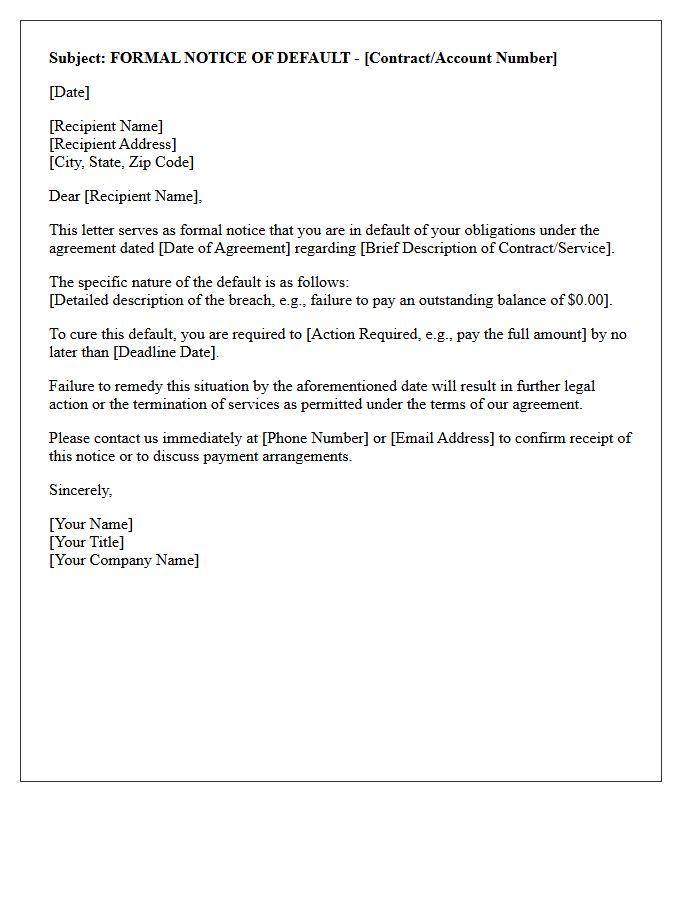

- Formal Notice Of Default Letter Subject Line

- Reference To Original Mortgage Loan Agreement

- Citation Of Property Maintenance And Repair Clauses

- Specific List Of Incomplete Required Property Repairs

- Notification Of Covenant Breach And Default Status

- Demand For Immediate Completion Of Property Repairs

- Specific Deadline For Curing The Current Default

- Consequences Of Failure To Cure Including Foreclosure

- Instructions For Scheduling A Verification Inspection

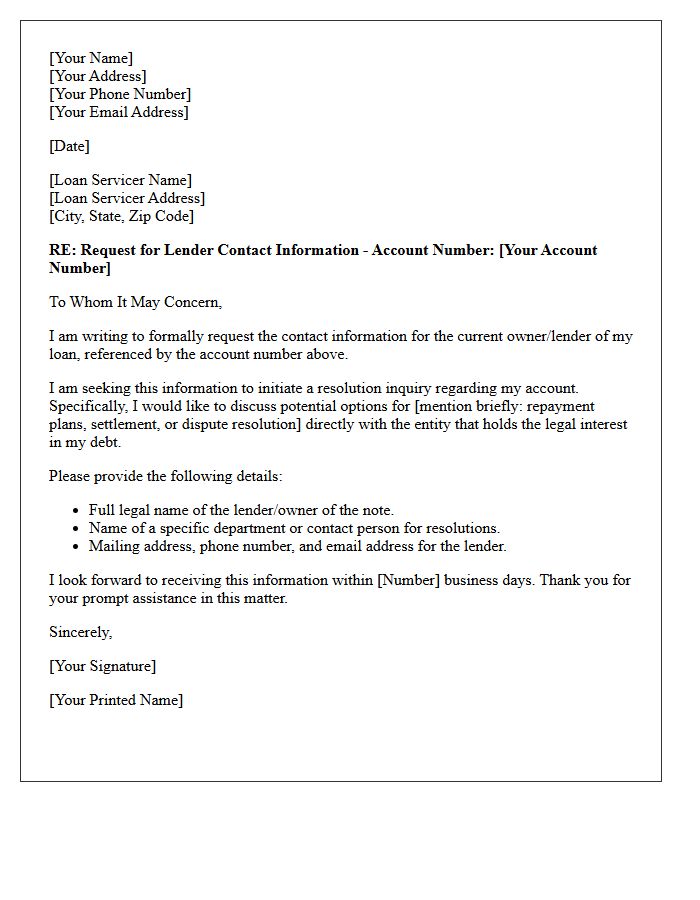

- Lender Contact Information For Resolution Inquiry

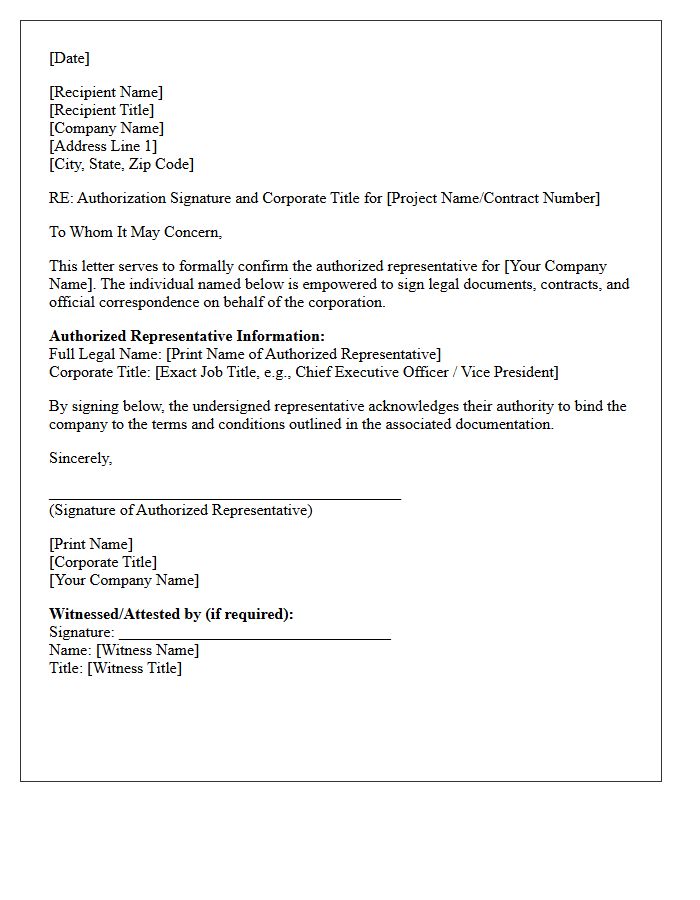

- Authorized Representative Signature And Corporate Title

Mortgage Lender Contact Information And Date

Maintaining accurate Mortgage Lender Contact Information and the specific correspondence date is vital for legal compliance and financial tracking. Always verify the lender's official phone number, mailing address, and email to ensure seamless communication regarding loan terms or payments. Recording the precise date helps establish a timeline for interest rate locks, application milestones, and regulatory deadlines. Keeping these details updated prevents missed notifications and protects your consumer rights during the home financing process.

Borrower Name And Secured Property Address

Accurate Borrower Name and Secured Property Address are fundamental for legal document validity in real estate transactions. The borrower name must match government-issued identification to ensure enforceability of the debt. Similarly, the property address identifies the specific collateral securing the loan. Discrepancies in these details can lead to title issues, funding delays, or legal challenges regarding ownership rights. Always verify that these fields precisely reflect the legal vesting and physical location to protect the interests of both the lender and the property owner.

Formal Notice Of Default Letter Subject Line

A Formal Notice of Default letter must feature a precise and urgent subject line to ensure legal compliance. It should explicitly include the case reference number, the property address, and the clear phrasing "Notice of Default." This heading serves as a formal warning that a contractual breach has occurred, typically regarding delinquent payments. Providing specific details helps establish a documented timeline, which is essential for potential foreclosure proceedings or legal remedies. A clear subject line ensures the recipient recognizes the gravity of the situation and the immediate need for action.

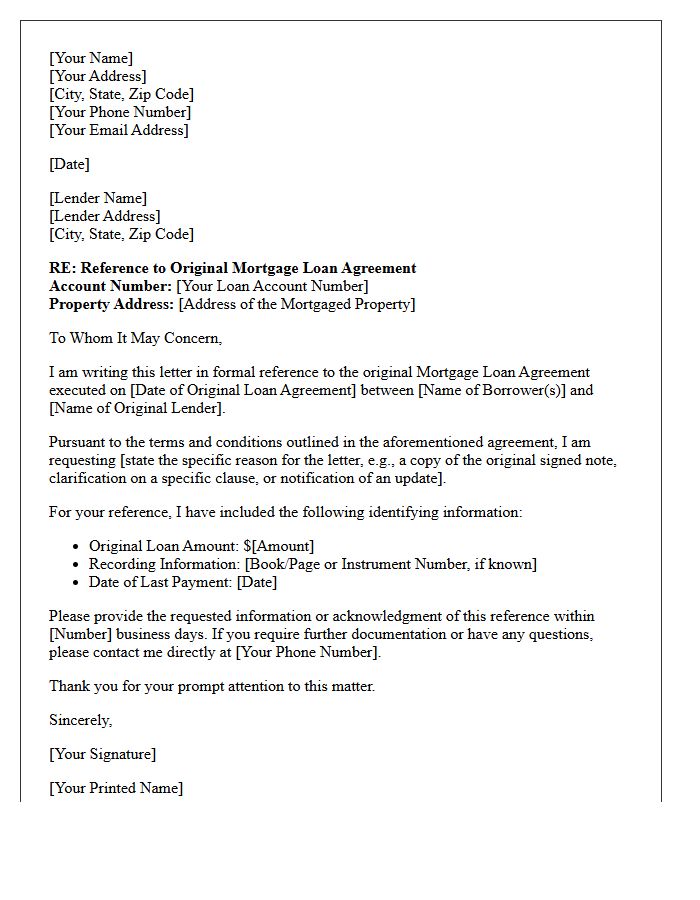

Reference To Original Mortgage Loan Agreement

The Reference To Original Mortgage Loan Agreement is a critical legal clause that identifies the primary debt contract. It ensures all subsequent modifications, assumptions, or riders are legally tied to the initial financing terms. This cross-reference maintains the priority of the lien and clarifies the borrower's obligations regarding the principal balance and interest rates. Verifying this information is essential during refinancing or property transfers to guarantee that all legal documents accurately reflect the current standing of the underlying security instrument and its historical amendments.

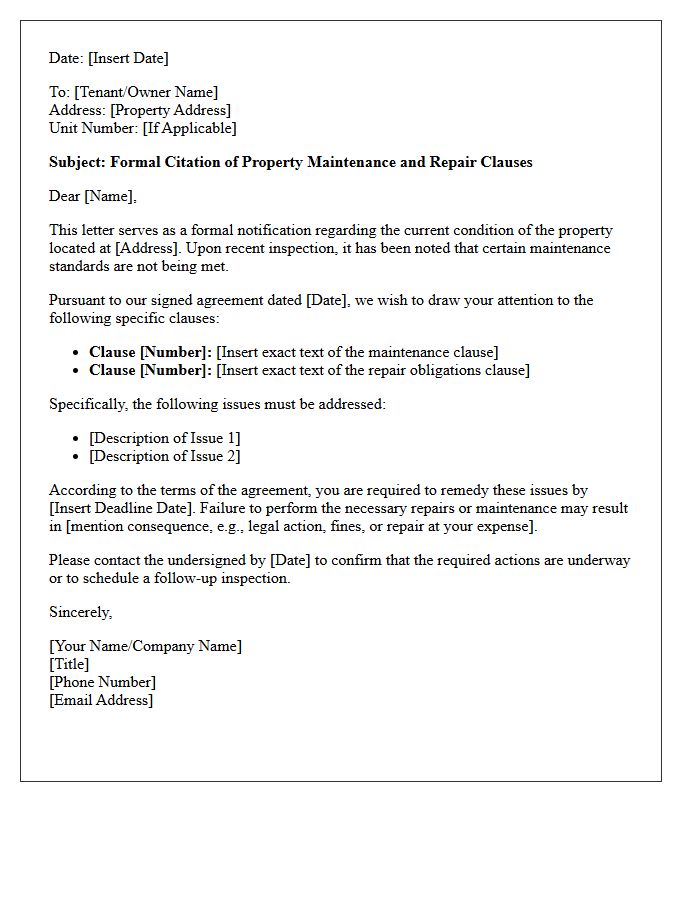

Citation Of Property Maintenance And Repair Clauses

Property maintenance and repair clauses are essential contractual terms that define the legal responsibilities between landlords and tenants. These provisions specify who must perform and fund upkeep, from minor fixes to major structural integrity. It is vital to cite specific clauses accurately during disputes to establish liability and prevent financial loss. Clear language regarding "wear and tear" versus "damage" ensures accountability, protecting the property's value while maintaining statutory compliance with local housing standards and safety regulations.

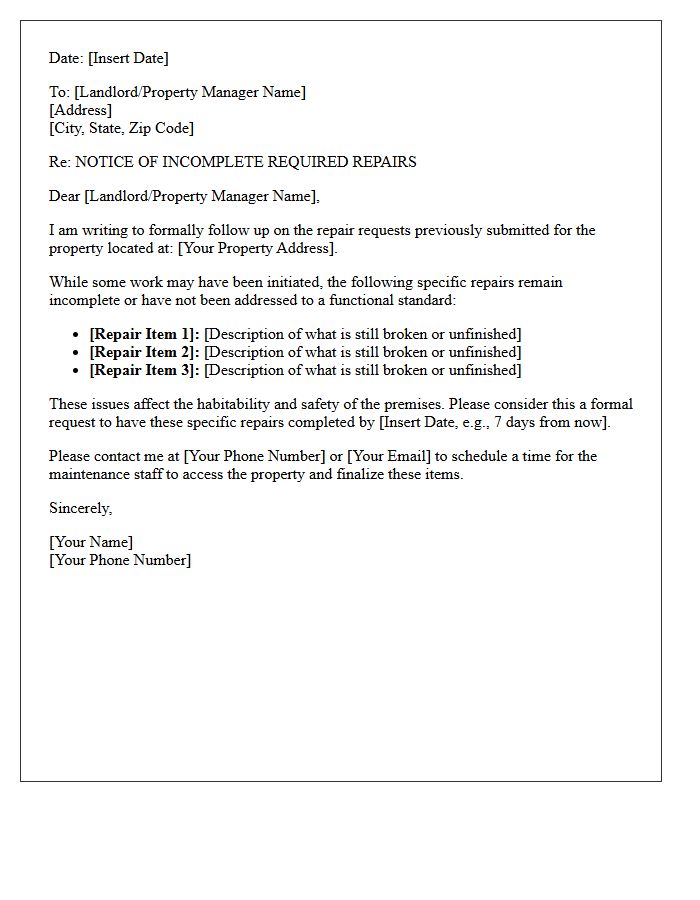

Specific List Of Incomplete Required Property Repairs

A Specific List of Incomplete Required Property Repairs is a critical legal document used during real estate transactions to identify outstanding maintenance issues. It ensures that the seller addresses agreed-upon defects before closing. This detailed record protects the buyer's investment by documenting safety hazards, structural concerns, or mechanical failures that remain unresolved. Reviewing this list carefully is essential for contract compliance and serves as a final checklist during the walkthrough inspection to verify that all necessary property improvements have been professionally completed according to the terms of the sale.

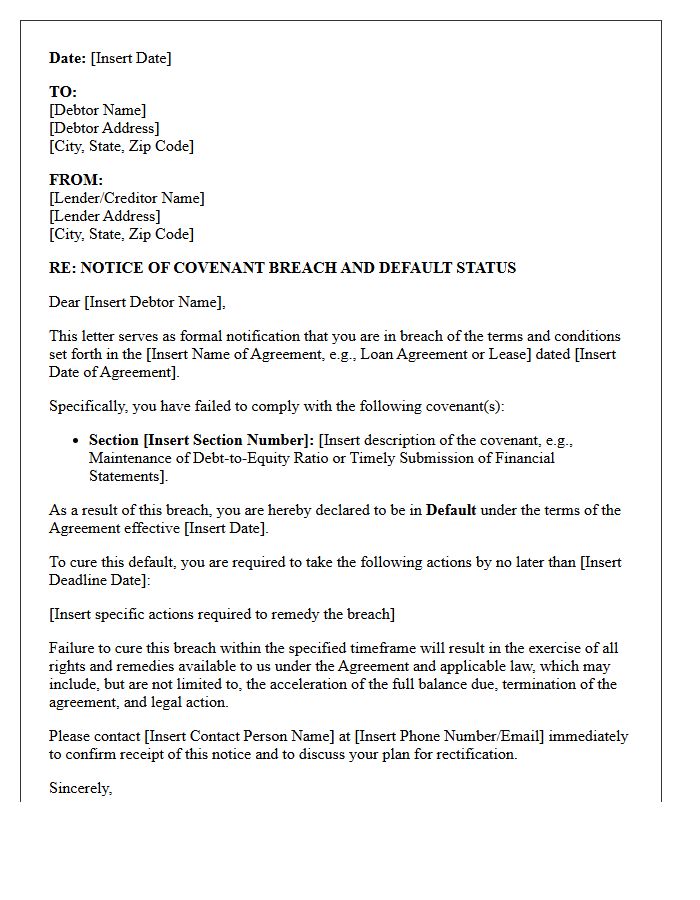

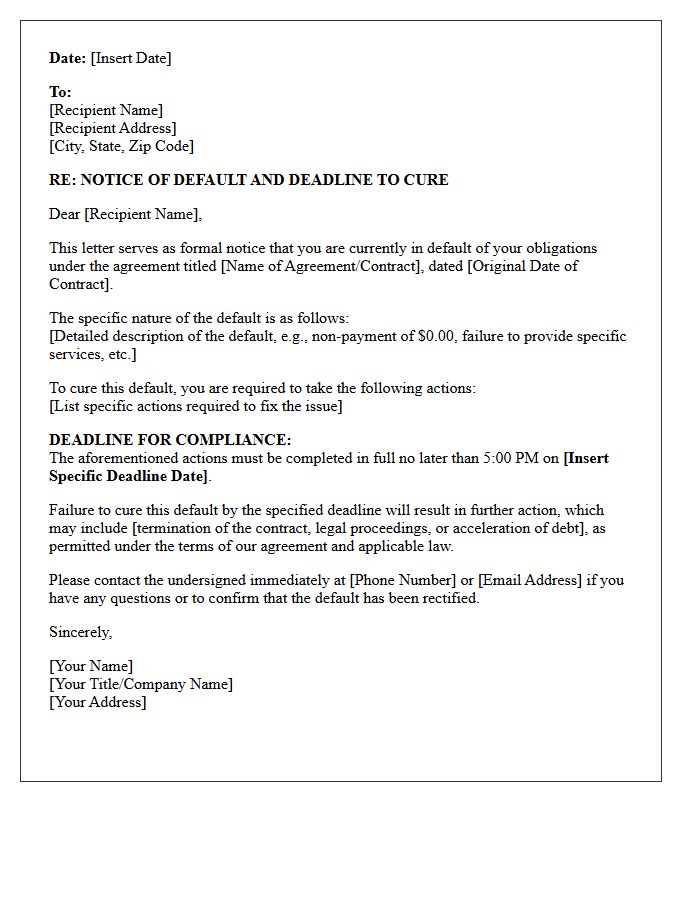

Notification Of Covenant Breach And Default Status

A Notification of Covenant Breach and Default Status is a formal legal warning issued when a borrower violates specific terms of a loan agreement. This document identifies the exact contractual failure, such as missing financial ratios or payment deadlines. Receiving this notice signifies that the lender may accelerate the debt, demand immediate repayment, or initiate foreclosure. It is critical to respond promptly during any provided cure period to rectify the violation and prevent permanent default, protecting your credit standing and collateral from potential seizure or legal action.

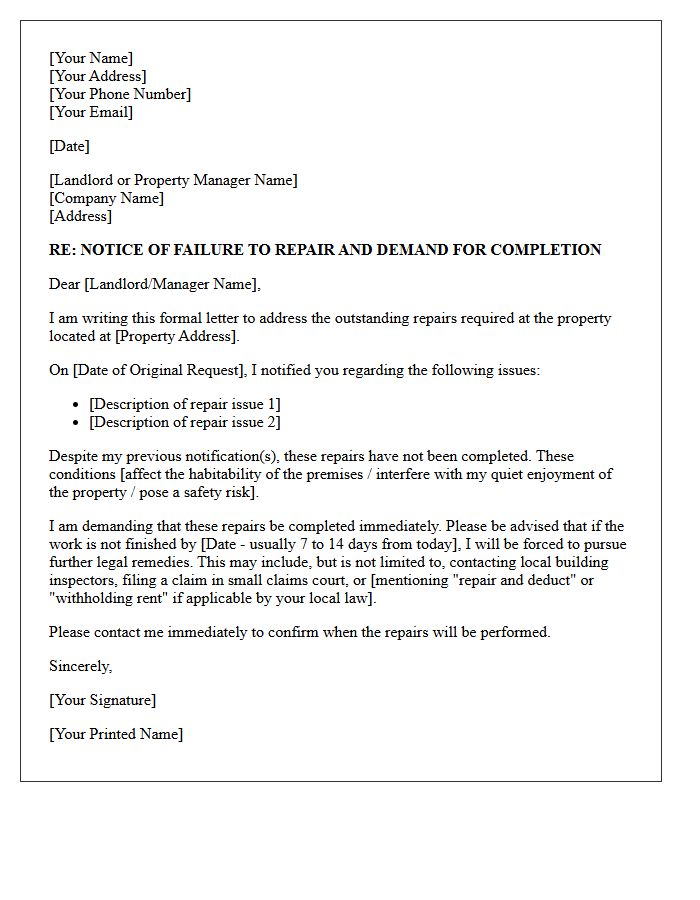

Demand For Immediate Completion Of Property Repairs

Issuing a formal demand for immediate completion of property repairs is essential to enforce landlord obligations and protect tenant safety. This written notice should clearly outline the outstanding maintenance defects and specify a reasonable deadline for resolution. Documenting all communication serves as vital evidence if legal action or rent withholding becomes necessary. Ensuring the property remains in a habitable condition is a fundamental right, making a structured demand the most effective way to compel urgent action and ensure structural integrity or safety standards are met promptly.

Specific Deadline For Curing The Current Default

Borrowers must adhere to the Specific Deadline For Curing The Current Default to prevent immediate foreclosure or legal action. This date represents the final opportunity to pay the outstanding balance and reinstate the loan agreement. Missing this window often results in the loss of property rights or severe financial penalties. It is essential to review your formal notice carefully, as the timeline is strictly enforced by lenders. Acting before this cutoff is the most effective way to resolve a delinquency and maintain your credit standing.

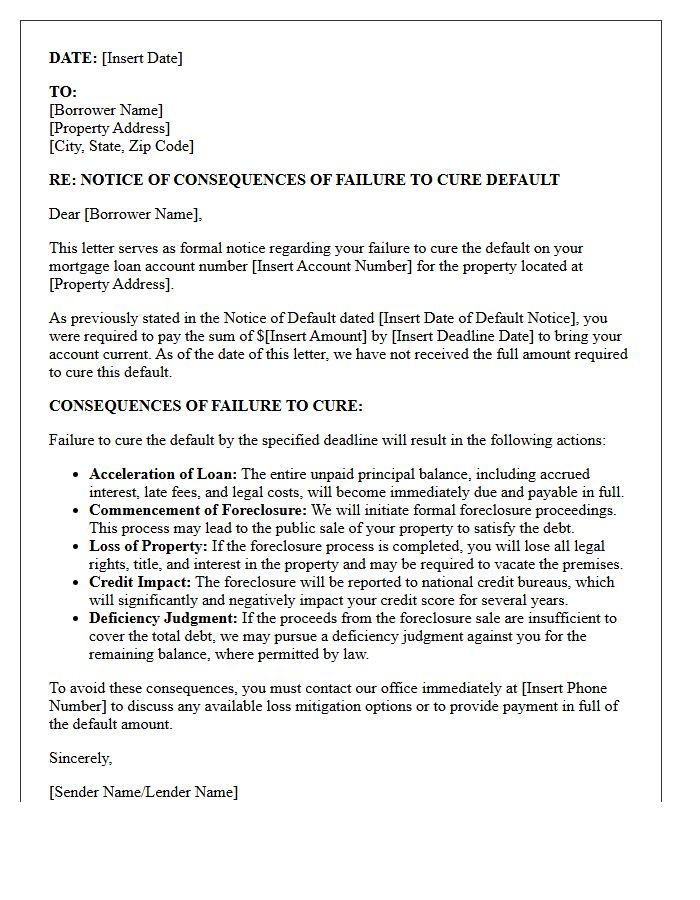

Consequences Of Failure To Cure Including Foreclosure

Failing to remedy a default within the specified grace period triggers severe legal outcomes. The most critical consequence is foreclosure, a process where the lender seizes and sells the property to recover the debt. Additionally, borrowers often face acceleration clauses, making the entire loan balance due immediately. This process results in significant credit score damage, the loss of home equity, and potential deficiency judgments. Timely action is essential to avoid permanent loss of ownership and long-term financial instability caused by a total breach of contract.

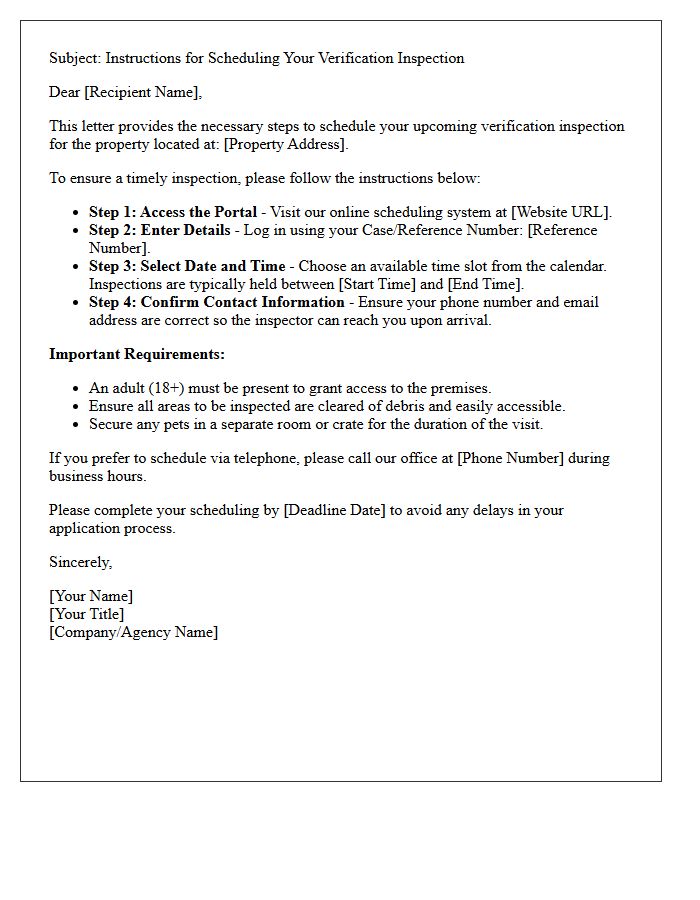

Instructions For Scheduling A Verification Inspection

To ensure a smooth process, always schedule your verification inspection through the official online portal at least forty-eight hours in advance. Confirm that all technical documentation is uploaded and accessible for the inspector's review. Ensure a designated site representative is present to grant entry and answer queries. Double-check that the physical premises are prepared and meet all safety compliance standards before the appointment. Timely scheduling prevents project delays and ensures your certification approval proceeds without administrative interruptions or additional rescheduling fees.

Lender Contact Information For Resolution Inquiry

When addressing loan discrepancies, having accurate lender contact information is essential for a timely resolution inquiry. Borrowers should locate the specific department handling disputes, often listed as "Customer Advocacy" or "Notice of Error" on monthly statements. Using the correct phone number or mailing address ensures your formal request reaches the appropriate compliance officer. Keeping a record of these contact details facilitates clear communication, helps track remediation progress, and protects your consumer rights during the inquiry process. Always verify the official contact channel to avoid delays in resolving account issues.

Authorized Representative Signature And Corporate Title

An Authorized Representative Signature legally binds a business entity to a contract. It is crucial that the individual signing possesses the formal delegated authority to act on the organization's behalf. Including the Corporate Title (such as CEO, President, or Director) serves as vital proof of their leadership role and legal capacity. This specific designation ensures transparency and protects all parties by confirming the agreement is an official corporate act rather than a personal obligation, maintaining the legal validity and enforceability of the signed document.

What is a Notice of Default for Failure to Complete Required Property Repairs?

A Notice of Default for Failure to Complete Required Property Repairs is a formal legal document issued by a lender or property owner notifying a borrower or tenant that they have breached their agreement by failing to maintain the property or complete specific repairs mandated by the contract or local housing codes.

What happens after receiving a Notice of Default for property repairs?

Upon receiving the notice, the recipient enters a "cure period," during which they must complete the specified repairs or provide proof of compliance. Failure to address the repairs within the timeframe stated in the notice can lead to further legal action, such as foreclosure proceedings or lease termination.

Can a lender foreclose if I fail to complete required property repairs?

Yes, most mortgage and deed of trust agreements include "covenant to maintain" clauses. If a homeowner fails to complete necessary repairs that protect the property's value or safety, the lender can declare a default and eventually initiate foreclosure to protect their collateral.

How long do I have to fix repairs listed in a Notice of Default?

The timeframe to complete repairs varies by state law and the specific terms of your contract, but it typically ranges from 30 to 90 days. The exact deadline for compliance will be explicitly stated within the Notice of Default document.

How can I resolve a Notice of Default for property maintenance issues?

To resolve the default, you must complete all repairs listed in the notice, pass a follow-up inspection if required, and provide documentation of the work to the issuing party. If you cannot afford the repairs, you should contact the lender immediately to discuss a workout agreement or seek local home improvement assistance programs.

Comments