Managing delinquent debt requires a formal Notice of Default and Acceleration to protect legal rights. This document notifies the borrower of their breach and demands immediate repayment of the entire loan balance. Understanding this process is essential for effective debt recovery and legal compliance. To help you get started, below are some ready to use templates.

Image cover: Notice of Default and Acceleration: Essential Templates and Legal Guidelines

Letter Samples List

- First Notice of Default and Intent to Accelerate Letter

- Final Demand and Promissory Note Acceleration Letter

- Commercial Mortgage Notice of Default Letter

- Residential Mortgage Loan Acceleration Letter

- Pre-Foreclosure Promissory Note Default Letter

- Breach of Mortgage Contract and Acceleration Letter

- Secured Promissory Note Default Warning Letter

- Notice of Default and Foreclosure Initiation Letter

- Delinquent Mortgage Note Acceleration Demand Letter

- Formal Notice of Acceleration and Payment Demand Letter

- Post-Forbearance Default and Promissory Note Letter

- Notice of Uncured Default and Loan Acceleration Letter

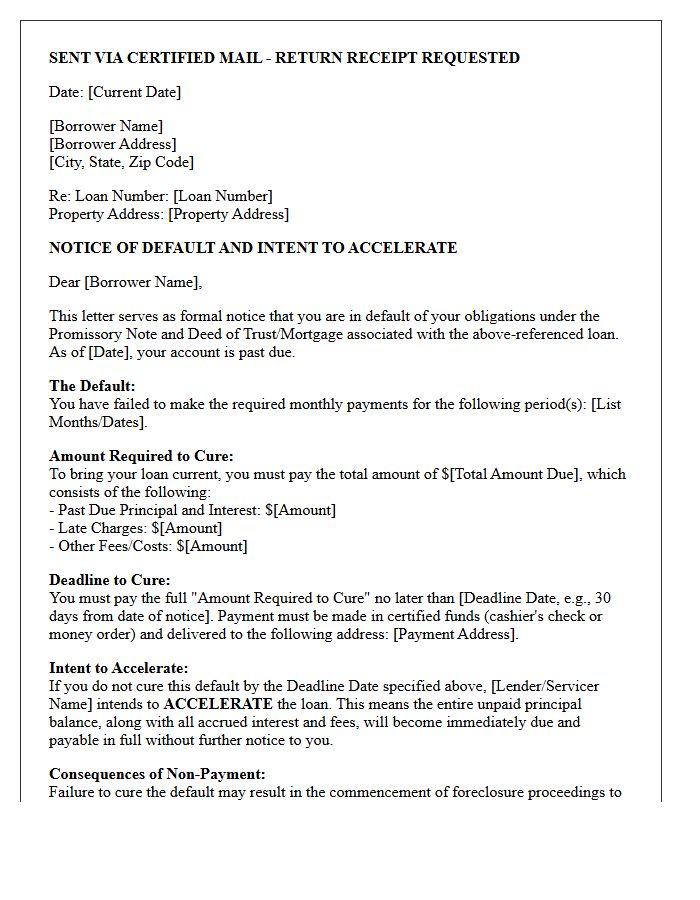

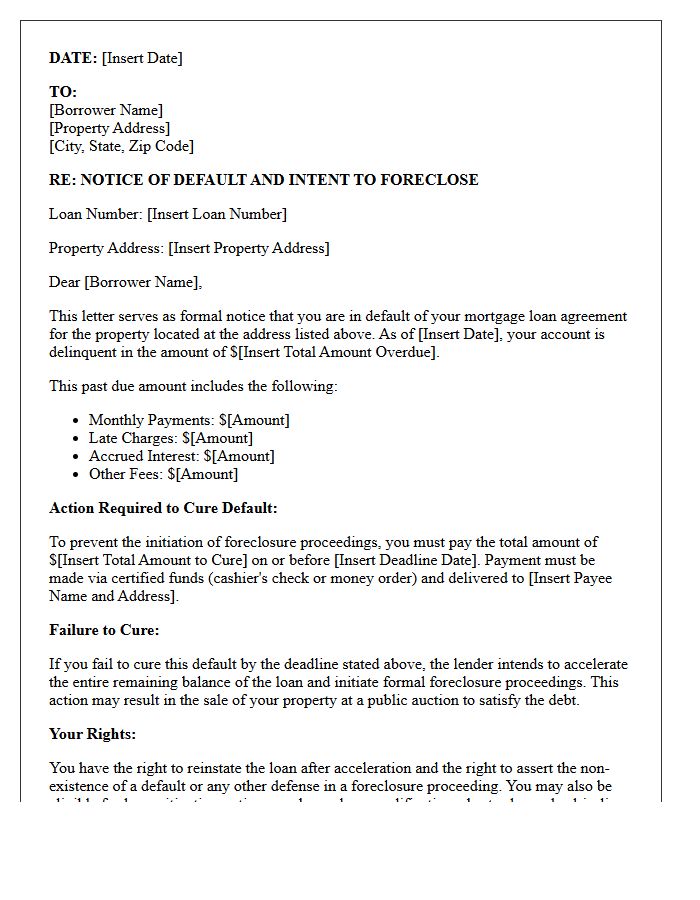

First Notice of Default and Intent to Accelerate Letter

Receiving a First Notice of Default and Intent to Accelerate is a critical warning from a mortgage lender that a borrower has breached their contract through non-payment. This formal letter signifies the start of the foreclosure process, providing a specific deadline to cure the delinquency. If the outstanding balance is not paid by the stated date, the lender will accelerate the loan, demanding the full remaining mortgage balance immediately. It is essential to act quickly by contacting the servicer to discuss loss mitigation options to save the property.

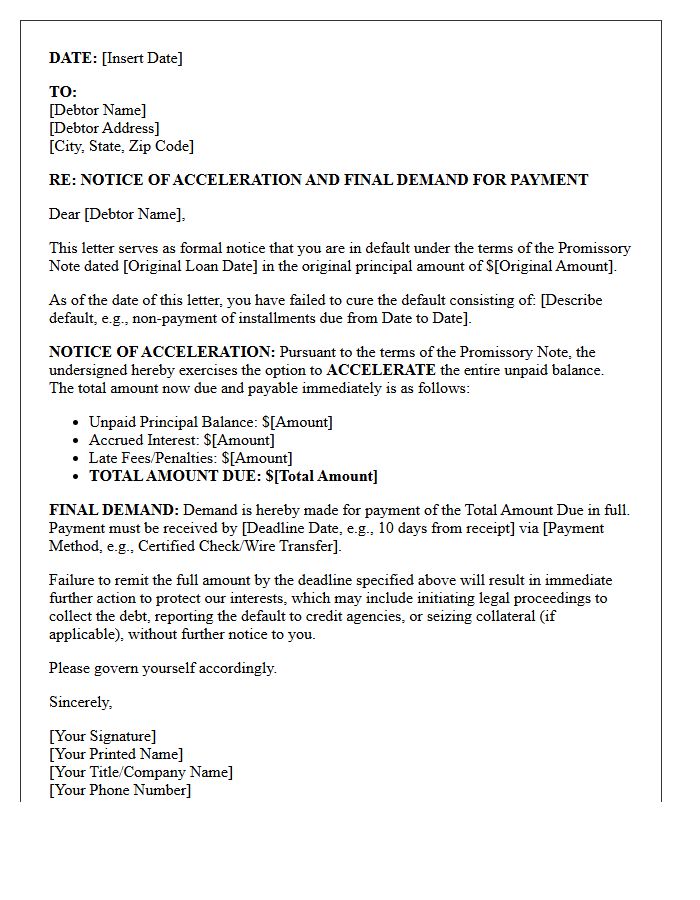

Final Demand and Promissory Note Acceleration Letter

A Final Demand and Promissory Note Acceleration Letter is a formal legal notice sent when a borrower defaults on a loan. It serves as a final warning that the lender is exercising the acceleration clause, making the entire outstanding balance due immediately rather than in installments. Receiving this letter indicates that the grace period has ended and legal action or foreclosure may follow if the full debt is not settled. It is a critical step in debt collection that terminates the original payment schedule and formalizes the legal intent to recover funds.

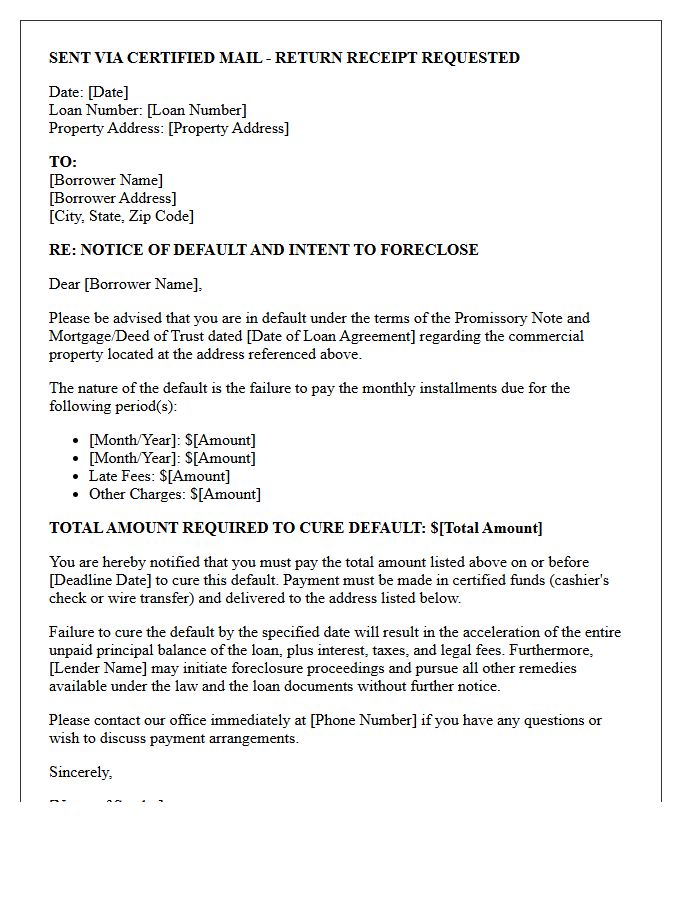

Commercial Mortgage Notice of Default Letter

A Commercial Mortgage Notice of Default is a formal legal alert issued by a lender when a borrower violates loan agreement terms, typically through missed payments. This critical document initiates the foreclosure process and outlines the specific breach, the total amount due, and a strict deadline for resolution. Receiving this letter signifies that the lender may accelerate the debt or seize the property. To protect your investment, it is vital to respond immediately and seek legal counsel to negotiate a workout or loan modification before losing ownership.

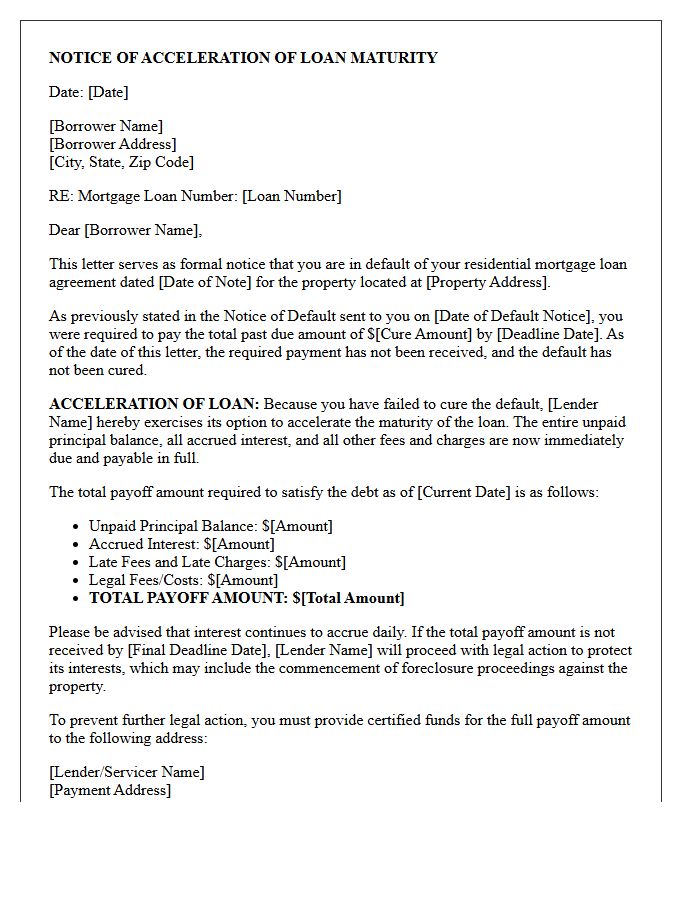

Residential Mortgage Loan Acceleration Letter

A residential mortgage loan acceleration letter is a formal legal notice issued by a lender when a borrower defaults on payments. This document warns that the entire remaining loan balance is now due immediately, effectively terminating the installment agreement. It serves as the final step before the lender initiates foreclosure proceedings. Borrowers must typically pay the full delinquent amount, including late fees and interest, within a specific timeframe to reinstate the loan and prevent the loss of their home. Seeking legal counsel or credit counseling immediately is critical upon receipt.

Pre-Foreclosure Promissory Note Default Letter

A Pre-Foreclosure Promissory Note Default Letter serves as a formal notice that a borrower has breached their loan agreement. This critical document warns that the lender intends to accelerate the debt if the arrears are not paid within a specific timeframe. It outlines the total amount due, late fees, and the deadline to cure the default. Receiving this notice is the final opportunity for homeowners to negotiate a loan modification or repayment plan to prevent the official foreclosure process from beginning against the property.

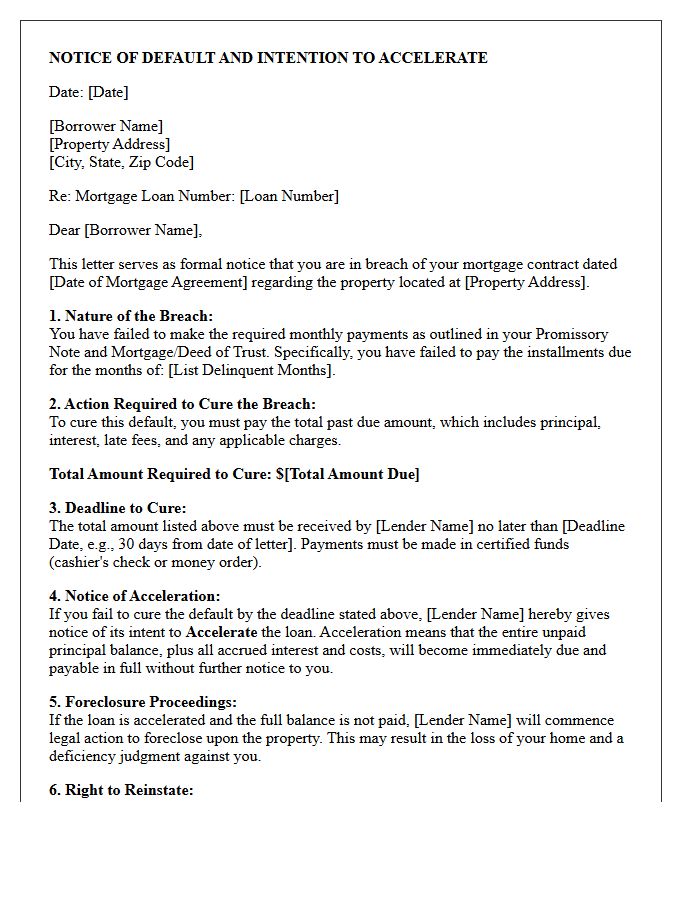

Breach of Mortgage Contract and Acceleration Letter

A breach of mortgage contract occurs when a borrower fails to meet legal obligations, typically through missed payments. This default triggers the lender's right to issue an acceleration letter. This formal notice demands immediate repayment of the entire remaining loan balance. Failure to resolve the delinquency or pay the full amount by the specified deadline usually leads to foreclosure. Understanding these terms is crucial for homeowners to protect their property rights and explore loss mitigation options before legal action intensifies.

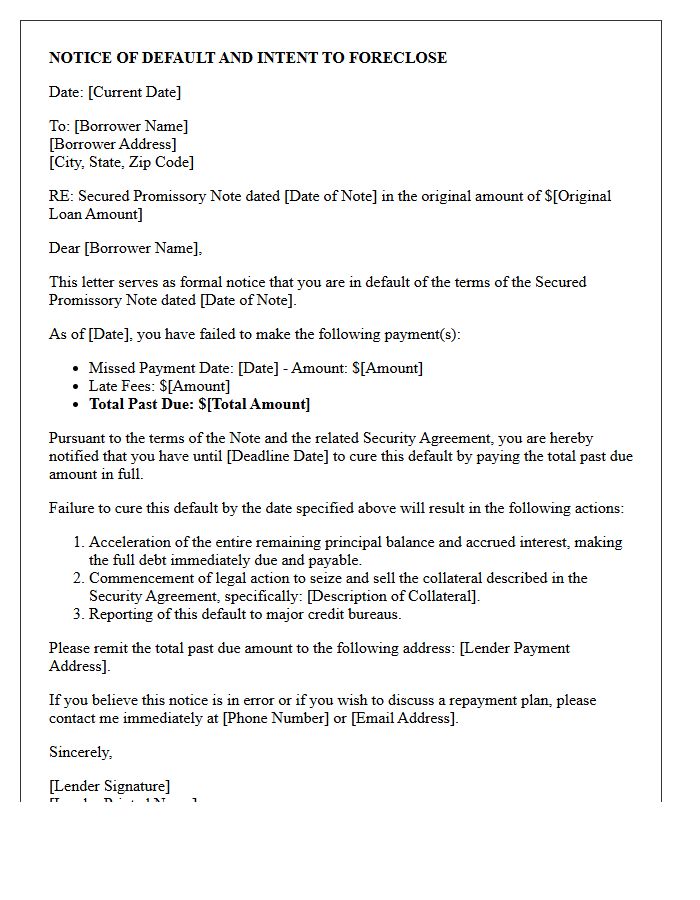

Secured Promissory Note Default Warning Letter

A Secured Promissory Note Default Warning Letter is a formal notice sent to a borrower who has missed payments. This legal document serves as a final demand for cure before the lender initiates foreclosure or seizes the underlying collateral. It must clearly outline the breach of contract, the specific amount overdue, and the deadline for rectification. Failure to respond to this warning typically triggers acceleration of the total debt, making the entire balance due immediately and potentially leading to legal action to recover the secured assets.

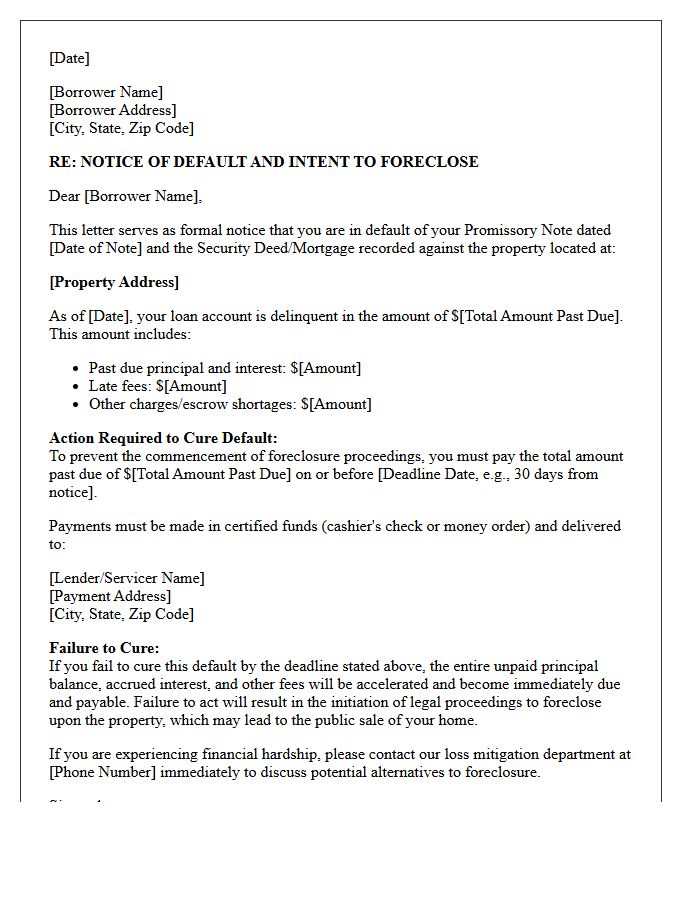

Notice of Default and Foreclosure Initiation Letter

A Notice of Default is a formal legal document signaling that a borrower has failed to make timely mortgage payments, officially marking the foreclosure initiation. This letter serves as a final warning, detailing the total amount owed to bring the loan current. Failure to resolve the delinquency within the specified grace period allows the lender to accelerate the debt and auction the property. It is crucial to act immediately by contacting your loan servicer to explore loss mitigation options or legal defenses to prevent permanent loss of your home.

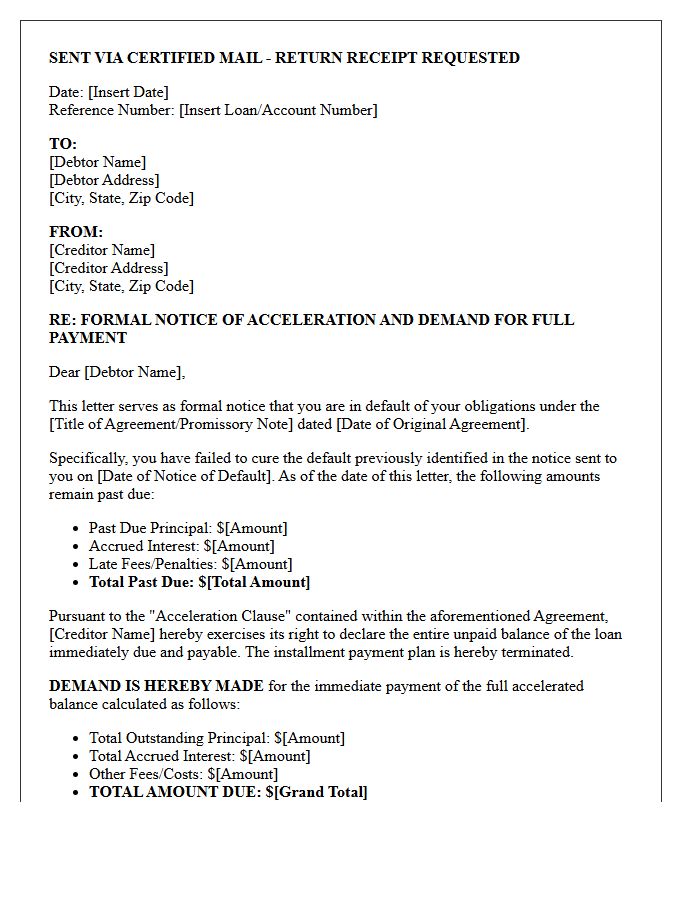

Delinquent Mortgage Note Acceleration Demand Letter

A Delinquent Mortgage Note Acceleration Demand Letter is a formal legal notice issued by a lender when a borrower defaults on payments. This critical document warns that unless the outstanding arrears are paid within a specific timeframe, the lender will "accelerate" the loan. Acceleration makes the entire unpaid principal balance due immediately, rather than just the missed installments. Receiving this letter is the final step before a lender initiates formal foreclosure proceedings. It serves as a last opportunity for the borrower to cure the default and reinstate the original loan terms.

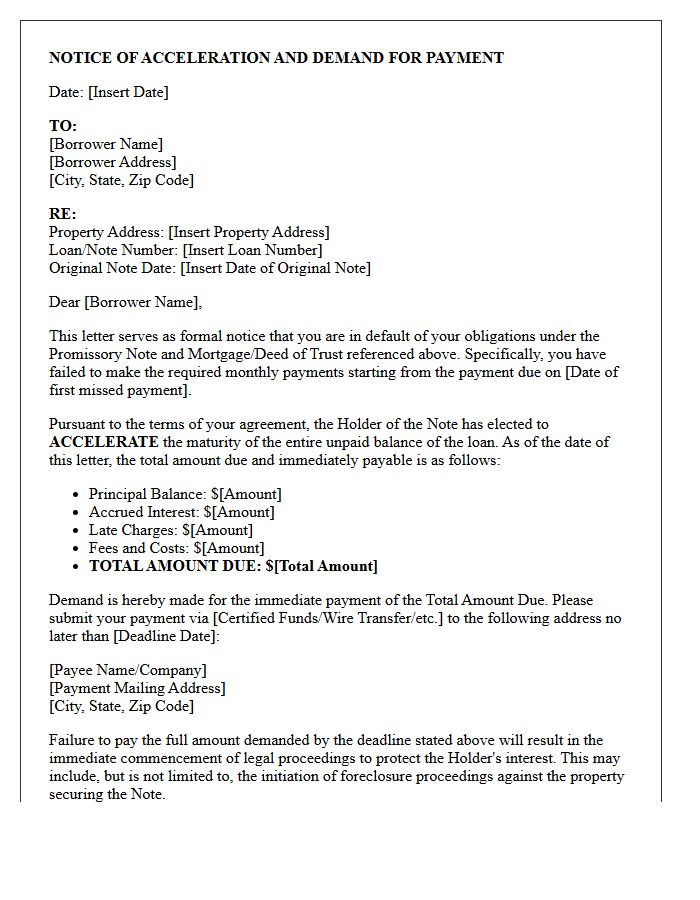

Formal Notice of Acceleration and Payment Demand Letter

A formal notice of acceleration is a critical legal document issued when a borrower defaults on a loan. It signifies that the entire loan balance is now due immediately, rather than in scheduled installments. This letter serves as a final payment demand before the lender initiates foreclosure or legal action. Receiving this notice means the grace period has ended, and the creditor is exercising their right to "accelerate" the debt. To prevent the loss of collateral, the recipient must pay the full amount or negotiate an immediate settlement to avoid litigation.

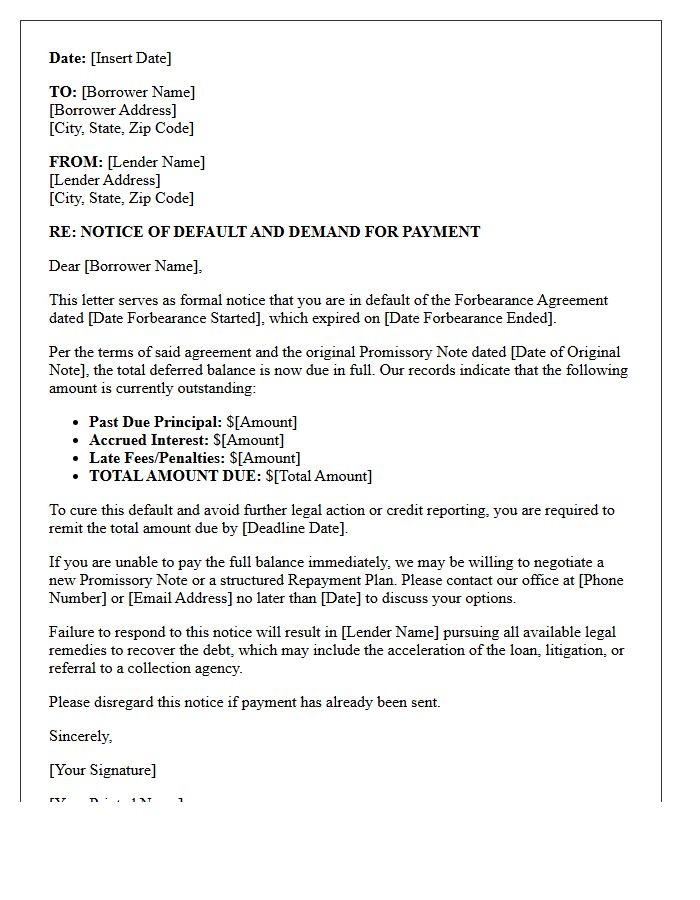

Post-Forbearance Default and Promissory Note Letter

A post-forbearance default occurs when a borrower fails to resume payments or meet repayment terms after a temporary pause. Upon default, the lender typically issues a promissory note letter, which serves as a formal legal notice. This document outlines the total debt owed, including missed payments and interest. It is a critical step before foreclosure, signifying that the original loan terms are being enforced. Borrowers must review this letter immediately to understand their remaining reinstatement options or potential legal consequences regarding their property and credit standing.

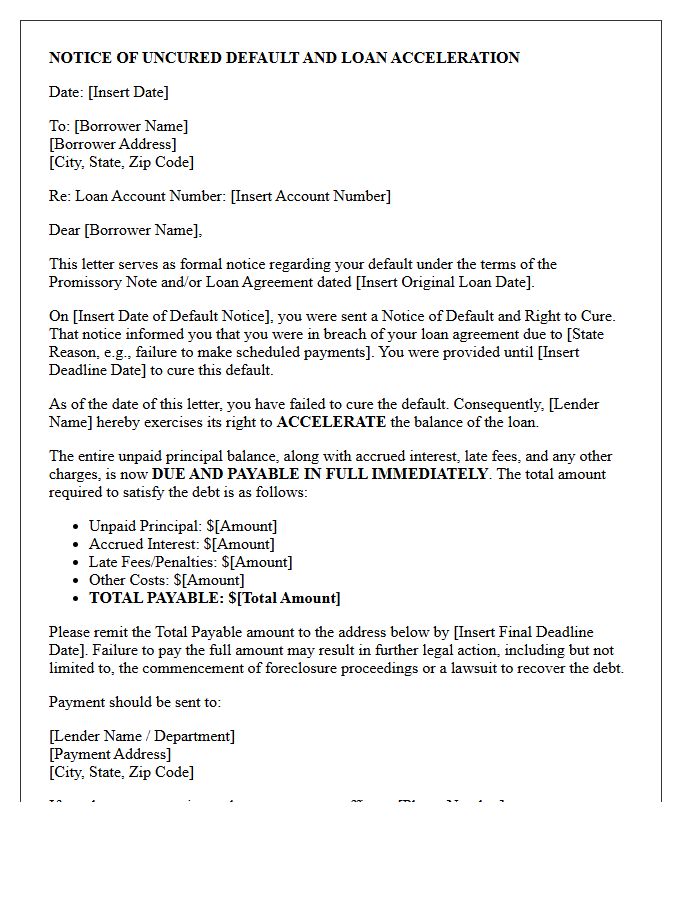

Notice of Uncured Default and Loan Acceleration Letter

A Notice of Uncured Default and Loan Acceleration Letter is a formal legal warning issued by a lender when a borrower fails to resolve missed payments. This document signifies that the grace period has expired, officially triggering loan acceleration. Once accelerated, the entire remaining balance becomes due immediately, rather than just the overdue installments. Receiving this notice is the final step before the lender initiates foreclosure or legal repossession. Borrowers must act urgently to negotiate a settlement or face the loss of their collateral and severe credit damage.

What is a Notice of Default and Acceleration of Promissory Note?

A Notice of Default and Acceleration is a formal legal document issued by a lender notifying a borrower that they have breached the terms of a promissory note and that the entire remaining balance of the loan is now due immediately.

What triggers the acceleration clause in a promissory note?

The acceleration clause is typically triggered by a specific event of default, most commonly the failure to make scheduled payments, but it can also be activated by a breach of other loan covenants such as failing to maintain insurance or transferring property title without consent.

Can a borrower stop the acceleration process after receiving a notice?

A borrower may be able to stop the acceleration by exercising "cure rights," which involves paying all past-due amounts, late fees, and legal costs within the specific grace period defined in the original promissory note or required by state law.

What is the difference between a Notice of Default and a Notice of Acceleration?

A Notice of Default informs the borrower of the specific breach and provides a deadline to remedy it, whereas a Notice of Acceleration confirms that the deadline has passed and the lender has called the full debt amount due, effectively ending the installment payment plan.

What are the legal consequences of ignoring a Notice of Default and Acceleration?

Ignoring these notices typically leads to the commencement of foreclosure proceedings or a collection lawsuit, which can result in the loss of collateral, a significant decrease in credit score, and a legal judgment for the full outstanding balance plus attorney fees.

Comments