Receive a Commercial Mortgage Notice of Default indicates a serious breach of your loan agreement. This formal warning often accompanies a Rent Assignment Demand, allowing lenders to collect tenant payments directly to satisfy debts. Understanding your legal rights and obligations is essential to protecting your property investment during financial distress. Below are some ready to use templates.

Image cover: Mastering Commercial Mortgage Default Notices and Rent Assignment Demands: Templates and Best Practices

Letter Samples List

- Letter Sender and Mortgage Lender Information

- Letter Date of Issuance

- Letter Recipient and Borrower Information

- Notice of Default Letter Subject Line

- Commercial Loan and Mortgage Agreement Reference

- Specific Event of Default Description

- Outstanding Mortgage Debt Declaration

- Demand for Immediate Assignment of Rents

- Commercial Tenant Rent Redirection Instructions

- Potential Foreclosure and Legal Action Warning

- Lender Legal Department Contact Information

- Formal Letter Signature Block

- Letter Exhibits and Loan Document Attachments

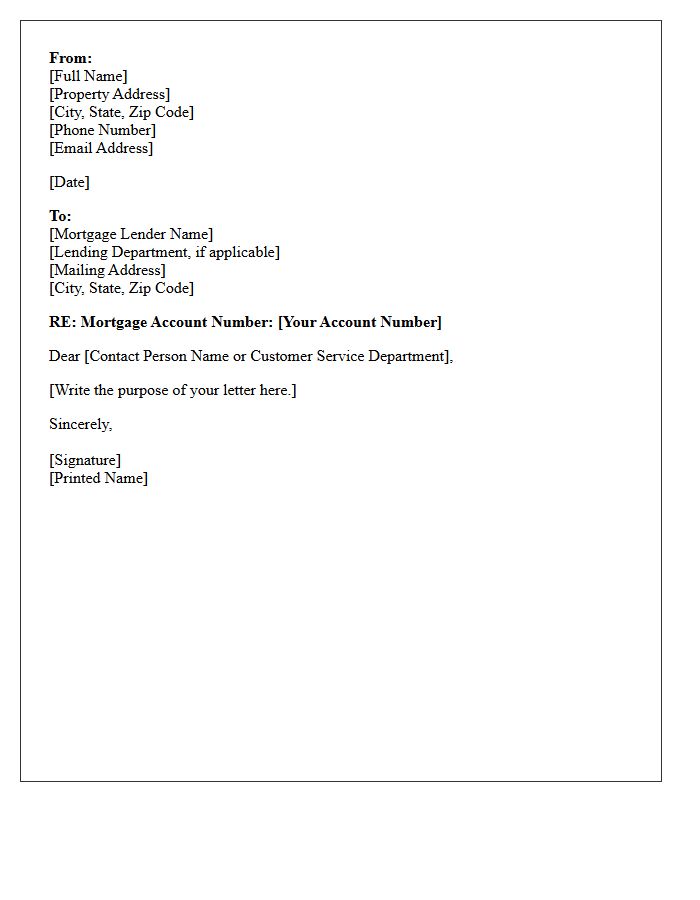

Letter Sender and Mortgage Lender Information

Accurate Letter Sender and Mortgage Lender Information is critical for verifying the legitimacy of financial correspondence. Always confirm the sender's identity to prevent phishing scams and ensure your payments reach the correct institution. Key details include the lender's registered name, official address, and NMLS ID. Understanding these identifiers helps homeowners maintain secure communication, track loan servicing changes, and protect personal data during mortgage management. Verifying these details ensures that all legal notices regarding your home loan are authentic and come from a trusted source.

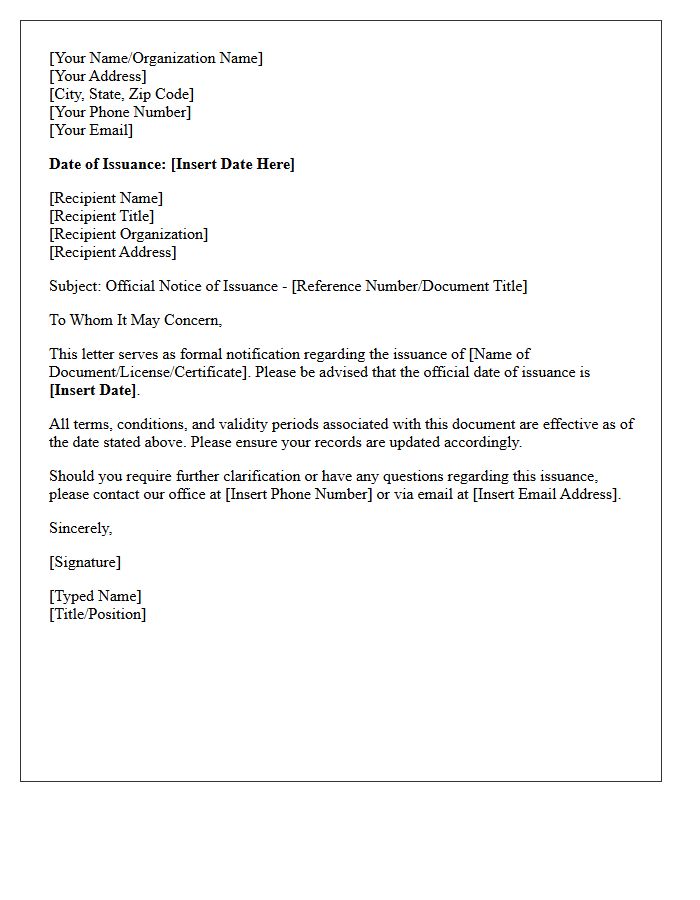

Letter Date of Issuance

The Letter Date of Issuance is the formal calendar date when a document is officially created and released. This legal reference point is critical for tracking deadlines, calculating expiration periods, and establishing the exact timeline for contractual obligations. In administrative and financial sectors, this date serves as the primary marker for validity and ensures all parties recognize the official commencement of the notice. It acts as the definitive benchmark for compliance and time-sensitive responses in professional correspondence.

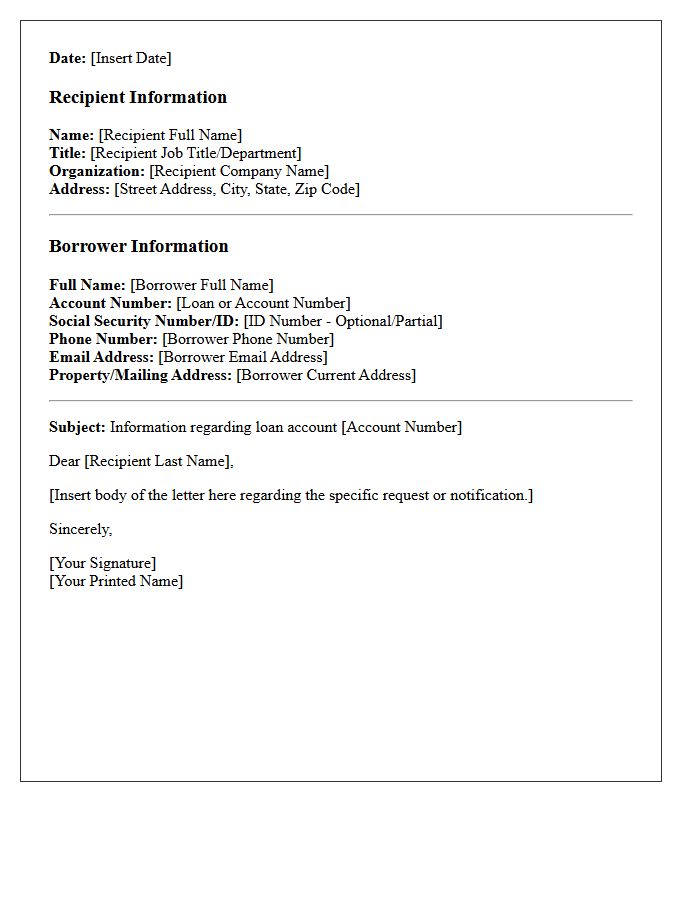

Letter Recipient and Borrower Information

Accurate borrower information is essential for legal compliance and effective communication. The letter recipient must be clearly identified with their full legal name and current mailing address to ensure documents reach the correct party. This verification prevents identity fraud and ensures that loan obligations are properly assigned. Precise data management facilitates seamless updates regarding repayment terms, interest rates, and regulatory disclosures. Maintaining up-to-date records minimizes delivery errors, protects sensitive financial data, and strengthens the formal relationship between the lending institution and the individual borrower.

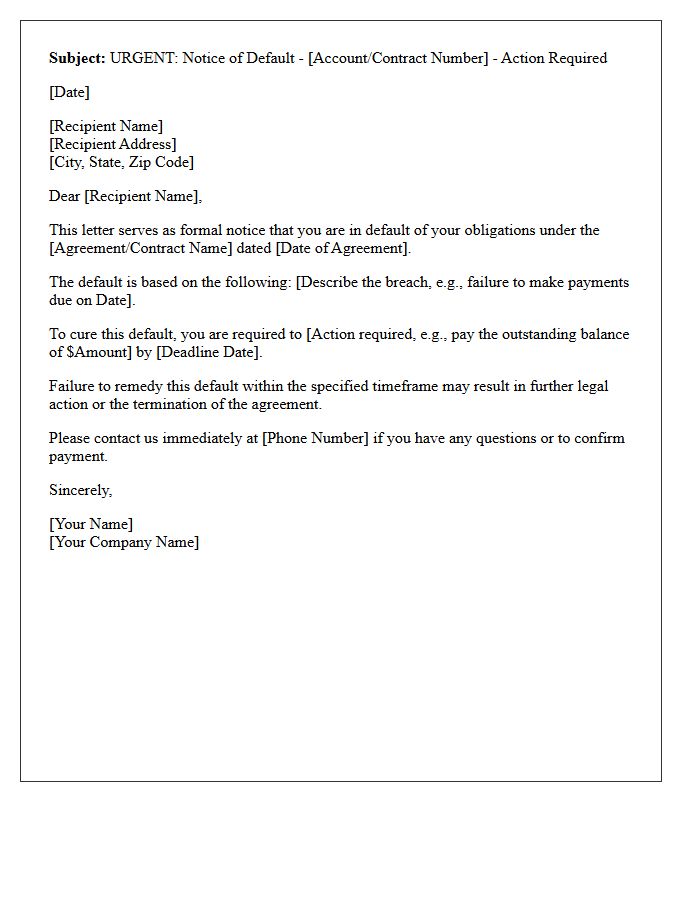

Notice of Default Letter Subject Line

A Notice of Default letter subject line must be clear, urgent, and legally compliant to ensure the recipient understands the severity of the situation. It typically includes the property address and the formal intent to accelerate the foreclosure process if the delinquency is not resolved. Providing the specific loan number helps the borrower identify the account immediately. An effective subject line acts as a critical legal warning, prompting the homeowner to take immediate action or contact the lender to discuss loss mitigation options and avoid permanent loss of their property.

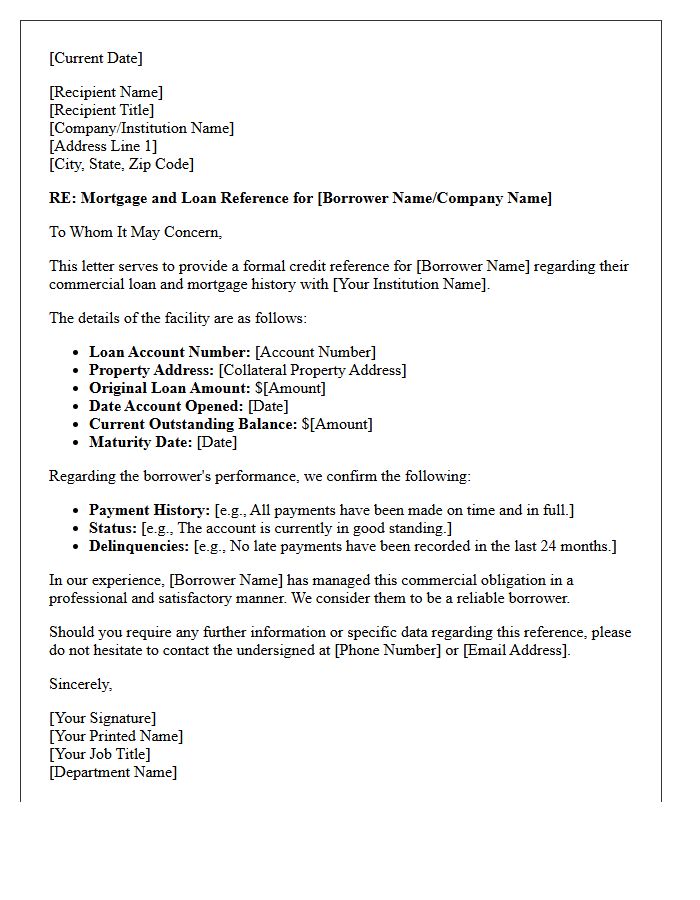

Commercial Loan and Mortgage Agreement Reference

A Commercial Loan and Mortgage Agreement Reference is a critical legal framework governing debt financing for business properties. It outlines the security interest granted to lenders, detailing repayment terms, interest rates, and covenants that borrowers must maintain. This document serves as the primary evidence of the lien placed against the real estate collateral. Understanding these references ensures compliance with financial obligations, protects ownership rights, and defines the specific remedies available to creditors in the event of a default or breach of contract.

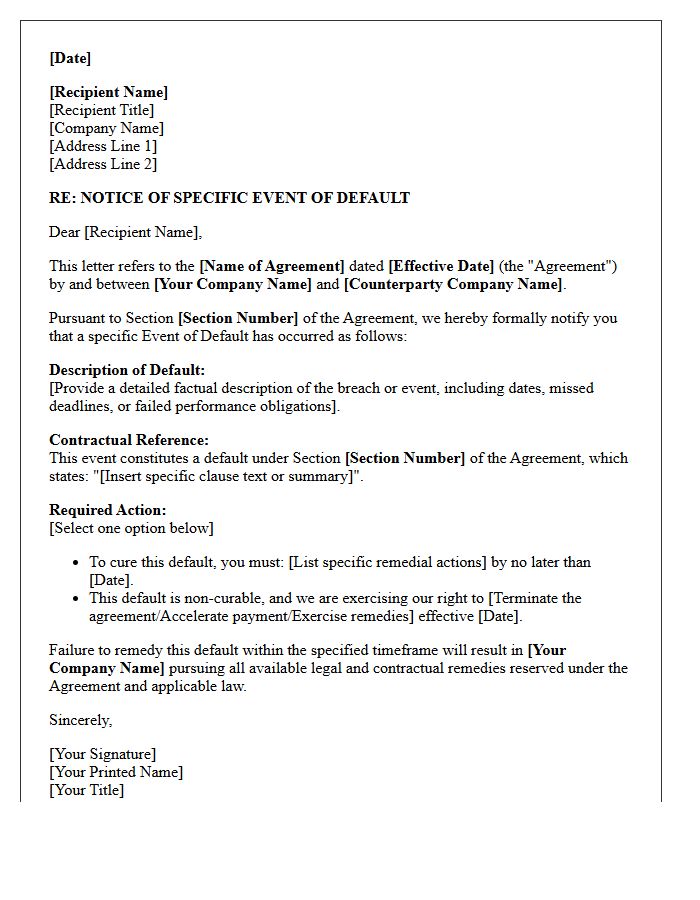

Specific Event of Default Description

A Specific Event of Default refers to a clearly defined breach within a legal agreement that allows a lender to demand immediate repayment. Common triggers include missed payments, insolvency, or a covenant violation. It is critical to monitor these provisions because they can cause a loan acceleration, resulting in total debt becoming due instantly. Understanding the exact cure periods and notification requirements is essential for maintaining compliance and preventing foreclosure or legal action against the borrower. Always review the specific definitions to mitigate financial and operational risks.

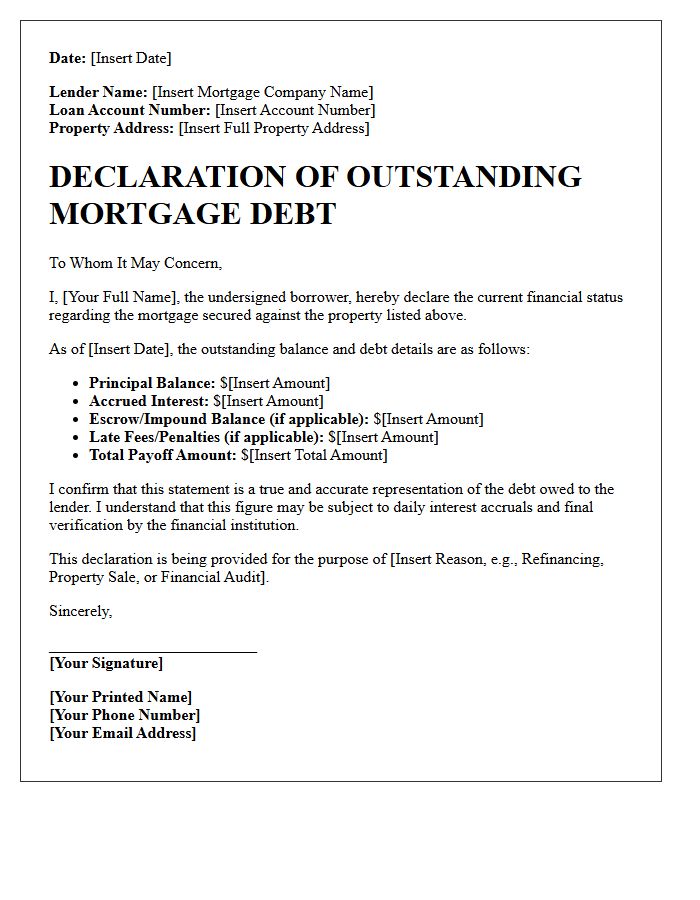

Outstanding Mortgage Debt Declaration

An Outstanding Mortgage Debt Declaration is a formal document verifying the remaining balance on a home loan. Lenders and tax authorities require this statement to confirm precise financial liabilities during property transfers, refinancing, or estate settlements. It serves as legal proof of the principal amount and accrued interest owed at a specific date. Accurate reporting is essential for calculating net equity and ensuring compliance with debt disclosure regulations. Always verify that the figures match your most recent amortization schedule to avoid processing delays or legal discrepancies during asset valuation.

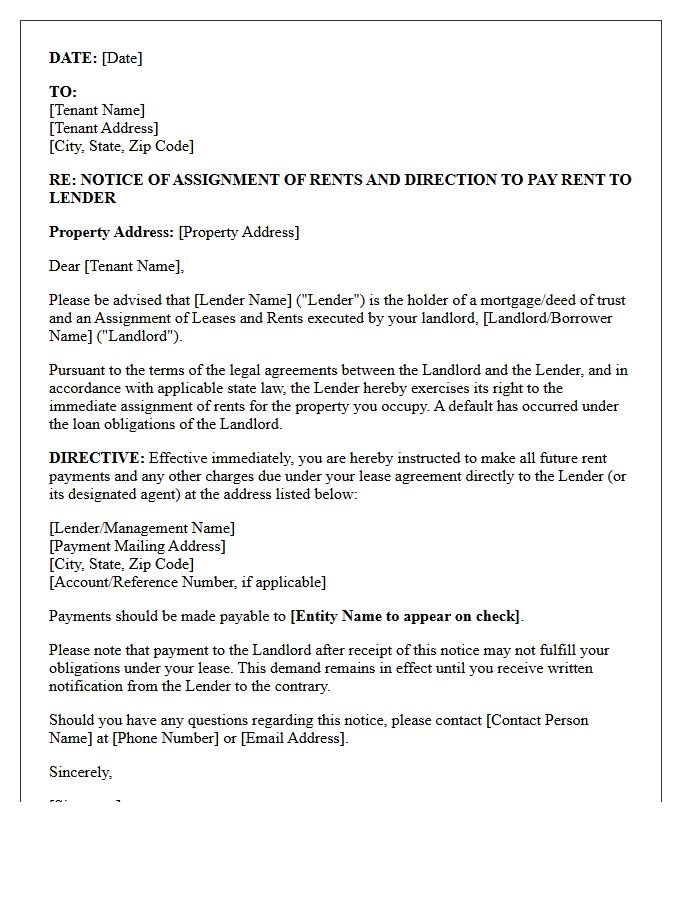

Demand for Immediate Assignment of Rents

A Demand for Immediate Assignment of Rents is a powerful legal remedy used by lenders during a mortgage default. It allows a creditor to bypass the property owner and directly collect rental income from tenants to cover outstanding debt. This mechanism provides immediate cash flow for the lender before a formal foreclosure completes. For tenants, receiving this notice means they must redirect their lease payments to the lender to avoid legal liability. It serves as a critical security interest protection, ensuring property revenue is preserved for loan repayment rather than being diverted by the borrower.

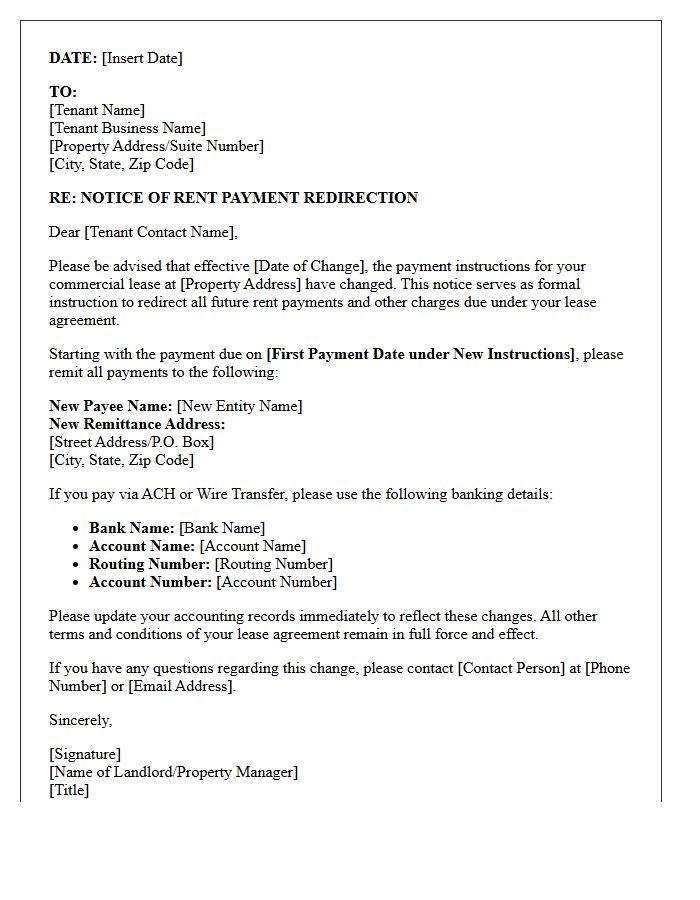

Commercial Tenant Rent Redirection Instructions

When dealing with Commercial Tenant Rent Redirection Instructions, tenants must verify any changes via independent verification to prevent fraud. Always confirm new payment details through a known contact person using a trusted phone number before transferring funds. Fraudulent redirection requests often mimic official correspondence to intercept lease payments. Scrutinize the sender's email address and look for official documentation or formal amendments to the lease agreement. Promptly notifying the property manager of suspicious requests ensures financial security and maintains compliance with contractual obligations under the existing tenancy arrangement.

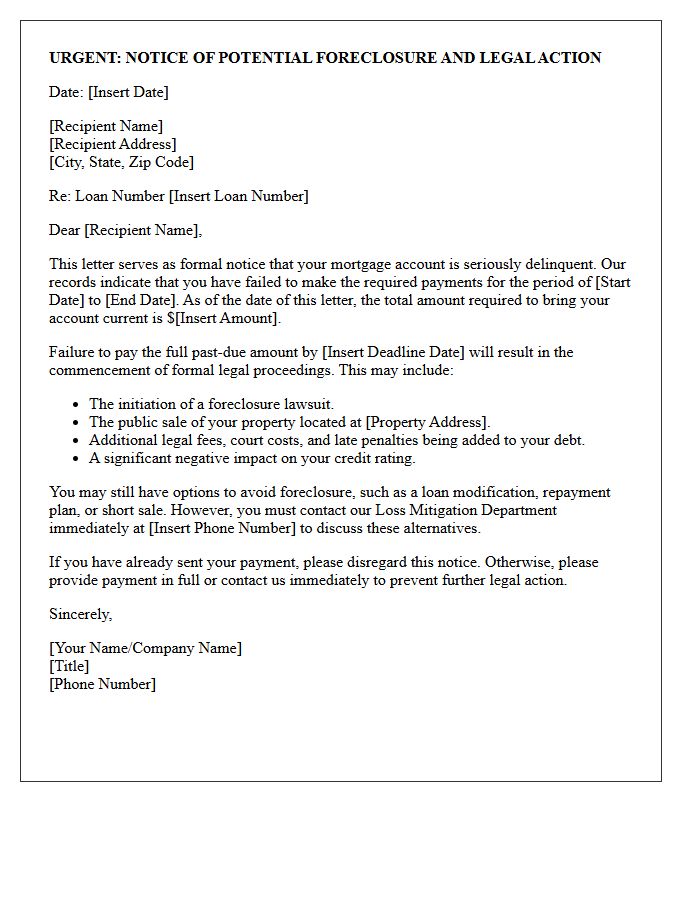

Potential Foreclosure and Legal Action Warning

A foreclosure occurs when a lender initiates legal action to seize a property after a borrower defaults on mortgage payments. Receiving a Notice of Default is a critical warning that requires immediate attention to avoid losing your home. Legal proceedings can lead to an auction, severely damaging your credit score. To prevent eviction, homeowners should explore loss mitigation options, such as loan modifications or short sales, and consult with legal counsel. Timely communication with your lender is the most vital step to resolving delinquency and stopping potential litigation before the final judgment.

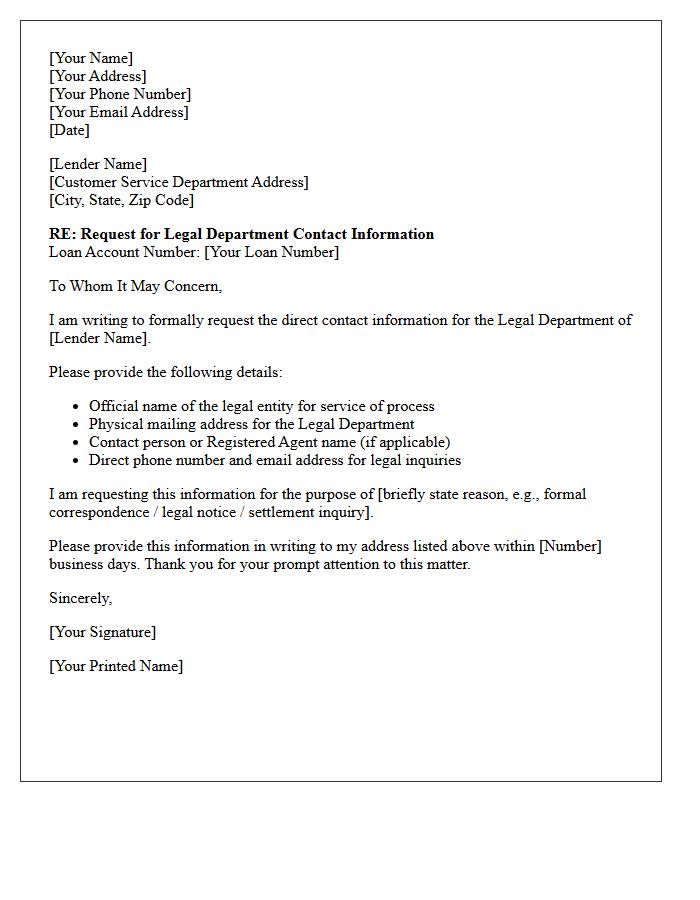

Lender Legal Department Contact Information

Obtaining the Lender Legal Department Contact Information is vital for formal notices, litigation, or complex subordination agreements. Unlike standard customer service, this department handles service of process and legal inquiries. Accessing this specific data ensures documents reach the correct statutory agent or legal counsel, preventing procedural delays. Most financial institutions list their registered agent for service through the Secretary of State database rather than public websites. Always verify the precise mailing address for legal correspondence to guarantee compliance with contractual obligations and statutory requirements.

Formal Letter Signature Block

A formal letter signature block is essential for professional closure. It typically includes a complimentary close like "Sincerely," followed by four blank lines for a handwritten signature. Below this, type your full name and current job title to ensure clarity. If you are sending a digital document, you may insert an image of your signature. Including contact information such as a phone number or email address directly under your name is a standard practice that helps the recipient respond efficiently while maintaining a polished, authoritative appearance.

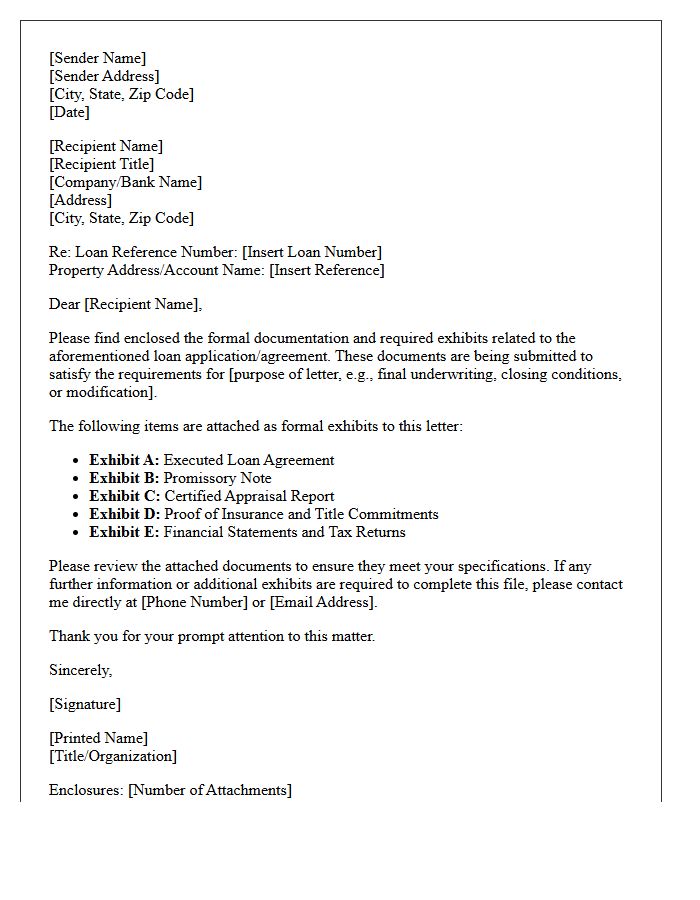

Letter Exhibits and Loan Document Attachments

When finalizing credit agreements, Letter Exhibits serve as essential templates for future notifications, such as borrowing requests or compliance certificates. These documents must be accurately completed to ensure legal enforceability and operational clarity. Proper management of Loan Document Attachments is critical during closing to prevent funding delays. Parties should meticulously verify that all schedules and exhibits are current, as these attachments define the specific financial terms, collateral details, and repayment obligations governing the entire lending relationship between the borrower and the financial institution.

What is a Commercial Mortgage Notice of Default?

A Commercial Mortgage Notice of Default (NOD) is a formal legal notification sent by a lender to a borrower stating that the loan terms have been breached, typically due to missed payments. This document serves as the official start of the foreclosure process and outlines the specific default, the amount required to cure the debt, and the deadline for payment.

What does an Assignment of Rents demand mean for a commercial landlord?

An Assignment of Rents demand is a legal mechanism that allows a lender to collect rental income directly from a commercial property's tenants when the borrower defaults. Once the demand is triggered and notice is served to tenants, the landlord loses the right to collect or use those rent payments until the default is resolved or the loan is reinstated.

How does a Notice of Default affect existing commercial tenants?

While a Notice of Default is primarily between the lender and the borrower, it may trigger an Assignment of Rents where tenants are legally required to redirect their monthly rent payments to the lender or a court-appointed receiver. Tenants are typically protected by Subordination, Non-Disturbance, and Attornment (SNDA) agreements, which allow them to remain in the space despite the landlord's financial distress.

Can a borrower stop an Assignment of Rents demand after a default?

A borrower can typically stop an Assignment of Rents demand by "curing" the default, which involves paying all past-due amounts, late fees, and legal costs within the timeframe specified in the Notice of Default. Additionally, borrowers may seek a forbearance agreement or a loan modification to restructure payments and regain control of the property's cash flow.

What is the difference between an Absolute Assignment and a Collateral Assignment of Rents?

An Absolute Assignment transfers the right to rent payments to the lender immediately upon the execution of the loan, though the lender stays passive until a default occurs. A Collateral Assignment serves as additional security for the loan, where the lender's right to the rent only "activates" as a lien once a Notice of Default has been recorded and a formal demand has been issued.

Comments