Receiving a Veterans Affairs Loan Notice of Default and Intention to Foreclose is a serious matter indicating your mortgage is significantly past due. This formal legal warning marks the beginning of the foreclosure process, but options like loan modification or VA assistance are still available to help save your home. To assist your communication with lenders, below are some ready to use templates.

Image cover: VA Notice of Default and Intent to Foreclose: Essential Templates and Guides for Veterans

Letter Samples List

- Veterans Affairs Loan Notice of Default and Intention to Foreclose Letter

- Letter of Intention to Foreclose and Notice of Default for Veterans Affairs Loan

- Veterans Affairs Mortgage Notice of Default and Foreclosure Intention Letter

- Notice of Default and Intention to Foreclose on Veterans Affairs Loan Letter

- VA Loan Default Notice and Intention to Foreclose Letter

- Letter of Default Notice and Foreclosure Intention for Veterans Affairs Mortgage

- Veterans Affairs Home Loan Notice of Default and Foreclosure Intention Letter

- Intention to Foreclose and Notice of Default Letter for VA Loan

- Veterans Affairs Loan Pre-Foreclosure Default Notice Letter

- Official Letter of Notice of Default and Intention to Foreclose for Veterans Affairs Loan

- Veterans Affairs Residential Loan Default and Foreclosure Intention Letter

- Letter Regarding Notice of Default and Intention to Foreclose on VA Loan

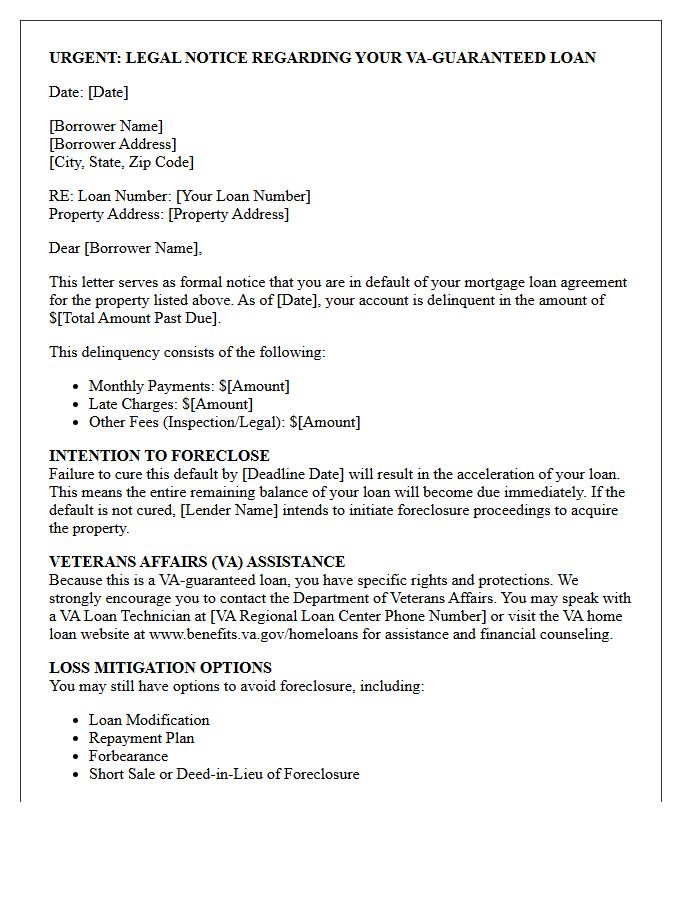

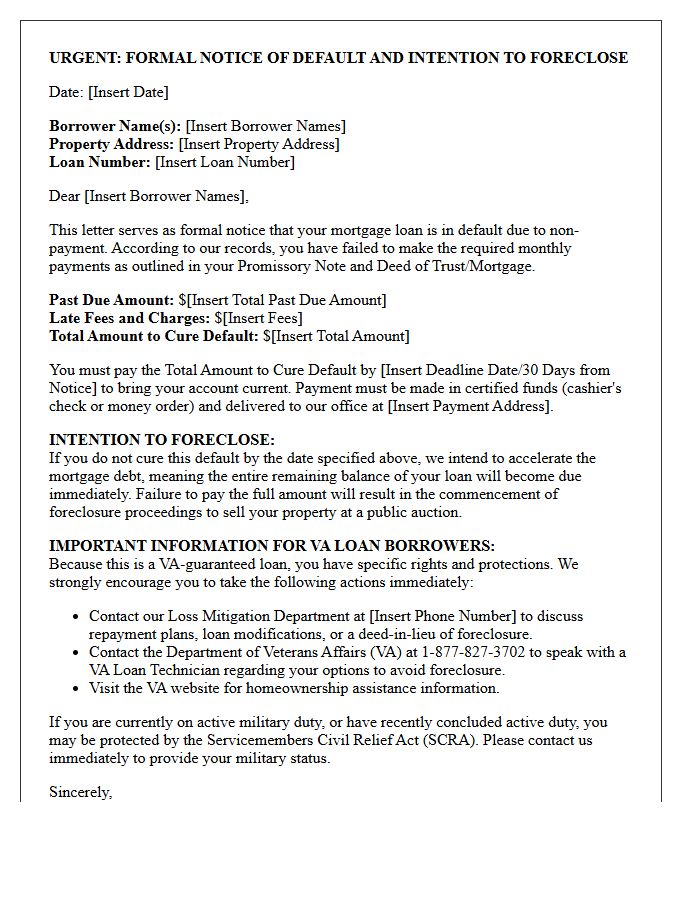

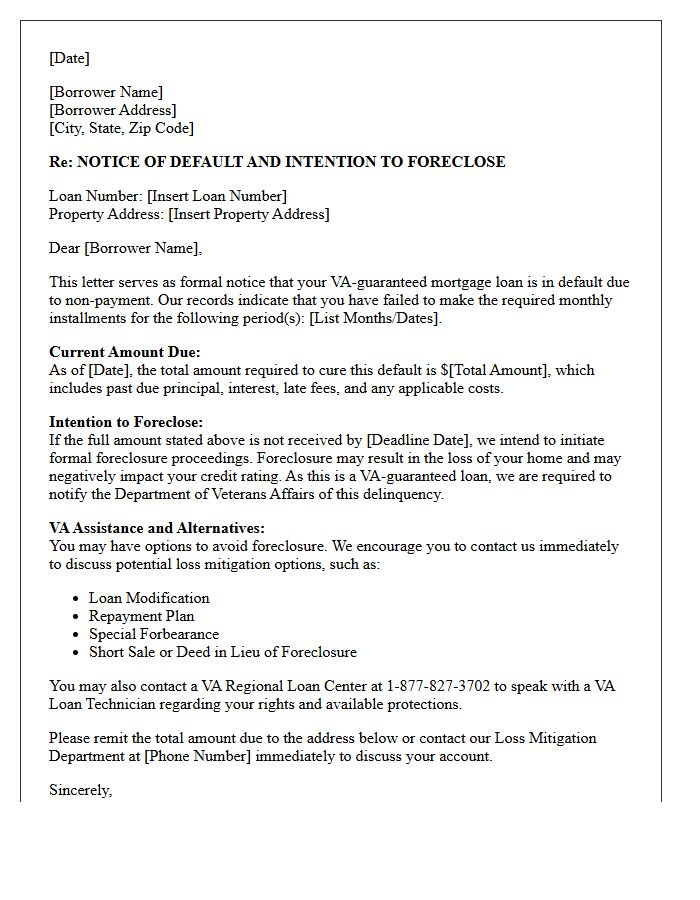

Veterans Affairs Loan Notice of Default and Intention to Foreclose Letter

Receiving a VA Loan Notice of Default is a formal warning that your mortgage is significantly delinquent. This legal document signifies the servicer's intention to foreclose unless the outstanding debt is resolved. It is crucial to contact your loan servicer immediately to explore loss mitigation options. Additionally, the Department of Veterans Affairs provides specialized financial counseling to help veterans avoid home loss. Acting quickly during this grace period can help you negotiate a repayment plan, loan modification, or partial claim to keep your home and protect your credit score.

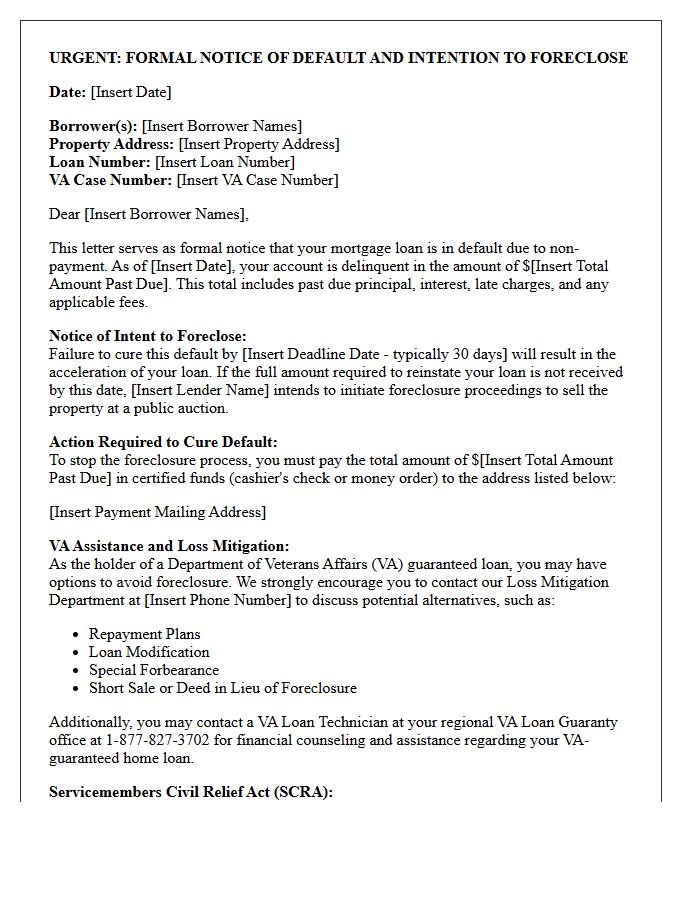

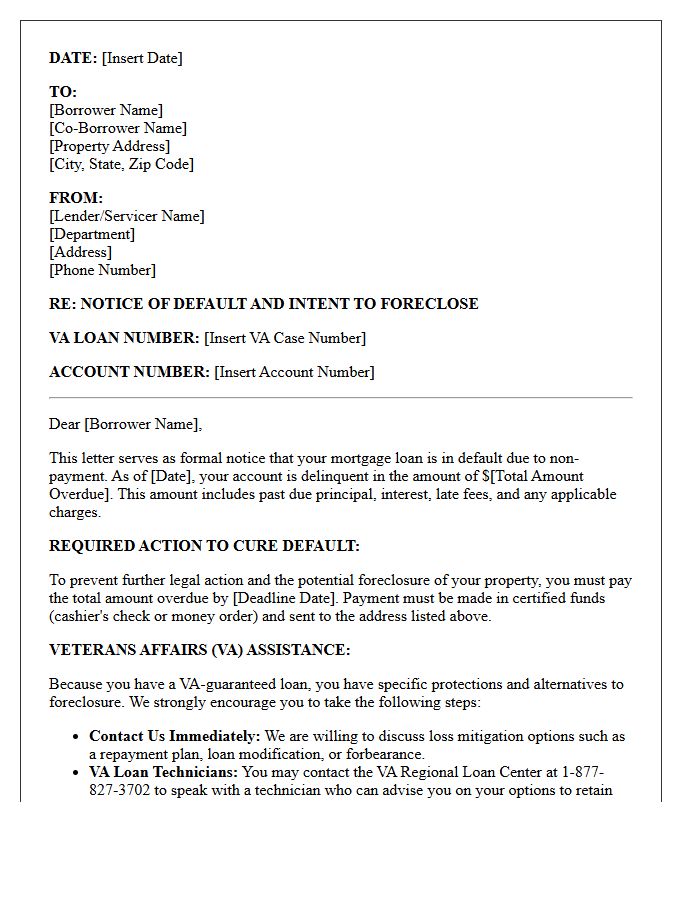

Letter of Intention to Foreclose and Notice of Default for Veterans Affairs Loan

For veterans with a VA-backed loan, receiving a Notice of Default is a critical legal warning that mortgage payments are past due. Before a foreclosure sale, lenders must issue a Letter of Intention to Foreclose, providing at least 30 days' notice. Importantly, the Department of Veterans Affairs offers dedicated foreclosure avoidance assistance. Veterans should immediately contact their loan servicer or a VA technician to explore loss mitigation options, such as repayment plans or loan modifications, designed specifically to protect military homeowners from losing their property.

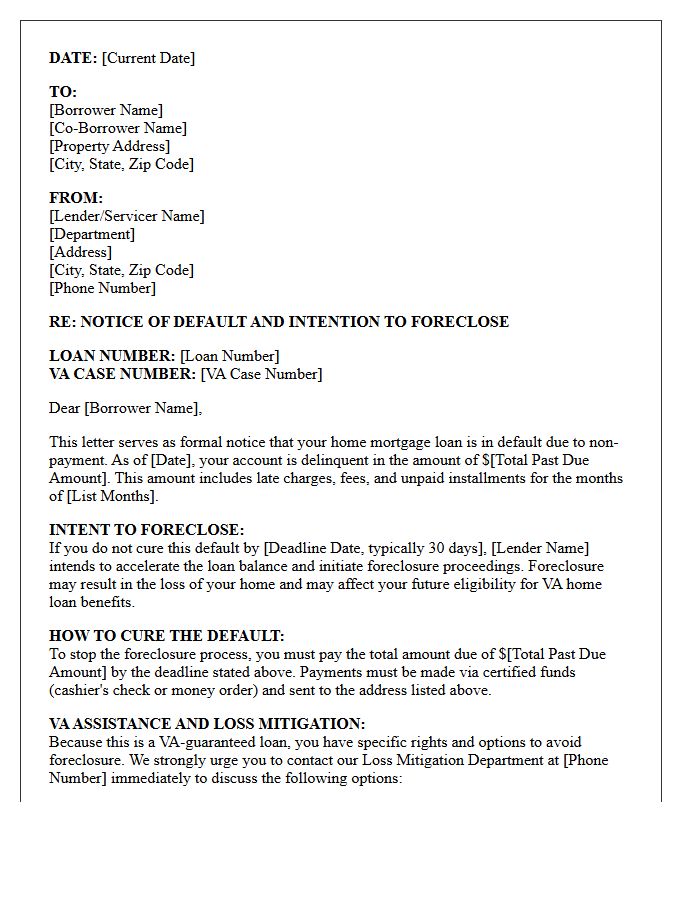

Veterans Affairs Mortgage Notice of Default and Foreclosure Intention Letter

A Veterans Affairs Mortgage Notice of Default and Foreclosure Intention Letter is a critical warning issued when a borrower falls significantly behind on payments. It serves as a formal notification that the lender intends to initiate foreclosure proceedings. Recipients should immediately contact their loan servicer or a VA technician to explore loss mitigation options, such as repayment plans or loan modifications. This document outlines the specific timeframe to cure the delinquency, making timely communication essential for veterans seeking to protect their home equity and maintain their unique VA housing benefits.

Notice of Default and Intention to Foreclose on Veterans Affairs Loan Letter

A Notice of Default and Intention to Foreclose is a critical legal warning sent to veterans who have fallen behind on mortgage payments. This document signifies that the lender has initiated the foreclosure process due to delinquency. It is essential to contact your loan servicer immediately to explore loss mitigation options, such as repayment plans or loan modifications. Additionally, the Department of Veterans Affairs offers financial counseling to help homeowners retain their property and avoid the finality of a foreclosure sale through specialized federal protections.

VA Loan Default Notice and Intention to Foreclose Letter

A VA Loan Default Notice and Intention to Foreclose Letter is a formal notification sent by lenders when a veteran falls behind on mortgage payments. This document triggers the VA Home Retention process, allowing the Department of Veterans Affairs to intervene. It is crucial to contact your servicer immediately to explore loss mitigation options, such as repayment plans or loan modifications. The VA provides dedicated technicians to help borrowers avoid foreclosure, ensuring that veterans can leverage specific federal protections and stay in their homes whenever possible.

Letter of Default Notice and Foreclosure Intention for Veterans Affairs Mortgage

A VA Notice of Default is a critical legal document sent to veterans who miss mortgage payments. It officially warns that the lender intends to initiate foreclosure proceedings if the delinquency is not resolved. Upon receiving this, homeowners should immediately contact their loan servicer to discuss loss mitigation. The Department of Veterans Affairs provides financial counseling and special assistance programs to help veterans avoid losing their homes. Timely communication is essential to explore options like repayment plans, loan modifications, or a forbearance agreement to protect your credit and property.

Veterans Affairs Home Loan Notice of Default and Foreclosure Intention Letter

Receiving a Veterans Affairs Home Loan Notice of Default is a critical warning that your mortgage is delinquent. This formal document indicates the lender's foreclosure intention if the debt remains unpaid. However, VA loans offer unique protections, including mandatory loss mitigation assistance. It is essential to contact your loan servicer immediately to explore options like repayment plans, loan modifications, or a deed in lieu of foreclosure. Engaging with a VA loan technician can provide specialized advocacy to help you retain your home and navigate the legal timeline effectively.

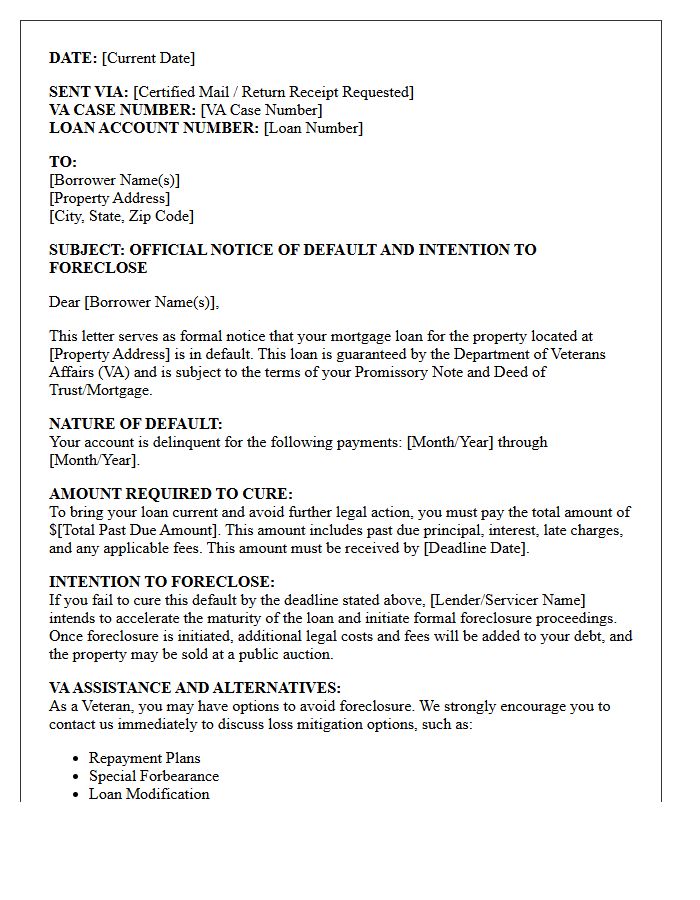

Intention to Foreclose and Notice of Default Letter for VA Loan

When you fall behind on payments, your servicer must send a Notice of Default before initiating legal action. For those with a VA Loan, federal regulations require the lender to provide at least 30 days' advance notice of their Intention to Foreclose. This letter is a critical warning, not a final eviction. It outlines the specific amount needed to reinstate the mortgage and highlights available loss mitigation options. Borrowers should immediately contact their servicer or a VA technician to explore repayment plans or loan modifications to protect their home equity.

Veterans Affairs Loan Pre-Foreclosure Default Notice Letter

A Veterans Affairs (VA) Loan Pre-Foreclosure Default Notice is a formal warning issued when a borrower misses mortgage payments. Receiving this Notice of Default signifies the beginning of the legal foreclosure process. It is vital to contact your loan servicer immediately to explore loss mitigation options, such as repayment plans or loan modifications. The VA provides dedicated financial counseling to help veterans avoid home loss. Acting quickly after receiving this letter is the most effective way to protect your credit and secure your housing stability before the foreclosure sale is scheduled.

Official Letter of Notice of Default and Intention to Foreclose for Veterans Affairs Loan

Receiving an official Notice of Default and Intention to Foreclose is a critical stage for veterans with a VA-backed mortgage. This formal document indicates that the Department of Veterans Affairs has been notified of a serious delinquency. It is essential to act immediately by contacting your loan servicer to discuss loss mitigation options, such as repayment plans or loan modifications. The VA provides specialized foreclosure avoidance assistance to help military members retain their homes, but legal timelines are strict once this official notice is issued.

Veterans Affairs Residential Loan Default and Foreclosure Intention Letter

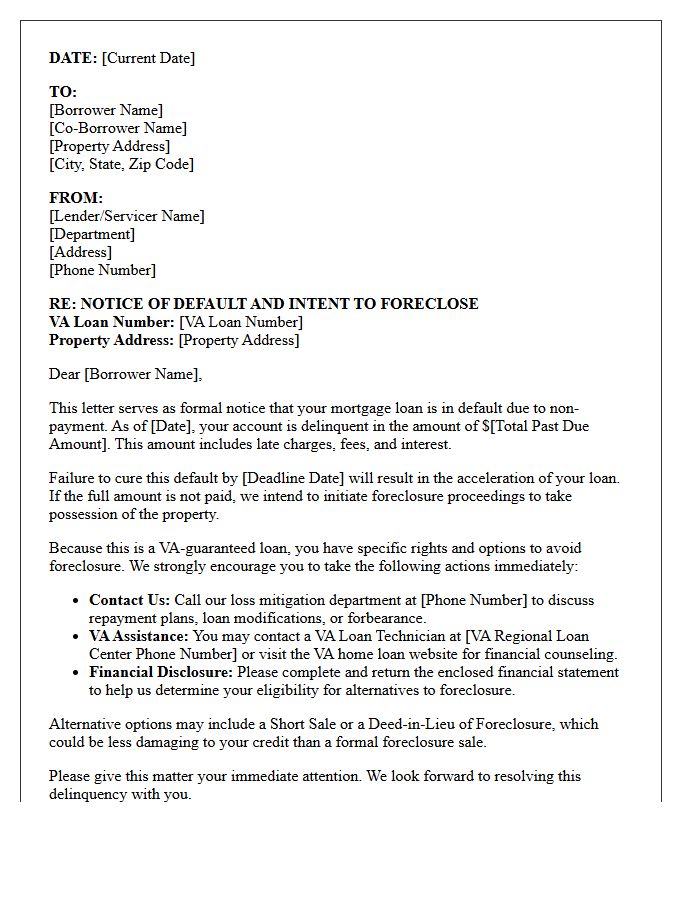

A Veterans Affairs (VA) loan default occurs when a borrower misses payments, triggering a formal Notice of Default. The servicer must then issue a Foreclosure Intention Letter, officially notifying the veteran of the intent to reclaim the property. This document is a critical legal warning, but it also highlights VA-specific loss mitigation options. Veterans should immediately contact their servicer or a VA technician to explore reinstatement, loan modification, or repayment plans to prevent the final loss of their home through the foreclosure process.

Letter Regarding Notice of Default and Intention to Foreclose on VA Loan

A Notice of Default is a formal warning issued when you miss payments on a VA-backed mortgage. This letter signifies the intention to foreclose, meaning the lender has initiated the legal process to repossess your home. It is crucial to contact your loan servicer immediately to explore loss mitigation options. The Department of Veterans Affairs offers financial counseling and specialized programs to help veterans avoid foreclosure. Acting quickly can help you secure a repayment plan or loan modification to protect your homeownership and credit standing.

What is a VA Loan Notice of Default and Intention to Foreclose?

A VA Loan Notice of Default and Intention to Foreclose is a formal legal notification sent by your mortgage servicer when you have fallen significantly behind on payments. It serves as an official warning that the lender intends to begin the foreclosure process unless the delinquency is resolved within a specific timeframe.

What should I do immediately after receiving a VA foreclosure notice?

You should immediately contact your mortgage servicer to discuss loss mitigation options and reach out to a VA Regional Loan Center to speak with a VA Loan Technician. The VA provides financial counseling and can often mediate between you and your lender to find an alternative to foreclosure.

Can the VA help me stop a foreclosure once it has started?

Yes, the Department of Veterans Affairs has dedicated loan specialists who can intervene to explore options such as repayment plans, loan modifications, forbearances, or "Refunding." Refunding is a unique VA power where the government buys the loan from the lender to manage it directly and help the Veteran keep their home.

What are the alternatives to foreclosure for VA loan holders?

Common alternatives include a repayment plan to catch up on missed payments, a loan modification to adjust terms, or a short sale. If you cannot keep the home, a Deed-in-Lieu of Foreclosure may be an option, which allows you to voluntarily transfer the property title to the lender to avoid a formal foreclosure on your credit report.

How many missed payments trigger a VA Notice of Default?

While timelines vary by lender, a Notice of Default is typically issued after you are 60 to 90 days delinquent. Under VA guidelines, lenders are required to notify the VA within 45 days of a missed payment and must exhaust all "loss mitigation" efforts before finalized foreclosure proceedings can occur.

Comments