Securing a New Construction Build Pre-Approval Letter is the essential first step in financing your dream home from the ground up. Unlike standard loans, this specialized document confirms your eligibility for land acquisition and construction costs, giving builders confidence in your financial backing. Understanding these specific requirements ensures a smooth development process. To help you begin, below are some ready to use template.

Image cover: Professional New Construction Pre-Approval Letter Templates and Guide

Letter Samples List

- Standard New Construction Build Pre-Approval Letter

- Conditional Construction-To-Permanent Pre-Approval Letter

- Custom Home Build Mortgage Pre-Approval Letter

- Lot Purchase And Construction Pre-Approval Letter

- End-Loan New Construction Pre-Approval Letter

- Builder Preferred Lender Pre-Approval Letter

- FHA New Construction Build Pre-Approval Letter

- VA New Construction Loan Pre-Approval Letter

- Jumbo Construction Build Pre-Approval Letter

- Turnkey New Construction Pre-Approval Letter

- Spec Home Build Pre-Approval Letter

- One-Time Close Construction Pre-Approval Letter

- Two-Time Close Construction Pre-Approval Letter

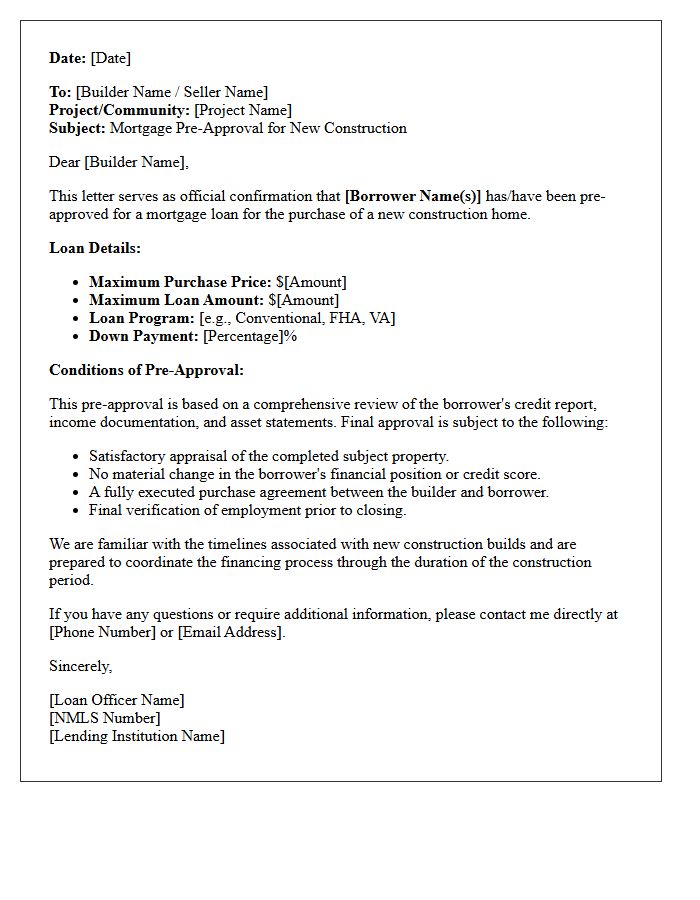

Standard New Construction Build Pre-Approval Letter

A standard new construction build pre-approval letter is a guaranteed commitment from a lender specifically tailored for long-term projects. Unlike regular home loans, these letters often account for extended rate locks and potential cost escalations during the building process. Builders require this document to verify your financial capacity to fund the project through completion. It ensures that your debt-to-income ratio remains stable despite the lengthy timeline, protecting both the buyer and the developer from financing contingencies during the final stages of the residential construction.

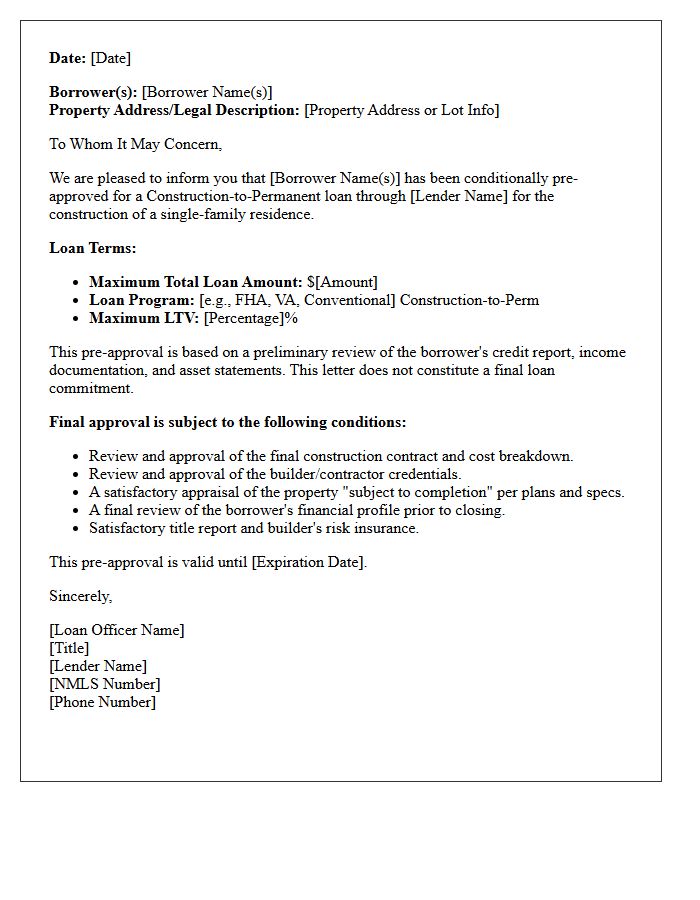

Conditional Construction-To-Permanent Pre-Approval Letter

A Conditional Construction-To-Permanent Pre-Approval Letter is a critical document confirming a lender's preliminary commitment to finance both the building phase and the long-term mortgage. It outlines specific underwriting conditions, such as final appraisal, plan approvals, and income verification, that must be met before funding. This letter demonstrates your borrowing capacity to builders and developers, ensuring you can cover land acquisition and construction costs. Securing this pre-approval streamlines the transition into a permanent loan, protecting your interest rate and long-term financial stability during the home-building process.

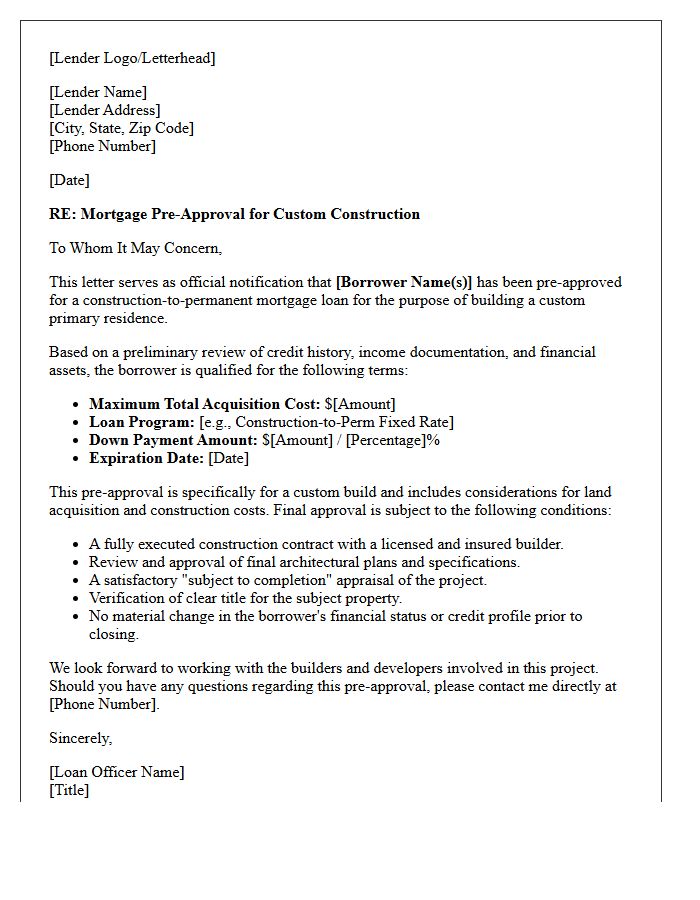

Custom Home Build Mortgage Pre-Approval Letter

A Custom Home Build Mortgage Pre-Approval is a formal commitment from a lender based on your creditworthiness and construction plans. Unlike standard loans, this specialized approval evaluates both the borrower and the project's feasibility. It provides a specific budget for land acquisition and construction costs, ensuring you can secure a construction-to-permanent loan. Obtaining this letter early is essential to prove financial capability to builders and architects, allowing you to lock in financing before breaking ground on your custom property.

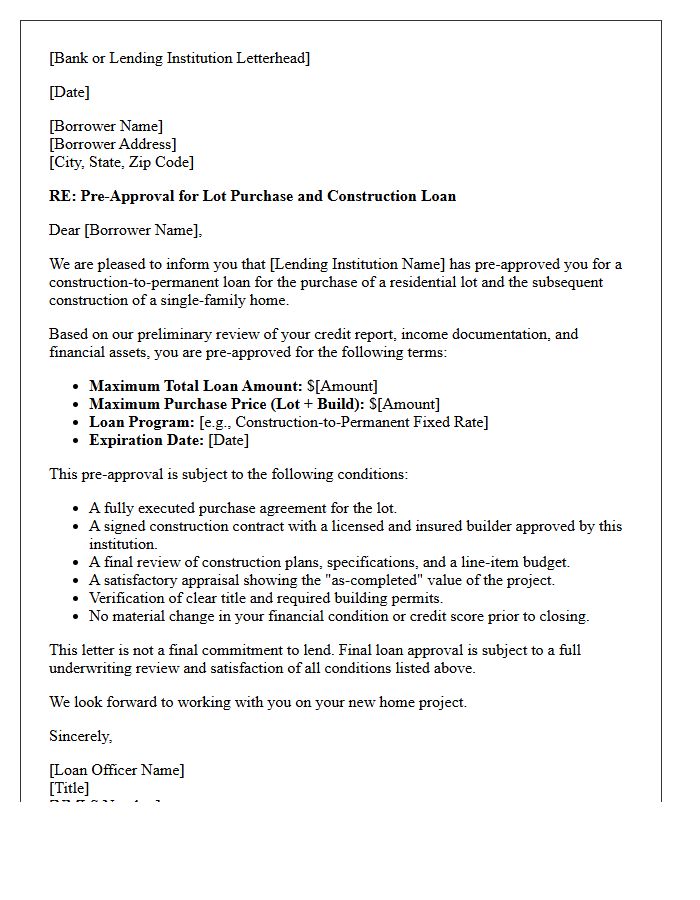

Lot Purchase And Construction Pre-Approval Letter

A Lot Purchase and Construction Pre-Approval Letter is a specialized document from a lender confirming you are qualified for a construction-to-permanent loan. Unlike standard mortgages, this letter verifies your ability to finance both the raw land acquisition and the subsequent building costs. It demonstrates to sellers and builders that you have the financial backing for a comprehensive project. Key factors include your creditworthiness and the estimated project budget, providing the financial certainty needed to secure a lot and initiate a custom home build simultaneously.

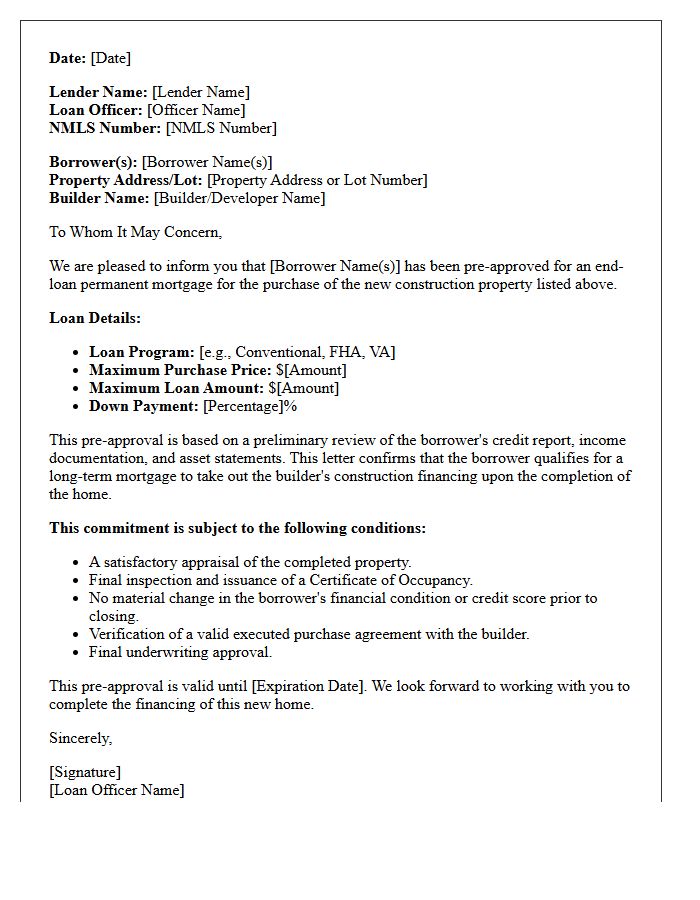

End-Loan New Construction Pre-Approval Letter

An End-Loan New Construction Pre-Approval Letter is a critical document for buyers financing a custom home. Unlike a builder's loan, an end-loan is mortgage financing disbursed only upon the property's completion. This letter proves to builders that you are qualified for a long-term loan once the certificate of occupancy is issued. It ensures your financial eligibility remains intact during the lengthy building process, though you may need a rate lock extension to protect against market fluctuations. This commitment provides the security needed to begin construction with confidence.

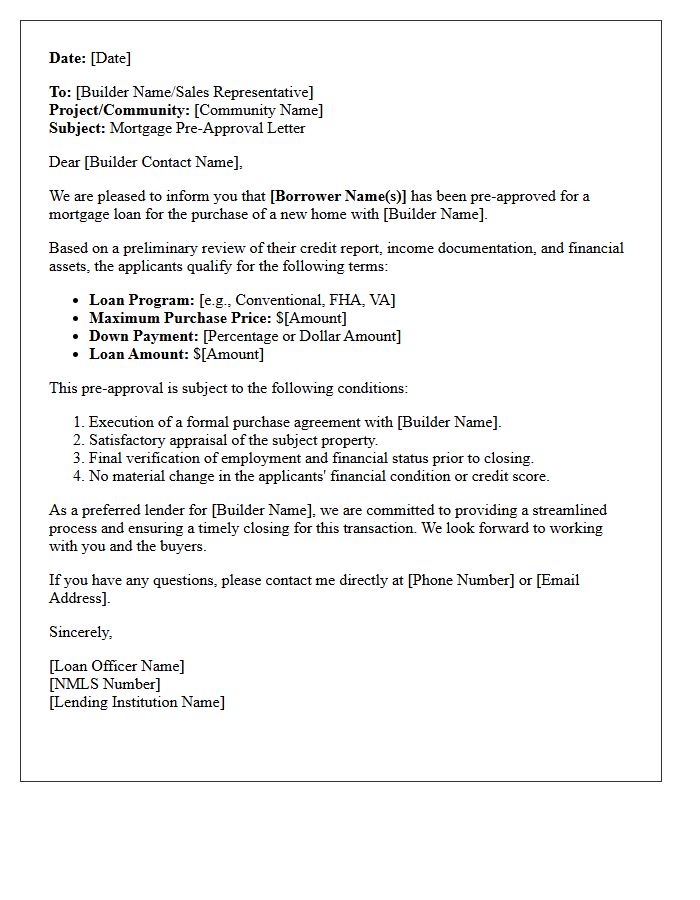

Builder Preferred Lender Pre-Approval Letter

A builder preferred lender pre-approval letter is a financial endorsement from a construction company's partnered mortgage provider. Obtaining this document is often a mandatory requirement before signing a purchase contract for a new-build home. While it simplifies the underwriting process and may unlock incentives like closing cost credits or design upgrades, buyers should compare rates independently. This letter proves to the builder that you are a qualified candidate who can meet specific construction milestones and successfully secure final funding upon the property's completion.

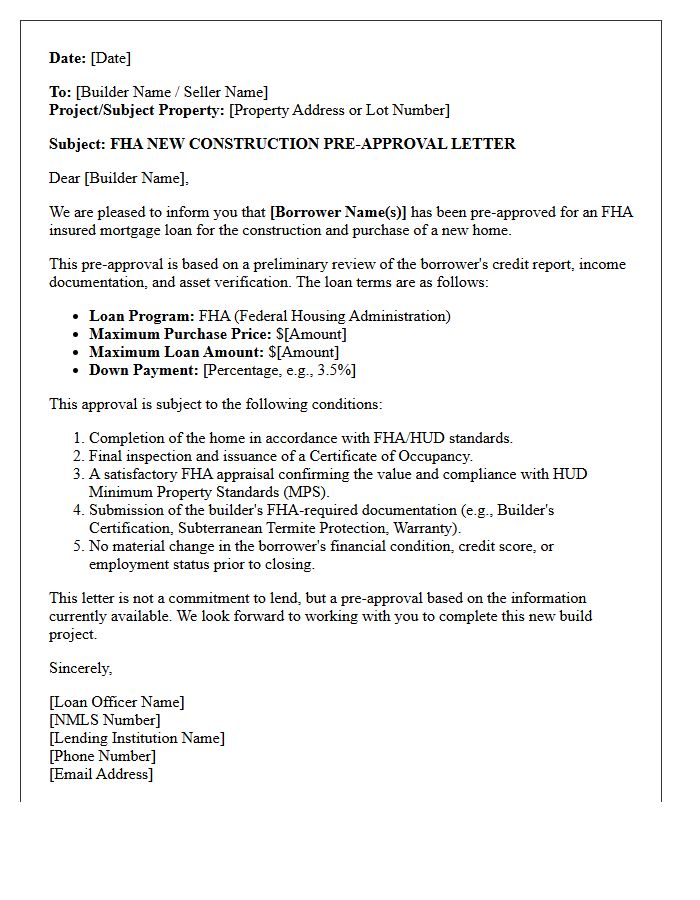

FHA New Construction Build Pre-Approval Letter

An FHA new construction build pre-approval letter confirms a borrower meets HUD guidelines for a mortgage on a home yet to be built. Unlike standard letters, it must account for potential cost escalations and specific property requirements like soil tests or builder certifications. This document proves financial readiness to builders, ensuring the loan covers both the land and construction phases. To maintain eligibility during long build times, buyers must avoid significant credit changes, as final underwriting occurs only after the home reaches substantial completion and passes a final inspection.

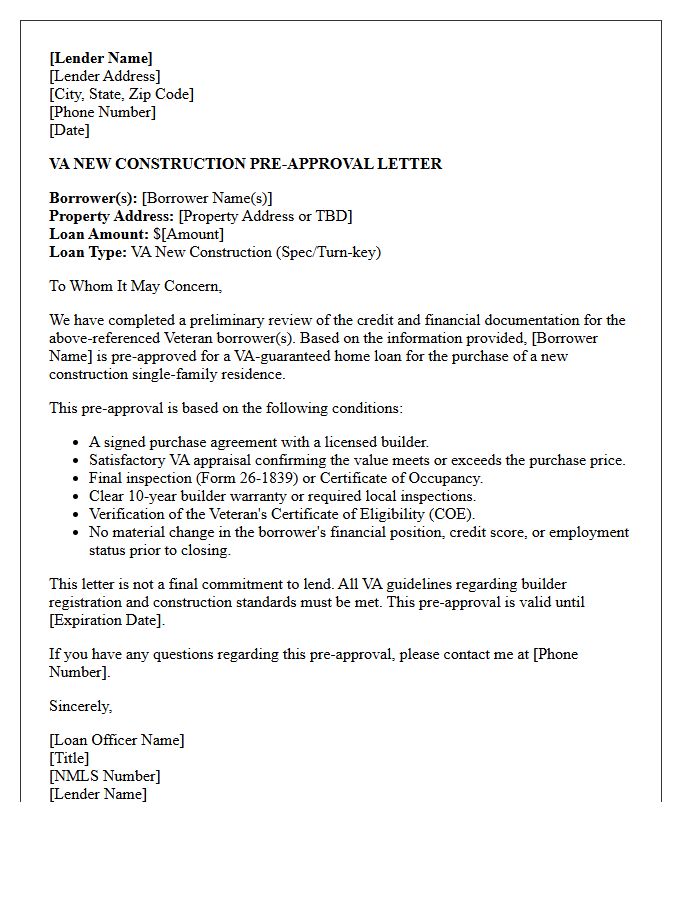

VA New Construction Loan Pre-Approval Letter

A VA new construction loan pre-approval letter is a critical document proving your eligibility and borrowing capacity to builders. Unlike standard home loans, this letter confirms that a VA-approved lender has verified your Certificate of Eligibility (COE), income, and credit score specifically for a one-time close construction process. It provides builders the confidence to start construction, knowing the Department of Veterans Affairs guarantees the financing. Securing this pre-approval ensures you can lock in interest rates and cover both the land purchase and home building costs with a zero-down payment benefit.

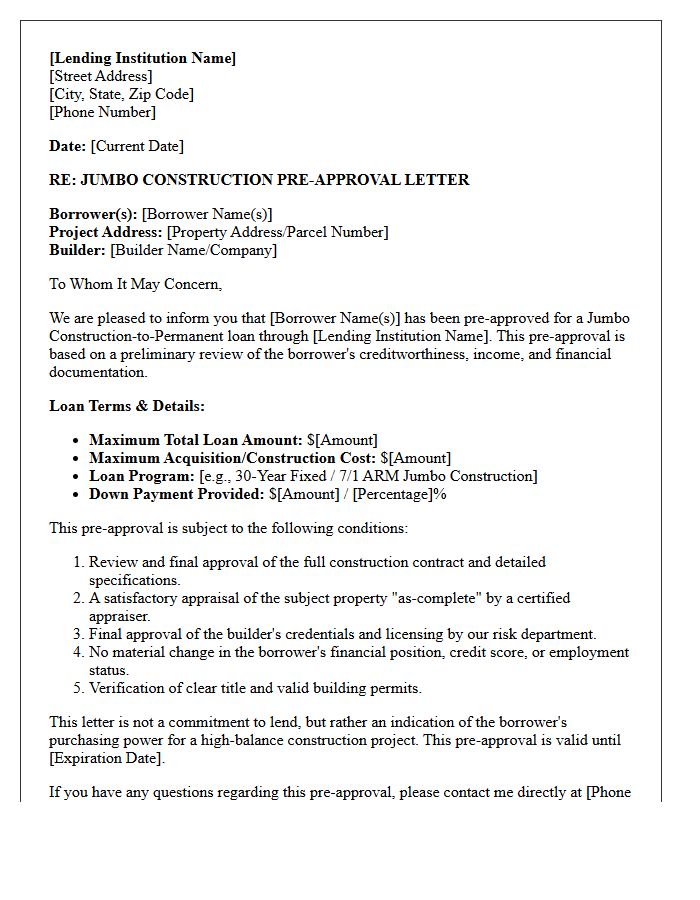

Jumbo Construction Build Pre-Approval Letter

A Jumbo Construction Build Pre-Approval Letter is a formal document proving a lender's commitment to financing a custom home project that exceeds standard conforming loan limits. It validates your creditworthiness, income, and down payment capacity specifically for high-value builds. This letter is essential for securing a licensed builder and purchasing a lot, as it demonstrates you have the financial backing to complete a complex permanent-to-construction loan process. Obtaining this early ensures you understand your budget constraints before finalizing architectural plans or breaking ground on your luxury residence.

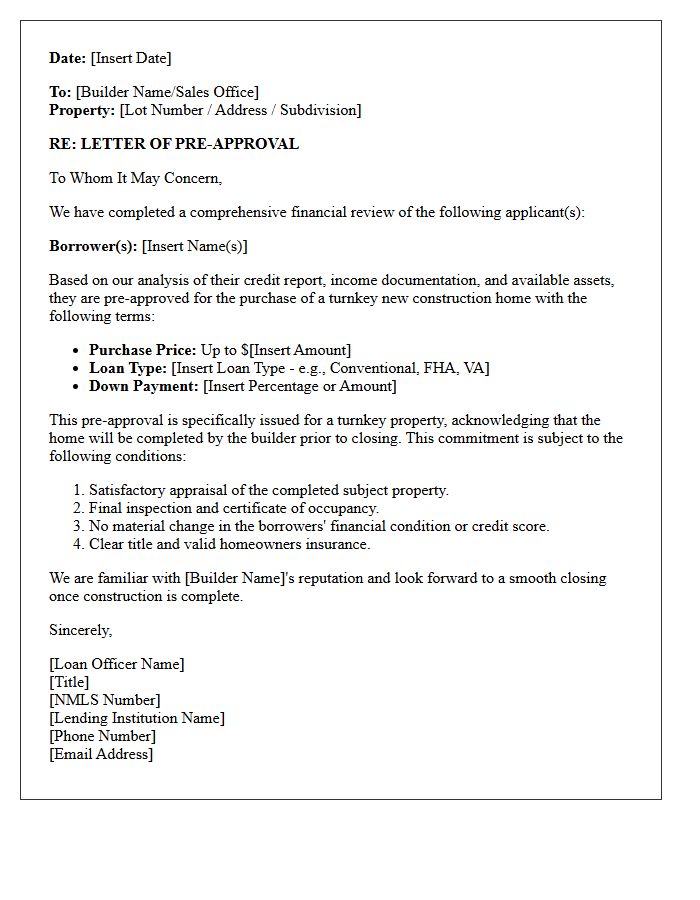

Turnkey New Construction Pre-Approval Letter

A Turnkey New Construction Pre-Approval Letter is a specialized document confirming a buyer's financial eligibility for move-in-ready homes. Unlike standard loans, this dedicated financing assurance accounts for specific builder requirements and final appraisal values. It signals to developers that you are qualified for an immediate closing once construction is complete. Securing this letter streamlines the purchase process, ensures budget certainty, and strengthens your negotiating position in competitive new-build markets. It is the essential first step to transitioning into a fully finished, maintenance-free property without unexpected financing delays.

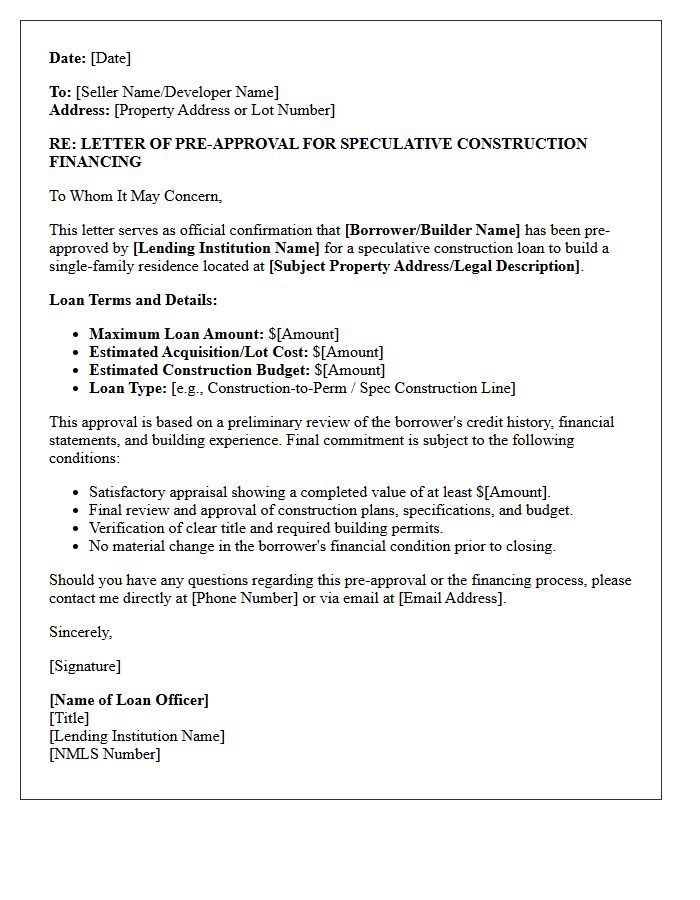

Spec Home Build Pre-Approval Letter

A Spec Home Build Pre-Approval Letter is a specialized document from a lender verifying a builder's financial capacity to construct a move-in ready residence without a pre-selected buyer. Unlike standard mortgages, this construction financing evaluation focuses on the builder's creditworthiness, liquidity, and project feasibility. It serves as essential proof to landowners and suppliers that funding is secured to complete the inventory home. Securing this letter is a critical first step in speculative development, ensuring the project remains viable from groundbreaking to the final sale in a competitive real estate market.

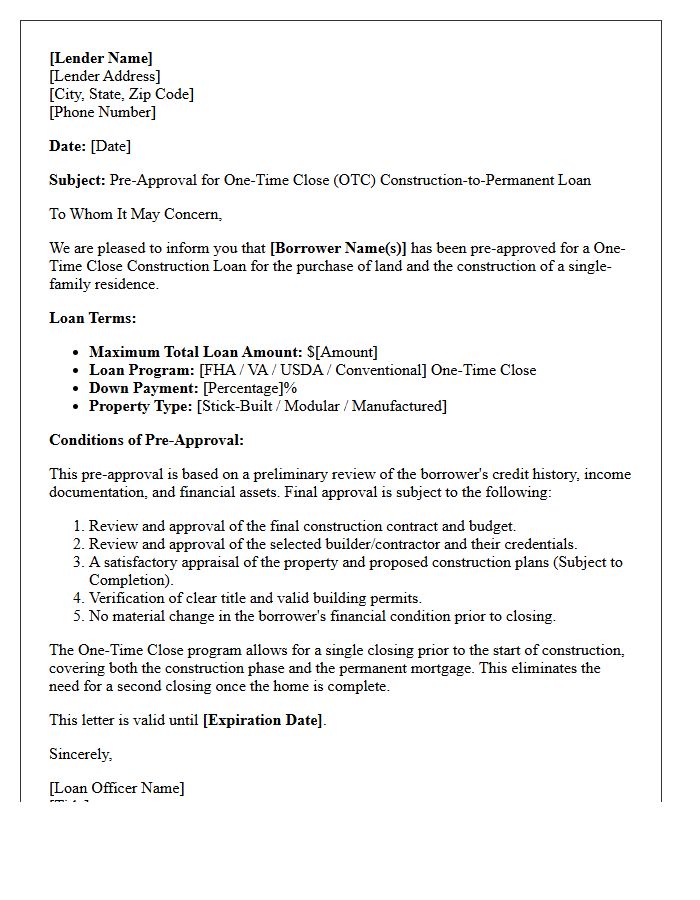

One-Time Close Construction Pre-Approval Letter

A One-Time Close Construction Pre-Approval Letter is a vital document confirming a lender's commitment to finance both the building phase and the permanent mortgage through a single closing process. This all-in-one financing solution simplifies the transition from construction to homeownership by locking in interest rates early. It verifies the borrower's creditworthiness and project feasibility, ensuring the builder and lender are aligned before breaking ground. Securing this letter is the essential first step to streamline your custom home project, reducing closing costs and eliminating the need for multiple loan applications.

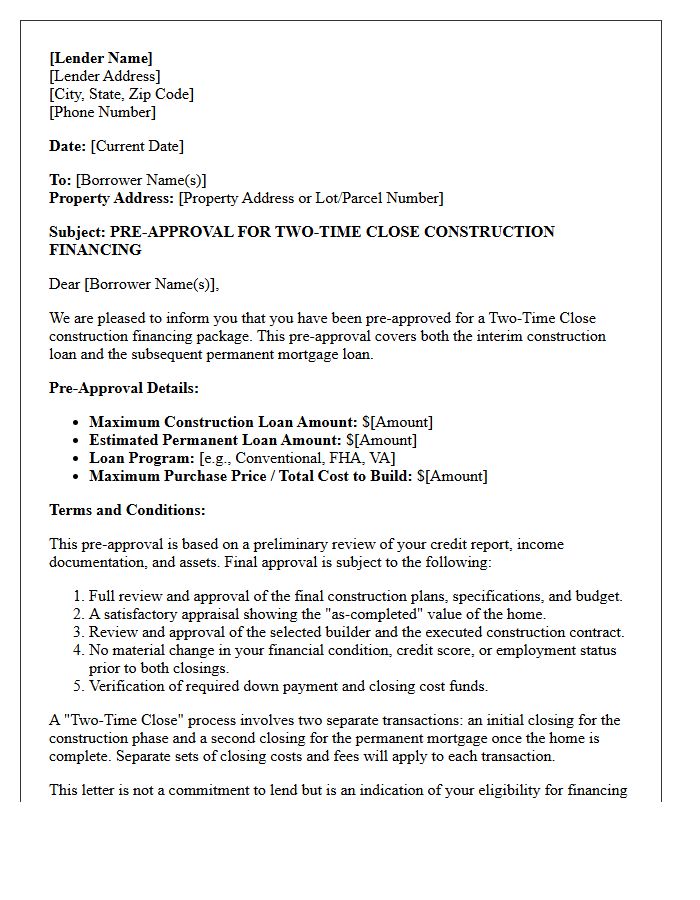

Two-Time Close Construction Pre-Approval Letter

A Two-Time Close Construction Pre-Approval Letter is a vital document for financing a custom home build. Unlike single-close options, this requires two separate underwriting phases: one for the construction loan and another for the permanent mortgage. This letter confirms a lender's preliminary commitment to fund both stages, ensuring you can cover labor and materials initially and refinance into a long-term loan upon completion. It provides builders with financial certainty, though borrowers must maintain stable credit and income throughout the entire building process to secure final permanent financing approval.

What is a pre-approval letter for a new construction build?

A new construction pre-approval letter is a document from a mortgage lender stating the specific amount they are willing to lend you for the purchase of a home that has yet to be built or is currently under development. Unlike standard pre-approvals, it often considers longer lock-in periods and specific builder requirements.

How does a pre-approval for a new build differ from an existing home loan?

Pre-approvals for new construction often require a more rigorous credit analysis and may include "extended rate locks" to protect against interest rate hikes during the 6-12 month build process. Lenders also evaluate the builder's reputation and the project's viability before issuing the final commitment.

Why do builders require a pre-approval letter before signing a contract?

Builders require a pre-approval letter to ensure the buyer has the financial capacity to secure a mortgage once the home is completed. This minimizes the builder's risk of carrying the inventory if the buyer's financing falls through at the end of the construction phase.

Can I use my own lender for a new construction pre-approval?

Yes, buyers have the right to use any lender for their pre-approval and mortgage. However, many builders offer incentives, such as closing cost credits or upgrades, if you use their "preferred lender" who is already familiar with the project's timeline and requirements.

How long is a pre-approval letter valid for a new home build?

Typically, a pre-approval letter is valid for 60 to 90 days. Because new construction can take a year or more to finish, you will likely need to provide updated financial documentation and refresh your pre-approval multiple times throughout the building process.

Comments