A Non-Qualified Mortgage Pre-Approval Letter proves your creditworthiness when you don't meet traditional lending criteria. This document validates your ability to secure financing using alternative income documentation like bank statements or assets. It strengthens your offer by showing sellers you are a qualified buyer ready to close. To help you get started, below are some ready to use templates.

Image cover: Proven Non-QM Pre-Approval Letter Templates and Expert Samples

Letter Samples List

- Bank Statement Non-Qualified Mortgage Pre-Approval Letter

- Debt Service Coverage Ratio Non-Qualified Mortgage Pre-Approval Letter

- Asset Depletion Non-Qualified Mortgage Pre-Approval Letter

- Foreign National Non-Qualified Mortgage Pre-Approval Letter

- Independent Contractor Non-Qualified Mortgage Pre-Approval Letter

- Investor Cash Flow Non-Qualified Mortgage Pre-Approval Letter

- Recent Credit Event Non-Qualified Mortgage Pre-Approval Letter

- Individual Taxpayer Identification Number Non-Qualified Mortgage Pre-Approval Letter

- Self-Employed Alternative Income Non-Qualified Mortgage Pre-Approval Letter

- Jumbo Non-Qualified Mortgage Pre-Approval Letter

- No Ratio Investment Property Non-Qualified Mortgage Pre-Approval Letter

- Interest Only Non-Qualified Mortgage Pre-Approval Letter

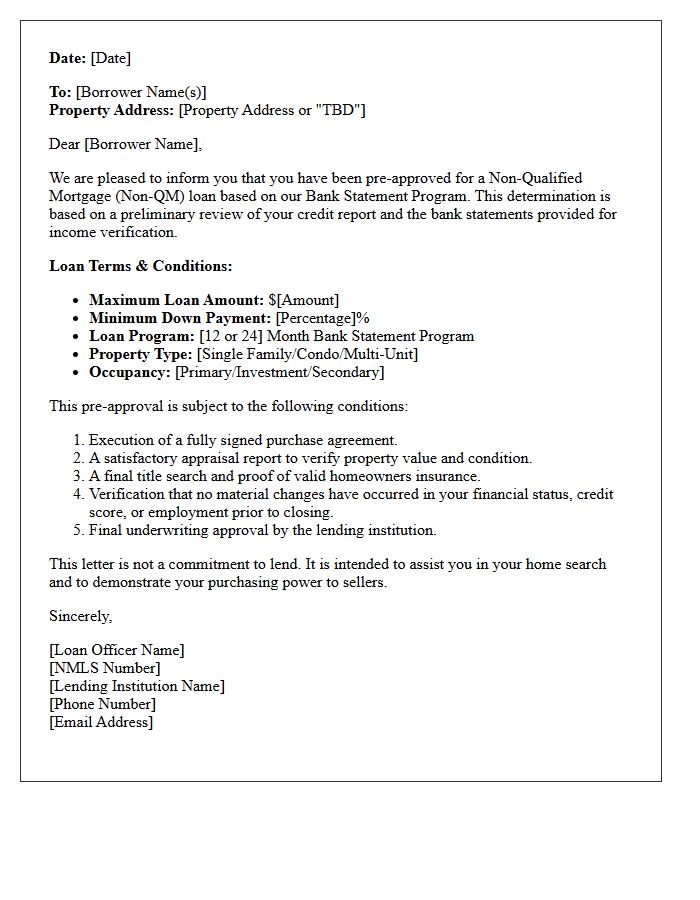

Bank Statement Non-Qualified Mortgage Pre-Approval Letter

A Bank Statement Non-QM Pre-Approval Letter is a vital document for self-employed borrowers seeking home financing without traditional tax returns. Instead of standard income verification, lenders analyze monthly deposits over a 12 or 24-month period to calculate qualifying cash flow. This specialized letter demonstrates to sellers that a buyer's alternative documentation has been verified, proving creditworthiness and liquidity. Securing this pre-approval ensures you can compete effectively in the real estate market by leveraging bank statement programs designed for entrepreneurs and business owners with complex financial profiles.

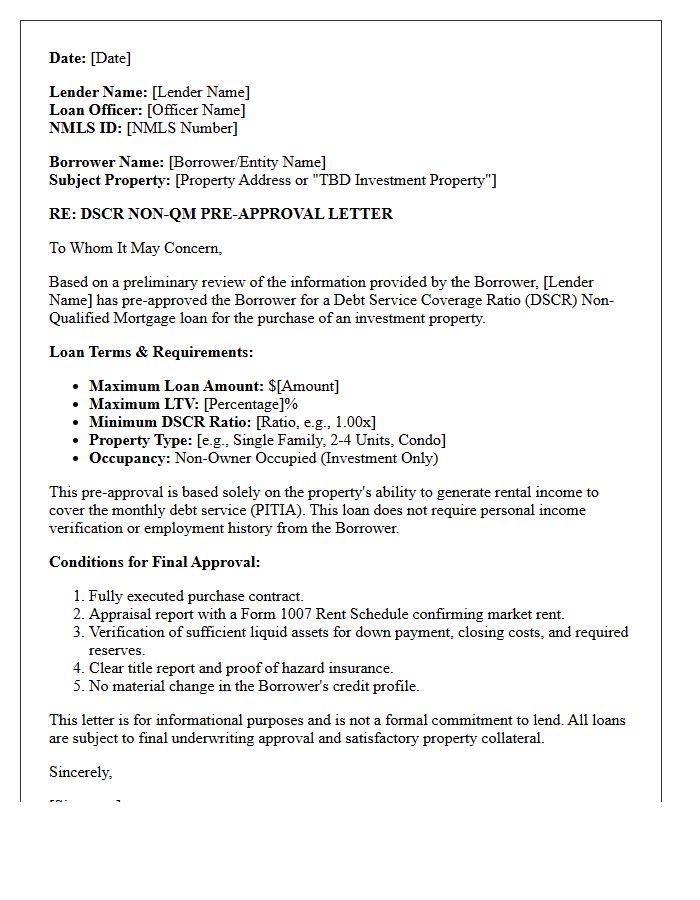

Debt Service Coverage Ratio Non-Qualified Mortgage Pre-Approval Letter

A DSCR Non-QM Pre-Approval Letter verifies a real estate investor's ability to qualify for financing based on a property's rental income rather than personal income documentation. Unlike traditional loans, lenders focus on the Debt Service Coverage Ratio to ensure the monthly rent covers the mortgage obligations. This document is essential for making competitive offers, as it proves the asset generates sufficient cash flow to support the debt. It allows investors with complex tax returns or self-employment history to secure funding quickly based on the investment property's performance.

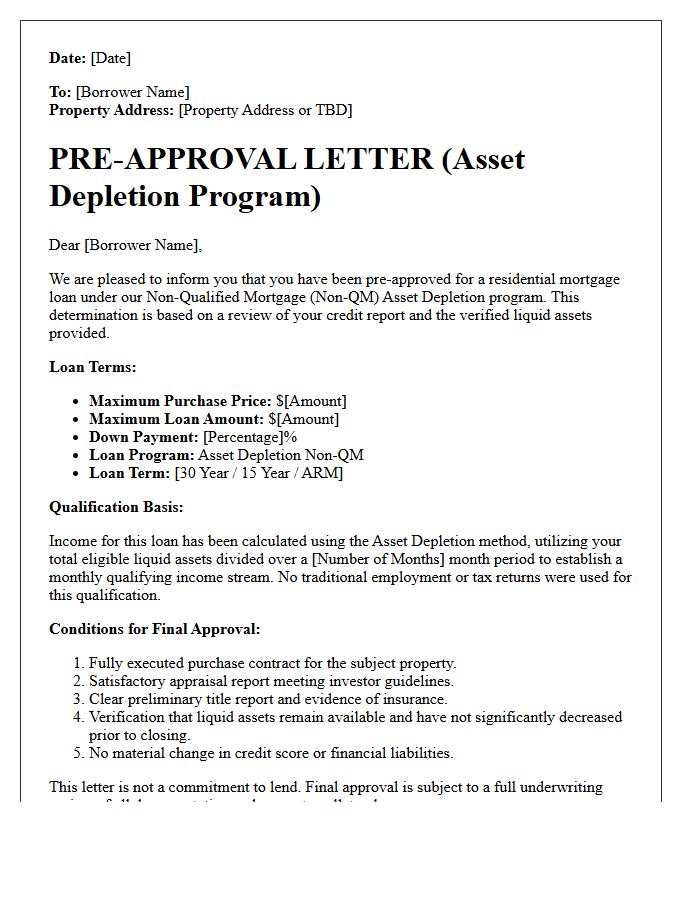

Asset Depletion Non-Qualified Mortgage Pre-Approval Letter

An Asset Depletion Non-QM Pre-Approval Letter verifies a borrower's purchasing power by converting liquid wealth into a qualifying monthly income stream. This specialized financing is essential for retirees or high-net-worth individuals with significant assets but limited traditional employment earnings. Unlike standard loans, the lender calculates a notional income based on total holdings to determine debt-to-income ratios. Securing this letter proves to sellers that you possess the necessary financial liquidity to satisfy long-term mortgage obligations without conventional paystubs, streamlining the closing process for non-traditional borrowers.

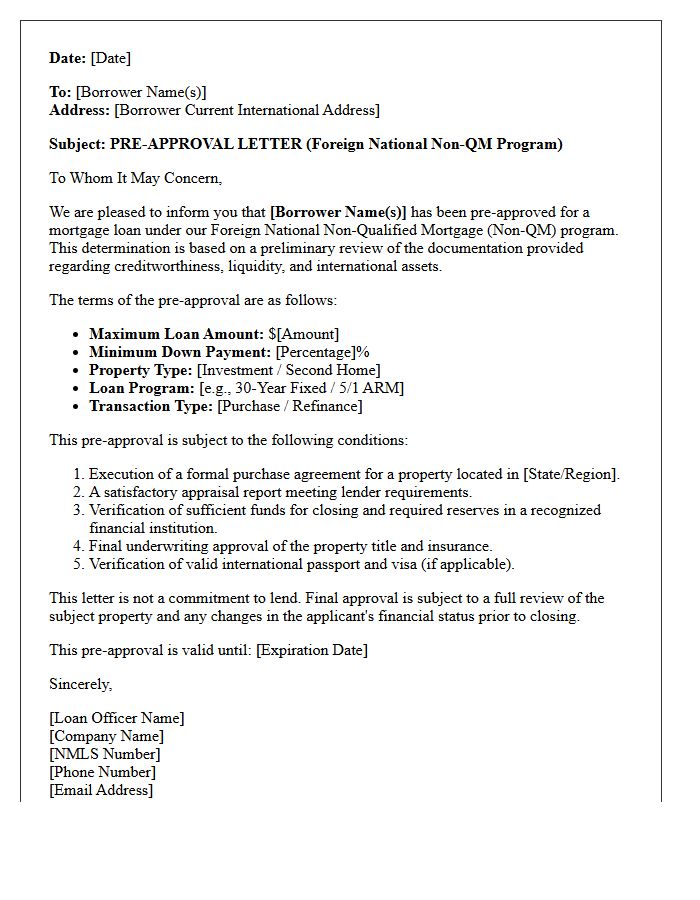

Foreign National Non-Qualified Mortgage Pre-Approval Letter

A Foreign National Non-Qualified Mortgage Pre-Approval Letter verifies a non-resident borrower's eligibility for real estate financing without standard U.S. credit or income documentation. Lenders issue this document after reviewing international assets, foreign credit references, and down payment sources. It is essential for proving financial credibility to sellers in a competitive market. This pre-approval confirms the lender's commitment to fund a loan based on alternative underwriting standards, ensuring the buyer can successfully navigate the complexities of cross-border property acquisitions while meeting specific Non-QM program requirements.

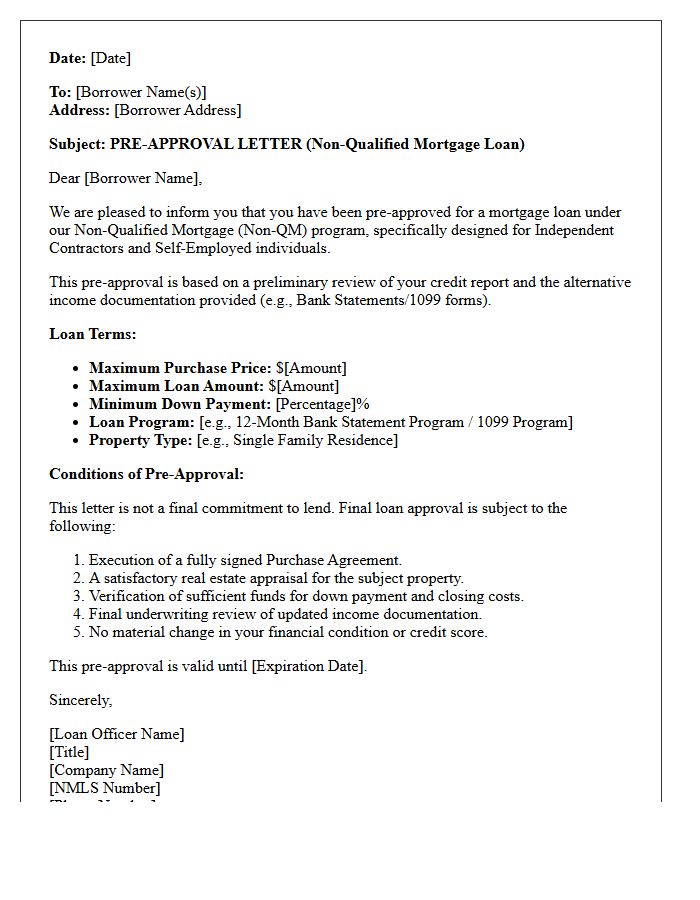

Independent Contractor Non-Qualified Mortgage Pre-Approval Letter

An Independent Contractor Non-Qualified Mortgage Pre-Approval Letter verifies purchasing power for self-employed borrowers using alternative documentation like bank statements rather than tax returns. This document confirms a lender has reviewed your 1099 income, credit history, and liquid assets to determine eligibility for Non-QM loans. It serves as essential proof for real estate agents and sellers that you qualify for financing despite having irregular income streams or significant business write-offs. Securing this letter ensures you are prepared to make competitive offers in a fast-paced housing market while bypassing traditional W-2 requirements.

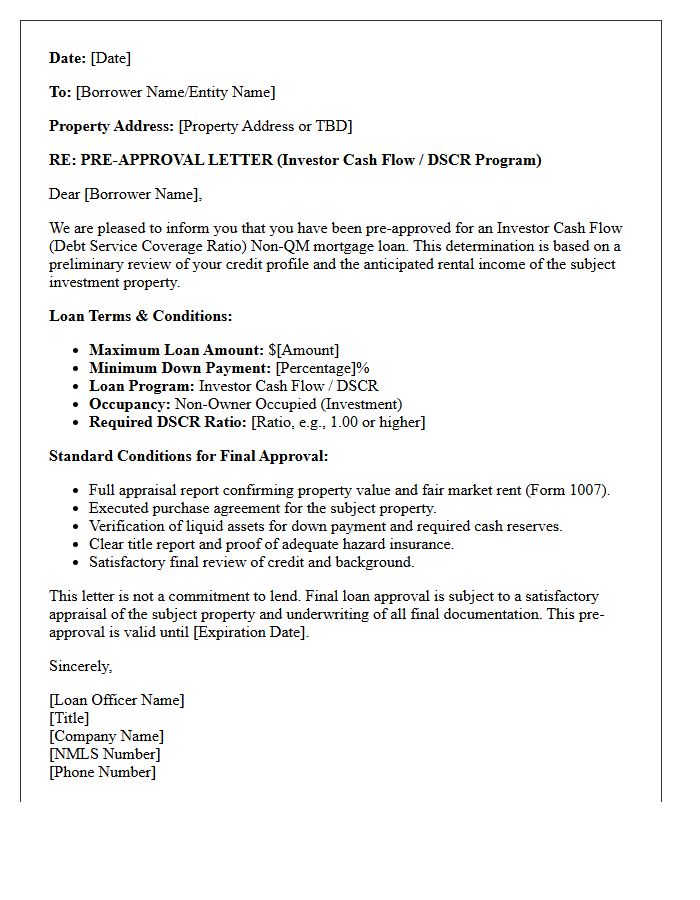

Investor Cash Flow Non-Qualified Mortgage Pre-Approval Letter

An Investor Cash Flow Non-QM Pre-Approval Letter verifies a borrower's eligibility based on a property's rental income rather than personal tax returns. This specialized financing uses the Debt Service Coverage Ratio (DSCR) to qualify real estate investors. The letter confirms that the projected monthly rent covers the mortgage payment, including taxes and insurance. Obtaining this document proves to sellers that you have the financial backing to close quickly, making it a critical tool for competitive real estate markets where traditional income verification is not required.

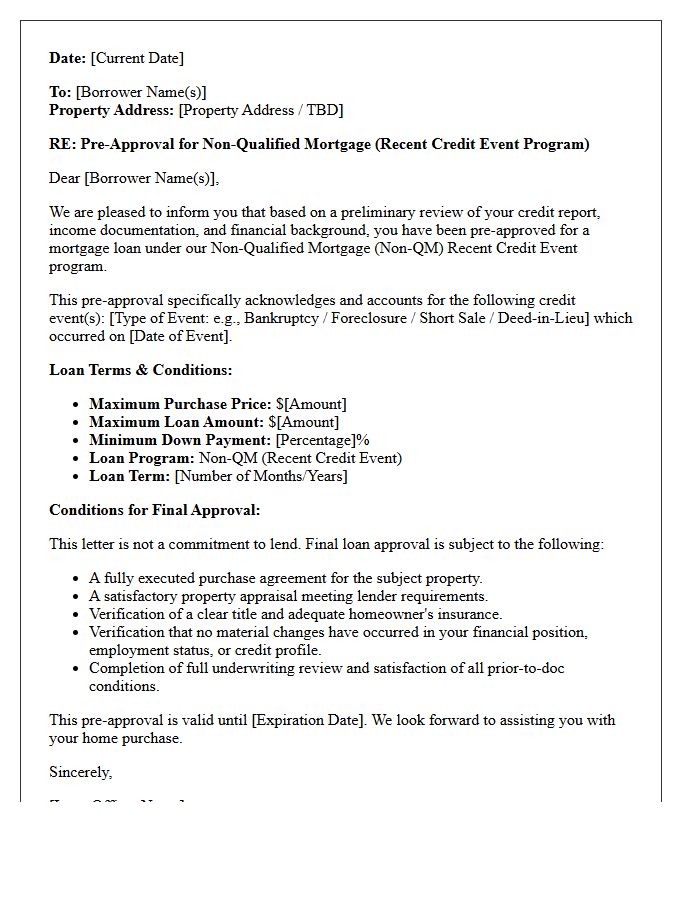

Recent Credit Event Non-Qualified Mortgage Pre-Approval Letter

A Recent Credit Event Non-Qualified Mortgage Pre-Approval Letter confirms eligibility for borrowers recovering from financial setbacks like foreclosure or bankruptcy. Unlike conventional loans, these Non-QM products use flexible underwriting to evaluate your current income stability rather than past credit mistakes. This document is essential for homebuyers with low scores, proving to sellers that they have secured specialized financing despite a recent derogatory event. Obtaining this letter ensures you can compete in the real estate market while utilizing alternative documentation to demonstrate your true creditworthiness and ability to repay.

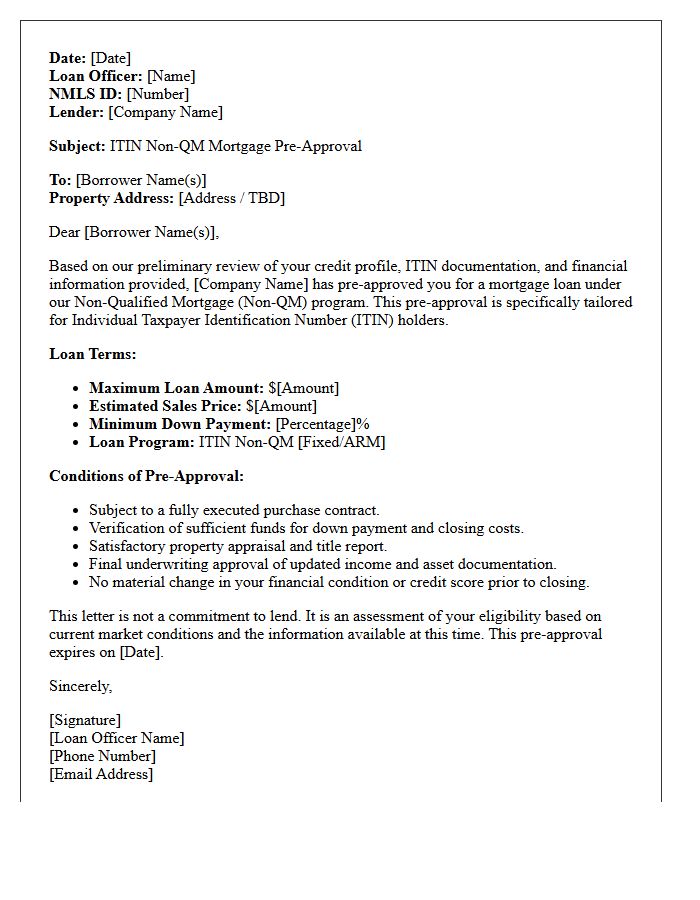

Individual Taxpayer Identification Number Non-Qualified Mortgage Pre-Approval Letter

An ITIN Non-QM Pre-Approval Letter is a vital document for foreign nationals or residents without a Social Security Number seeking home financing. It confirms that a non-qualified mortgage lender has verified your Individual Taxpayer Identification Number, income, and creditworthiness through alternative documentation. This letter demonstrates your financial eligibility to real estate agents and sellers, proving you can secure a loan despite not meeting traditional banking criteria. Obtaining this pre-approval is the essential first step to navigating the specialty credit market and successfully purchasing property in the United States.

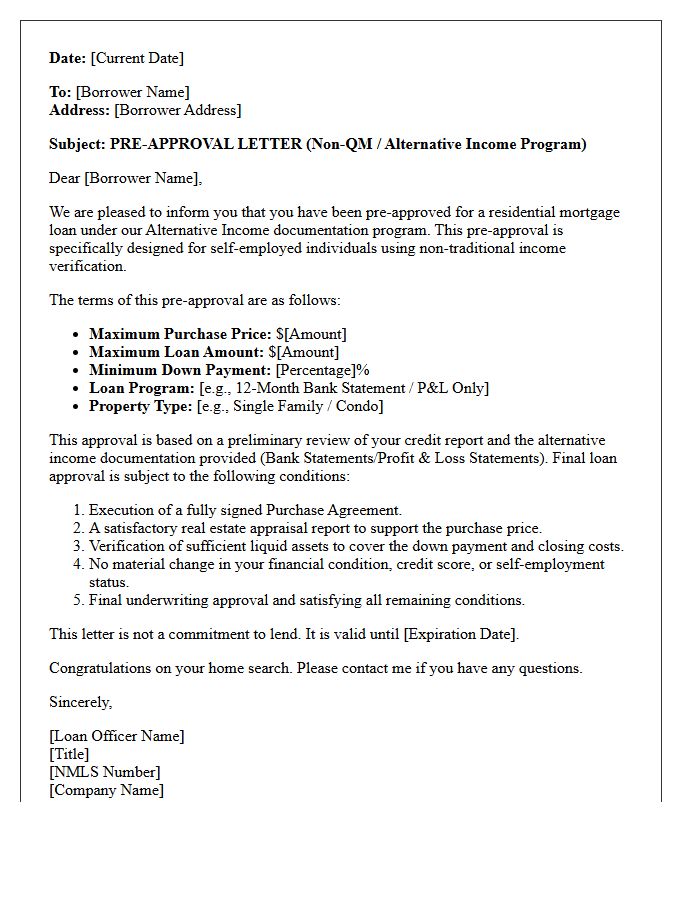

Self-Employed Alternative Income Non-Qualified Mortgage Pre-Approval Letter

A Self-Employed Alternative Income Non-Qualified Mortgage Pre-Approval Letter is essential for entrepreneurs who cannot qualify through traditional tax returns. Instead of standard W-2s, lenders verify creditworthiness using bank statements, 1099 forms, or asset depletion. This document proves your purchasing power to sellers by highlighting your ability to manage debt-to-income ratios through non-traditional documentation. Securing this letter ensures you are viewed as a serious buyer in a competitive market while utilizing flexible underwriting standards tailored specifically for business owners and independent contractors seeking homeownership.

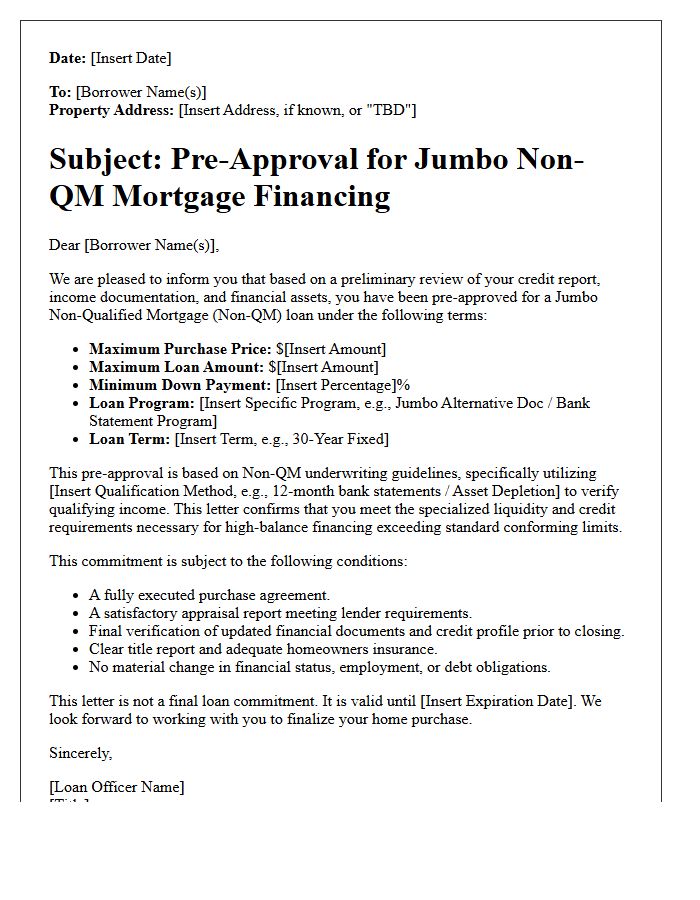

Jumbo Non-Qualified Mortgage Pre-Approval Letter

A Jumbo Non-Qualified Mortgage Pre-Approval Letter proves a borrower's eligibility for high-value loans exceeding conforming limits. Since these loans do not follow standard federal guidelines, the letter demonstrates that a lender has verified complex financials, such as self-employment income or high debt-to-income ratios. For luxury real estate, this document is essential to show sellers you possess the purchasing power for premium properties. It signals financial credibility in competitive markets where traditional financing is unavailable, ensuring your offer is taken seriously by high-end listing agents.

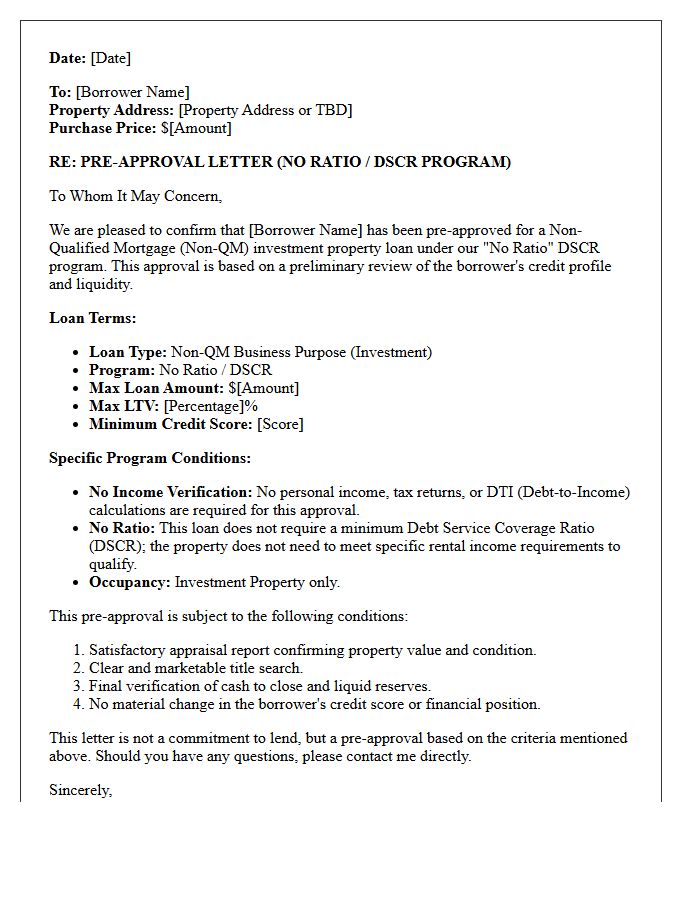

No Ratio Investment Property Non-Qualified Mortgage Pre-Approval Letter

A No Ratio Investment Property Non-QM Pre-Approval Letter is a specialized financing tool for real estate investors. Unlike traditional loans, this mortgage does not require income verification or debt-to-income calculations. Instead, lenders focus entirely on the property's potential to generate revenue rather than the borrower's personal tax returns. This streamlined underwriting process allows for faster closing times and provides a competitive advantage in aggressive markets. It is the ideal solution for self-employed investors seeking to expand their portfolio without disclosing personal financial statements or complex employment history.

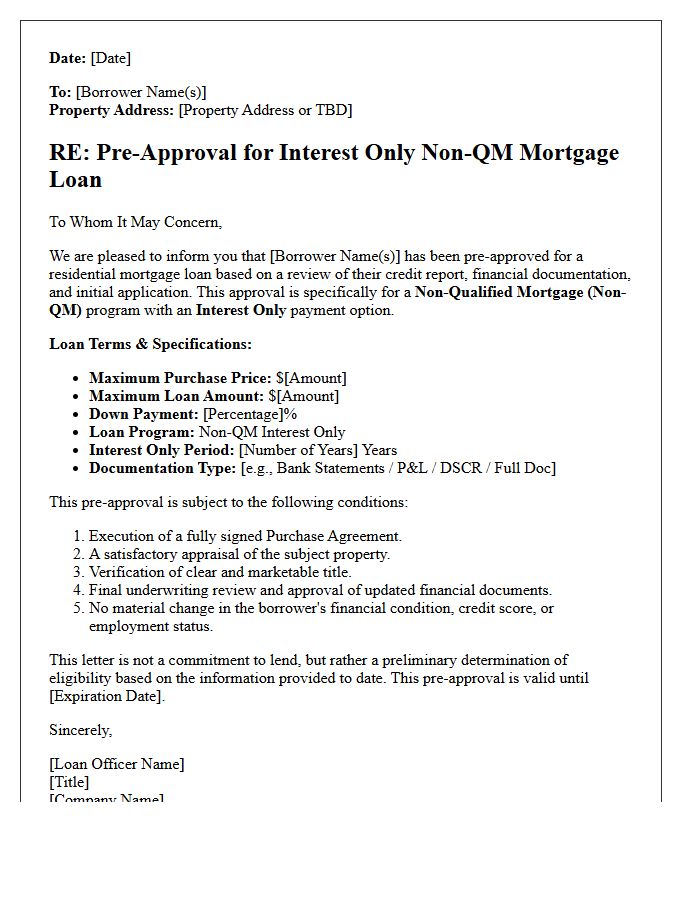

Interest Only Non-Qualified Mortgage Pre-Approval Letter

An Interest Only Non-Qualified Mortgage Pre-Approval Letter proves a borrower's eligibility for specialized financing where monthly payments exclude principal. This document is essential for real estate investors and self-employed individuals using alternative income verification, such as bank statements. It confirms that a lender has vetted your creditworthiness and liquidity under Non-QM guidelines. Having this letter strengthens your offer in competitive markets by demonstrating you can secure flexible financing despite not meeting traditional government-backed loan requirements. It provides a clear maximum loan amount to guide your property search effectively.

What is a Non-Qualified Mortgage (Non-QM) pre-approval letter?

A Non-QM pre-approval letter is a document from a lender stating that a borrower is tentatively approved for a home loan using non-traditional income verification, such as bank statements or asset depletion, rather than standard tax returns.

How do I qualify for a Non-QM pre-approval letter?

To qualify, borrowers typically need to provide alternative documentation of their ability to repay, such as 12 to 24 months of personal or business bank statements, a solid credit score (usually 620+), and a down payment ranging from 10% to 20%.

How long does it take to get a Non-QM pre-approval?

While traditional pre-approvals can be instant, a Non-QM pre-approval often takes 24 to 72 hours because a manual underwriter must review complex income documents like bank statements or Profit & Loss statements.

Does a Non-QM pre-approval letter guarantee a loan?

No, a pre-approval letter is not a final loan commitment. It is subject to a satisfactory property appraisal, a final credit review, and verification that the borrower's financial situation has not changed since the letter was issued.

What are the benefits of having a Non-QM pre-approval letter when making an offer?

A Non-QM pre-approval letter signals to sellers that a self-employed or high-net-worth buyer has already passed a rigorous manual underwriting review, making their offer as competitive as a traditional buyer's offer.

Comments