Secure your financing with a Condominium Project Specific Pre-Approval Letter. Unlike standard approvals, this document confirms both your creditworthiness and the building's eligibility against lender guidelines. It ensures the condo association meets insurance, budget, and litigation requirements before you make an offer, providing a competitive advantage in the real estate market. Below are some ready to use templates.

Image cover: Condo-Specific Financing: Professional Pre-Approval Letter Templates and Samples

Letter Samples List

- Fannie Mae Condominium Project Pre-Approval Letter

- Freddie Mac Condominium Project Pre-Approval Letter

- Federal Housing Administration Condominium Project Pre-Approval Letter

- Veterans Affairs Condominium Project Pre-Approval Letter

- New Construction Condominium Project Pre-Approval Letter

- Established Condominium Project Pre-Approval Letter

- Non-Warrantable Condominium Project Exception Letter

- Condominium Project Limited Review Pre-Approval Letter

- Condominium Project Full Review Pre-Approval Letter

- Condominium Project Pre-Approval Conditions Letter

- Condominium Project Pre-Approval Denial Letter

- Condominium Project Recertification Pre-Approval Letter

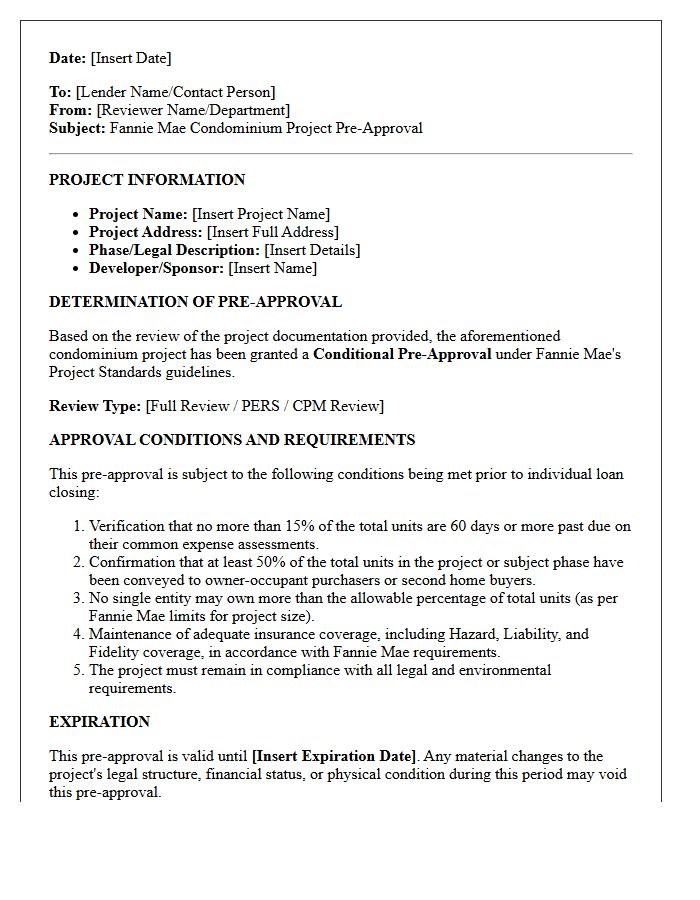

Fannie Mae Condominium Project Pre-Approval Letter

A Fannie Mae Condominium Project Pre-Approval Letter confirms that a specific condo development meets eligibility standards for conventional financing. This document indicates the project has undergone a Full Review or belongs to the PERS list, verifying stable insurance, financial reserves, and owner-occupancy ratios. For buyers and lenders, this letter reduces closing risks by ensuring the homeowners association complies with secondary mortgage market requirements. It is an essential tool for streamlining the loan process in warrantable condo communities.

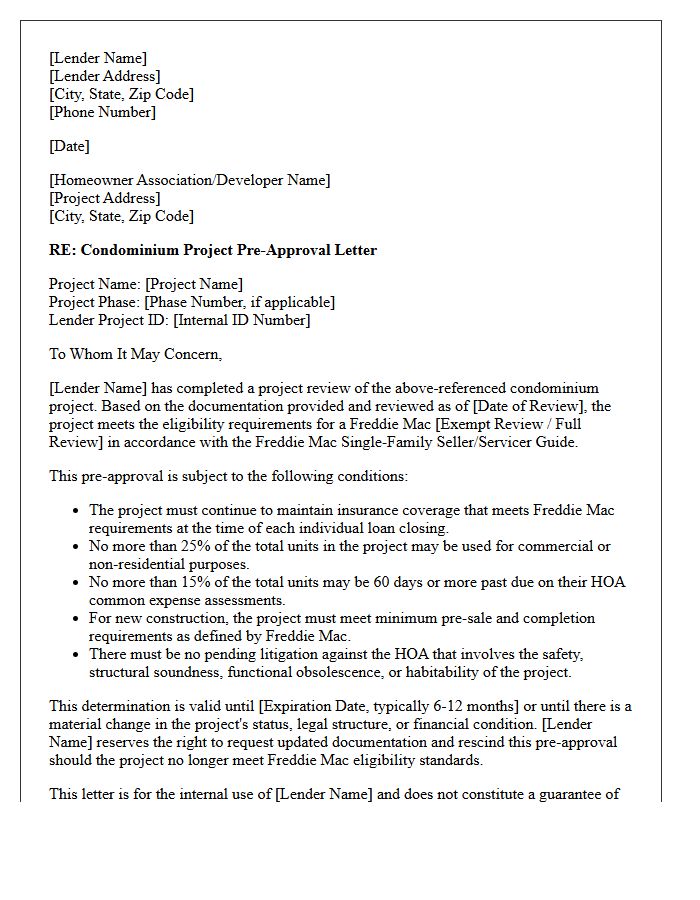

Freddie Mac Condominium Project Pre-Approval Letter

A Freddie Mac Condominium Project Pre-Approval Letter is an official document confirming that a specific development meets eligibility standards for conventional financing. This letter streamlines the mortgage process by verifying that the homeowners association maintains adequate insurance, financial stability, and proper management structures. For buyers and lenders, this certification reduces closing delays and ensures the project aligns with secondary market requirements. Obtaining this status indicates the condo is a "warrantable" investment, making it easier for borrowers to secure competitive interest rates and favorable loan terms within that community.

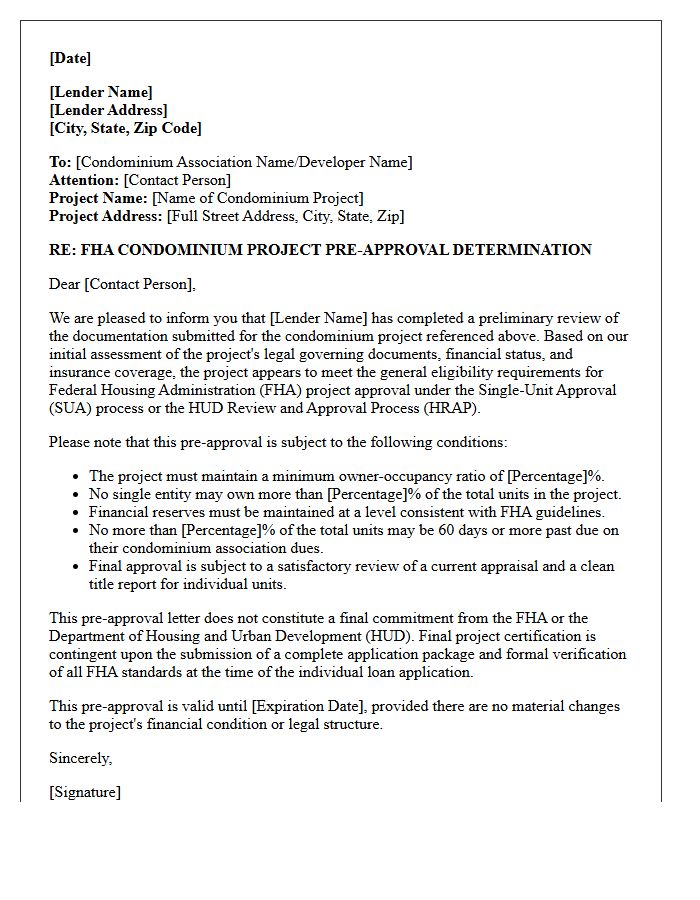

Federal Housing Administration Condominium Project Pre-Approval Letter

An FHA Condominium Project Pre-Approval Letter verifies that a specific housing development meets strict federal eligibility standards. This document confirms the Homeowners Association (HOA) complies with owner-occupancy ratios, financial reserve requirements, and insurance coverage. Buyers must ensure the project is on the approved list before applying for financing, as FHA-insured loans cannot be issued for non-certified communities. This certification mitigates lender risk and guarantees the property is a stable investment, making it a critical first step in the condo buying process for FHA borrowers.

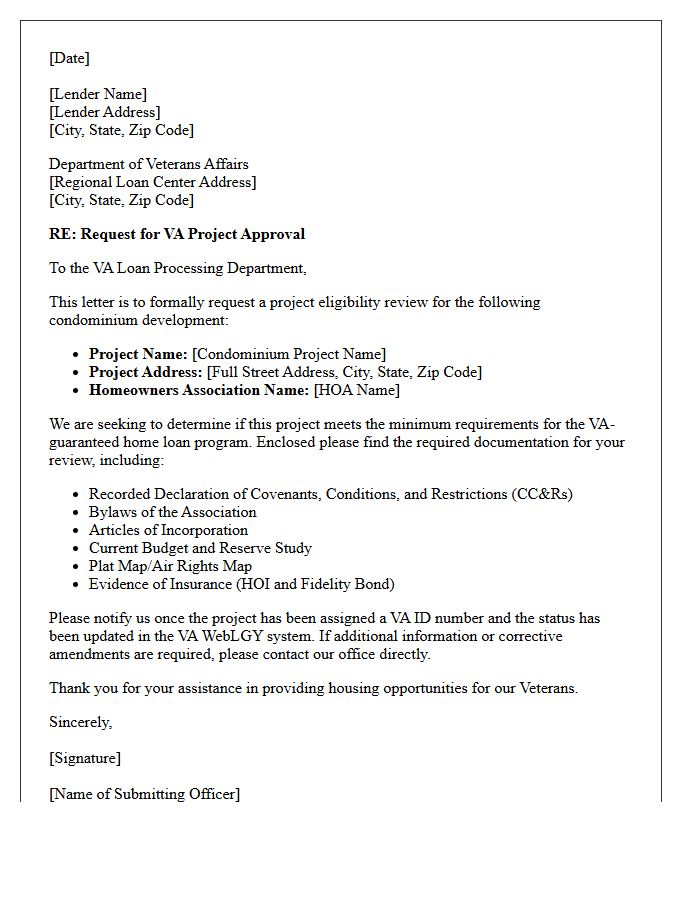

Veterans Affairs Condominium Project Pre-Approval Letter

A Veterans Affairs Condominium Project Pre-Approval Letter confirms that a specific complex meets VA eligibility standards for financing. Before a veteran can utilize their home loan benefit, the development must be on the VA-approved list. This letter ensures the project complies with structural, legal, and financial requirements set by the Department of Veterans Affairs. Obtaining this verification is a critical first step, as lenders cannot process a VA loan for a unit in an unapproved community, regardless of the buyer's personal creditworthiness or military service history.

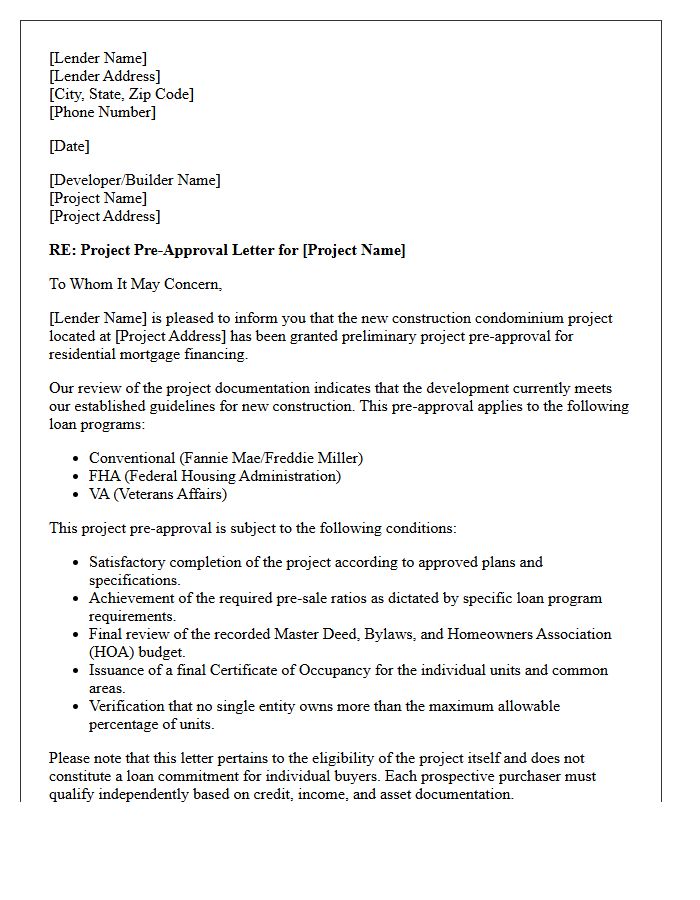

New Construction Condominium Project Pre-Approval Letter

A new construction condominium project pre-approval letter is a formal document from a lender indicating that a development meets specific financing guidelines. This certification is crucial because it confirms the project is warrantable, allowing buyers to secure traditional mortgages. Key factors reviewed include owner-occupancy ratios, homeowners association budgets, and insurance coverage. Obtaining this pre-approval minimizes financing risks, ensures a smoother closing process for units, and provides assurance to lenders that the structural and financial health of the entire condominium complex is stable and compliant with industry standards.

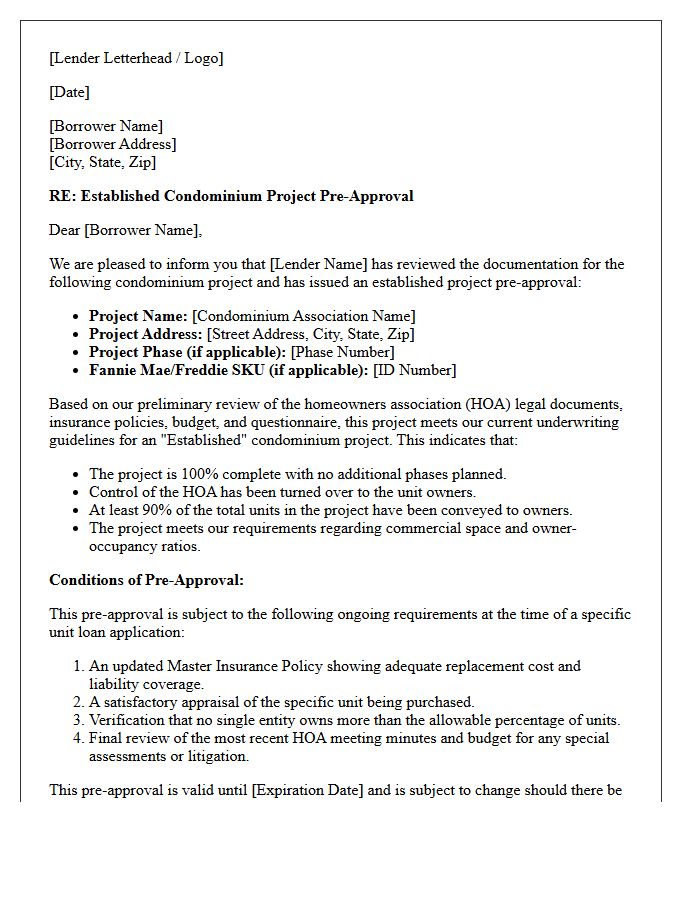

Established Condominium Project Pre-Approval Letter

An Established Condominium Project Pre-Approval Letter is a formal document issued by a lender confirming that a specific condo development meets conventional financing standards. Unlike standard pre-approvals for borrowers, this letter verifies the project's financial health, insurance coverage, and owner-occupancy ratios. Having this document accelerates the mortgage process because it proves the building is already vetted for Fannie Mae or Freddie Mac guidelines. It provides buyers and agents certainty that the association is eligible for low-down-payment loans, reducing the risk of financing rejection during escrow.

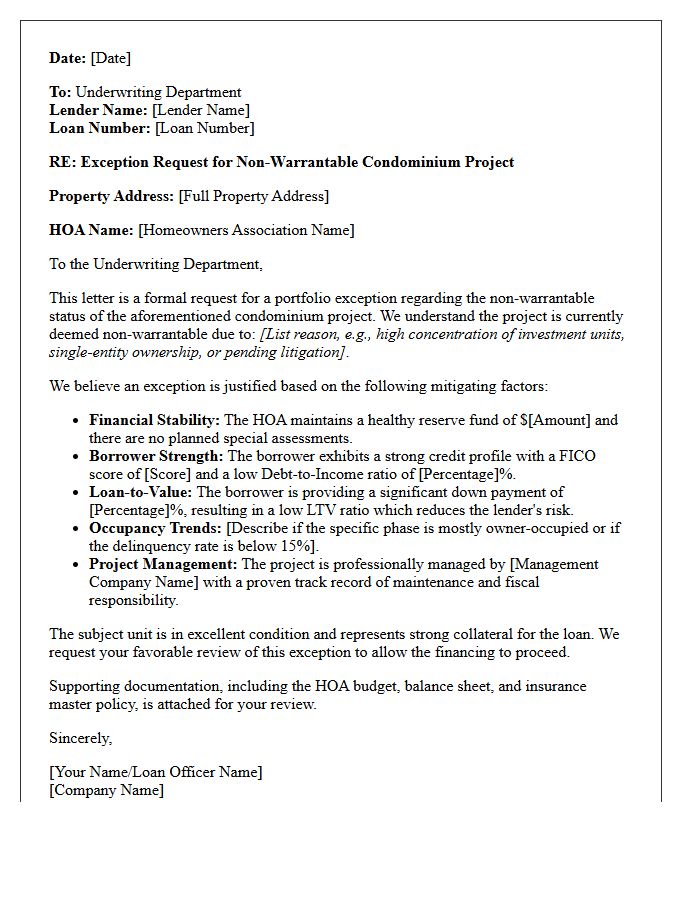

Non-Warrantable Condominium Project Exception Letter

A Non-Warrantable Condominium Project Exception Letter is a formal request sent to mortgage underwriters to approve financing for units that do not meet standard Fannie Mae or Freddie Mac guidelines. This exception request typically addresses issues like high investor concentration, pending litigation, or budget deficits. Lenders use this document to justify why a specific project remains a safe investment risk despite its non-warrantable status. Providing strong compensatory factors within the letter is essential for securing loan approval in complex real estate transactions.

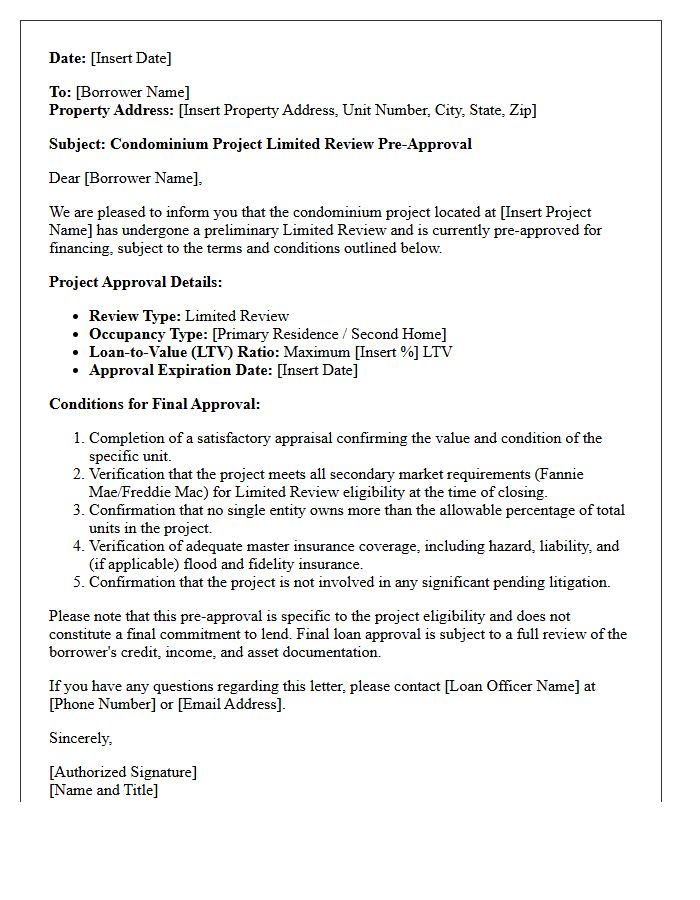

Condominium Project Limited Review Pre-Approval Letter

A Condominium Project Limited Review Pre-Approval Letter confirms that a specific condo development meets simplified eligibility criteria for conventional financing. This process focuses on the homeowners association's financial stability and insurance coverage rather than a full structural audit. It is typically available for established projects with high owner-occupancy rates and manageable budgets. Receiving this letter streamlines the mortgage approval process, giving buyers a significant advantage by verifying the property is "warrantable" before they make an official offer in a competitive real estate market.

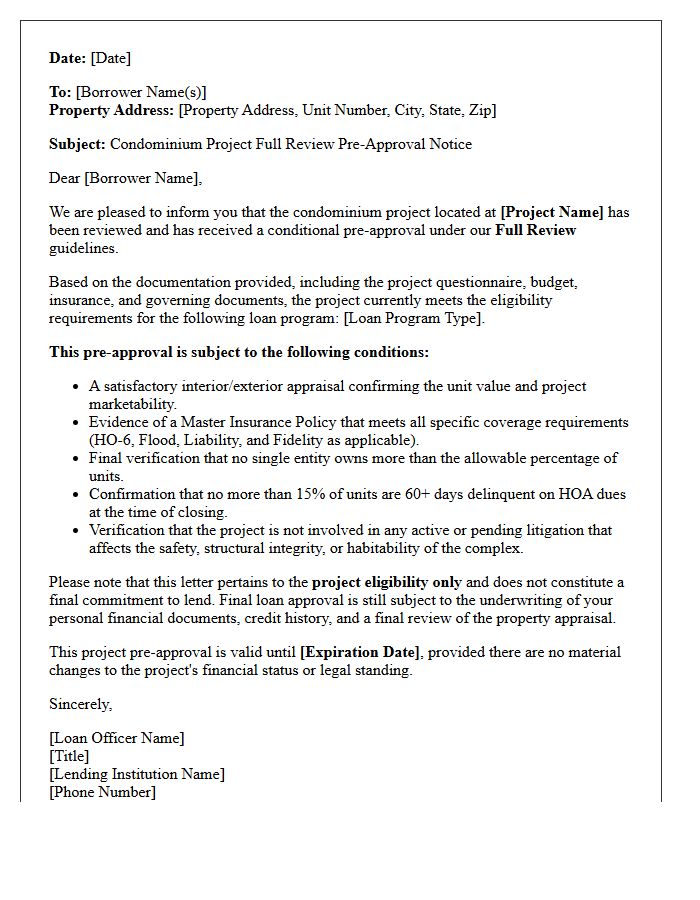

Condominium Project Full Review Pre-Approval Letter

A Condominium Project Full Review Pre-Approval Letter signifies that a lender has thoroughly vetted a development's financial stability, insurance coverage, and legal structure. Unlike a limited review, this comprehensive assessment ensures the homeowners association meets strict conforming loan guidelines set by Fannie Mae or Freddie Mac. Obtaining this document early is vital for buyers, as it confirms the project eligibility, reducing the risk of loan denial due to litigation, inadequate reserve funds, or excessive commercial space. It provides financing certainty for both the borrower and the seller during the real estate transaction.

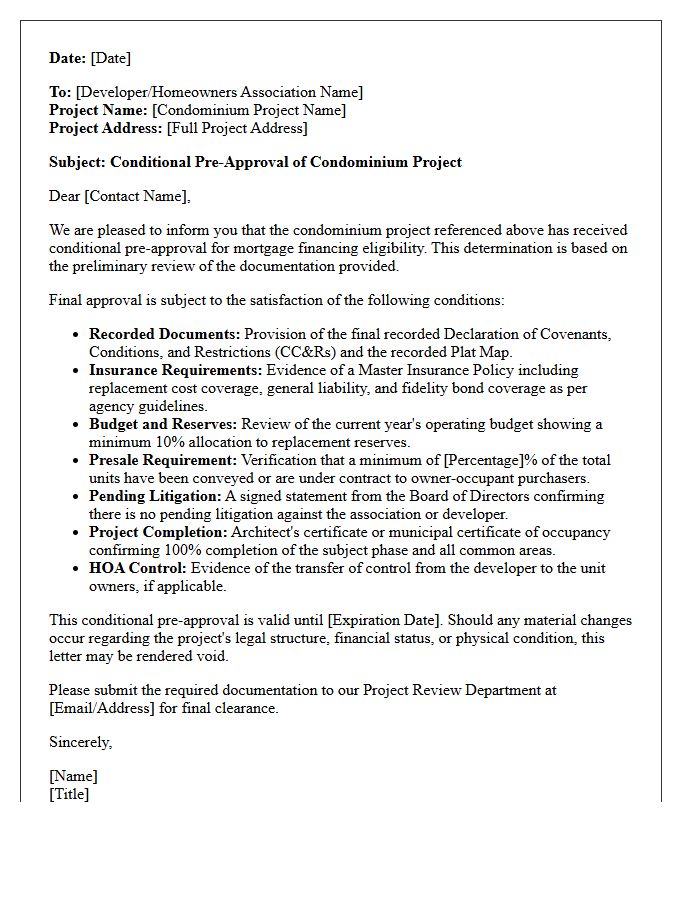

Condominium Project Pre-Approval Conditions Letter

A Condominium Project Pre-Approval Conditions Letter is a critical document issued by lenders indicating that a development meets specific underwriting guidelines. It outlines mandatory requirements such as owner-occupancy ratios, insurance coverage, and financial reserve standards. This letter ensures the homeowners association complies with secondary market regulations, like those from Fannie Mae or Freddie Mac. Obtaining this document is essential for buyers to secure financing, as it confirms the project is warrantable and minimizes the risk of loan denial during the final mortgage approval process.

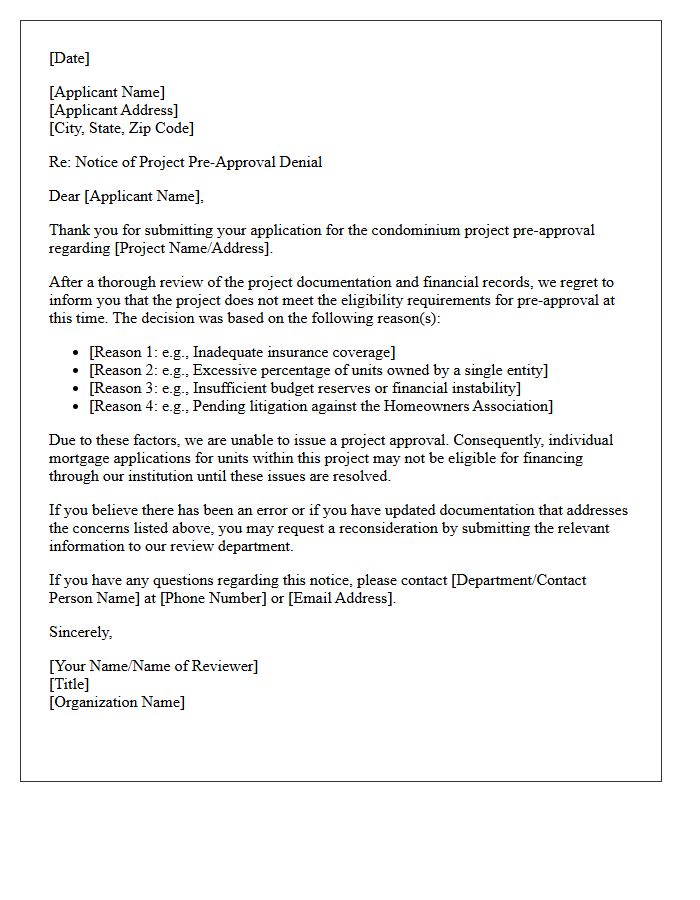

Condominium Project Pre-Approval Denial Letter

Receiving a Condominium Project Pre-Approval Denial Letter indicates that a residential complex fails to meet specific underwriting guidelines set by lenders or secondary market investors like Fannie Mae. Common reasons for rejection include excessive tenant-occupied units, inadequate insurance coverage, or ongoing structural litigation. This document is critical because it prevents buyers from securing traditional financing, often requiring a non-warrantable loan instead. Understanding the specific deficiency codes listed in the letter allows the HOA board to address compliance issues and restore the project's eligibility for future mortgage approvals.

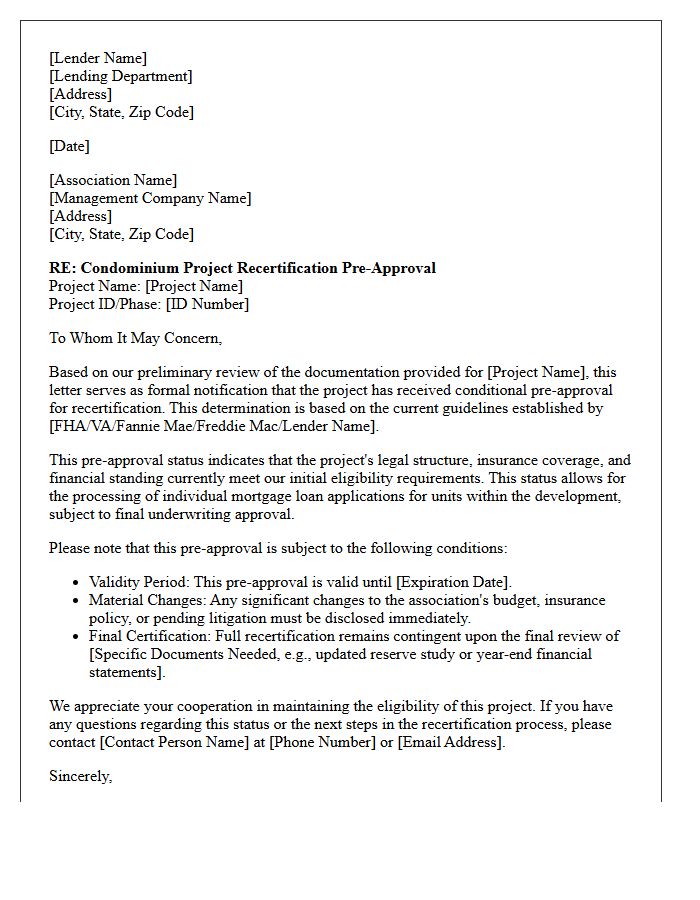

Condominium Project Recertification Pre-Approval Letter

A Condominium Project Recertification Pre-Approval Letter confirms that a homeowners association meets current secondary market standards. This document is essential for lenders to verify that a development maintains FHA or Fannie Mae eligibility regarding financial reserves, insurance coverage, and legal compliance. Obtaining this pre-approval streamlines the mortgage process for individual units by ensuring the entire project is deemed a secure investment. Without valid recertification, buyers may face higher interest rates or loan denials, making it a critical factor for both property values and financing accessibility.

What is a Condominium Project Specific Pre-Approval Letter?

A Condominium Project Specific Pre-Approval Letter is a document from a lender confirming that both the individual borrower and the specific condo association have been vetted and meet the necessary underwriting guidelines for a mortgage loan.

How does this differ from a standard mortgage pre-approval?

While a standard pre-approval only verifies a borrower's financial eligibility, a project-specific pre-approval also confirms that the condominium complex meets warrantability standards, including insurance coverage, owner-occupancy ratios, and financial reserve requirements.

Why do sellers require a project-specific letter for condo transactions?

Sellers and listing agents require this letter to ensure the building is "warrantable," meaning it qualifies for financing. This reduces the risk of the deal falling through due to building-related issues like pending litigation or inadequate budget reserves.

What criteria must a condo project meet to be included in the pre-approval?

To issue the letter, lenders typically review the condo's legal documents, insurance policies, and a completed HOA questionnaire to ensure no single entity owns too many units and that at least 10% of the budget is allocated to replacement reserves.

Can a project-specific pre-approval letter be used for different condo buildings?

No, this letter is unique to one specific development. If a buyer decides to make an offer on a unit in a different building, the lender must perform a new review of that specific association's documents before issuing a new pre-approval letter.

Comments