A Self-Employed Borrower Bank Statement Program Pre-Approval Letter verifies your purchasing power using personal or business deposits instead of traditional tax returns. This specialized financing solution helps entrepreneurs secure competitive mortgage terms by highlighting true cash flow. Gain a competitive edge in the real estate market by proving your creditworthiness through documented income history. Below are some ready to use templates.

Image cover: Professional Pre-Approval Letter Templates for Self-Employed Bank Statement Loans

Letter Samples List

- Self-Employed Borrower Bank Statement Program Pre-Approval Letter

- Twelve-Month Bank Statement Program Pre-Approval Letter

- Twenty-Four Month Bank Statement Mortgage Pre-Approval Letter

- Business Bank Statement Loan Pre-Approval Letter

- Personal Bank Statement Mortgage Pre-Approval Letter

- Self-Employed Alternative Documentation Pre-Approval Letter

- Non-Qualified Mortgage Bank Statement Program Pre-Approval Letter

- Entrepreneur Bank Statement Mortgage Pre-Approval Letter

- Independent Contractor Bank Statement Pre-Approval Letter

- Self-Employed Income Verification Bank Statement Pre-Approval Letter

- Freelancer Bank Statement Program Pre-Approval Letter

- Bank Statement Program Conditional Pre-Approval Letter

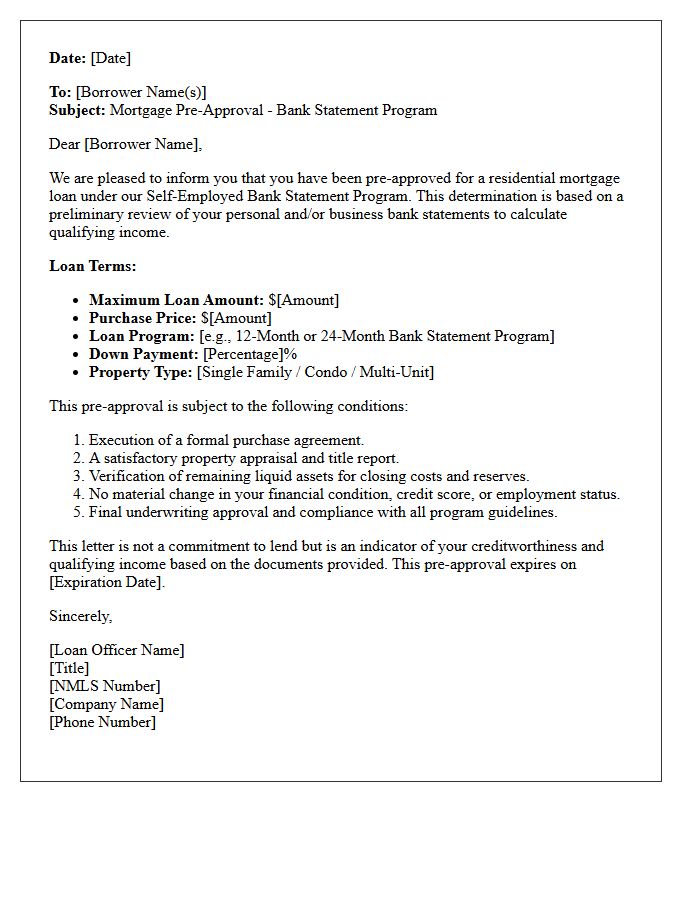

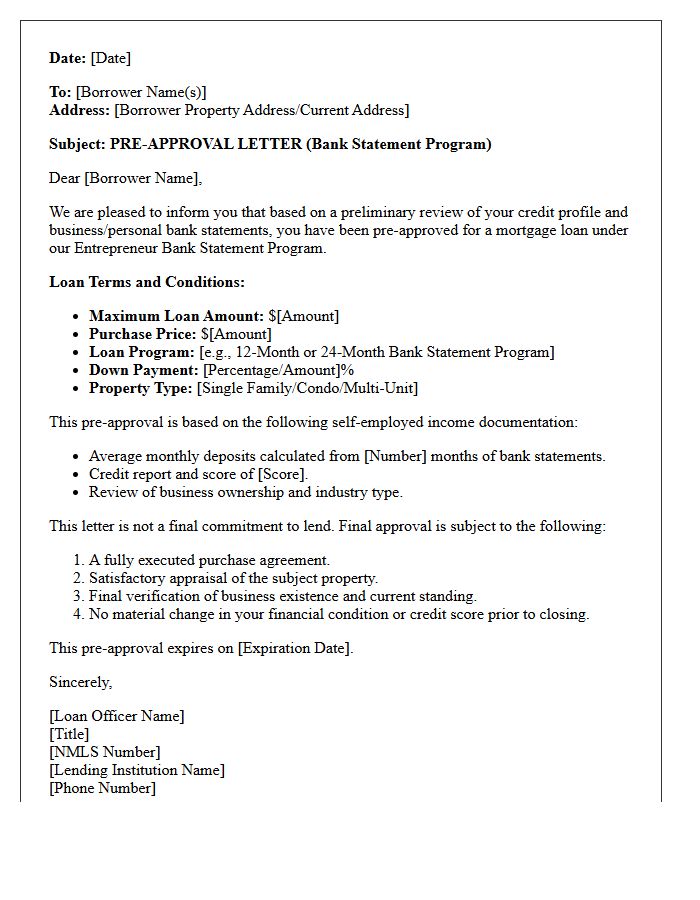

Self-Employed Borrower Bank Statement Program Pre-Approval Letter

A self-employed borrower bank statement program pre-approval letter confirms your purchasing power using bank statements rather than tax returns to verify income. This alternative document is essential for entrepreneurs with significant business write-offs. It demonstrates to sellers that a lender has analyzed your cash flow and monthly deposits to determine loan eligibility. Obtaining this letter early provides a competitive advantage in real estate transactions, proving you meet the specific debt-to-income requirements of non-QM lending without traditional 1040 forms.

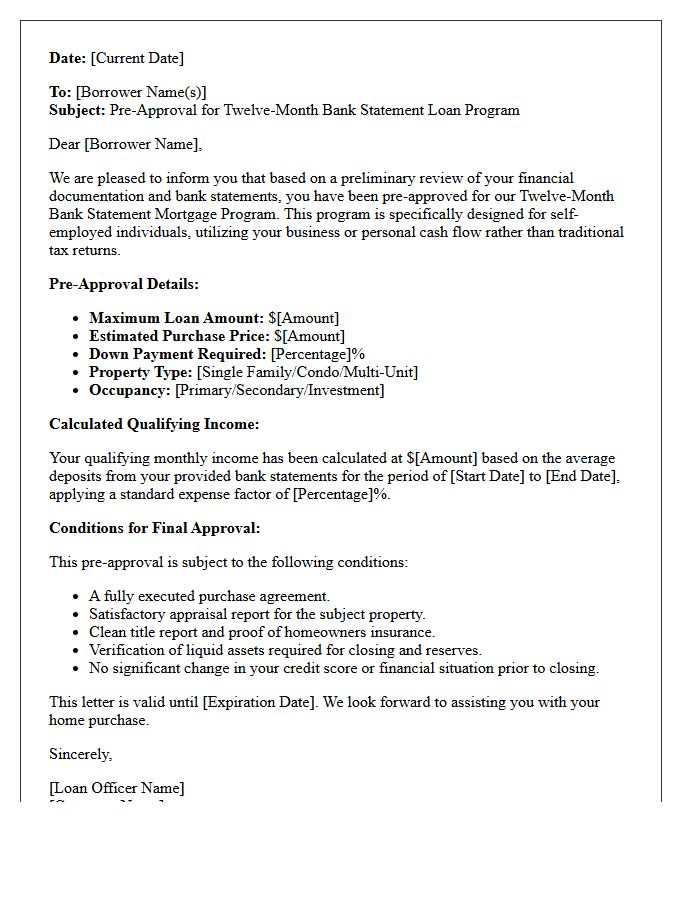

Twelve-Month Bank Statement Program Pre-Approval Letter

A Twelve-Month Bank Statement Program Pre-Approval Letter verifies a self-employed borrower's purchasing power based on cash flow rather than tax returns. To secure this document, lenders analyze one year of personal or business deposits to calculate qualifying income. This letter is a critical credential for entrepreneurs, proving financial credibility to sellers in a competitive real estate market. It confirms that the borrower meets specific liquidity requirements and credit standards, streamlining the path to homeownership without traditional employment documentation.

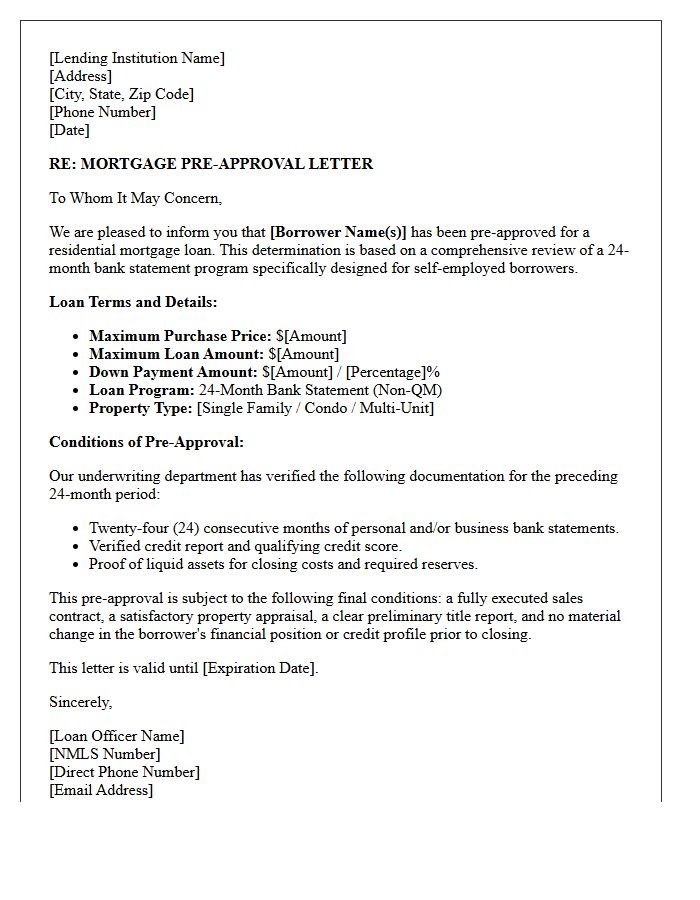

Twenty-Four Month Bank Statement Mortgage Pre-Approval Letter

A Twenty-Four Month Bank Statement Mortgage Pre-Approval Letter is a vital document for self-employed borrowers. Instead of traditional tax returns, lenders verify income consistency by analyzing two years of personal or business deposits. This letter confirms your borrowing power based on actual cash flow, making it essential for securing a home in competitive markets. It proves to sellers that you meet specific non-QM loan requirements despite having complex financial structures or significant business deductions. Securing this pre-approval ensures you are qualified for alternative financing before starting your property search.

Business Bank Statement Loan Pre-Approval Letter

A Business Bank Statement Loan Pre-Approval Letter serves as conditional proof that a lender has reviewed your cash flow and is willing to fund your enterprise. Unlike traditional financing, this process focuses on monthly deposits rather than tax returns or high credit scores. It outlines the maximum funding amount, estimated terms, and necessary closing conditions. Obtaining this letter early strengthens your negotiating position when purchasing equipment or securing real estate, demonstrating that your business has the liquidity required to manage debt obligations efficiently and professionally.

Personal Bank Statement Mortgage Pre-Approval Letter

A personal bank statement mortgage pre-approval letter is a crucial document for self-employed borrowers seeking home financing. Unlike traditional loans that require tax returns, lenders verify income by analyzing monthly deposits over a 12 to 24-month period. This alternative documentation proves your ability to repay based on actual cash flow rather than taxable profit. Obtaining this letter demonstrates financial stability to sellers, ensuring you are a qualified buyer ready to secure a property in a competitive real estate market.

Self-Employed Alternative Documentation Pre-Approval Letter

A self-employed alternative documentation pre-approval letter evaluates creditworthiness using bank statements instead of traditional tax returns. This stated income approach allows entrepreneurs to qualify based on actual cash flow and business deposits. It is a vital tool for non-QM lending, proving purchasing power to sellers while bypassing the complexities of net income deductions. To secure this letter, lenders typically analyze 12 to 24 months of personal or business banking activity to calculate a qualifying debt-to-income ratio.

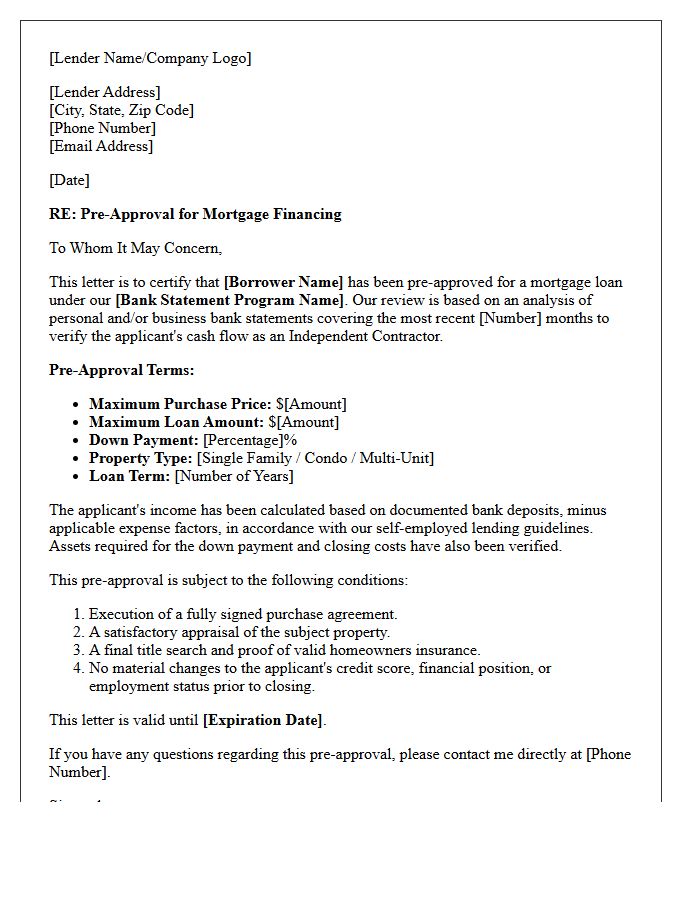

Non-Qualified Mortgage Bank Statement Program Pre-Approval Letter

A Non-Qualified Mortgage (Non-QM) bank statement program pre-approval letter validates your purchasing power without traditional tax returns. Lenders calculate income by analyzing 12 to 24 months of deposits to verify cash flow for self-employed borrowers. This document is essential for making competitive offers, proving you meet specific credit and reserve requirements. It signifies that a lender has reviewed your financial statements and is prepared to fund the loan based on your actual business earnings rather than net taxable income, ensuring a credible commitment to sellers during the home-buying process.

Entrepreneur Bank Statement Mortgage Pre-Approval Letter

For self-employed applicants, an Entrepreneur Bank Statement Mortgage Pre-Approval Letter is a vital tool that verifies purchasing power without traditional tax returns. Lenders analyze cash flow through twelve to twenty-four months of personal or business bank deposits to calculate qualifying income. This alternative documentation method proves financial stability for business owners who utilize significant legal tax deductions. Obtaining this letter ensures you are viewed as a qualified buyer, allowing you to compete effectively in the real estate market by demonstrating your actual liquidity and debt-to-income eligibility.

Independent Contractor Bank Statement Pre-Approval Letter

An Independent Contractor Bank Statement Pre-Approval Letter verifies mortgage eligibility using cash flow rather than tax returns. Lenders analyze twelve to twenty-four months of deposits to calculate qualifying income, bypassing complex business deductions. This non-QM loan product is essential for self-employed borrowers seeking to prove financial stability. Obtaining this letter provides a competitive advantage, confirming to sellers that your liquid assets and business revenue meet strict underwriting guidelines despite a non-traditional employment structure.

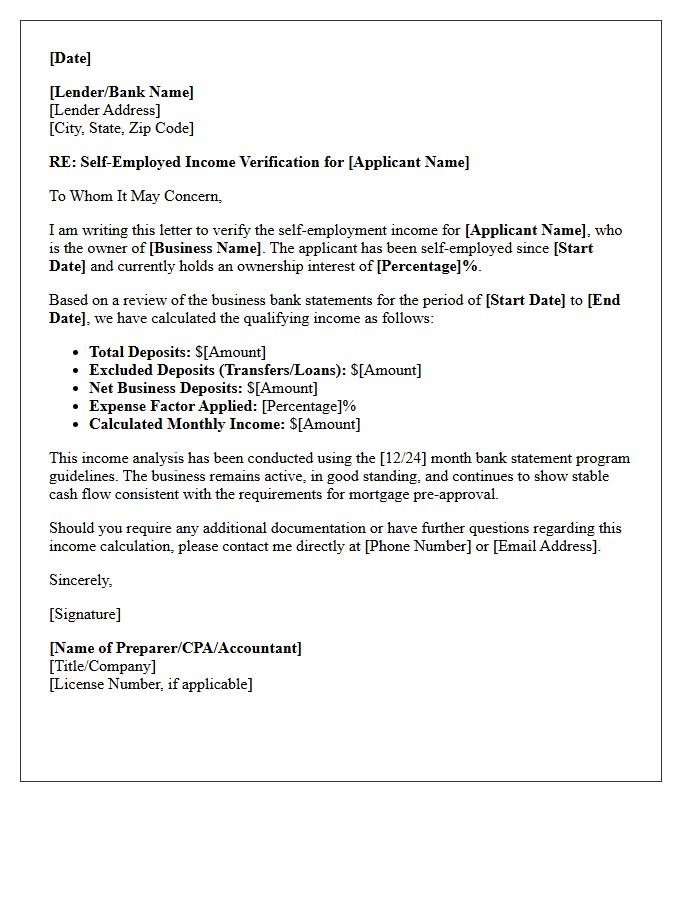

Self-Employed Income Verification Bank Statement Pre-Approval Letter

A Self-Employed Bank Statement Pre-Approval is a vital tool for business owners seeking a mortgage without traditional tax returns. Lenders evaluate your creditworthiness by analyzing 12 to 24 months of personal or business deposits to determine qualifying income. This process bypasses complex write-offs that often lower reported earnings. To secure a letter, ensure consistent cash flow and maintain organized records. This specialized financing provides a competitive advantage in real estate markets, proving your purchasing power to sellers while highlighting your financial stability as an entrepreneur.

Freelancer Bank Statement Program Pre-Approval Letter

A Freelancer Bank Statement Program Pre-Approval Letter is a crucial document for self-employed borrowers seeking a mortgage. Instead of traditional tax returns, lenders verify income using average monthly deposits from personal or business bank statements over 12 to 24 months. This letter confirms your purchasing power based on cash flow rather than net taxable income. Securing this pre-approval early ensures you meet lender-specific debt-to-income requirements, providing a competitive advantage when making offers on a home without standard W-2 documentation.

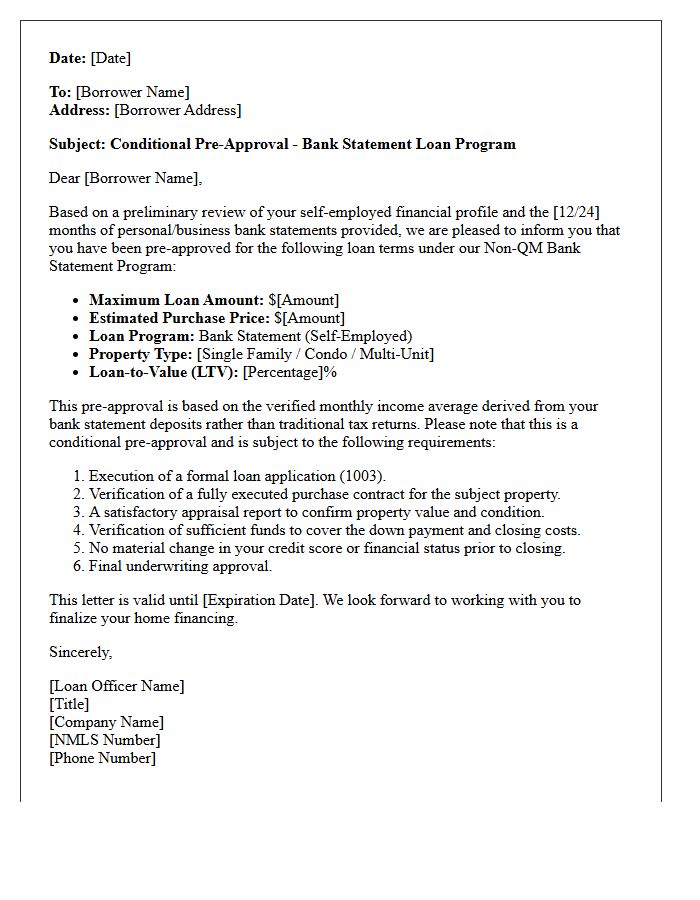

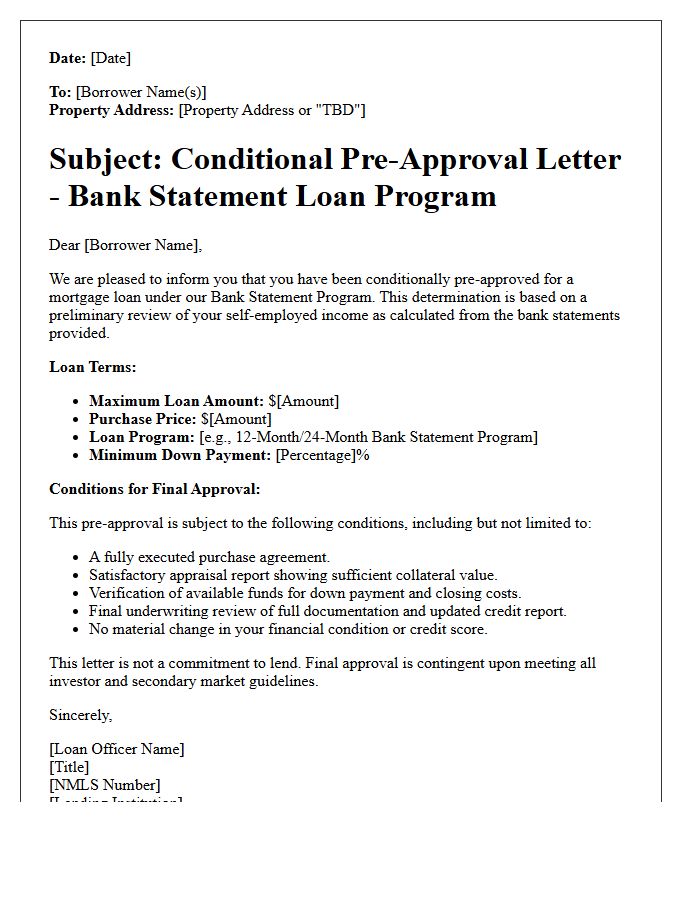

Bank Statement Program Conditional Pre-Approval Letter

A Bank Statement Program Conditional Pre-Approval Letter verifies a self-employed borrower's purchasing power based on bank deposits rather than tax returns. This essential document signals to sellers that a lender has reviewed your 12 to 24 months of statements and determined a qualifying income. It is conditional because final funding depends on a satisfactory property appraisal, a formal title search, and no significant changes to your credit profile. Obtaining this letter is a critical first step for non-QM loan applicants to prove financial credibility in competitive real estate markets.

What is a self-employed bank statement program pre-approval letter?

A bank statement program pre-approval letter is a document issued by a lender verifying that a self-employed borrower qualifies for a mortgage based on their business or personal bank deposits rather than tax returns. It indicates a specific loan amount the borrower is eligible for after a preliminary review of 12 to 24 months of bank statements.

How do lenders calculate income for a bank statement mortgage pre-approval?

Lenders calculate qualifying income by averaging the total eligible deposits shown over a 12 or 24-month period. For business bank statements, an expense factor (standard or CPA-certified) is applied to determine the net qualifying income, while personal bank statements often allow for 100% of the deposits to be counted.

What documents are required to get a pre-approval letter for a self-employed borrower?

To obtain a pre-approval letter, self-employed borrowers typically must provide 12 to 24 months of consecutive bank statements, a valid business license or letter from a CPA confirming the business has been active for at least two years, and a current government-issued ID. Unlike traditional loans, federal tax returns and W-2s are generally not required.

How long does it take to receive a bank statement loan pre-approval letter?

The timeline for a bank statement pre-approval usually ranges from 24 to 72 hours. This process takes slightly longer than a traditional pre-approval because a loan officer or underwriter must manually analyze every deposit across one to two years of statements to determine the official qualifying monthly income.

Does a bank statement pre-approval letter guarantee a mortgage loan?

A pre-approval letter is not a final loan commitment; it is a conditional offer based on an initial review of your credit and cash flow. Final mortgage approval is subject to a full underwriting review, a satisfactory property appraisal, and verification that the borrower's financial situation has not changed since the letter was issued.

Comments