A USDA Rural Development Pre-Approval Letter is a vital document confirming your eligibility for government-backed home financing in qualifying rural areas. It demonstrates your creditworthiness and purchasing power to sellers, ensuring a smoother homebuying process with zero down payment options. Securing this letter is the first step toward rural property ownership. Below are some ready to use template.

Image cover: USDA Rural Development Pre-Approval: Official Letter Samples and Professional Templates

Letter Samples List

- United States Department of Agriculture Rural Development Pre-Approval Letter

- United States Department of Agriculture Guaranteed Rural Housing Pre-Approval Letter

- Section 502 Guaranteed Rural Housing Loan Pre-Approval Letter

- Section 502 Direct Rural Housing Loan Pre-Approval Letter

- United States Department of Agriculture Single Family Housing Pre-Approval Letter

- Conditional United States Department of Agriculture Mortgage Pre-Approval Letter

- Verified United States Department of Agriculture Rural Development Pre-Approval Letter

- Zero Down Payment Rural Development Mortgage Pre-Approval Letter

- United States Department of Agriculture Income Eligibility Pre-Approval Letter

- United States Department of Agriculture Property Eligibility Pre-Approval Letter

- Preliminary Rural Development Mortgage Pre-Approval Letter

- Standard Rural Housing Program Pre-Approval Letter

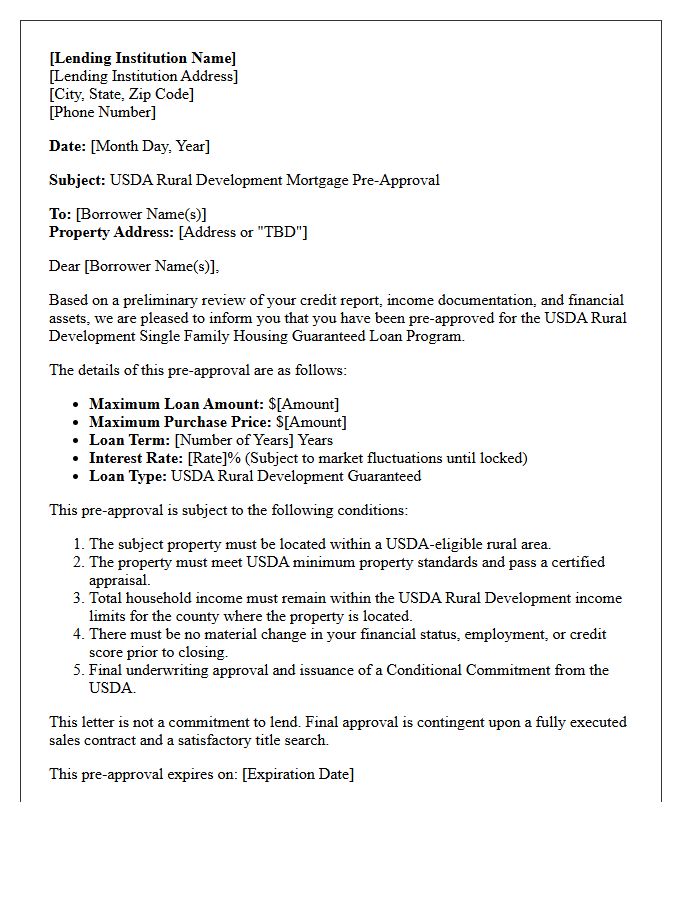

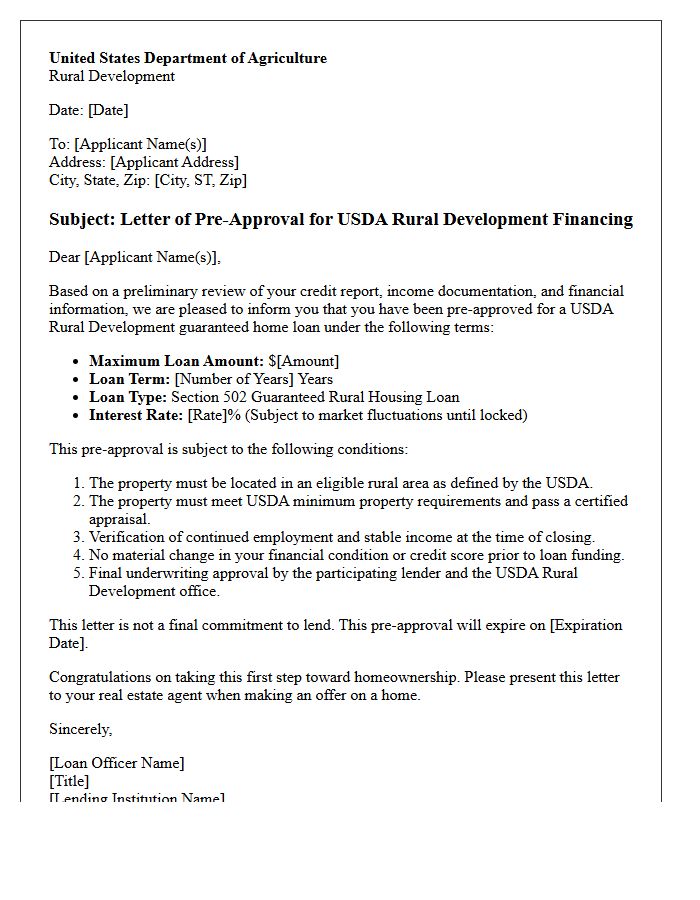

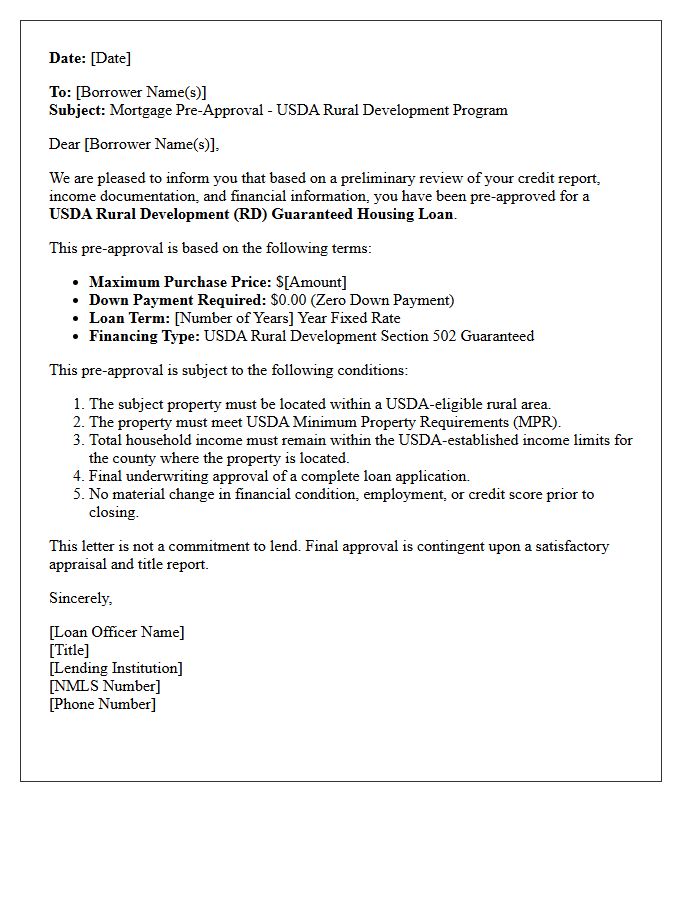

United States Department of Agriculture Rural Development Pre-Approval Letter

A USDA Rural Development pre-approval letter is a critical document verifying that a lender has evaluated your credit, income, and debt to determine your eligibility for a zero-down payment mortgage. It specifies the maximum loan amount you qualify for based on strict income limits and property location requirements. Obtaining this letter is the essential first step in the home-buying process, signaling to sellers that you are a qualified buyer capable of securing government-backed financing for properties in designated rural areas.

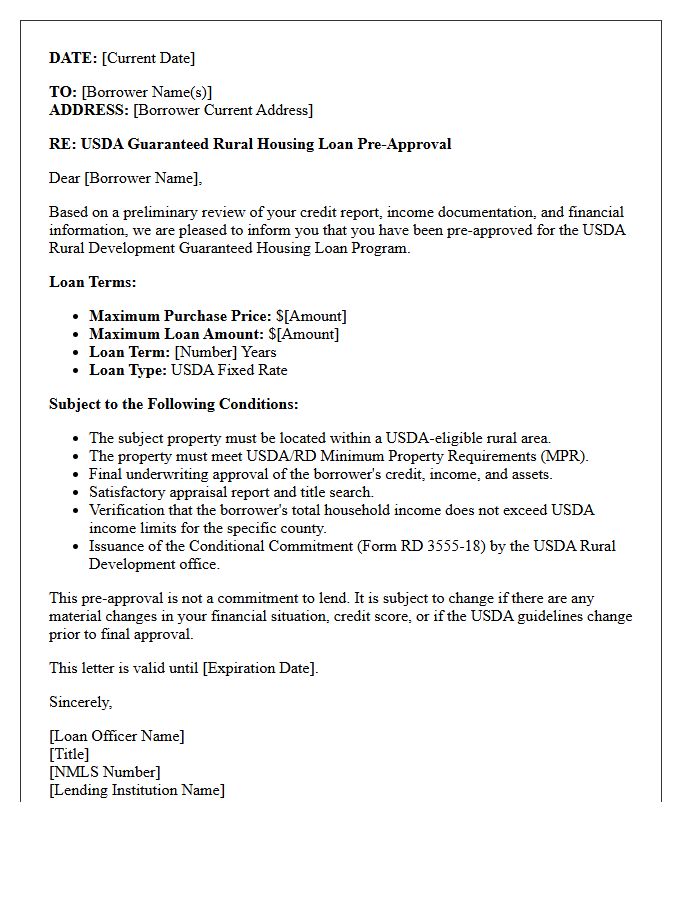

United States Department of Agriculture Guaranteed Rural Housing Pre-Approval Letter

A USDA pre-approval letter is a critical document confirming a lender's preliminary commitment to finance a home purchase in eligible rural areas. It verifies that a borrower meets specific income limits and credit requirements for the Guaranteed Rural Housing program. This letter demonstrates financial credibility to sellers, outlining the maximum loan amount authorized without a down payment. Obtaining this document is the essential first step in the home-buying process, ensuring the property meets geographic eligibility standards before an offer is made.

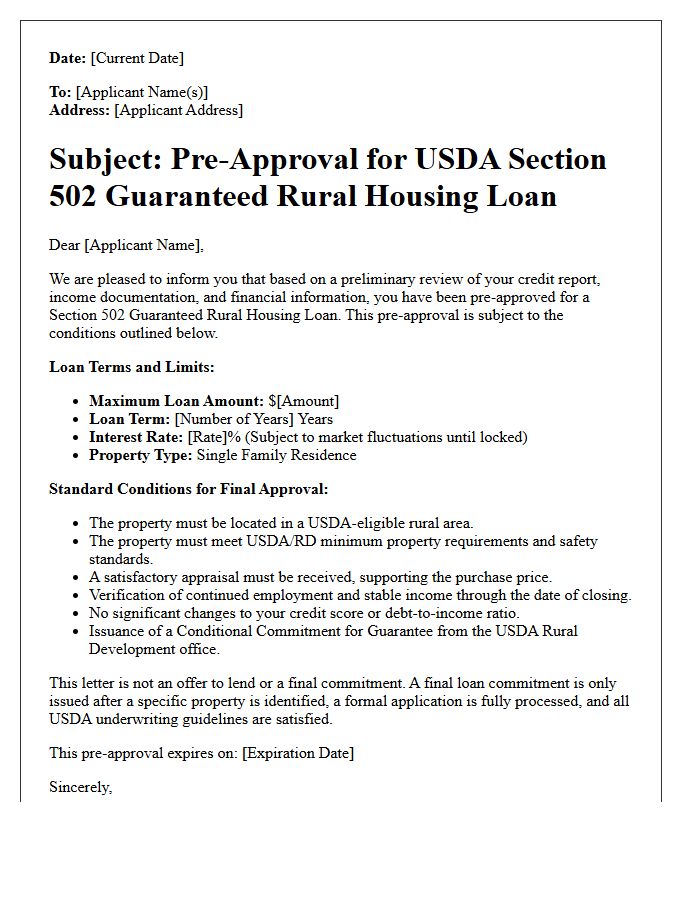

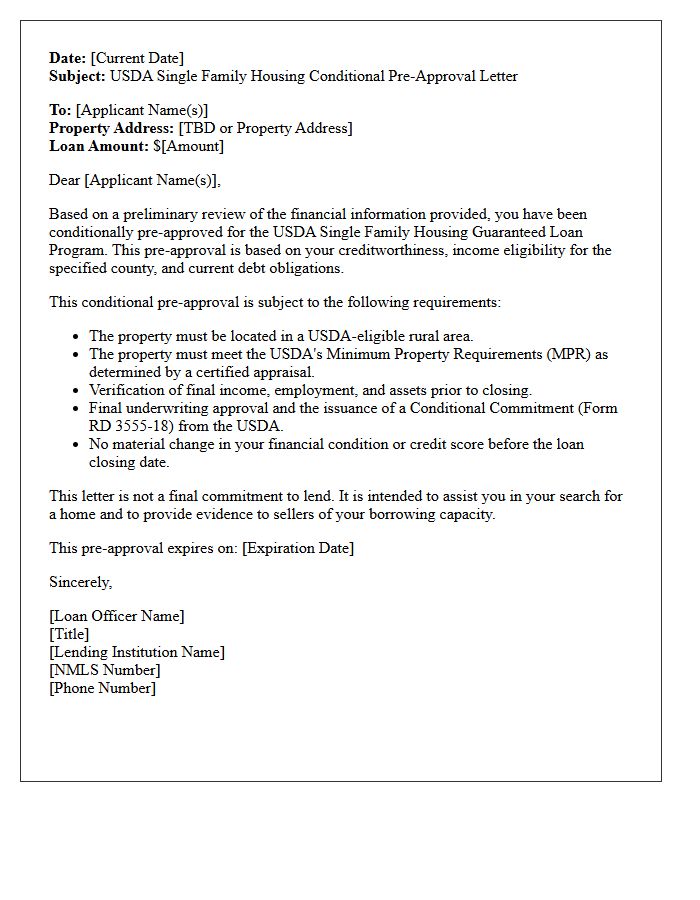

Section 502 Guaranteed Rural Housing Loan Pre-Approval Letter

A Section 502 Guaranteed Rural Housing Loan Pre-Approval Letter is a critical document confirming a lender's preliminary commitment to fund your home purchase. It validates that your income, credit, and debt-to-income ratio meet USDA eligibility requirements for low-to-moderate-income borrowers. This letter strengthens your position when making offers, proving you are a qualified buyer for properties in designated rural areas. It serves as a vital benchmark, outlining your maximum loan amount and estimated interest rate before you begin the formal underwriting process and final property appraisal.

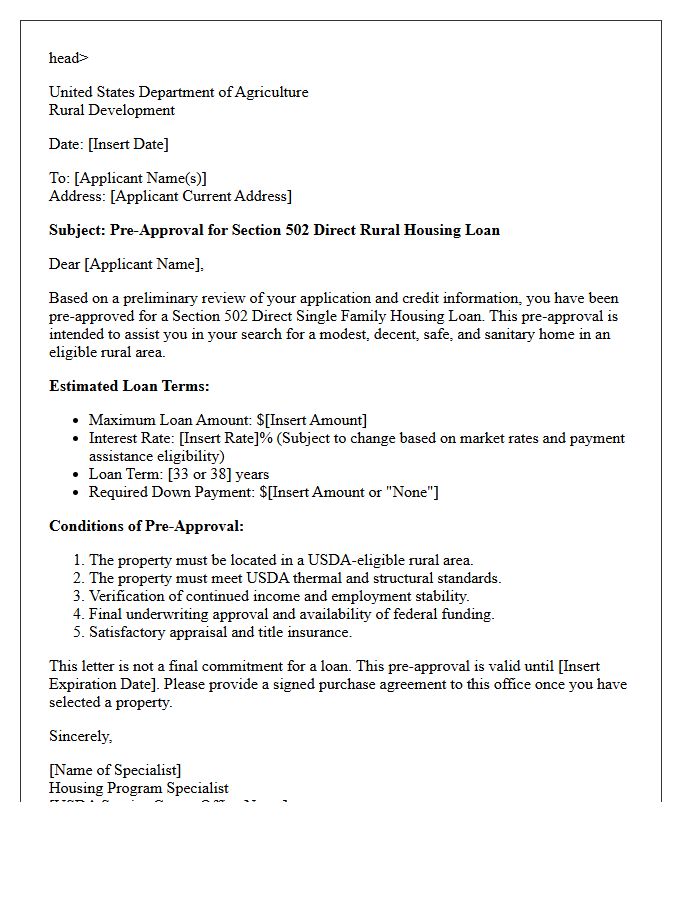

Section 502 Direct Rural Housing Loan Pre-Approval Letter

A Section 502 Direct Rural Housing Loan Pre-Approval Letter is a critical document issued by the USDA confirming a low-income applicant's potential eligibility for subsidized financing. It specifies a maximum loan amount based on household income, credit history, and debt ratios. This letter strengthens a buyer's position when making offers on modest, rural properties. However, it is not a final guarantee; the specific property must also meet USDA standards regarding location and condition before the loan receives final approval and funding.

United States Department of Agriculture Single Family Housing Pre-Approval Letter

A USDA Single Family Housing Pre-Approval Letter is a critical document confirming a borrower's preliminary eligibility for zero-down payment financing in rural areas. It signifies that a USDA-approved lender has verified your income, credit score, and debt-to-income ratio against strict federal guidelines. This letter strengthens your offer by proving financial backing for a Direct or Guaranteed loan. Remember, the property must be located within a designated eligible region and meet specific safety standards to finalize the mortgage process and secure your home.

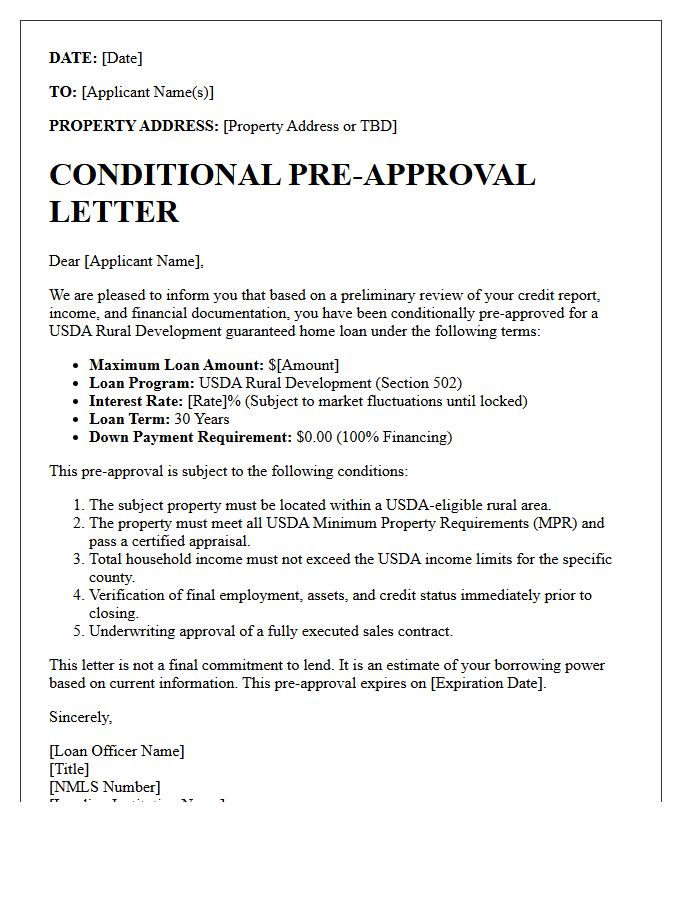

Conditional United States Department of Agriculture Mortgage Pre-Approval Letter

A Conditional USDA Mortgage Pre-Approval Letter is a critical document indicating a lender has reviewed your financial profile and determined you meet basic eligibility requirements. It outlines the estimated loan amount based on income, credit score, and debt ratios. However, final approval is contingent upon verifying your documentation and ensuring the specific property meets strict USDA location and safety standards. This letter strengthens your offer by proving to sellers that you are a qualified buyer ready to utilize this zero-down payment government-backed financing program.

Verified United States Department of Agriculture Rural Development Pre-Approval Letter

A verified USDA RD Pre-Approval Letter is a critical document confirming a borrower meets specific credit, income, and property eligibility requirements. Unlike a basic pre-qualification, this letter signifies that a lender has thoroughly vetted your financial documentation. It demonstrates to sellers that you are a serious buyer backed by a government-guaranteed loan program offering zero down payment. This conditional commitment strengthens your negotiating power in competitive rural markets, ensuring the home meets USDA safety standards and the location qualifies for financing under rural development guidelines.

Zero Down Payment Rural Development Mortgage Pre-Approval Letter

A Zero Down Payment Rural Development Mortgage Pre-Approval Letter is a critical document for buyers targeting homes in eligible rural areas. Issued by lenders, it confirms you meet the USDA income and credit requirements for 100% financing. This letter strengthens your offer by proving financial readiness to sellers. To obtain one, you must demonstrate stable employment and a debt-to-income ratio that fits program guidelines. Securing this pre-approval is the first step toward purchasing a home with no money down while benefiting from low mortgage insurance rates and fixed-interest terms.

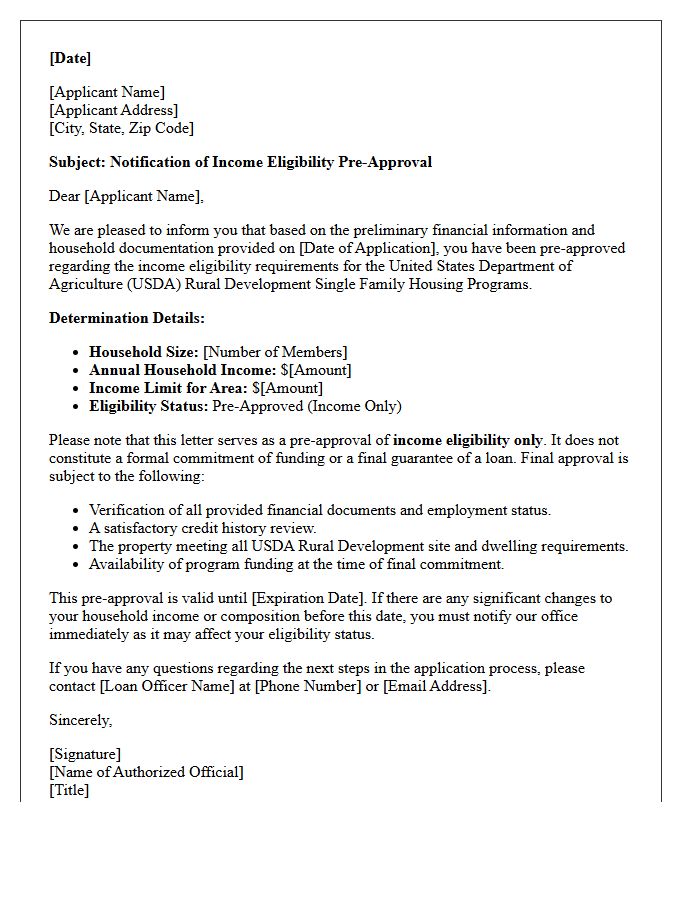

United States Department of Agriculture Income Eligibility Pre-Approval Letter

A USDA pre-approval letter verifies your income eligibility for low-to-moderate income housing programs. It confirms that your household earnings fall within specific county limits while meeting credit and debt-to-income requirements. This document is essential for securing a no-down-payment mortgage, demonstrating to sellers that you are a qualified buyer for properties in designated rural areas. Obtaining this letter is the primary step in leveraging government-backed financing to achieve affordable homeownership with favorable interest rates.

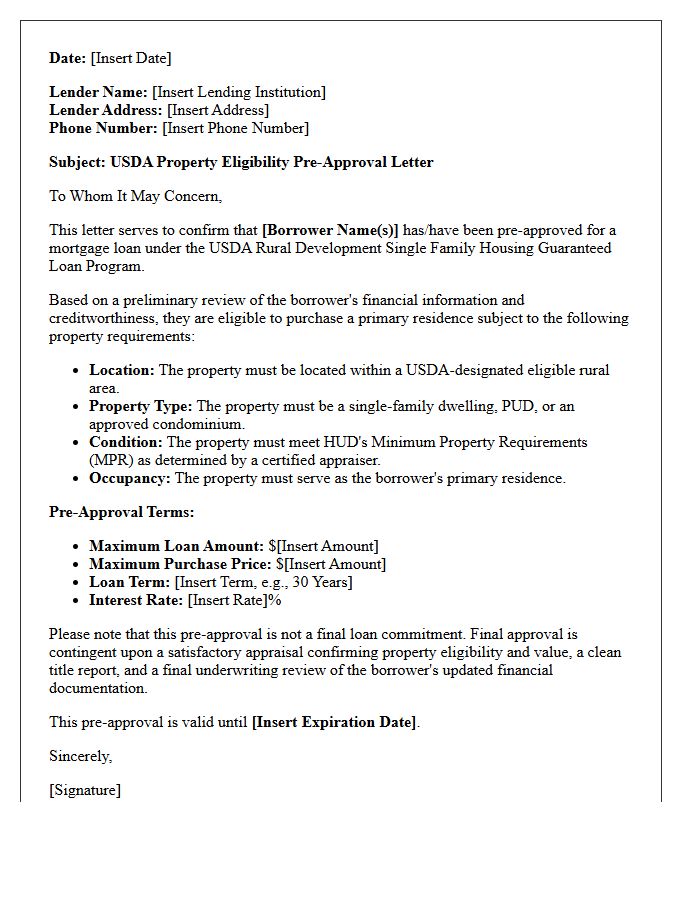

United States Department of Agriculture Property Eligibility Pre-Approval Letter

A USDA Property Eligibility Pre-Approval Letter confirms that a specific home meets the geographic and structural requirements for government-backed financing. Unlike a standard buyer pre-approval, this document verifies that the dwelling is located within a designated rural area and adheres to agency safety standards. It is a critical step for borrowers using the Single Family Housing Guaranteed Loan Program, ensuring the collateral qualifies before the final underwriting phase. Obtaining this letter reduces the risk of financing falling through during the closing process due to location or property condition issues.

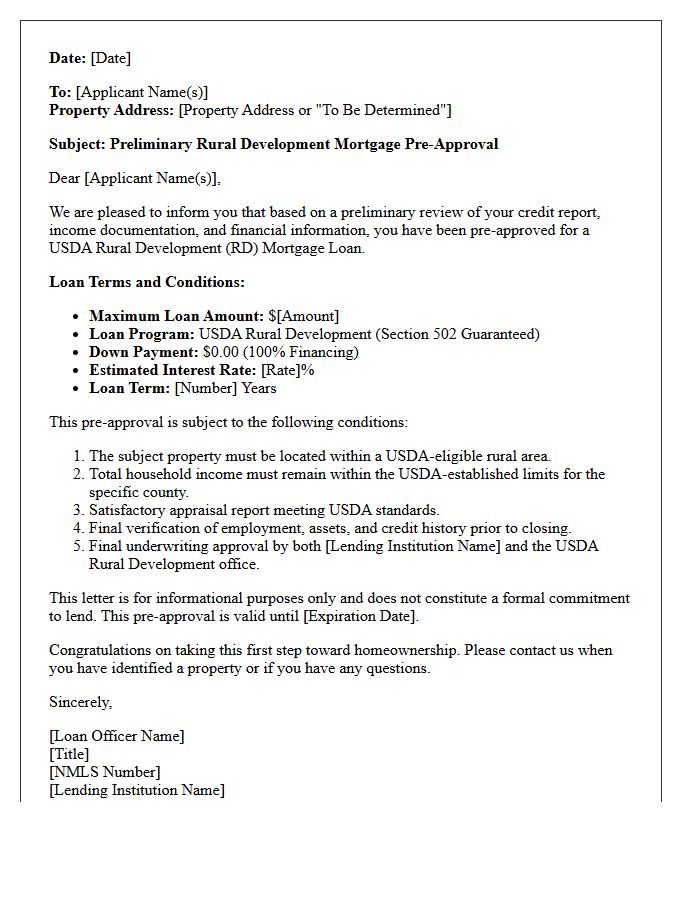

Preliminary Rural Development Mortgage Pre-Approval Letter

A preliminary rural development mortgage pre-approval letter is a document from a lender indicating you are likely eligible for a USDA loan. It confirms that both your income and the specific property location meet strict government guidelines for rural housing assistance. This letter strengthens your offer by proving financial backing for a zero-down payment mortgage. However, it is not a final guarantee; your application must still pass rigorous underwriting and federal funding availability checks before closing the deal on your suburban or rural home.

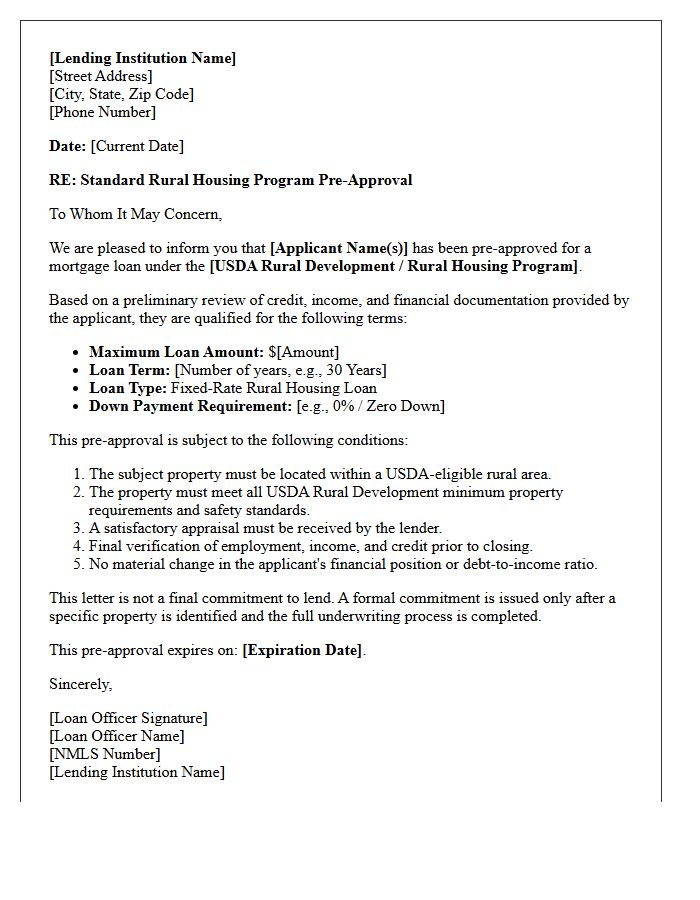

Standard Rural Housing Program Pre-Approval Letter

A Standard Rural Housing Program Pre-Approval Letter is a formal document from a lender indicating you qualify for a USDA loan. It confirms your eligibility based on creditworthiness and income limits specific to rural development guidelines. This letter is essential when making an offer, as it proves to sellers you have secured 100% financing with no down payment requirements. Ensure the property is located in a designated eligible area and that your debt-to-income ratio meets program standards to maintain the validity of your pre-approval during the home search process.

What is a USDA Rural Development Pre-Approval Letter?

A USDA Rural Development Pre-Approval Letter is an official document from a mortgage lender indicating that a homebuyer meets the preliminary credit and income guidelines for a USDA Section 502 Guaranteed Rural Housing Loan.

How do I qualify for a USDA loan pre-approval?

To qualify, applicants must meet specific income eligibility limits based on household size, possess a stable credit history (typically a 640 minimum score for automated underwriting), and intend to purchase a primary residence in a USDA-designated rural area.

Does a USDA pre-approval letter guarantee a mortgage?

No, a pre-approval letter is not a final commitment. The loan is subject to a satisfactory property appraisal, a determination that the home is in an eligible rural area, and final review of the applicant's financial documentation by both the lender and the USDA.

How long is a USDA Rural Development Pre-Approval Letter valid?

A USDA pre-approval letter is typically valid for 60 to 90 days, depending on the lender's policy. If the timeframe expires before a purchase contract is signed, the lender will need to refresh the applicant's credit report and income documentation.

What is the difference between a USDA pre-qualification and a pre-approval?

A pre-qualification is a basic estimate based on unverified information, while a USDA pre-approval involves a comprehensive review of credit reports, pay stubs, and tax returns, providing a much stronger signal of a buyer's purchasing power to sellers.

Comments