A Bank Statement Loan Pre-Qualification Letter demonstrates a borrower's creditworthiness using personal or business deposits instead of traditional tax returns. This essential document provides sellers with proof that a self-employed professional or entrepreneur has the verified cash flow necessary to secure financing. It streamlines the home-buying process by confirming your buying power upfront. Below are some ready to use template options.

Image cover: Unlock Your Home Loan: Professional Bank Statement Pre-Qualification Letter Templates

Letter Samples List

- Self-Employed Bank Statement Loan Pre-Qualification Letter

- Twelve-Month Bank Statement Loan Pre-Qualification Letter

- Twenty-Four-Month Bank Statement Loan Pre-Qualification Letter

- Personal Account Bank Statement Loan Pre-Qualification Letter

- Business Account Bank Statement Loan Pre-Qualification Letter

- Non-QM Bank Statement Loan Pre-Qualification Letter

- Jumbo Bank Statement Loan Pre-Qualification Letter

- Independent Contractor Bank Statement Loan Pre-Qualification Letter

- Freelance Professional Bank Statement Loan Pre-Qualification Letter

- Real Estate Investor Bank Statement Loan Pre-Qualification Letter

- High Net Worth Bank Statement Loan Pre-Qualification Letter

- Commingled Funds Bank Statement Loan Pre-Qualification Letter

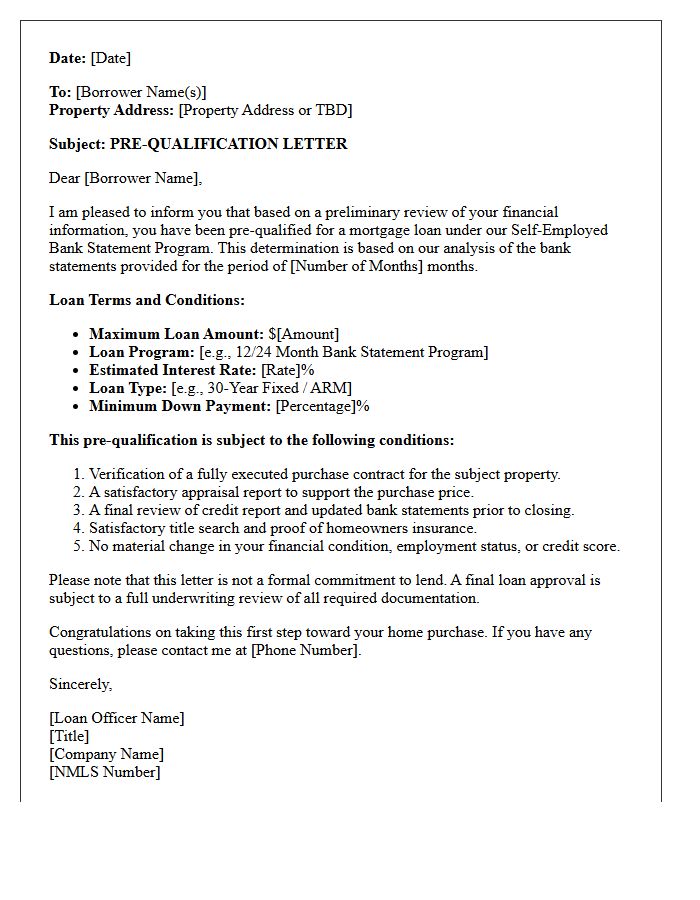

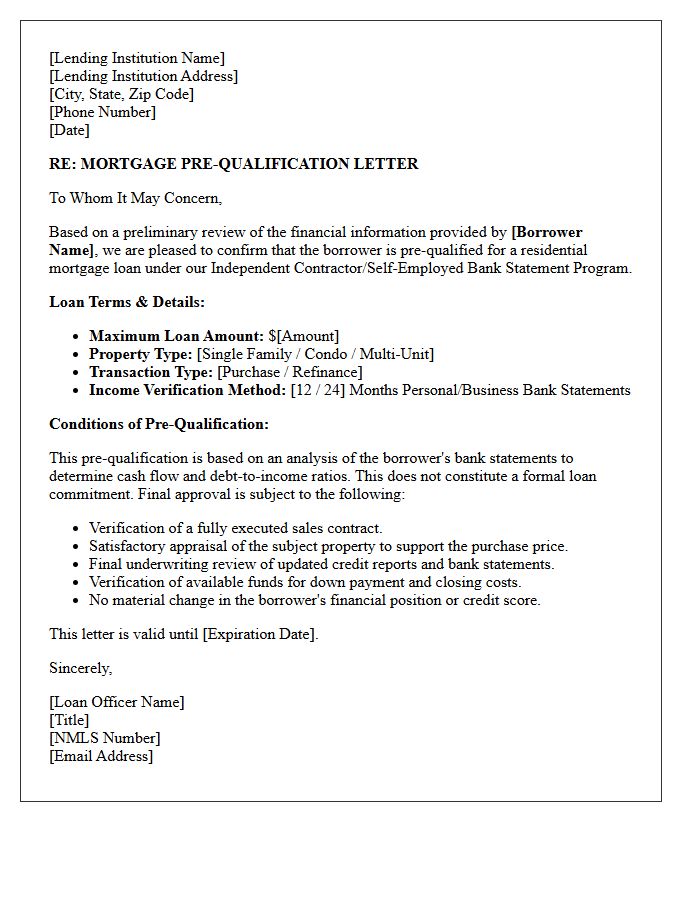

Self-Employed Bank Statement Loan Pre-Qualification Letter

A self-employed bank statement loan pre-qualification letter proves your borrowing power without traditional tax returns. Lenders evaluate your cash flow by analyzing monthly deposits into personal or business accounts over a 12 to 24-month period. This document is essential for entrepreneurs to demonstrate creditworthiness and secure a competitive edge when making offers on homes. It signifies that a lender has reviewed your liquid revenue and verified you meet specific debt-to-income requirements, streamlining the path to mortgage approval for non-traditional earners.

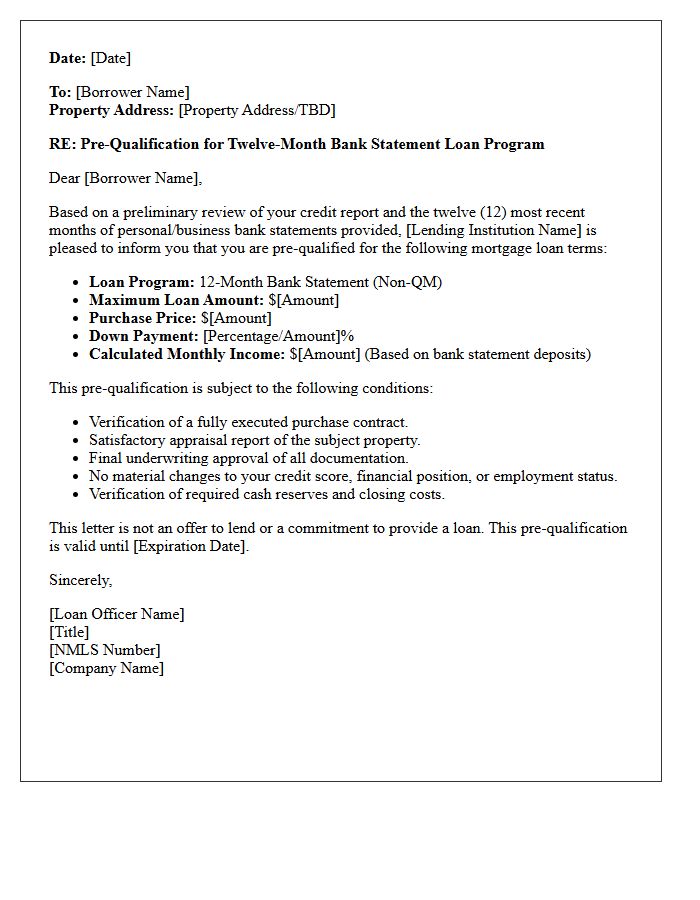

Twelve-Month Bank Statement Loan Pre-Qualification Letter

A Twelve-Month Bank Statement Loan Pre-Qualification Letter proves a self-employed borrower's creditworthiness without traditional tax returns. Lenders analyze a full year of deposits to calculate qualifying income, reflecting true cash flow. This document is essential for entrepreneurs and freelancers to verify purchasing power before making an offer on a home. Obtaining this letter early demonstrates financial readiness to sellers, confirming that a non-QM lender has reviewed consistent revenue patterns and credit scores to support the mortgage application process effectively.

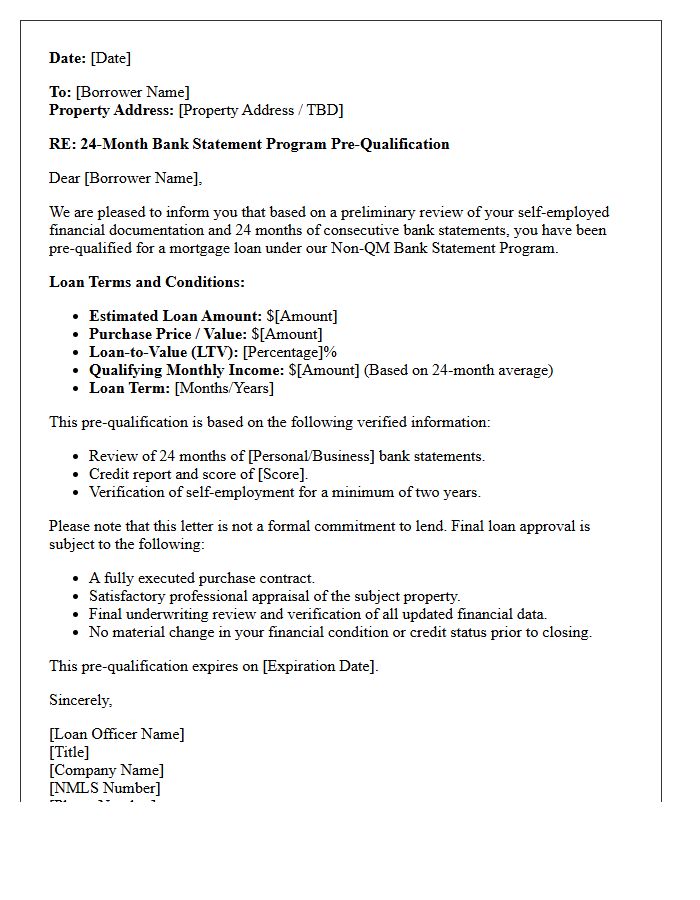

Twenty-Four-Month Bank Statement Loan Pre-Qualification Letter

A twenty-four-month bank statement loan pre-qualification letter proves your eligibility for non-QM mortgage financing based on self-employed cash flow. Instead of traditional tax returns, lenders analyze two years of deposits to calculate qualifying income. This document confirms a loan officer has reviewed your business or personal bank statements to determine a maximum loan amount. It is a critical tool for self-employed borrowers to demonstrate purchasing power to sellers, showing you meet specific credit scores and debt-to-income requirements without standard employment verification.

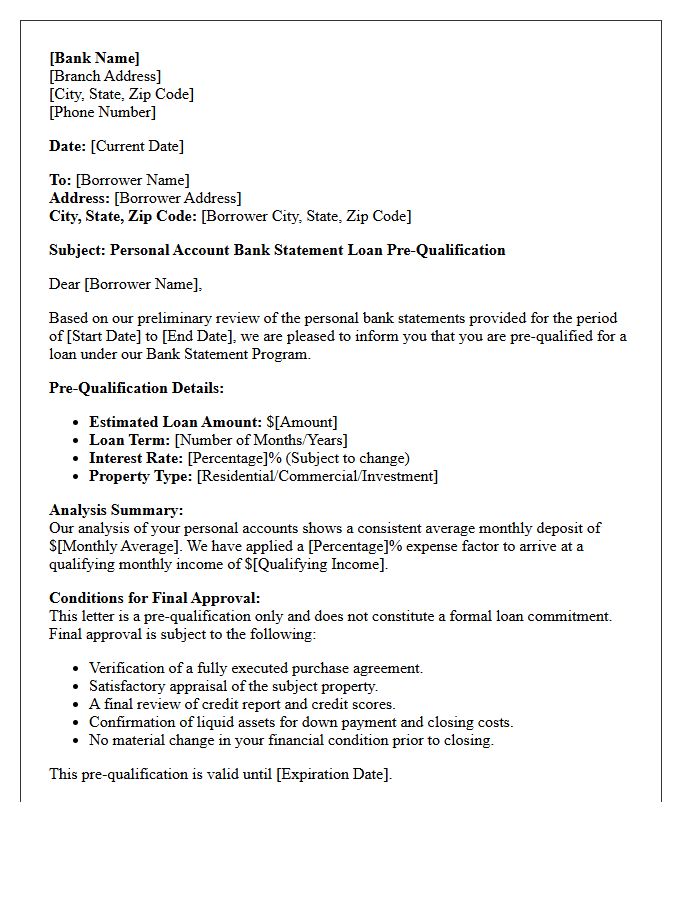

Personal Account Bank Statement Loan Pre-Qualification Letter

To secure a mortgage, lenders require a Personal Account Bank Statement to verify your liquidity and cash reserves. This documentation proves you have sufficient funds for a down payment and closing costs. Simultaneously, a Loan Pre-Qualification Letter acts as an initial estimate of your borrowing power based on self-reported data. Together, these documents demonstrate your financial readiness to sellers, strengthening your offer in a competitive market. Always ensure your statements are recent and reflect stable asset management to streamline the official approval process.

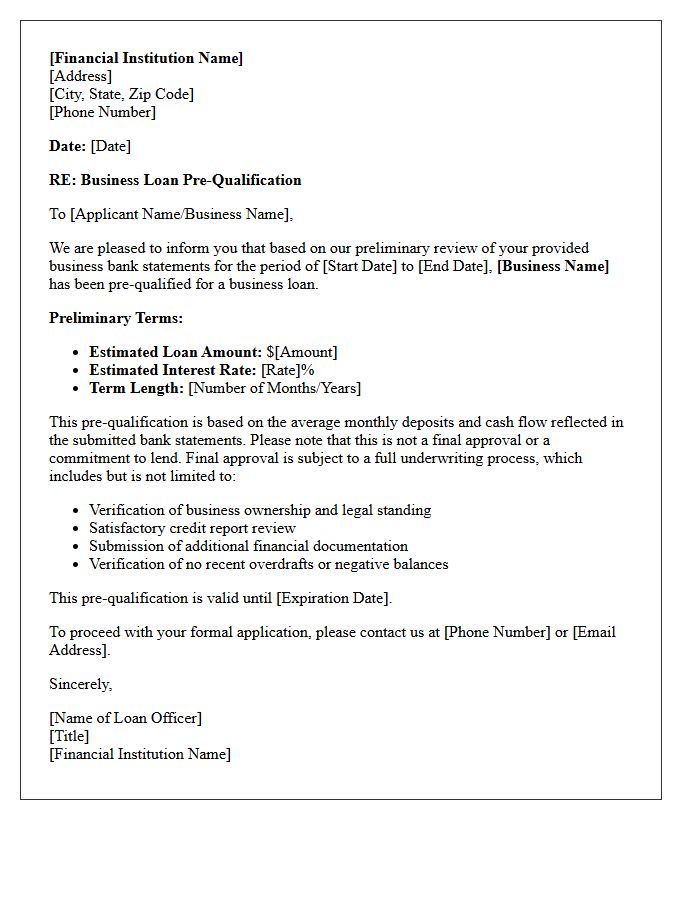

Business Account Bank Statement Loan Pre-Qualification Letter

A business bank statement serves as critical financial evidence of your company's cash flow, stability, and revenue patterns. Lenders analyze these documents to issue a loan pre-qualification letter, which estimates the funding amount you may receive. Maintaining consistent deposits and healthy balances is vital, as these statements verify your ability to manage debt. This preliminary letter strengthens your position when negotiating with sellers or vendors by proving creditworthiness. Always ensure your business account reflects accurate, transparent transactions to streamline the official approval process and secure the best possible financing terms.

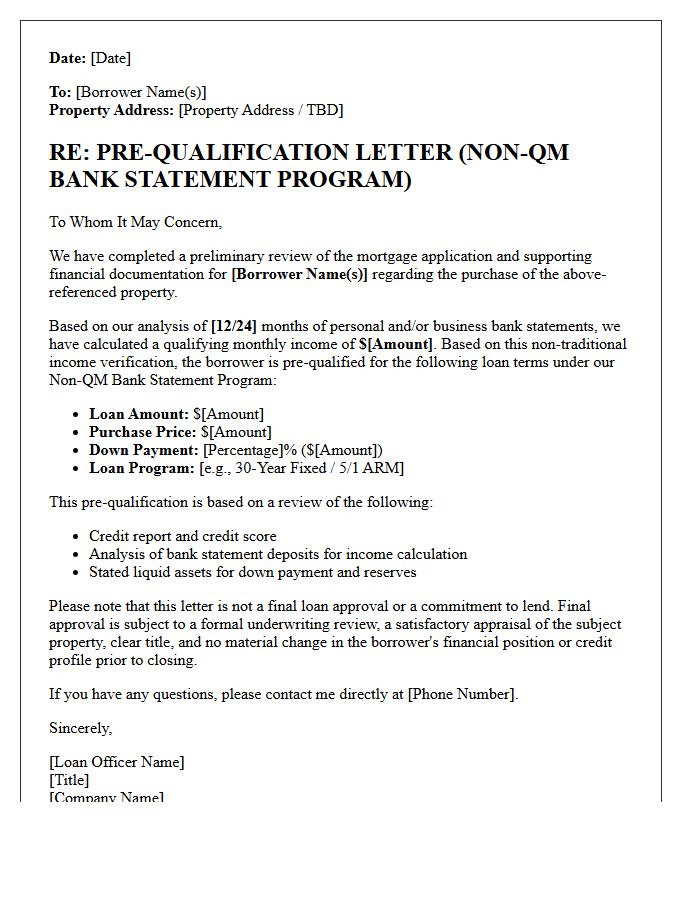

Non-QM Bank Statement Loan Pre-Qualification Letter

A Non-QM bank statement loan pre-qualification letter proves your creditworthiness by using personal or business deposits instead of tax returns. To secure this document, lenders calculate your qualifying income based on a 12 or 24-month average of bank statements. This letter is essential for self-employed borrowers to demonstrate purchasing power to sellers. It confirms you meet specific debt-to-income ratios and credit score requirements without traditional documentation. Always ensure your liquid assets are verified to strengthen your offer in a competitive real estate market.

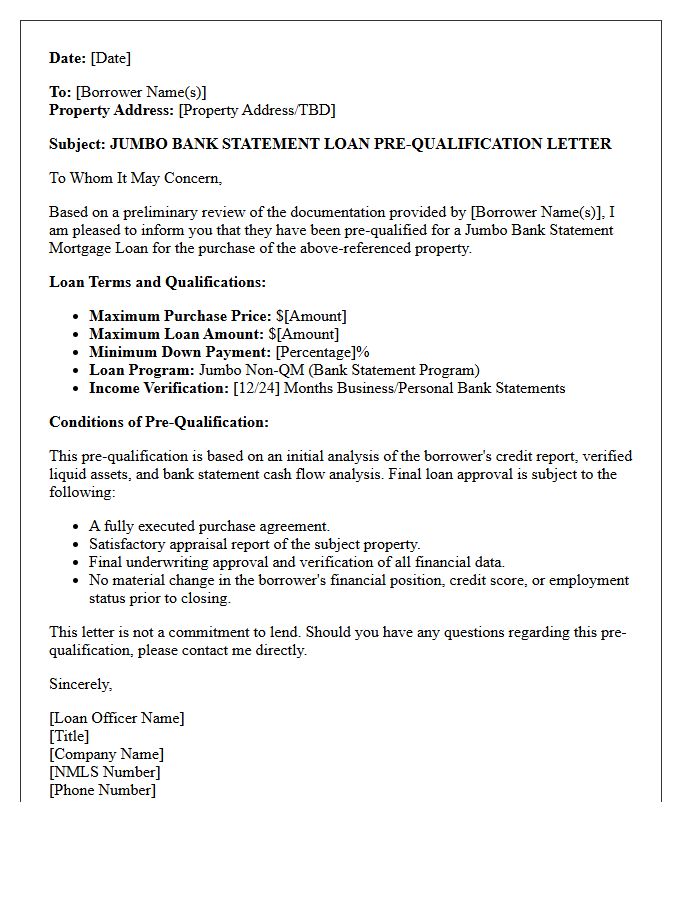

Jumbo Bank Statement Loan Pre-Qualification Letter

A Jumbo Bank Statement Loan Pre-Qualification Letter proves a self-employed borrower's creditworthiness without traditional tax returns. Lenders analyze 12 to 24 months of deposits to calculate qualifying income for high-balance financing. This document is essential for luxury homebuyers, signaling to sellers that the buyer meets specific liquidity and credit score requirements. Obtaining this letter ensures you understand your maximum purchasing power before making an offer on a premium property, streamlining the underwriting process by verifying cash flow and available reserves upfront in a competitive real estate market.

Independent Contractor Bank Statement Loan Pre-Qualification Letter

An Independent Contractor Bank Statement Loan Pre-Qualification Letter proves your creditworthiness using bank statements rather than tax returns. This document confirms a lender has verified your average monthly deposits to determine qualifying income. It is essential for self-employed borrowers to demonstrate mortgage eligibility when making offers on property. To obtain one, you must provide 12 to 24 months of business or personal records showing consistent cash flow. This letter serves as a preliminary approval, signaling to sellers that your alternative documentation meets specific non-QM loan requirements.

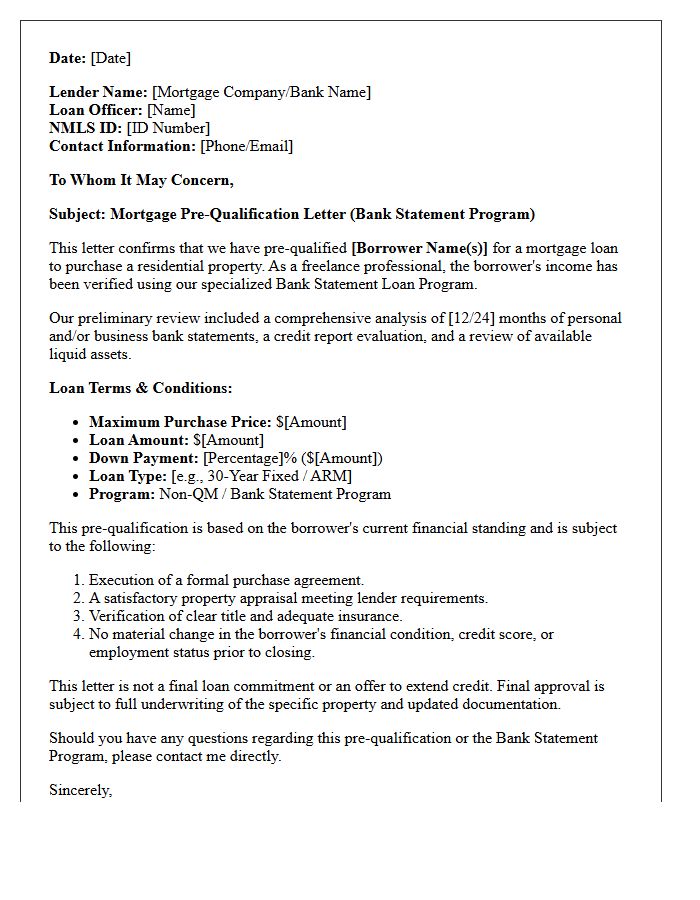

Freelance Professional Bank Statement Loan Pre-Qualification Letter

A Freelance Professional Bank Statement Loan Pre-Qualification Letter is a crucial document for self-employed borrowers seeking a mortgage without traditional tax returns. Lenders analyze cash flow directly from personal or business bank statements to determine eligibility. This letter proves you meet specific income requirements based on average monthly deposits rather than net profit. It provides credibility during the home-buying process, signaling to sellers that your alternative documentation has been verified by a lender, ensuring you are financially capable of securing a non-QM loan despite irregular income streams.

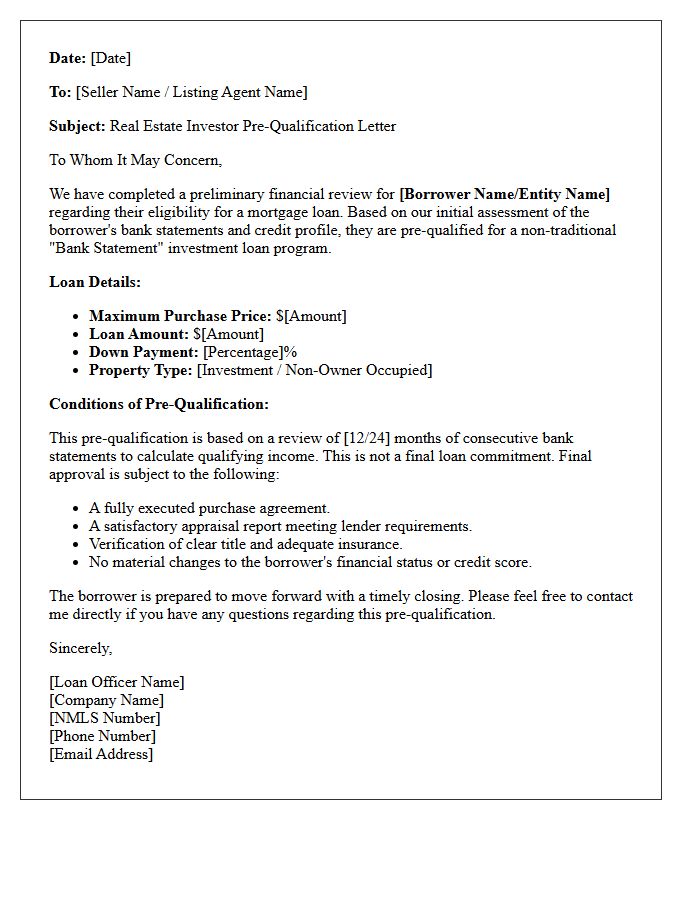

Real Estate Investor Bank Statement Loan Pre-Qualification Letter

A Bank Statement Loan Pre-Qualification Letter proves a real estate investor's purchasing power without using tax returns. Lenders verify liquidity and cash flow by analyzing 12 to 24 months of personal or business bank deposits to calculate qualifying income. This document is essential for self-employed borrowers seeking to secure investment properties quickly. It signals to sellers that the investor meets specific debt-to-income requirements based on actual revenue. Obtaining this letter is the critical first step in bypassing traditional income documentation hurdles to close competitive real estate deals.

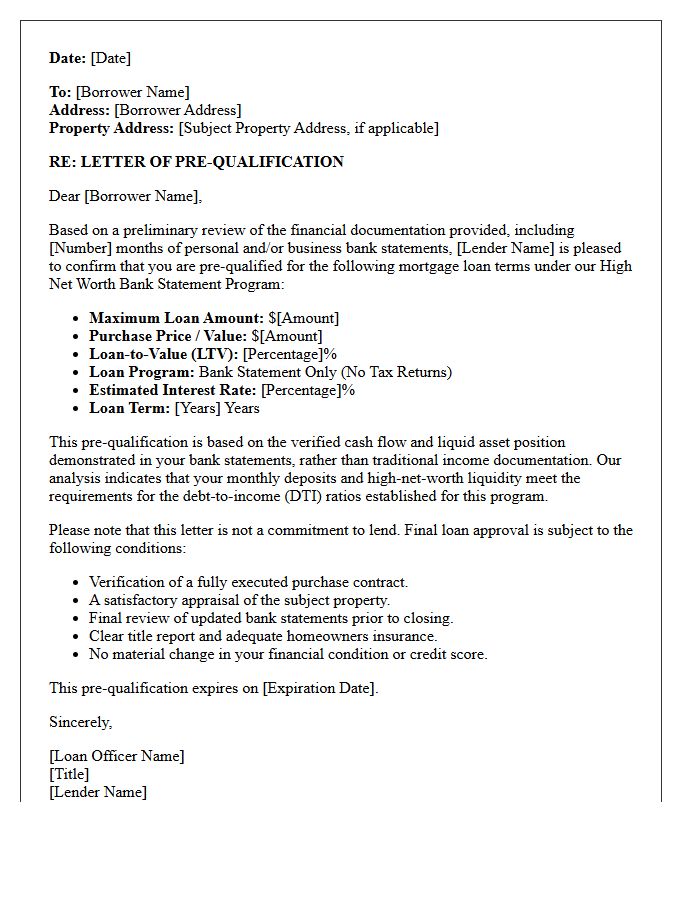

High Net Worth Bank Statement Loan Pre-Qualification Letter

A high net worth bank statement loan pre-qualification letter verifies your borrowing power based on liquid assets rather than traditional tax returns. This document confirms a lender has reviewed your asset depletion or cash flow history, signaling to sellers that you are a qualified buyer. It is a critical tool for self-employed investors or wealthy individuals needing to bypass strict income documentation requirements. Securing this letter ensures you can move quickly in competitive real estate markets by proving your financial credibility and ability to cover mortgage payments through substantial wealth reserves.

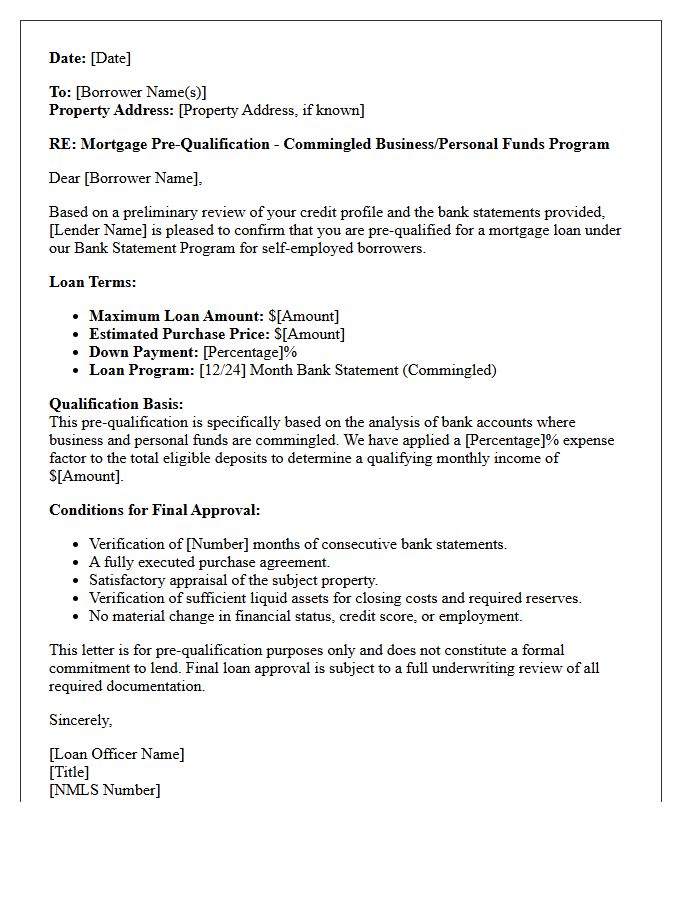

Commingled Funds Bank Statement Loan Pre-Qualification Letter

A Commingled Funds Bank Statement Loan Pre-Qualification Letter confirms a borrower's eligibility by analyzing combined personal and business income. Lenders review deposits across multiple accounts to calculate debt-to-income ratios without requiring traditional tax returns. It is essential to provide consecutive monthly statements to verify consistent cash flow. This document proves financial strength for self-employed individuals, though lenders often apply a standard expense factor to total deposits. Obtaining this letter early streamlines the home-buying process by establishing a clear maximum loan amount based on verified liquid assets.

What is a Bank Statement Loan Pre-Qualification Letter?

A Bank Statement Loan Pre-Qualification Letter is an official document from a lender indicating that a self-employed borrower likely qualifies for a mortgage based on a preliminary review of their business or personal bank deposits rather than tax returns.

How do I qualify for a bank statement mortgage pre-qualification?

To qualify, you typically need to provide 12 to 24 months of consecutive bank statements, maintain a specific minimum credit score (usually 620 or higher), and demonstrate a consistent history of self-employment for at least two years.

Does a pre-qualification letter for a bank statement loan guarantee financing?

No, a pre-qualification letter is not a binding commitment. It is an estimate of borrowing power based on unverified data; final loan approval requires a full underwriter review of credit, assets, and a property appraisal.

What income is used for a bank statement loan pre-qualification?

Lenders calculate qualifying income by averaging the total eligible deposits shown in your bank statements over a 12 or 24-month period, often applying a standard expense ratio to determine the net effective income for the loan.

How long is a bank statement loan pre-qualification letter valid?

Most bank statement loan pre-qualification letters are valid for 60 to 90 days. If the timeframe expires before you find a property, you may need to provide your most recent two months of bank statements to refresh the letter.

Comments