Securing a mortgage on a fixed income requires a specialized Fixed-Income Retiree Pre-Qualification Letter to verify your purchasing power. This document validates pension, Social Security, and investment distributions to strengthen your offer in a competitive market. Understanding how lenders evaluate non-employment revenue is essential for a smooth home-buying journey. To help you get started, below are some ready to use template.

Image cover: Securing Your Mortgage: Pre-Qualification Guide and Templates for Fixed-Income Retirees

Letter Samples List

- Standard Fixed-Income Retiree Pre-Qualification Letter

- Pension Based Retiree Mortgage Pre-Qualification Letter

- Social Security Income Retiree Pre-Qualification Letter

- Retirement Account Drawdown Pre-Qualification Letter

- Annuity Income Mortgage Pre-Qualification Letter

- High Equity Retiree Pre-Qualification Letter

- Fixed-Income Guarantor Pre-Qualification Letter

- Reverse Mortgage Retiree Pre-Qualification Letter

- Trust Income Retiree Pre-Qualification Letter

- Veteran Benefit Retiree Mortgage Pre-Qualification Letter

- Disability Pension Retiree Pre-Qualification Letter

- Joint Retiree Fixed-Income Pre-Qualification Letter

- Supplemental Income Retiree Pre-Qualification Letter

- Debt Consolidation Retiree Pre-Qualification Letter

- Downsizing Retiree Mortgage Pre-Qualification Letter

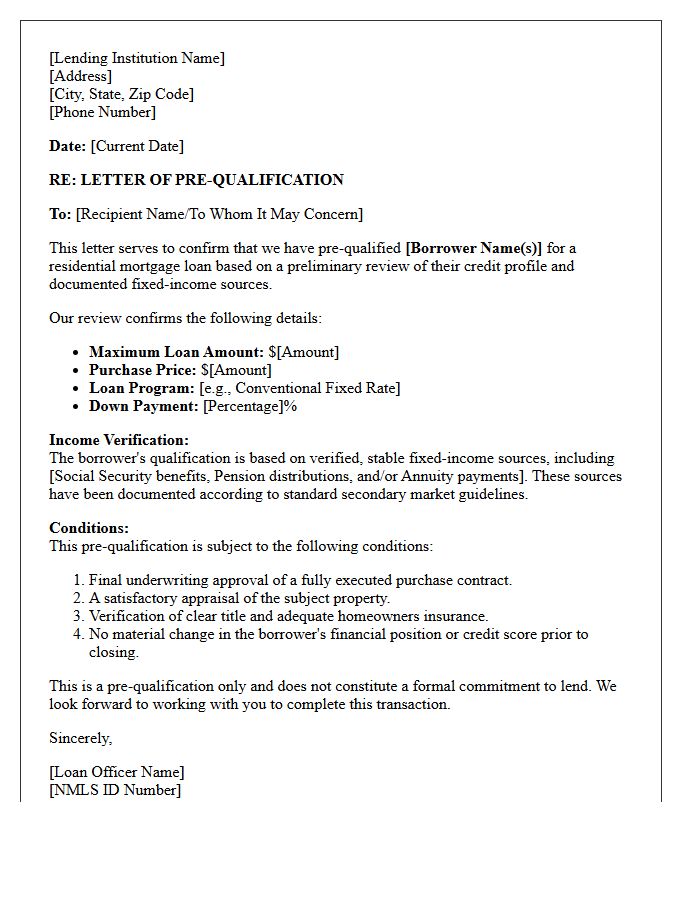

Standard Fixed-Income Retiree Pre-Qualification Letter

A Standard Fixed-Income Retiree Pre-Qualification Letter is a document confirming a senior's borrowing capacity based on stable pension and Social Security distributions. Lenders analyze the continuity of these guaranteed income streams rather than traditional employment wages. This letter provides credibility when making offers on homes, proving the retiree has the liquidity and assets required for mortgage approval. It essential for streamlining the home-buying process, ensuring that fixed monthly distributions meet the lender's debt-to-income requirements without the need for active salary verification.

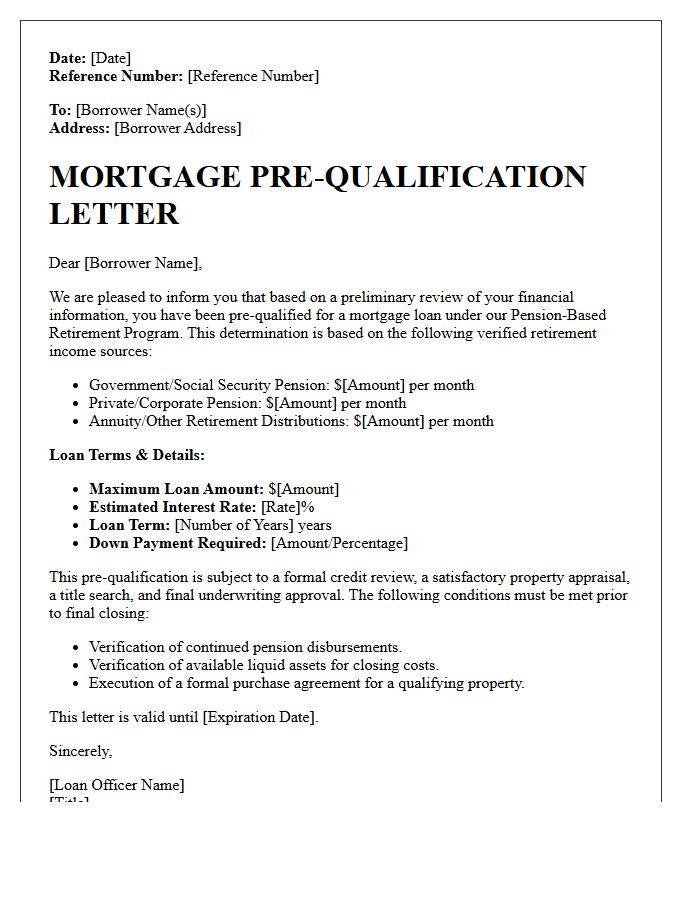

Pension Based Retiree Mortgage Pre-Qualification Letter

A Pension Based Retiree Mortgage Pre-Qualification Letter is an essential document for seniors using fixed income to purchase a home. Lenders verify your guaranteed monthly pension and Social Security payments to calculate a stable debt-to-income ratio. This letter proves your financial capacity to sellers, demonstrating that your retirement funds meet mortgage affordability requirements. Securing this document early ensures your purchasing power is accurately represented, allowing for a streamlined approval process tailored to your unique financial situation without traditional employment verification.

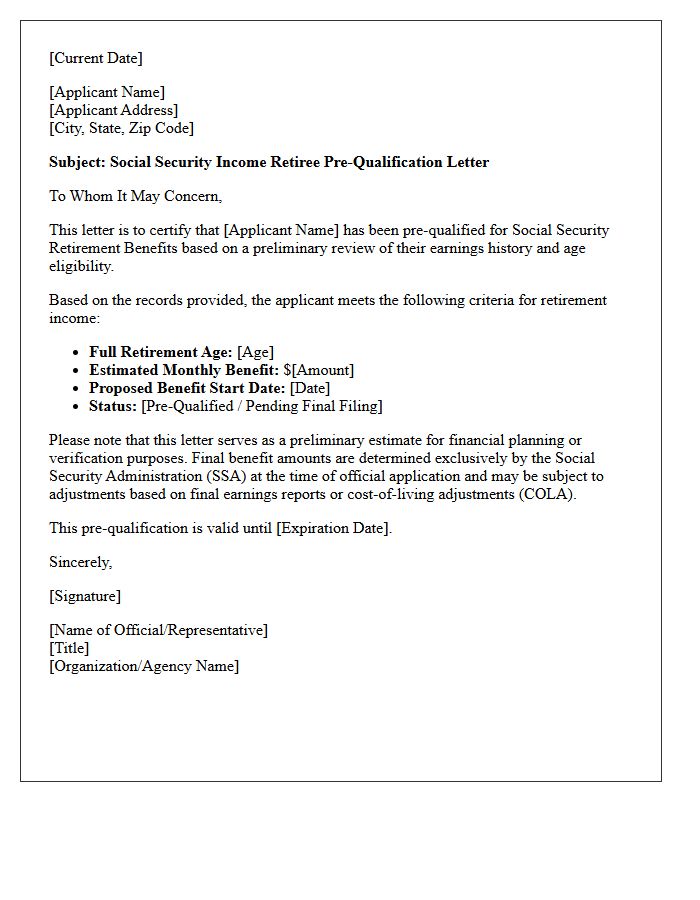

Social Security Income Retiree Pre-Qualification Letter

A Social Security Income Retiree Pre-Qualification Letter serves as official verification of your anticipated monthly benefits. This document is essential for retirees seeking mortgage approval or rental agreements, as it proves future cash flow before payments actually begin. It outlines your eligibility status and projected payment amount, allowing lenders to calculate your debt-to-income ratio accurately. To obtain one, contact the Social Security Administration or access your online account to ensure your financial credibility is verified during major life transitions.

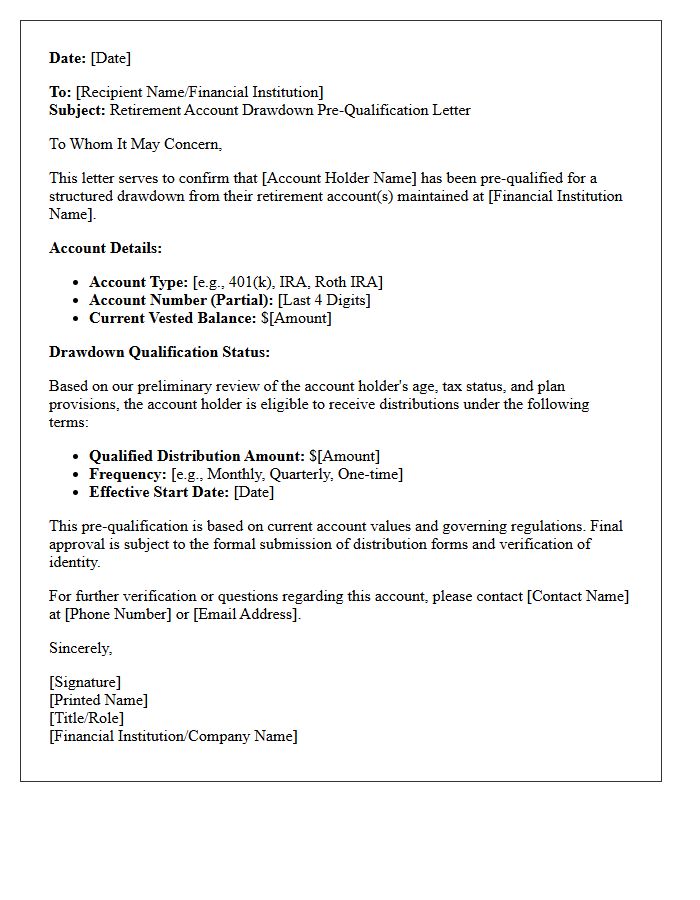

Retirement Account Drawdown Pre-Qualification Letter

A Retirement Account Drawdown Pre-Qualification Letter is a formal document from a financial institution verifying your eligibility to use retirement funds for a mortgage down payment or closing costs. It confirms the account's liquidity and the specific distribution rules governing your assets. This letter is essential for homebuyers using a 401(k) or IRA, as it proves to lenders that you possess the verified capital necessary to close a real estate transaction without incurring unexpected financing gaps or early withdrawal penalties that could jeopardize the loan approval process.

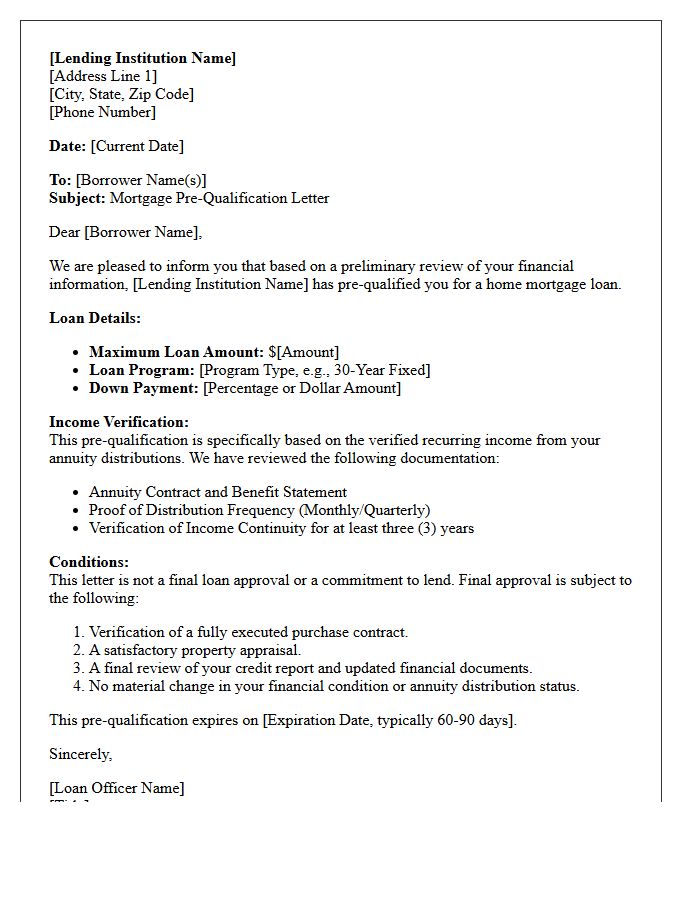

Annuity Income Mortgage Pre-Qualification Letter

An Annuity Income Mortgage Pre-Qualification Letter proves a borrower's eligibility by using recurring payments from an annuity as a stable revenue source. Lenders verify the distribution frequency and remaining duration to ensure long-term stability for loan repayment. This document is essential for retirees or investors, confirming that their structured settlements meet specific debt-to-income requirements. Securing this letter early streamlines the home-buying process, demonstrating financial credibility and intent to sellers while establishing a clear budget based on verified passive income streams.

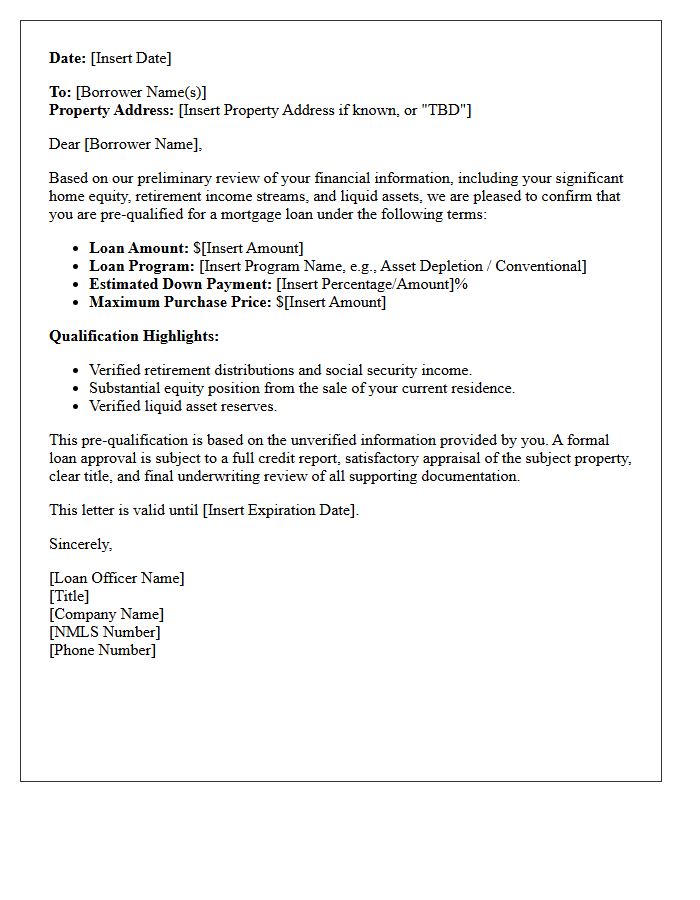

High Equity Retiree Pre-Qualification Letter

A High Equity Retiree Pre-Qualification Letter is a specialized document proving a senior homeowner's ability to purchase a new property using retained home equity rather than traditional employment income. This letter verifies that the borrower has significant net proceeds from a pending home sale or liquid assets to cover down payment costs and closing requirements. It streamlines the buying process by demonstrating financial strength to sellers, confirming that the retiree qualifies for specific financing options like H4P loans or jumbo products without needing a standard monthly paycheck.

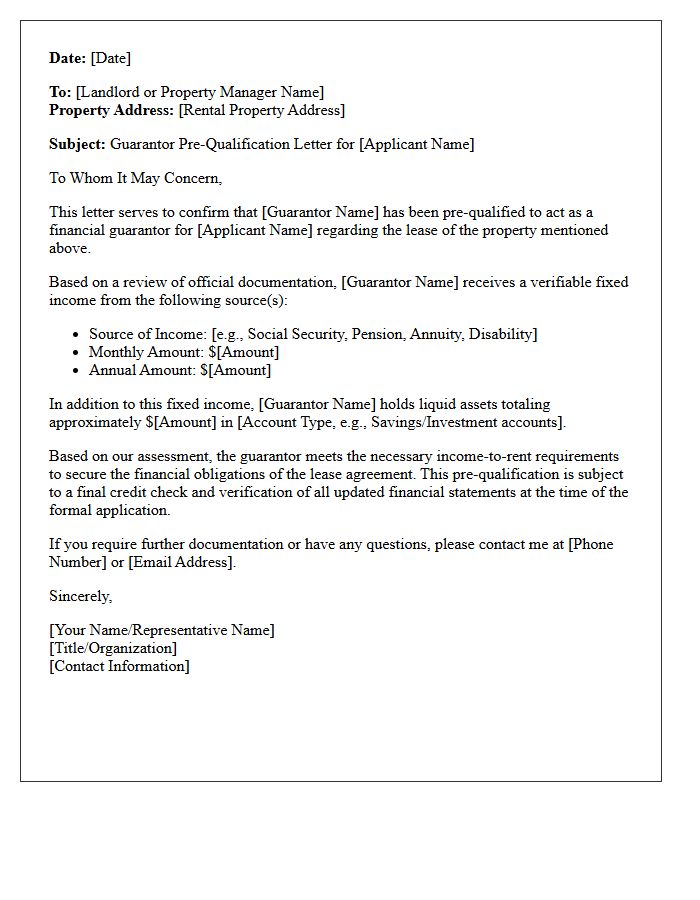

Fixed-Income Guarantor Pre-Qualification Letter

A Fixed-Income Guarantor Pre-Qualification Letter is a crucial document for retirees or individuals relying on non-employment earnings to secure a lease. It verifies that a third-party guarantor possesses sufficient liquid assets or consistent monthly distributions to cover rent obligations if the tenant defaults. Landlords require this letter to mitigate financial risk when the primary applicant lacks traditional payroll income. Obtaining this certification early streamlines the rental application process, proving financial stability through verified institutional backing or private asset verification.

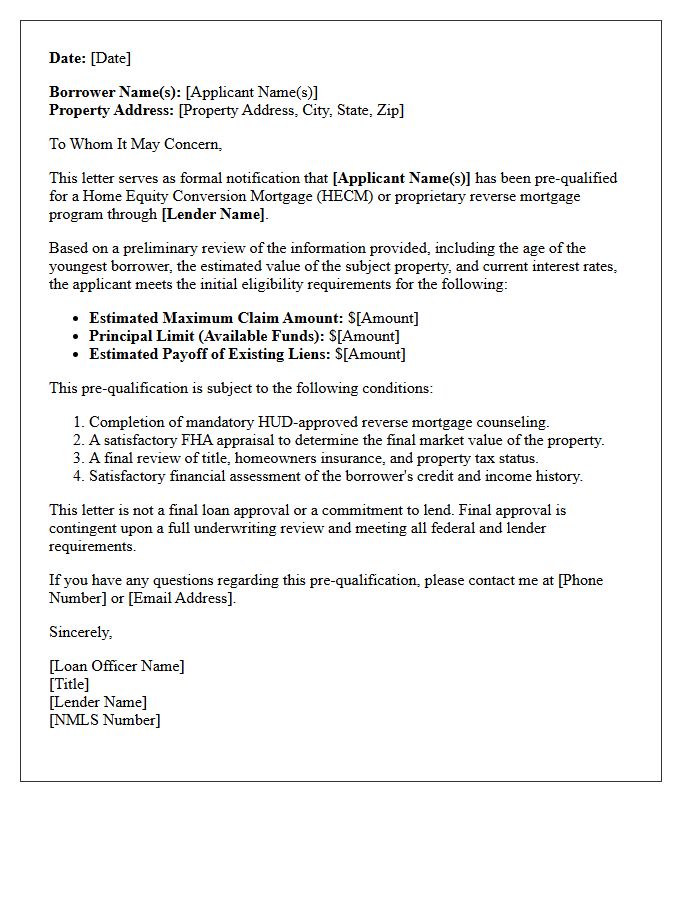

Reverse Mortgage Retiree Pre-Qualification Letter

A Reverse Mortgage Retiree Pre-Qualification Letter is a formal document estimates the maximum loan amount a senior can access based on age, home value, and current interest rates. This letter serves as essential proof for sellers during a home purchase (HECM for Purchase), confirming the borrower meets federal financial assessment guidelines. It demonstrates a retiree's borrowing capacity and creditworthiness, streamlining the transition to a more suitable residence while ensuring long-term financial stability without the burden of monthly mortgage payments during retirement.

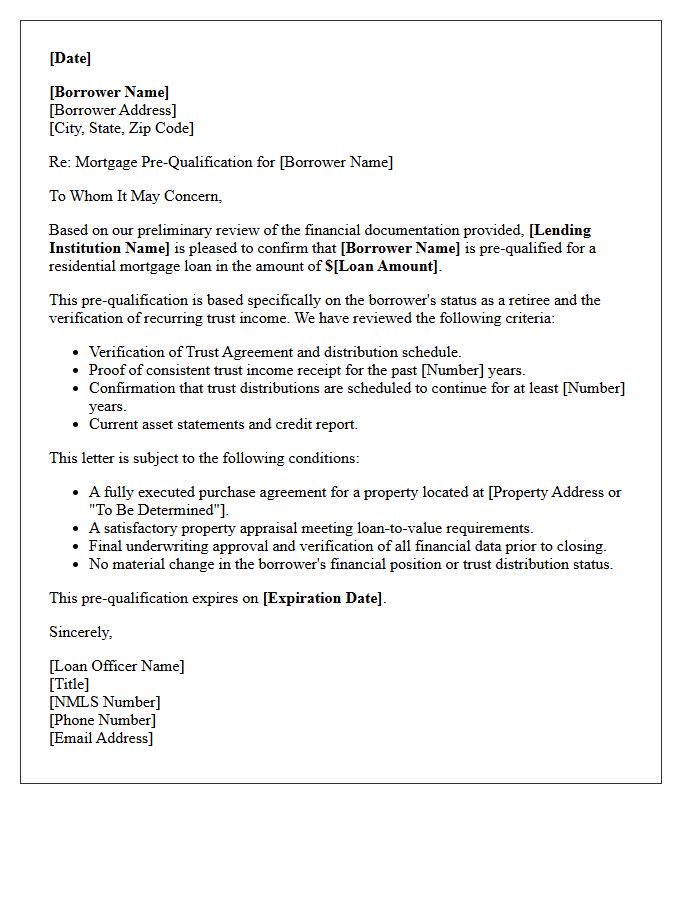

Trust Income Retiree Pre-Qualification Letter

A Trust Income Retiree Pre-Qualification Letter is a crucial document for mortgage approval when using wealth management assets as a primary funding source. This letter confirms that a beneficiary receives consistent distributions from a trust, ensuring the income meets specific lending guidelines. Lenders require this verification to establish financial stability and debt-to-income ratios for retirees. To qualify, the trust must typically guarantee payments for at least three years. Obtaining this formal validation from a trustee streamlines the home-buying process by proving reliable long-term liquidity without traditional employment verification.

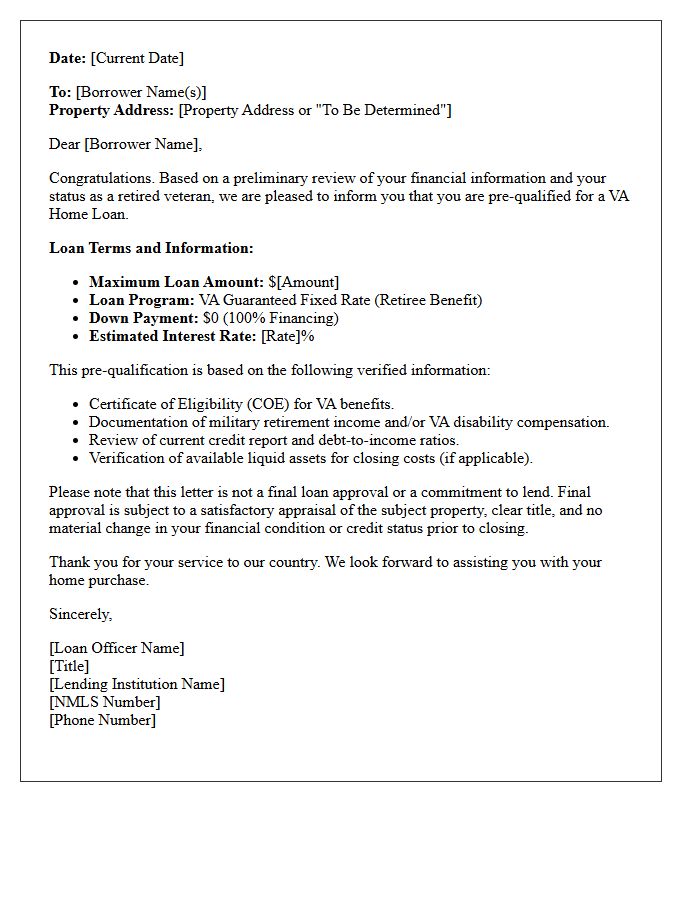

Veteran Benefit Retiree Mortgage Pre-Qualification Letter

A VA mortgage pre-qualification letter is a preliminary assessment confirming a veteran's eligibility for home financing based on basic income and credit data. For retirees, it is crucial to provide documentation of stable retirement income, such as Social Security or pension statements. This document signals to sellers that you are a serious buyer backed by government-guaranteed benefits. While not a final loan approval, it establishes your purchasing power and highlights the advantage of zero down payment requirements, ensuring a smoother transition into your new home during retirement.

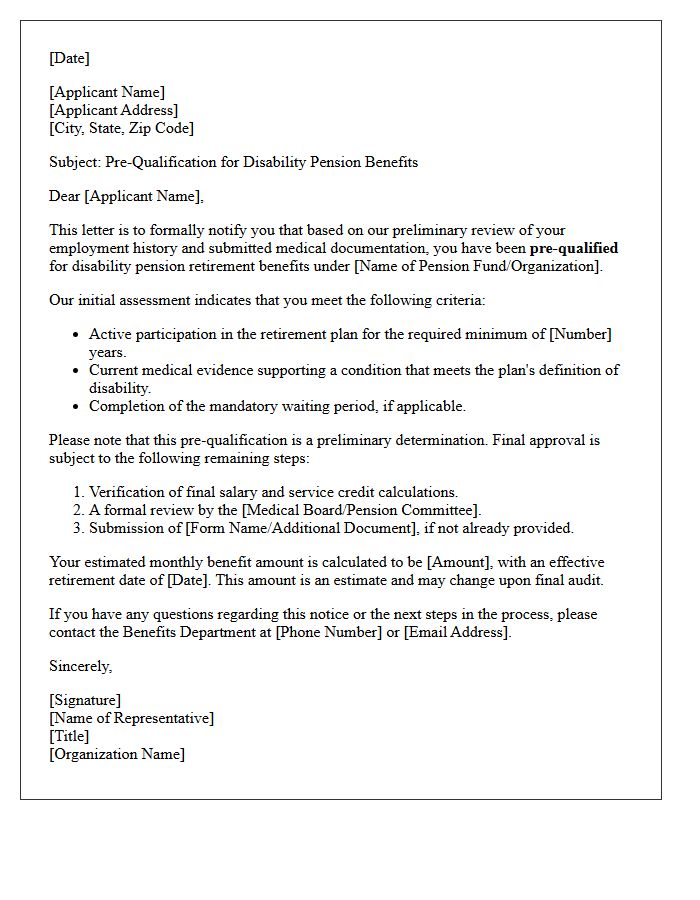

Disability Pension Retiree Pre-Qualification Letter

A Disability Pension Retiree Pre-Qualification Letter is a formal document verifying your eligibility for benefits before official approval. It confirms you meet specific criteria, such as service years and medical necessity, established by your pension fund. This letter is essential for financial planning and securing housing or loans during the transition from active work to retirement. It provides legal assurance that your monthly income stream is pending, ensuring stability while the final application is processed by the board. Always ensure your medical documentation is current to expedite the verification.

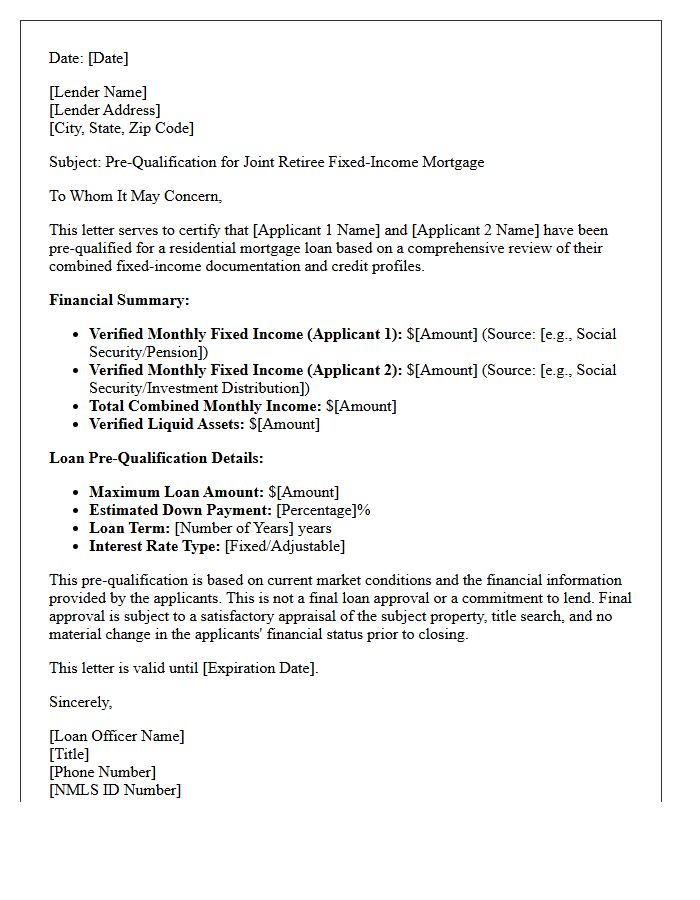

Joint Retiree Fixed-Income Pre-Qualification Letter

A Joint Retiree Fixed-Income Pre-Qualification Letter serves as official verification from a lender that two retired co-borrowers possess the combined financial stability to secure a mortgage. This document specifically evaluates pension distributions, Social Security benefits, and investment dividends to determine purchasing power. It is crucial because lenders apply unique debt-to-income calculations to non-employment revenue. Obtaining this letter proves to sellers that your collective fixed-income streams are reliable, documented, and sufficient to cover long-term housing costs, making your offer competitive in the real estate market.

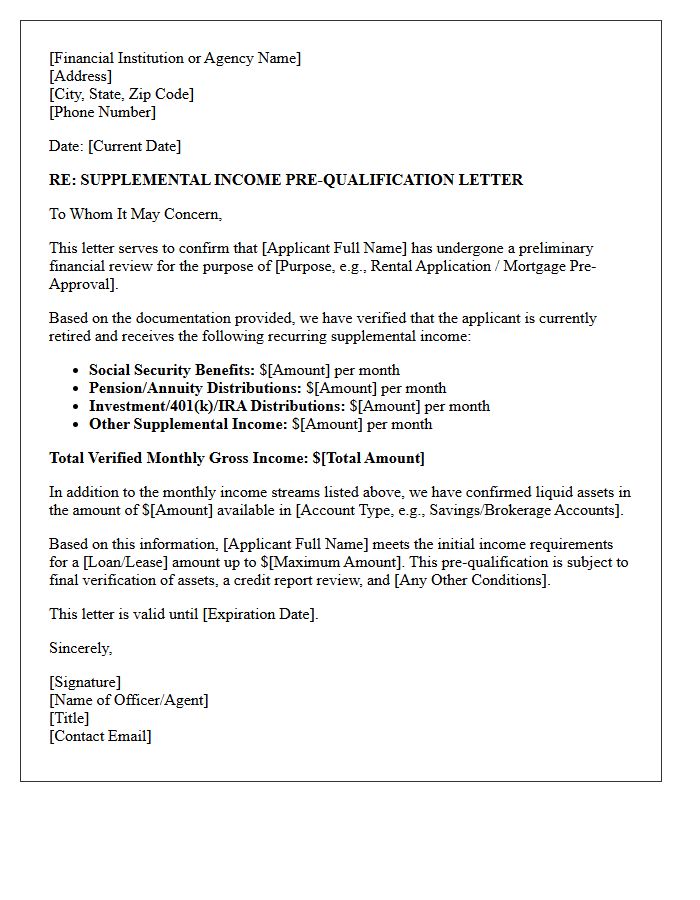

Supplemental Income Retiree Pre-Qualification Letter

A Supplemental Income Retiree Pre-Qualification Letter is a vital document verifying that a non-employment revenue stream, such as Social Security, pensions, or investment distributions, meets specific lending criteria. It serves as formal proof of financial capacity for retirees seeking new financing or housing. Lenders evaluate the stability and continuity of these funds to determine creditworthiness. Obtaining this letter early streamlines the approval process, ensuring that your fixed income is accurately calculated to support your future mortgage or rental commitments effectively.

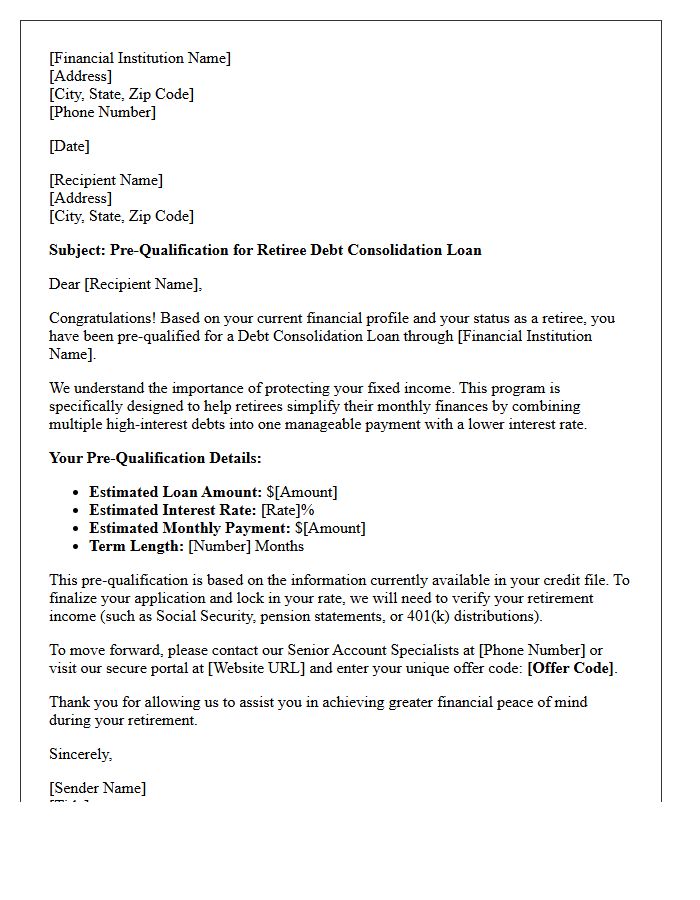

Debt Consolidation Retiree Pre-Qualification Letter

A Debt Consolidation Retiree Pre-Qualification Letter is an essential document that estimates how much a senior can borrow to merge high-interest debts into a single payment. It evaluates fixed income sources like Social Security or pensions rather than traditional employment wages. Obtaining this letter is a vital first step to verify eligibility without impacting your credit score. It provides a clear overview of potential interest rates and terms, helping retirees streamline their monthly budget and protect their financial stability during retirement by reducing total interest costs and simplifying debt management.

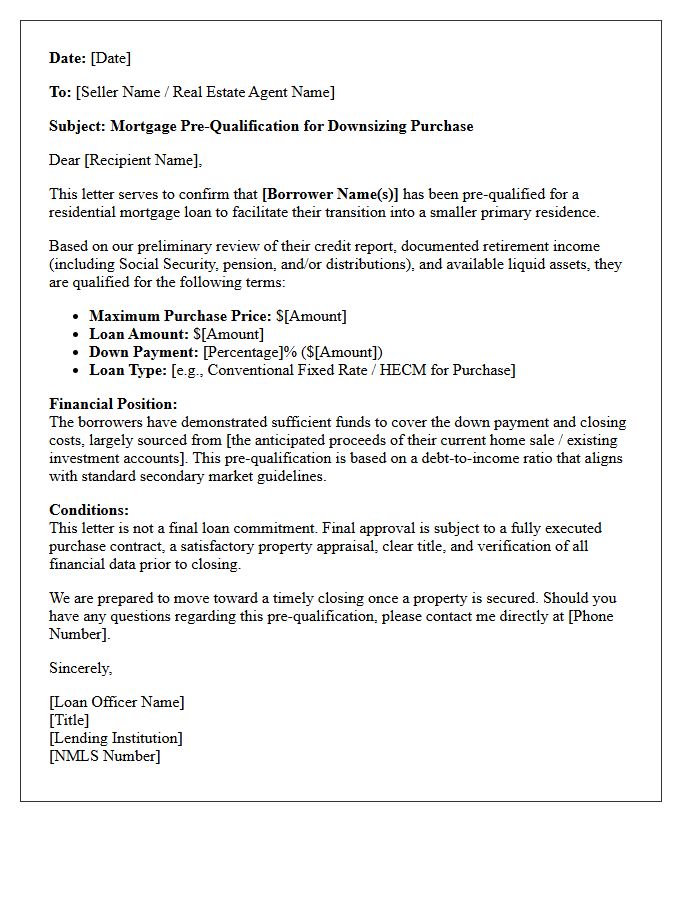

Downsizing Retiree Mortgage Pre-Qualification Letter

A mortgage pre-qualification letter is a vital tool for retirees planning to downsize. It proves to sellers that you possess the financial credibility to secure a loan, even with a shifting income. Lenders evaluate your retirement distributions, social security, and assets to determine your borrowing limit. Obtaining this document early streamlines the home-buying process and strengthens your competitive advantage in the real estate market. It ensures you understand your affordability range before listing your current residence, allowing for a seamless transition into your new, smaller home.

What is a Fixed-Income Retiree Pre-Qualification Letter?

A Fixed-Income Retiree Pre-Qualification Letter is a document from a mortgage lender estimating how much a home buyer can borrow based specifically on stable retirement sources such as Social Security, pensions, and structured distributions from retirement accounts.

Can I get pre-qualified for a mortgage using Social Security and pension income?

Yes, lenders treat Social Security and pension payments as reliable fixed income. To receive a pre-qualification letter, you will typically need to provide your most recent benefit award letters and bank statements to verify the monthly deposit amounts.

How do lenders calculate debt-to-income ratios for retired applicants?

Lenders compare your total monthly fixed income (including 401(k) or IRA distributions) against your projected monthly housing expenses and existing debts. In many cases, lenders can "gross up" non-taxable Social Security income by 25% to help you qualify for a higher loan amount.

What documentation is needed for a retiree pre-qualification letter?

You will generally need to provide Social Security award letters, pension statements, 1099 forms from the previous two years, and documentation showing that regular retirement account withdrawals are set to continue for at least three years.

Does a pre-qualification letter guarantee a mortgage for a retiree?

A pre-qualification letter is an initial estimate based on unverified or preliminary data. Final loan approval requires a formal application, a full credit check, and a comprehensive underwriting review of your assets and fixed-income stability.

Comments