A Cross-Collateralization Letter is a formal document used to release a specific asset from a multi-collateral loan agreement once its obligations are met. This process clarifies ownership rights and ensures clear titles for property sales or refinancing. Understanding the legal requirements is essential for protecting your equity. To simplify your documentation, below are some ready to use template.

Image cover: Official Cross-Collateralization Release Letter: Professional Samples and Templates

Letter Samples List

- Formal Request for Partial Release of Cross-Collateralization Letter

- Borrower Application for Cross-Collateralized Property Release Letter

- Lender Approval of Cross-Collateralization Lien Release Letter

- Conditional Release of Cross-Collateralized Assets Letter

- Notice of Intent to Release Cross-Collateralized Mortgage Letter

- Appraisal Requirement for Cross-Collateralization Release Letter

- Payoff and Release of Cross-Collateralized Loan Letter

- Title Company Instruction for Cross-Collateralization Release Letter

- Final Authorization for Cross-Collateralization Discharge Letter

- Mortgage Servicer Partial Release of Collateral Letter

- Underwriting Review for Cross-Collateralization Release Letter

- Denial of Cross-Collateralized Property Release Letter

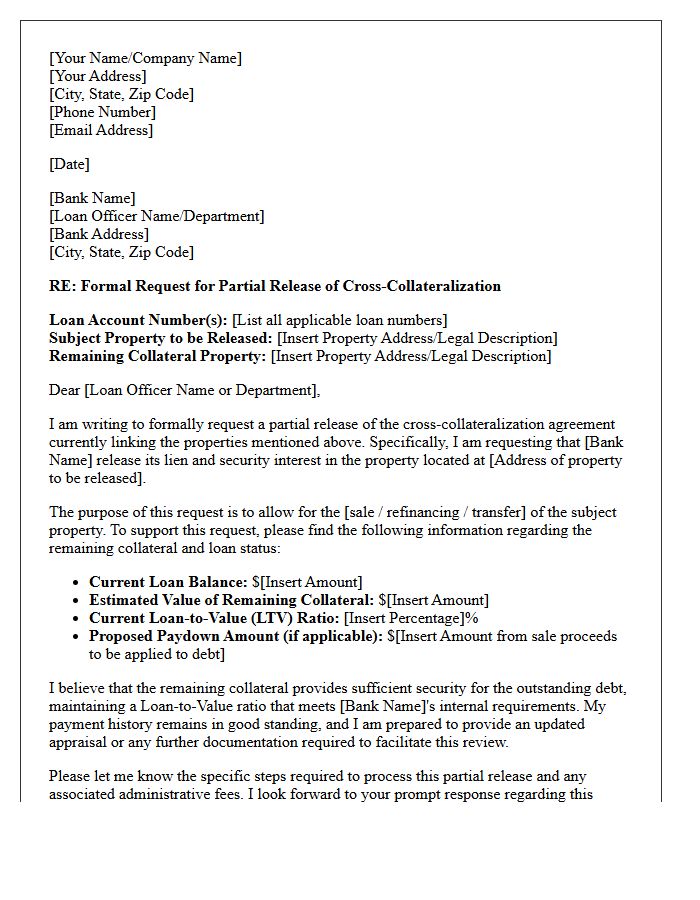

Formal Request for Partial Release of Cross-Collateralization Letter

A formal request for partial release of cross-collateralization is a legal document asking a lender to free a specific asset from a multi-property lien. This process is essential when a borrower wants to sell or refinance one property without paying off the entire blanket mortgage. To succeed, the borrower must prove that the remaining collateral maintains a sufficient loan-to-value ratio to secure the debt. Providing an updated appraisal and a formal proposal ensures the lender retains adequate security while granting the borrower financial flexibility.

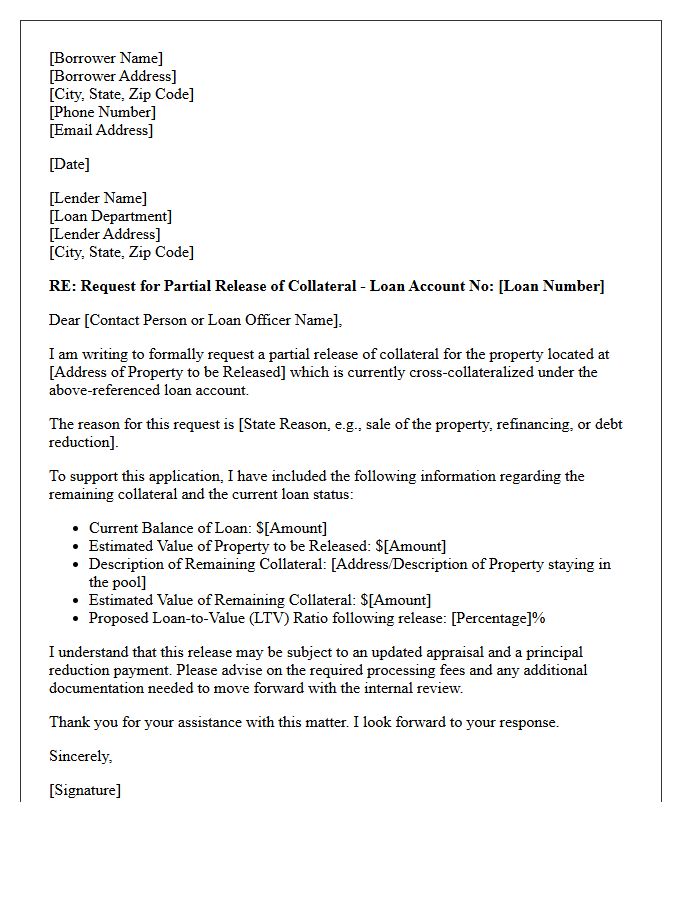

Borrower Application for Cross-Collateralized Property Release Letter

A borrower application for a cross-collateralized property release is a formal request to remove a specific asset from a multi-property lien. Lenders evaluate the Loan-to-Value (LTV) ratio and debt coverage to ensure remaining collateral sufficiently secures the outstanding balance. Successful approval often requires a partial release price payment or substitute security to mitigate lender risk. This process is essential for investors seeking to sell individual properties or refinance specific assets within a blanket mortgage structure while maintaining the primary loan agreement.

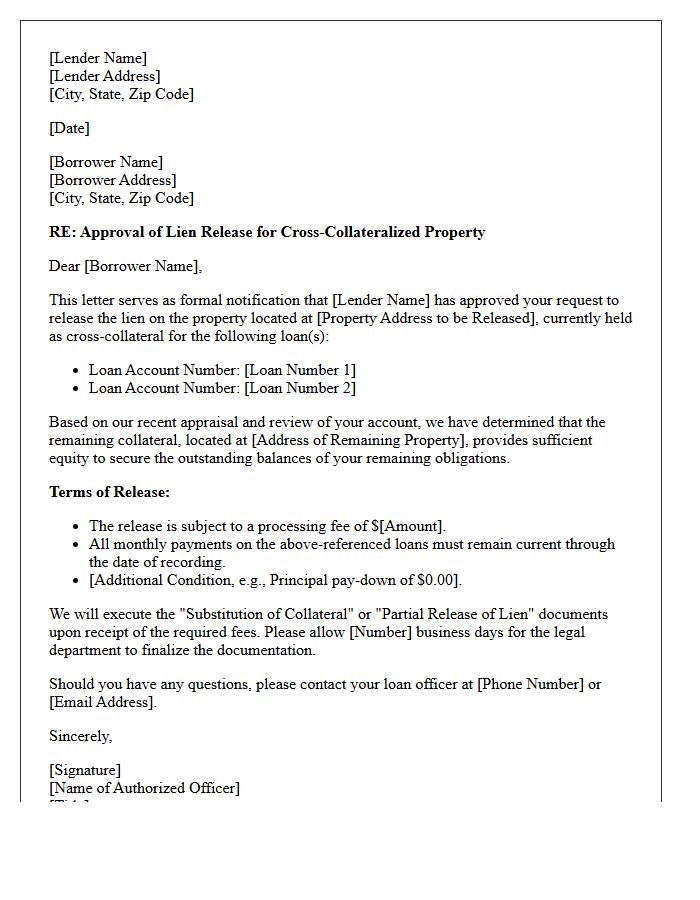

Lender Approval of Cross-Collateralization Lien Release Letter

A lender approval of a cross-collateralization lien release letter is a formal document authorizing the removal of a lien from a specific asset. In cross-collateralized loans, one property secures multiple debts, making partial releases complex. To obtain approval, the borrower must typically meet loan-to-value requirements or provide a pay-down to maintain the lender's security position. This letter confirms the lender's consent to release their legal claim on the collateral, allowing for its sale or refinancing without affecting the remaining encumbered assets within the loan portfolio.

Conditional Release of Cross-Collateralized Assets Letter

A Conditional Release of Cross-Collateralized Assets Letter is a formal legal document used to free a specific asset from a multi-asset lien. This occurs when a borrower requests to sell or refinance one property while keeping others pledged as security. The lender grants this partial release only if certain terms are met, such as a significant principal reduction or maintaining a specific loan-to-value ratio. Understanding these conditions is vital to ensuring the remaining collateral provides sufficient equity to satisfy the lender's risk requirements during the transition.

Notice of Intent to Release Cross-Collateralized Mortgage Letter

A Notice of Intent to Release Cross-Collateralized Mortgage is a critical legal document informing borrowers that a lender plans to decouple multiple properties secured by a single blanket mortgage. This process typically occurs after a partial debt repayment or during a refinancing event. It is essential to verify that the release correctly identifies the specific collateral being unpledged to ensure clear property titles. Failing to review this notice can impact your equity access and future borrowing capacity across your real estate portfolio.

Appraisal Requirement for Cross-Collateralization Release Letter

To obtain a release letter for cross-collateralized property, lenders typically mandate a current professional appraisal. This requirement ensures the remaining collateral maintains a sufficient Loan-to-Value (LTV) ratio to cover the total debt. The valuation must prove that the equity remaining after the partial release adequately protects the lender's financial position. Borrowers should anticipate valuation fees and potential delays, as the bank will not relinquish its security interest until the market value of the remaining assets meets specific internal underwriting guidelines and debt coverage requirements.

Payoff and Release of Cross-Collateralized Loan Letter

A Payoff and Release of Cross-Collateralized Loan Letter is a legal document confirming that multiple loans secured by the same assets are fully satisfied. In cross-collateralization, one asset serves as collateral for several debts. This letter is crucial because it ensures the lender releases liens on all associated properties or assets once the debt is paid. Without this formal release, clear title cannot be transferred to a new owner. Always verify that the document explicitly lists every affected account to guarantee a total discharge of financial obligations.

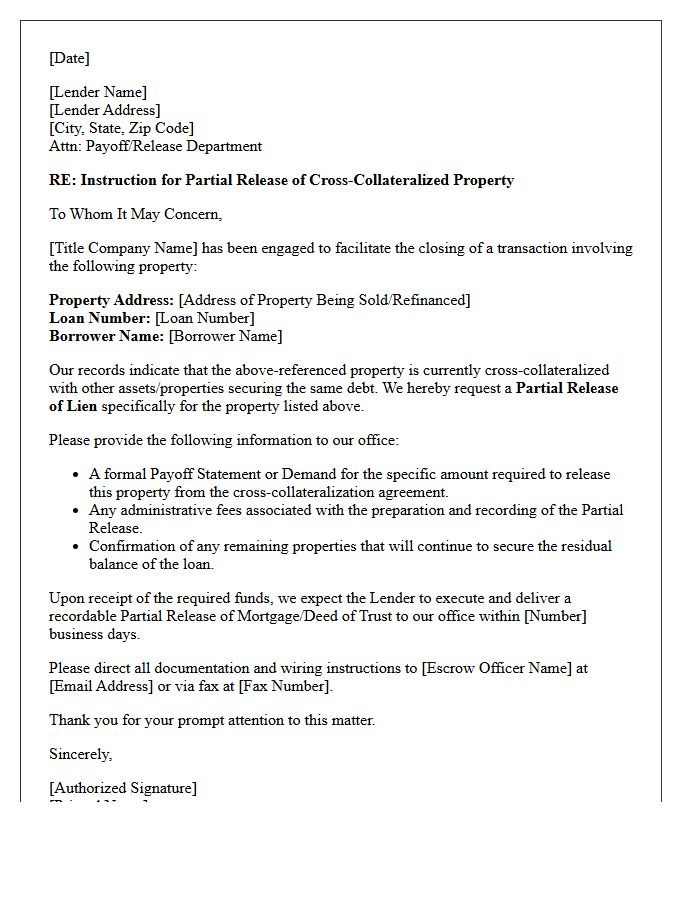

Title Company Instruction for Cross-Collateralization Release Letter

A Title Company Instruction for a Cross-Collateralization Release Letter is a formal request to a lender to release a specific property lien while keeping other secured assets active. It ensures the title is unencumbered for a pending sale or refinance. To avoid delays, the instruction must specify the exact payoff amount, legal descriptions, and terms for partial release. Clear communication between the escrow agent and lender is essential to confirm that the remaining collateral maintains sufficient equity to satisfy the primary loan obligations without breaching existing security agreements.

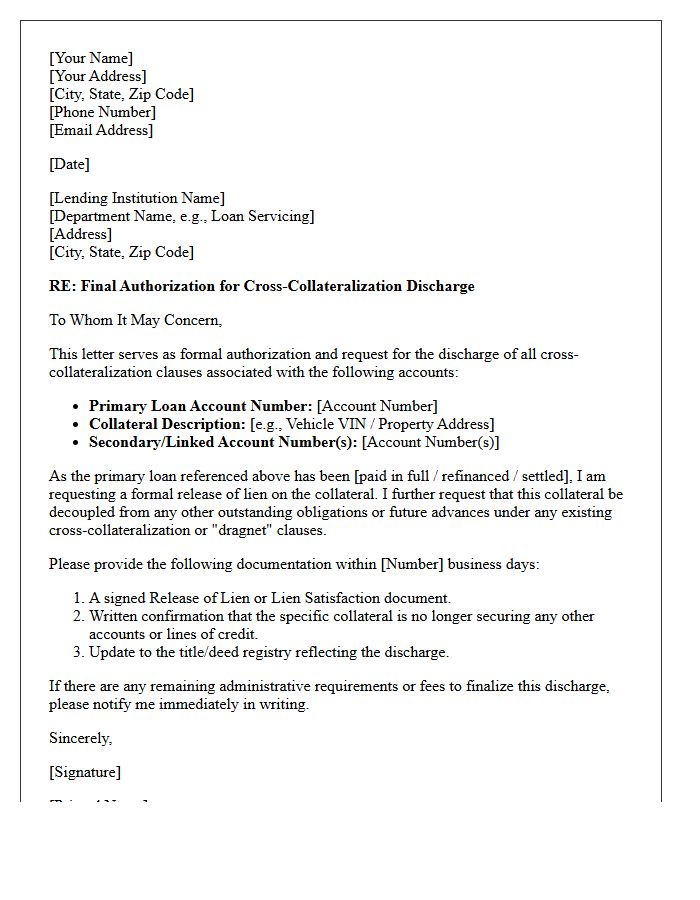

Final Authorization for Cross-Collateralization Discharge Letter

A Final Authorization for Cross-Collateralization Discharge Letter is a critical legal document used to release a specific asset, typically a vehicle or property, from a cross-collateralization clause. This occurs when one asset secures multiple loans within the same financial institution. Obtaining this formal discharge ensures that once the primary debt is satisfied, the lender relinquishes their secondary claim. Without this signed authorization, the lienholder may legally withhold the title or deed to cover other outstanding balances, such as credit cards or personal loans held by the borrower.

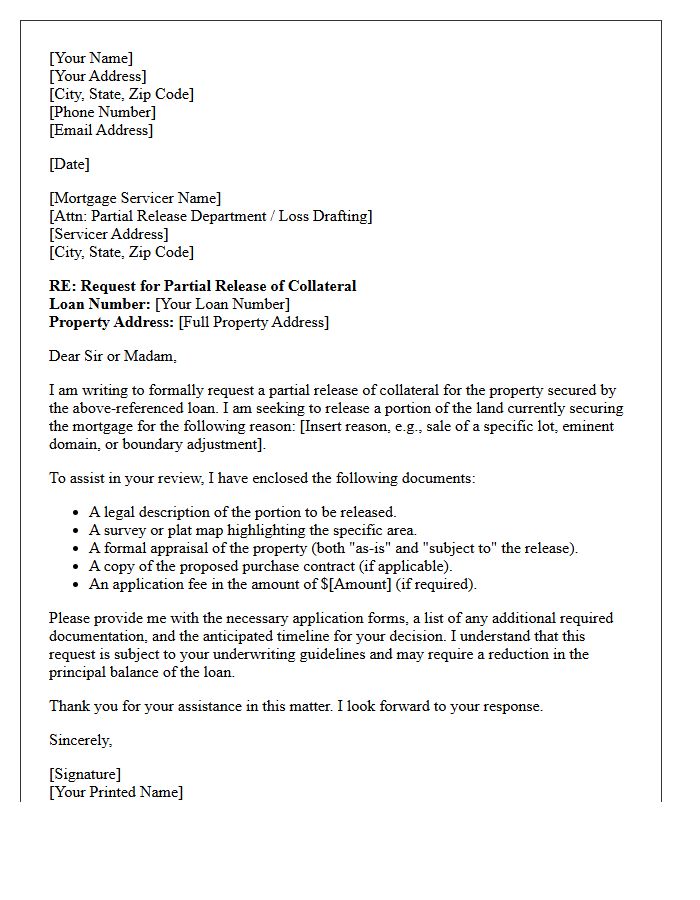

Mortgage Servicer Partial Release of Collateral Letter

A Mortgage Servicer Partial Release of Collateral Letter is a formal legal document used when a borrower wants to release a specific portion of their property from a mortgage lien. This process is essential when selling a subdivided parcel or granting an easement without paying off the entire loan. The servicer must evaluate if the remaining property value maintains a safe loan-to-value ratio. Obtaining this written approval ensures the lender's security interest is officially removed from the released land, allowing for a clear title transfer to a new owner.

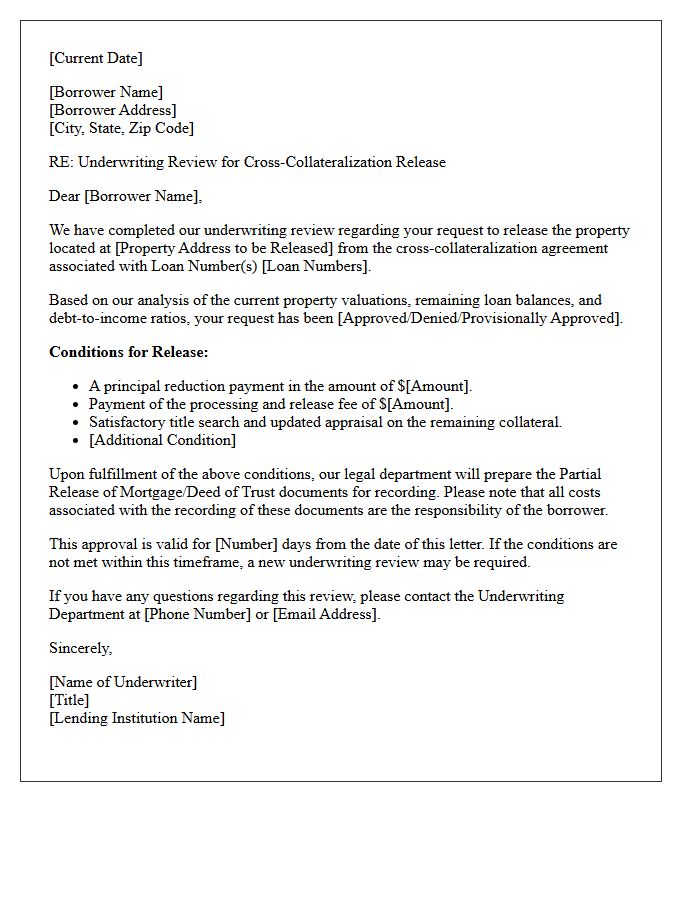

Underwriting Review for Cross-Collateralization Release Letter

An underwriting review is critical when requesting a cross-collateralization release letter. Lenders evaluate the remaining loan-to-value ratio and debt service coverage to ensure the remaining collateral sufficiently secures the outstanding debt. They analyze property valuations and financial stability to mitigate risk before releasing a specific asset from a blanket lien. Providing updated financial statements and appraisals speeds up this process. Understanding these risk assessment criteria is essential for borrowers seeking to decouple assets or refinance individual properties within a multi-asset portfolio efficiently.

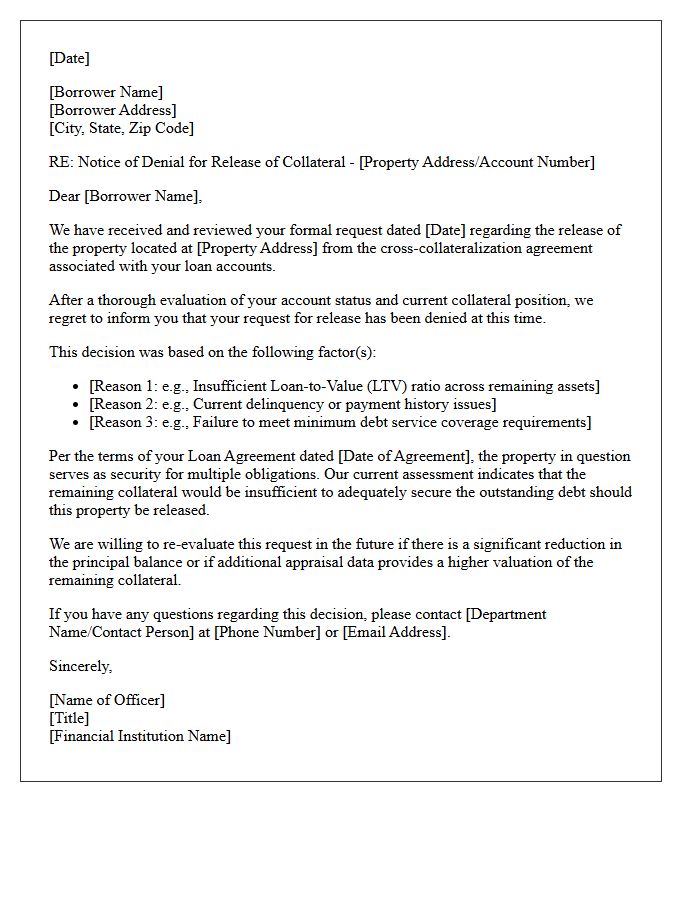

Denial of Cross-Collateralized Property Release Letter

A Denial of Cross-Collateralized Property Release Letter informs a borrower that their request to release a specific asset from a multi-asset loan agreement has been rejected. This occurs because the remaining collateral fails to meet the required loan-to-value ratio or fails to provide adequate security for the outstanding debt. Lenders issue this formal notice when the equity in the remaining properties is insufficient to mitigate financial risk. Understanding this denial is crucial for managing real estate portfolios, as it prevents the sale or refinancing of individual properties until additional debt obligations are satisfied.

What is a Release of Cross-Collateralization Letter?

A Release of Cross-Collateralization Letter is a formal legal document issued by a lender that officially decouples a specific asset from other loans. This document confirms that the asset is no longer serving as security for multiple debts, allowing the owner to sell or refinance the property independently.

When should I request a Release of Cross-Collateralization?

You should request this letter when you have paid off a specific portion of your debt, or when the remaining collateral provides sufficient equity to cover your outstanding loan balances. It is essential when you intend to sell one of the properties tied to a blanket mortgage or cross-collateralized loan agreement.

How does a cross-collateralization release affect my credit and equity?

While the release itself does not directly impact your credit score, it improves your financial flexibility by freeing up equity in a specific asset. By removing the cross-collateralization clause, you gain the ability to leverage that individual asset for new financing without the interference of existing lienholders from other accounts.

What information is required to process a Release of Cross-Collateralization Letter?

Lenders typically require the loan account numbers, a legal description of the property being released, a current appraisal to ensure the remaining collateral maintains a safe Loan-to-Value (LTV) ratio, and a formal written request. Some institutions may also charge a processing or administrative fee to execute the release.

Can a lender refuse to issue a Release of Cross-Collateralization?

Yes, a lender may refuse to issue the release if the remaining collateral does not meet their required equity thresholds or if the borrower is currently in default on any associated loans. The release is subject to the lender's risk assessment and the specific terms outlined in the original security agreement.

Comments