Agreed-Upon Procedures comfort letters provide essential verification for financial stakeholders by reporting specific findings without providing a formal opinion. These engagements enhance transparency during transactions by verifying data accuracy through predefined standards. They are vital for regulatory compliance and risk management in corporate finance. To assist your process, below are some ready to use template options.

Image cover: Expert Templates and Samples for Agreed-Upon Procedures Comfort Letters

Letter Samples List

- Agreed-Upon Procedures Comfort Letter for Debt Offerings

- Underwriter Comfort Letter for Initial Public Offerings

- Agreed-Upon Procedures Letter for Accounts Receivable Verification

- Merger and Acquisition Due Diligence Comfort Letter

- Agreed-Upon Procedures Letter for Inventory Observation

- Loan Covenant Compliance Comfort Letter

- Agreed-Upon Procedures Letter for Royalty Agreement Verification

- Securitization Transaction Agreed-Upon Procedures Letter

- Agreed-Upon Procedures Letter for Grant Expenditure Compliance

- Franchise Agreement Revenue Comfort Letter

- Agreed-Upon Procedures Letter for Employee Benefit Plans

- Bond Issuance Agreed-Upon Procedures Comfort Letter

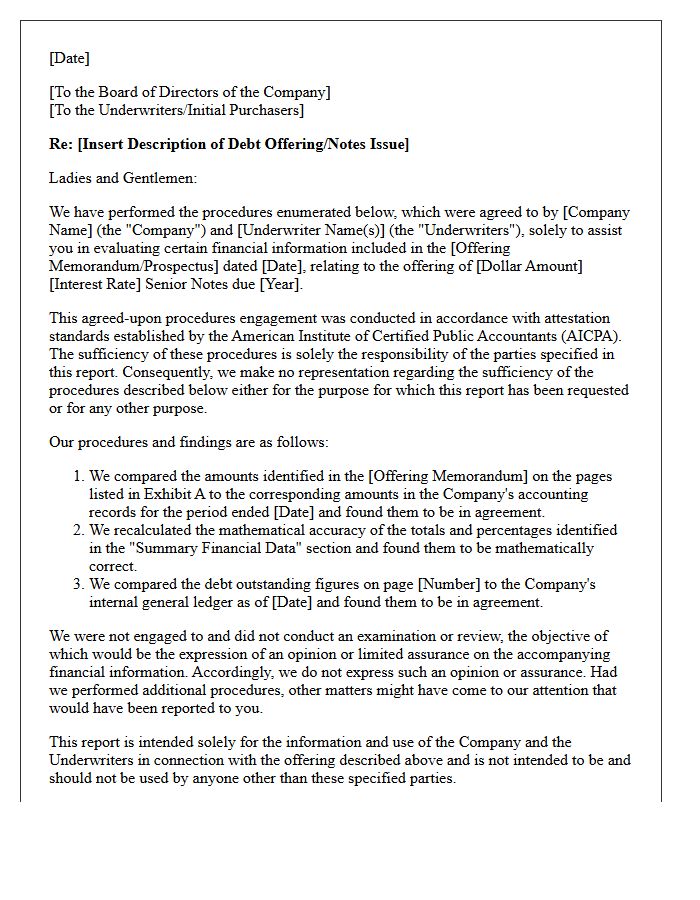

Agreed-Upon Procedures Comfort Letter for Debt Offerings

An Agreed-Upon Procedures (AUP) comfort letter is a vital document issued by independent auditors during debt offerings. It provides financial due diligence to underwriters by verifying specific data within the offering memorandum. Unlike a full audit, the auditor perform procedures specifically requested by the parties, reporting factual findings rather than a formal opinion. This process helps underwriters establish a due diligence defense under securities laws, ensuring the accuracy of financial information and building investor confidence throughout the capital raising process.

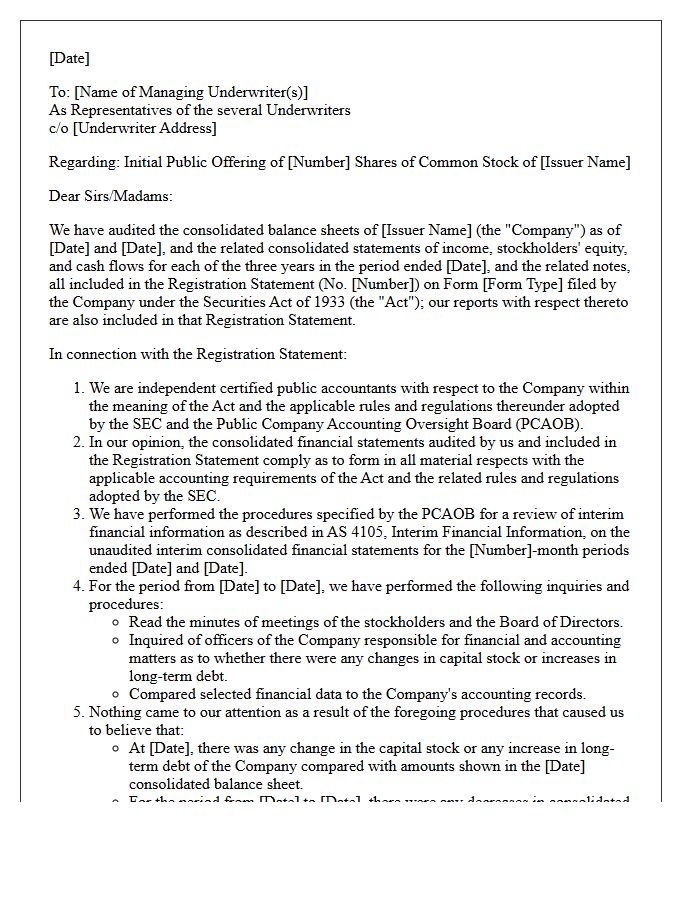

Underwriter Comfort Letter for Initial Public Offerings

An Underwriter Comfort Letter is a critical document issued by independent auditors to investment banks during an Initial Public Offering. It provides negative assurance that financial data in the prospectus aligns with audited statements. This process is essential for establishing a due diligence defense under securities laws, protecting underwriters from liability regarding material misstatements. By verifying unaudited financial information and subsequent changes, the letter builds investor confidence and ensures the integrity of the registration statement before the offering officially goes effective in the capital markets.

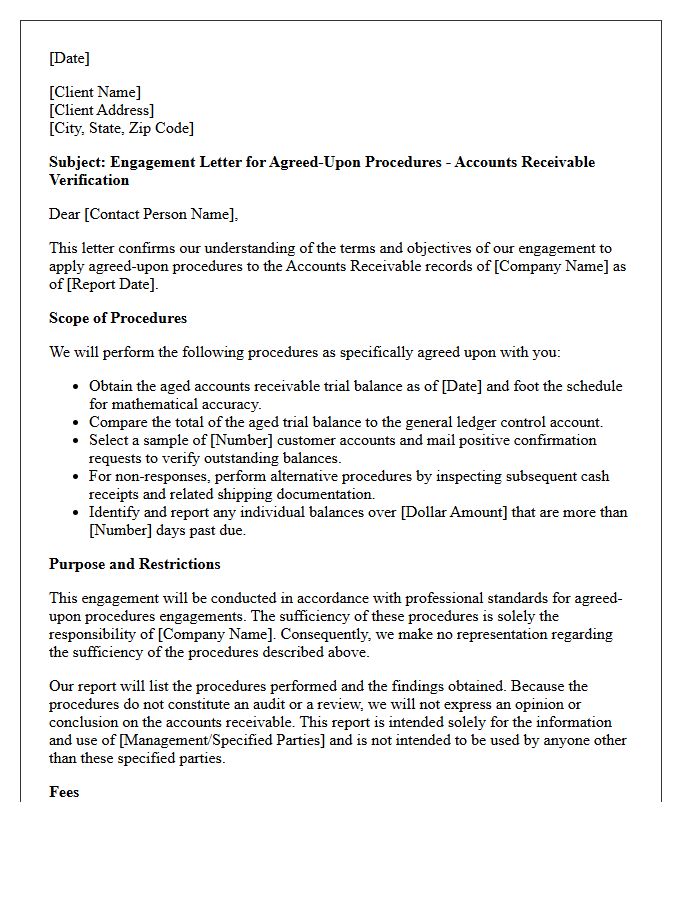

Agreed-Upon Procedures Letter for Accounts Receivable Verification

An Agreed-Upon Procedures letter for accounts receivable verification defines the specific steps an independent accountant takes to confirm balances. Unlike a full audit, the practitioner performs customized testing-such as verifying individual invoices or aging reports-without providing a formal opinion. This process offers stakeholders a factual findings report based on objective data. It is a cost-effective tool for identifying discrepancies, ensuring valuation accuracy, and enhancing internal controls over customer debts. Clear communication of the engagement scope is essential to meet the specific compliance or financing needs of the organization.

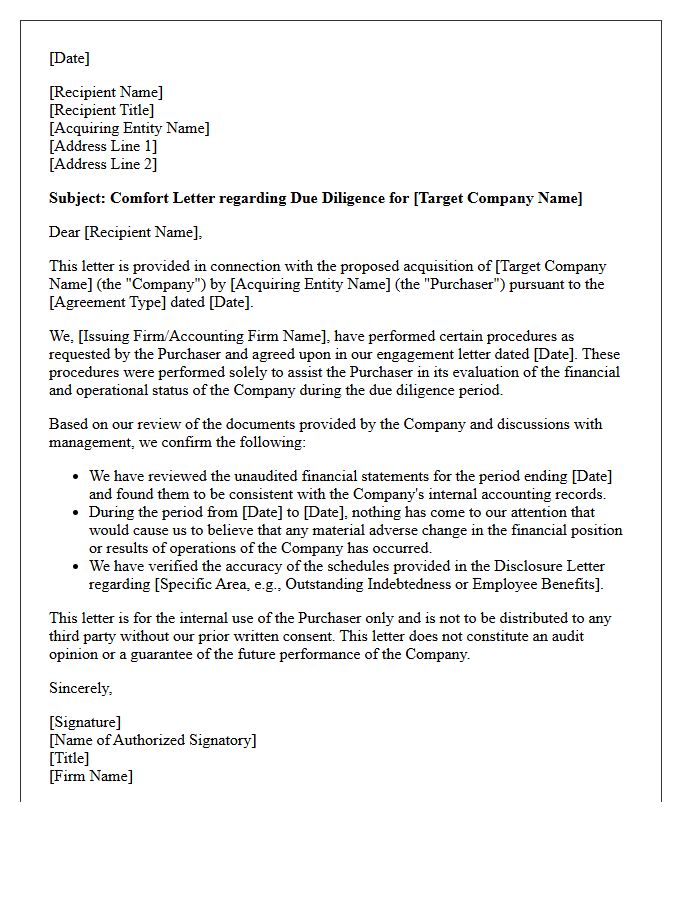

Merger and Acquisition Due Diligence Comfort Letter

A merger and acquisition due diligence comfort letter is a formal document issued by an independent auditor to underwriters or buyers. It provides negative assurance regarding the accuracy of financial statements and confirms that no material changes have occurred since the last audit. This letter mitigates risk by verifying financial data and ensuring financial transparency during the transaction. It serves as a critical component of the due diligence process, protecting parties from liability by validating that the financial information relied upon for the deal is consistent and verified according to professional standards.

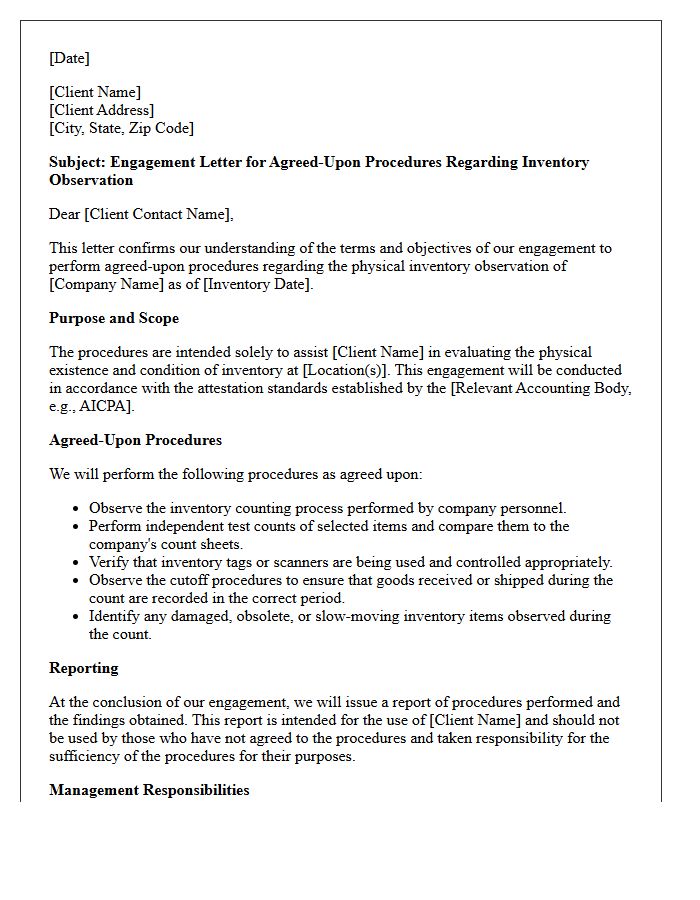

Agreed-Upon Procedures Letter for Inventory Observation

An Agreed-Upon Procedures letter for inventory observation outlines specific audit-related tasks performed by an independent practitioner. Unlike a full audit, the accountant only reports factual findings based on procedures requested by the client or third parties. This engagement focuses on verifying physical stock counts and existence at a specific location. It is crucial for stakeholders who need independent verification of inventory levels without the cost of a comprehensive financial statement opinion. The resulting report provides transparency regarding inventory accuracy and procedural compliance.

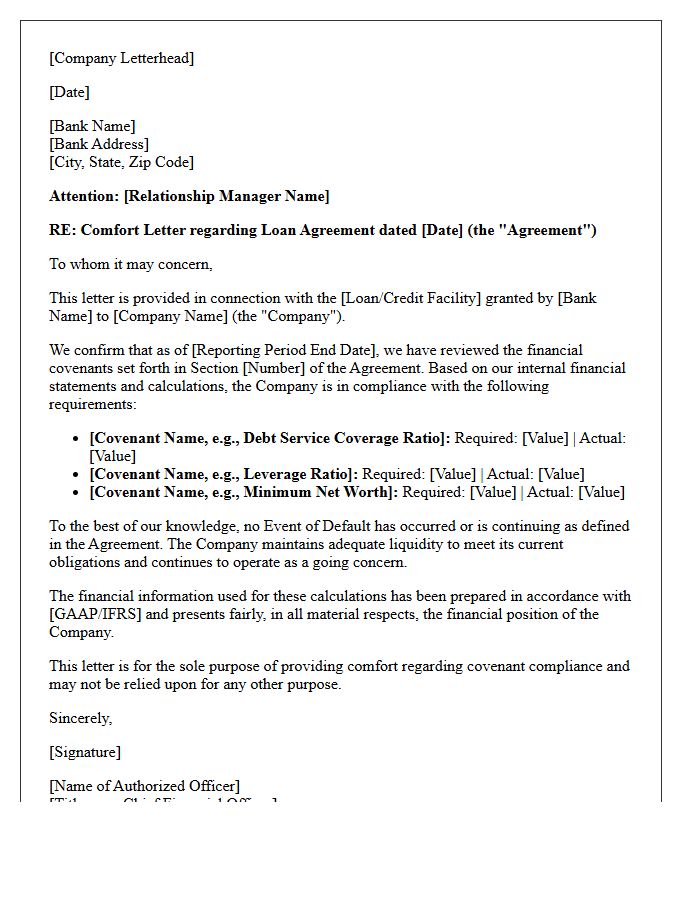

Loan Covenant Compliance Comfort Letter

A Loan Covenant Compliance Comfort Letter is a formal document issued by an independent auditor to a lender. It provides limited assurance regarding a borrower's financial position and their ability to meet specific debt covenants. This letter confirms that the financial data used to calculate ratios aligns with audited statements. It serves as a vital risk management tool, offering credibility to the borrower's reporting. Understanding these requirements is essential for maintaining healthy banking relationships and ensuring continuous access to capital without triggering technical defaults.

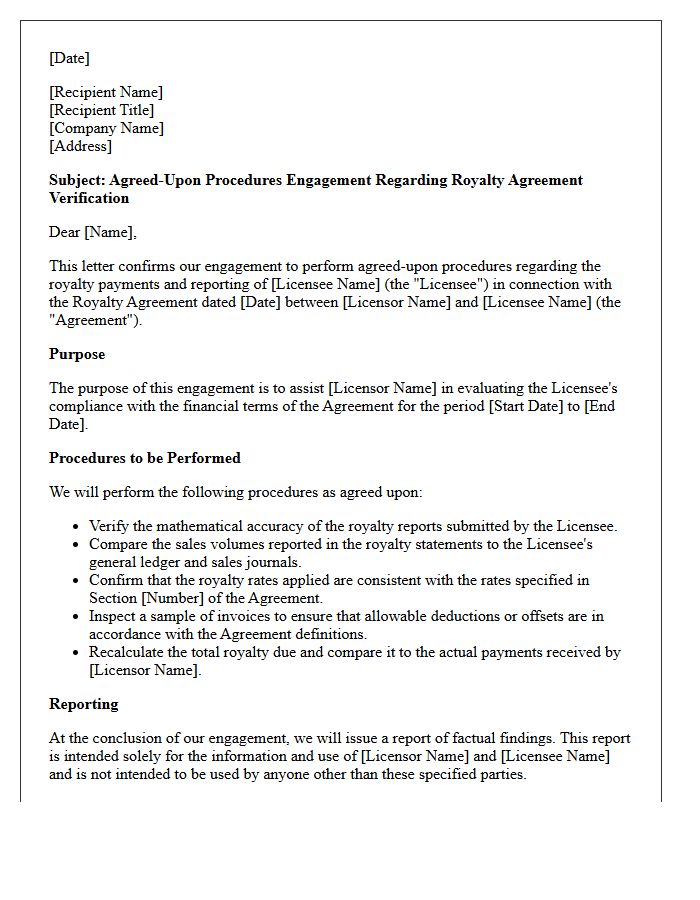

Agreed-Upon Procedures Letter for Royalty Agreement Verification

An Agreed-Upon Procedures letter is a targeted audit report where an independent practitioner performs specific tests requested by a licensor. This document is essential for royalty agreement verification, as it validates sales data, calculation accuracy, and contractual compliance without providing a full financial opinion. It offers transparency by identifying underpayments or reporting discrepancies directly to the parties involved. For stakeholders, this engagement provides a cost-effective way to ensure financial integrity and accountability within complex licensing partnerships, ensuring that all royalty obligations are met according to the established legal contract.

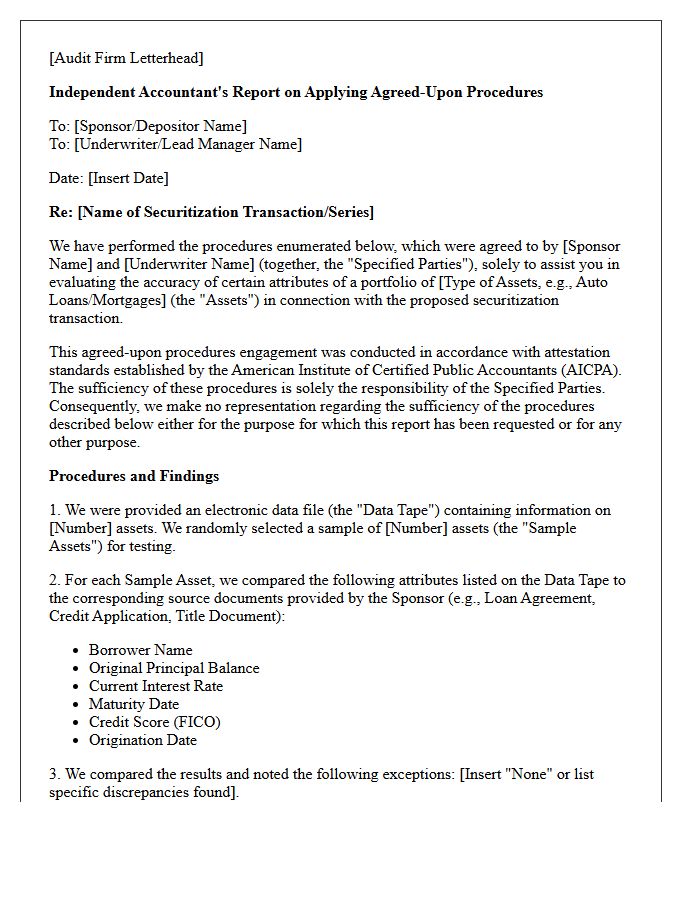

Securitization Transaction Agreed-Upon Procedures Letter

A Securitization Transaction Agreed-Upon Procedures Letter, commonly known as a comfort letter, is a critical document issued by independent accountants. It details specific audit-related procedures performed on the underlying asset pool data. This letter verifies the accuracy of financial information within the offering documents, providing investors and underwriters with assurance regarding data integrity. By validating the collateral characteristics, it mitigates risk and ensures compliance with regulatory standards, which is essential for the successful execution of an asset-backed securitization deal.

Agreed-Upon Procedures Letter for Grant Expenditure Compliance

An Agreed-Upon Procedures (AUP) letter provides a specific report on grant expenditure compliance. Unlike a full audit, an independent auditor performs exact procedures defined by the grantor to verify that funds were spent according to legal and contractual terms. This process ensures financial transparency and identifies potential ineligible costs or documentation gaps. It is a critical tool for organizations to demonstrate accountability, mitigate risks of funding clawbacks, and confirm that all disbursements align with the approved project budget and regulatory requirements.

Franchise Agreement Revenue Comfort Letter

A Franchise Agreement Revenue Comfort Letter is a financial verification document issued by an accountant or auditor. It provides assurance to lenders or franchisors regarding the accuracy of a franchisee's reported income. This letter confirms that the revenue data aligns with the entity's financial records, helping to secure financing or maintain contractual compliance. It serves as a reliability check, reducing risk for stakeholders by validating the gross sales figures used to calculate royalties or loan eligibility within a franchise system.

Agreed-Upon Procedures Letter for Employee Benefit Plans

An Agreed-Upon Procedures letter for employee benefit plans outlines specific tests performed by an auditor on plan data. Unlike a full audit, the practitioner performs defined procedures requested by the plan sponsor or trustee to verify compliance and data integrity. This engagement focuses on participant eligibility, contribution accuracy, and distribution testing. The final report identifies specific factual findings rather than providing a formal opinion. It is a critical tool for identifying operational errors and ensuring the plan adheres to Department of Labor and IRS regulations during internal reviews or transitions.

Bond Issuance Agreed-Upon Procedures Comfort Letter

A Bond Issuance Agreed-Upon Procedures (AUP) Comfort Letter is a critical document provided by independent auditors to underwriters. It verifies specific financial data within offering documents through predefined procedures rather than a full audit. This process helps underwriters establish due diligence and mitigate legal risks by ensuring the accuracy of financial figures. While not providing a formal opinion, the letter offers negative assurance or factual findings, confirming that financial information aligns with the issuer's records, thereby fostering investor confidence during the capital-raising process.

What is an Agreed-Upon Procedures (AUP) Comfort Letter?

An Agreed-Upon Procedures comfort letter is a formal document issued by an independent auditor to underwriters or requesting parties, detailing specific findings based on procedures previously agreed upon by all involved stakeholders regarding financial data or non-financial disclosures.

When is a comfort letter required for Agreed-Upon Procedures?

Comfort letters are typically required during securities offerings, mergers and acquisitions, or debt financing rounds where underwriters seek "negative assurance" or verification of specific financial information that has not been subjected to a full audit.

What is the difference between an audit and an AUP comfort letter?

Unlike an audit, which provides an opinion on the overall fairness of financial statements, an AUP comfort letter provides no opinion or assurance; instead, it reports only the factual results and findings derived from the specific procedures requested by the client.

Who are the intended users of an Agreed-Upon Procedures comfort letter?

The intended users are strictly limited to the parties who agreed to the procedures, such as investment banks, underwriters, or specific regulatory bodies, as they are the only ones who can determine if the procedures performed are sufficient for their purposes.

What professional standards govern the issuance of comfort letters?

In the United States, comfort letters are primarily governed by the AICPA's Statements on Auditing Standards (specifically AS 6101 for public companies), which outline the requirements for independence, content, and the scope of procedures performed by the practitioner.

Comments