A Comfort Letter is a critical document issued by auditors to provide assurance regarding financial data during the due diligence phase of mergers and acquisitions. It mitigates risk for underwriters and buyers by verifying unaudited financial statements and ensuring regulatory compliance. Understanding these reports is essential for smooth deal execution. To help you get started, below are some ready to use template.

Image cover: Navigating M&A Transactions: Essential Comfort Letter Samples and Templates

Letter Samples List

- Standard Financial Statement Comfort Letter

- Bring-Down Comfort Letter

- Pro Forma Financial Information Comfort Letter

- Negative Assurance Comfort Letter

- Subsequent Events Comfort Letter

- Internal Control Review Comfort Letter

- Tax Compliance Comfort Letter

- Unaudited Interim Financials Comfort Letter

- Agreed-Upon Procedures Comfort Letter

- Material Adverse Change Comfort Letter

- Target Company Financials Comfort Letter

- Acquisition Financing Comfort Letter

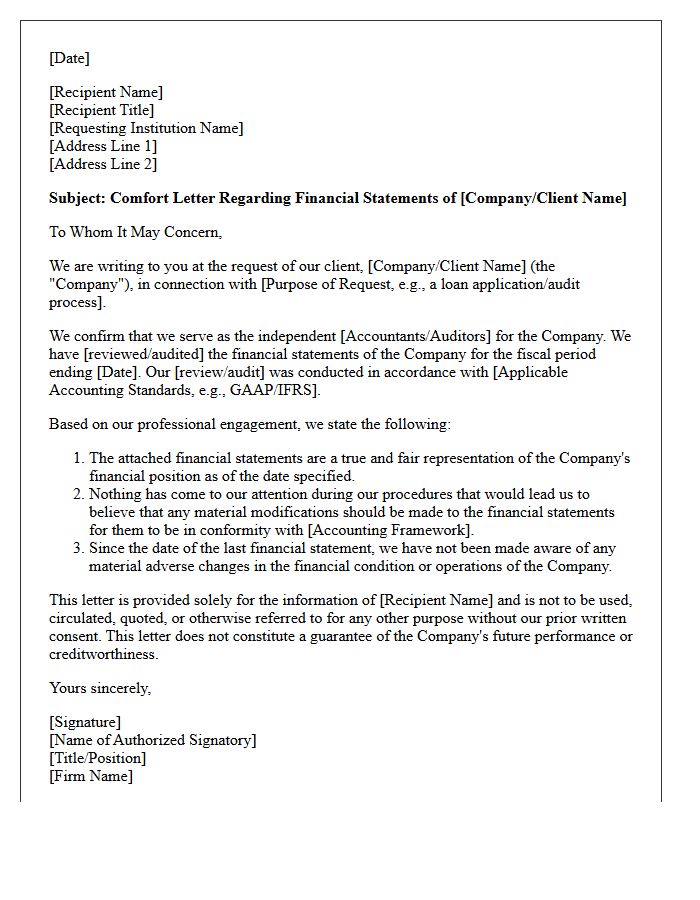

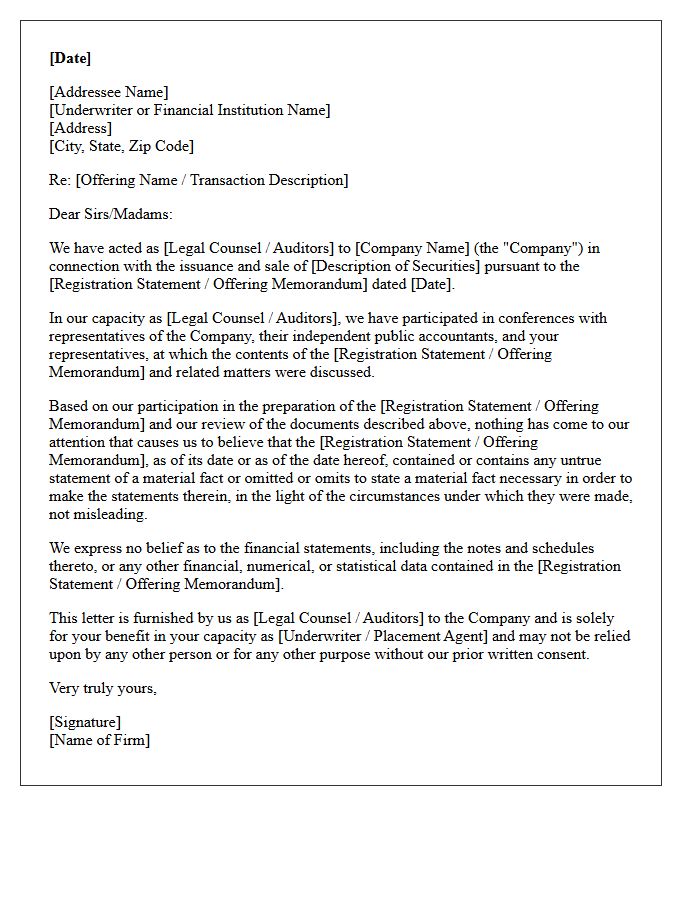

Standard Financial Statement Comfort Letter

A Standard Financial Statement Comfort Letter is a critical document issued by independent auditors to underwriters during securities offerings. It provides negative assurance that no material changes have occurred in the financial position since the last audit. This letter helps underwriters fulfill their due diligence obligations, offering a layer of protection against legal liability under securities laws. By verifying that financial data remains consistent with audited reports, the comfort letter builds investor confidence and ensures the accuracy of the registration statement before the final transaction occurs.

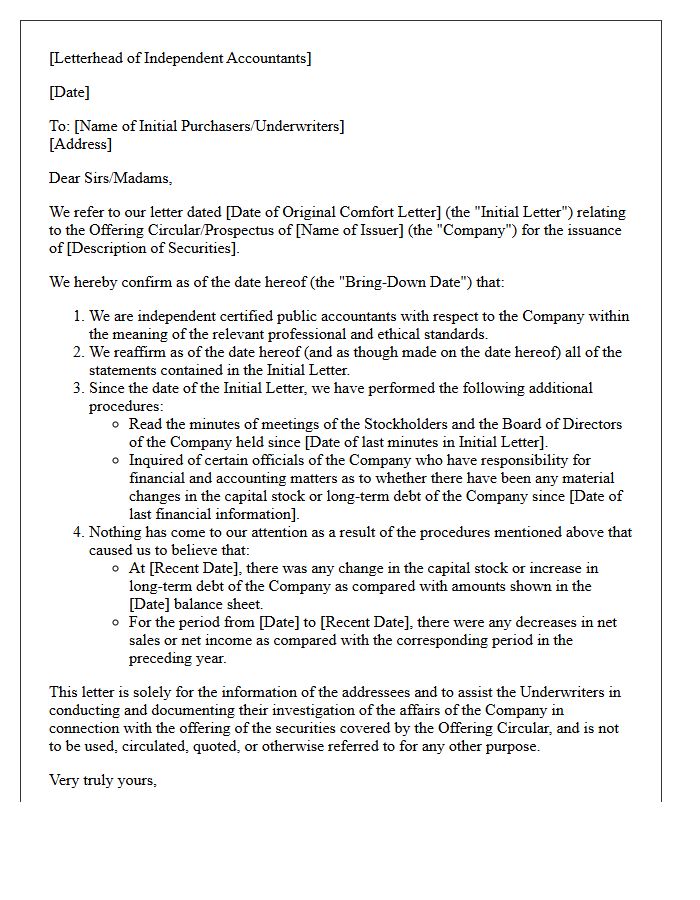

Bring-Down Comfort Letter

A Bring-Down Comfort Letter is a critical financial document issued by auditors during securities offerings. It serves to update the findings of a previous comfort letter, confirming that no material adverse changes have occurred in a company's financial position between the initial audit and the closing date. This process ensures due diligence for underwriters by verifying the continued accuracy of financial data. By providing this contemporaneous assurance, the letter mitigates risk and protects parties involved in the transaction from potential legal liabilities related to undisclosed financial shifts.

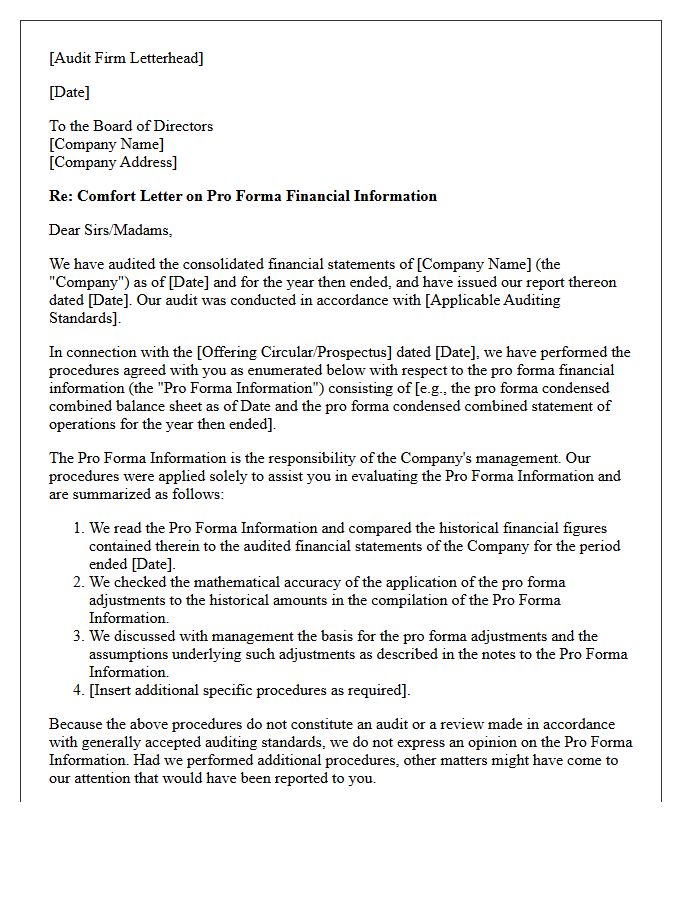

Pro Forma Financial Information Comfort Letter

A Pro Forma Financial Information Comfort Letter is a critical assurance document issued by independent auditors to underwriters during capital market transactions. It confirms that pro forma adjustments comply with regulatory requirements, ensuring that hypothetical financial scenarios-such as mergers or acquisitions-are presented accurately. By providing negative assurance on the compilation of pro forma data, auditors help mitigate risk and verify that the financial statements reflect the economic impact of significant events, maintaining transparency for potential investors and ensuring compliance with SEC standards or similar financial regulations.

Negative Assurance Comfort Letter

A Negative Assurance Comfort Letter is a critical document issued by auditors to underwriters during securities offerings. It confirms that, based on a limited review, no material modifications are required for the financial statements to align with accounting standards. Unlike a full audit, it provides limited assurance rather than an absolute opinion. This document helps underwriters establish a due diligence defense, reducing legal liability by verifying that financial data is not misleading. It serves as a vital bridge of trust between issuers, auditors, and investment banks during the complex capital raising process.

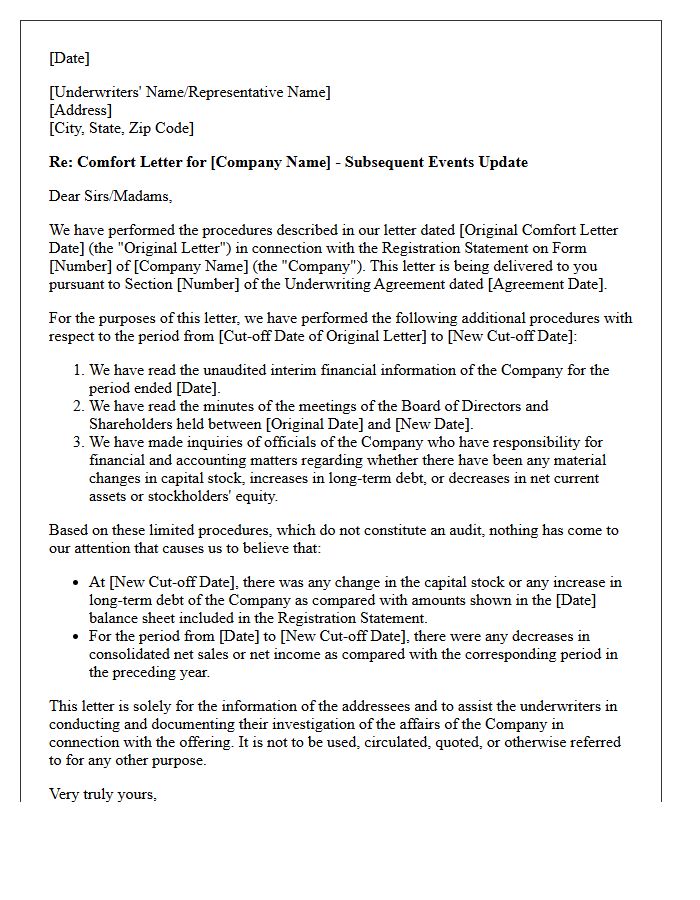

Subsequent Events Comfort Letter

A Subsequent Events Comfort Letter is a critical document issued by independent auditors to underwriters during a securities offering. It provides negative assurance that no material adverse changes occurred in a company's financial position between the last audit and the effective date of the registration statement. This process is essential for establishing a due diligence defense under securities law, ensuring that financial information remains accurate and reliable for investors. By verifying recent financial trends, the letter mitigates risk and validates the integrity of the issuer's financial disclosures before closing.

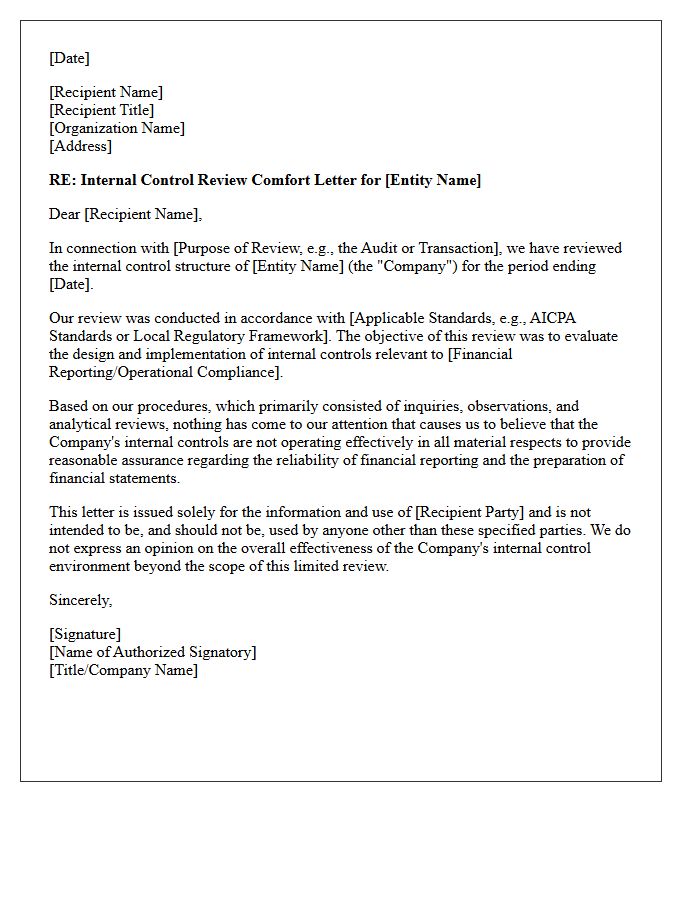

Internal Control Review Comfort Letter

An Internal Control Review Comfort Letter is a formal document issued by independent auditors to underwriters during a securities offering. It provides negative assurance regarding the effectiveness of a company's financial reporting systems. This letter confirms that nothing came to the auditors' attention to suggest significant weaknesses in internal controls. It serves as a vital due diligence tool, helping to mitigate legal risks for underwriters by verifying that the issuer maintains robust processes to ensure financial statement accuracy and regulatory compliance throughout the investment process.

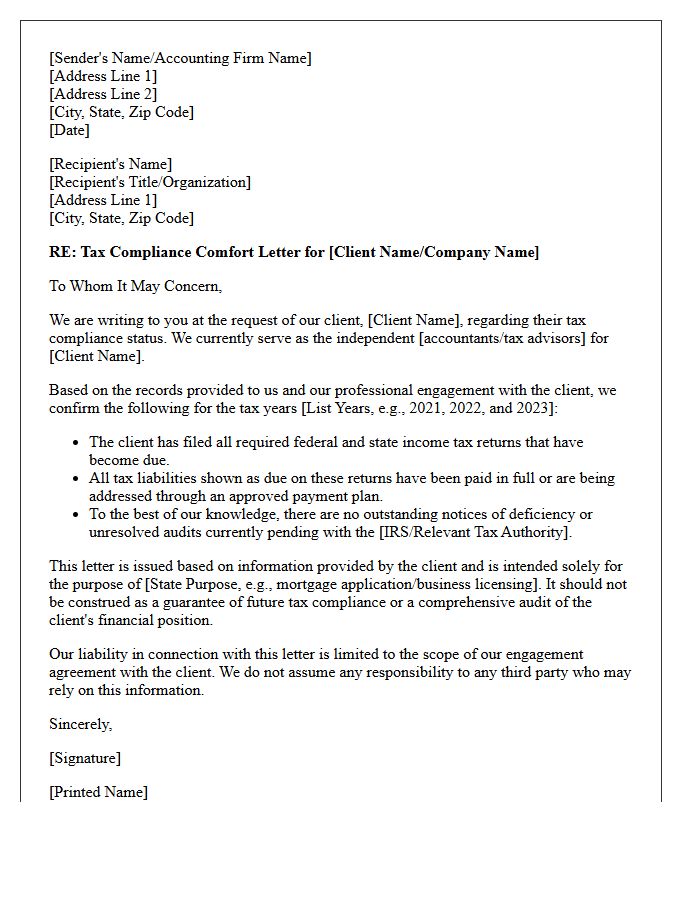

Tax Compliance Comfort Letter

A Tax Compliance Comfort Letter is a formal document issued by an accountant to provide assurance regarding a taxpayer's financial status or filing history. Often required by lenders or third parties, it verifies that a business or individual is meeting their legal obligations. While it offers a layer of verification, it is not a full audit or a guarantee of future solvency. Understanding the scope of these letters is essential to manage liability and ensure that all reported fiscal information aligns with current regulatory standards and official tax filings.

Unaudited Interim Financials Comfort Letter

An Unaudited Interim Financials Comfort Letter is a document issued by independent auditors to underwriters during securities offerings. It provides negative assurance, confirming that no material modifications are needed for interim statements to comply with accounting standards. While not a full audit, it mitigates financial risk by verifying that the data is consistent with audited records. This letter is a vital component of the due diligence process, helping protect parties from liability by ensuring the reliability of financial information reported between annual audit periods.

Agreed-Upon Procedures Comfort Letter

An Agreed-Upon Procedures engagement involves an independent practitioner performing specific audit-style tasks requested by a client. The resulting comfort letter reports objective findings rather than providing a formal legal opinion or high-level assurance. This document is essential in financial transactions, such as mergers or underwriting, to verify data accuracy. Because the practitioner does not perform a full audit, the sufficiency of the procedures is the responsibility of the specified parties. It provides transparency and risk mitigation by documenting factual results based on predefined criteria and evidence.

Material Adverse Change Comfort Letter

A Material Adverse Change (MAC) Comfort Letter is a critical document issued by auditors to underwriters during financial transactions. It provides assurance that no significant negative shifts in a company's financial position have occurred since the last audited statement. By confirming the absence of material adverse developments, this letter mitigates risk for investors and lenders. It serves as a vital due diligence tool, ensuring transparency and maintaining market confidence by bridging the information gap between reporting periods and the closing of an offering or loan agreement.

Target Company Financials Comfort Letter

A Comfort Letter is a critical document issued by independent auditors to underwriters during corporate transactions. It provides negative assurance regarding the accuracy of a target company's financial statements and subsequent changes. This letter verifies that financial data has been properly prepared in accordance with accounting standards, helping to mitigate legal liability for parties involved. By performing specific agreed-upon procedures, auditors bridge the gap between the last audited period and the closing date, ensuring stakeholders have confidence in the financial integrity of the merger or acquisition process.

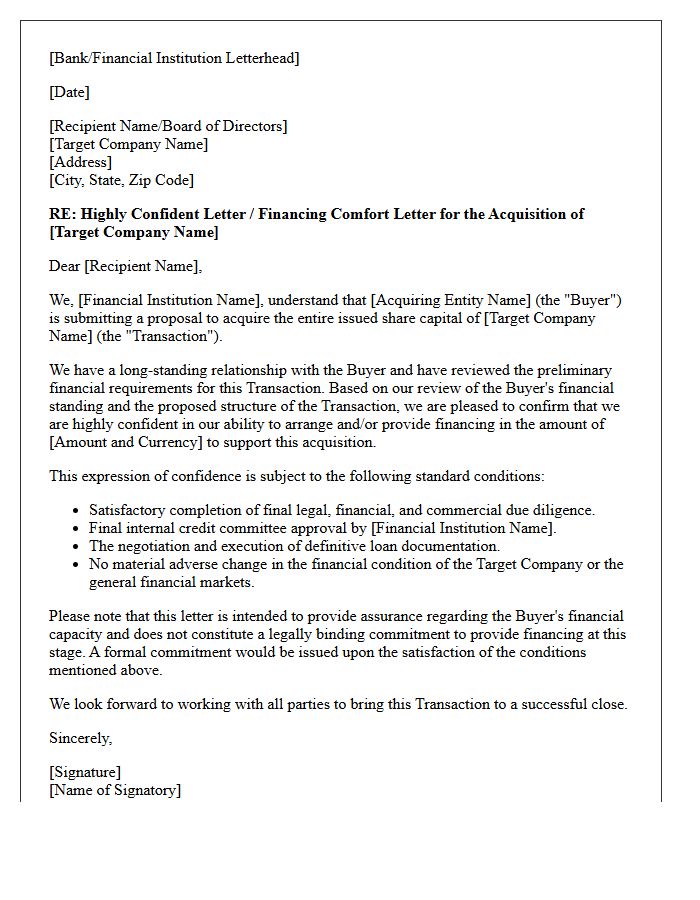

Acquisition Financing Comfort Letter

An Acquisition Financing Comfort Letter is a document issued by a bank to confirm that a buyer has the financial capacity to complete a transaction. While not a legally binding guarantee to provide funds, it serves as a critical signal of credibility during M&A negotiations. It reassures the seller that the lender has performed preliminary due diligence and intends to support the deal. For buyers, securing this letter is essential to demonstrate transaction certainty and strengthen their competitive position when bidding for a target company.

What is a comfort letter in a merger and acquisition transaction?

A comfort letter is a document issued by an independent auditor to underwriters or buyers during an M&A due diligence process. It provides negative assurance that the target company's financial statements have been reviewed and that no material changes have occurred since the last audited balance sheet.

Why are comfort letters important for M&A due diligence?

Comfort letters are essential because they bridge the gap between the last audited financial statements and the closing date of the deal. They help the buyer or underwriter establish a "due diligence defense" by verifying that financial data not covered by a full audit remains accurate and consistent with accounting standards.

What is the difference between positive and negative assurance in a comfort letter?

Positive assurance is an explicit statement that financial records comply with GAAP, typically used for audited figures. Negative assurance, which is the standard for comfort letters, states that "nothing has come to the auditor's attention" that indicates the financial data is incorrect or non-compliant, covering unaudited interim periods.

Who typically requests and receives a comfort letter?

Comfort letters are primarily requested by the investment banks or underwriters managing the transaction. While the buyer benefits from the findings, the letter is formally addressed to the parties assuming the financial risk to provide them with a layer of professional verification regarding the target's financial health.

What are the standard procedures auditors follow to issue a comfort letter?

Auditors follow professional standards, such as AS 6101, which involve performing limited procedures including reading interim financial statements, inquiring with management about financial changes, and comparing current financial data against prior periods to identify any significant fluctuations or "caps" in reporting.

Comments