A high-yield bond offering comfort letter provides essential financial assurance to underwriters during debt issuance. These documents verify that unaudited financial data aligns with accounting standards, mitigating legal risks and ensuring due diligence compliance for issuers and auditors. Understanding these reports is vital for successful capital market transactions. Below are some ready to use templates.

Image cover: Expert Guide to High-Yield Bond Comfort Letter Samples and Templates

Letter Samples List

- Initial Draft Comfort Letter

- Pricing Bring-Down Comfort Letter

- Closing Bring-Down Comfort Letter

- Negative Assurance Comfort Letter

- Agreed-Upon Procedures Comfort Letter

- Circle-Up Financial Data Comfort Letter

- Subsequent Events Review Comfort Letter

- Pro Forma Financial Information Comfort Letter

- Capsule Financial Data Comfort Letter

- Rule 144A Offering Comfort Letter

- Regulation S Offering Comfort Letter

- Underwriter Representation Comfort Letter

- Guarantor Financial Statements Comfort Letter

- Final Executed Comfort Letter

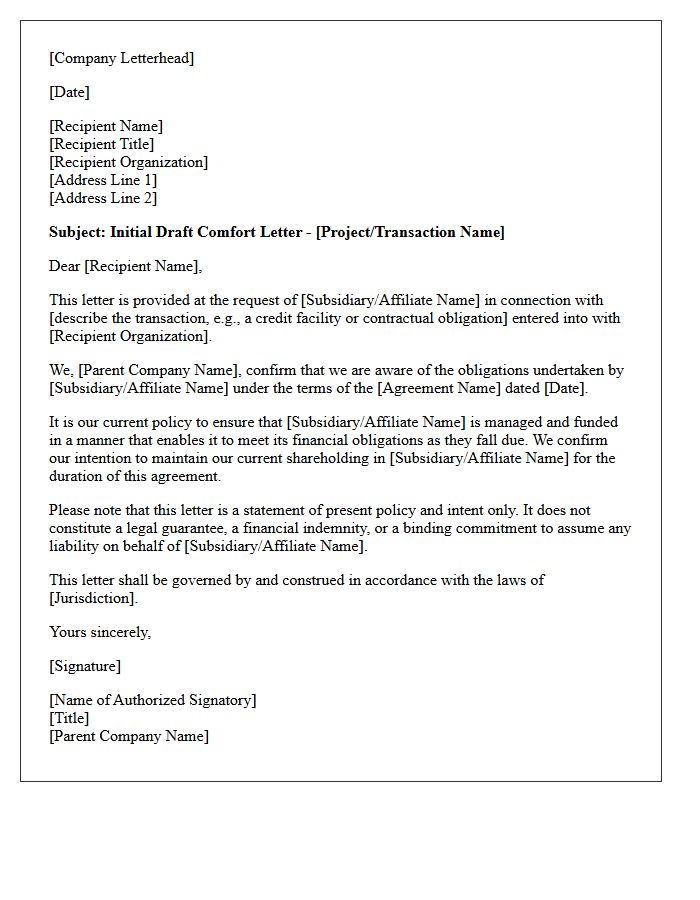

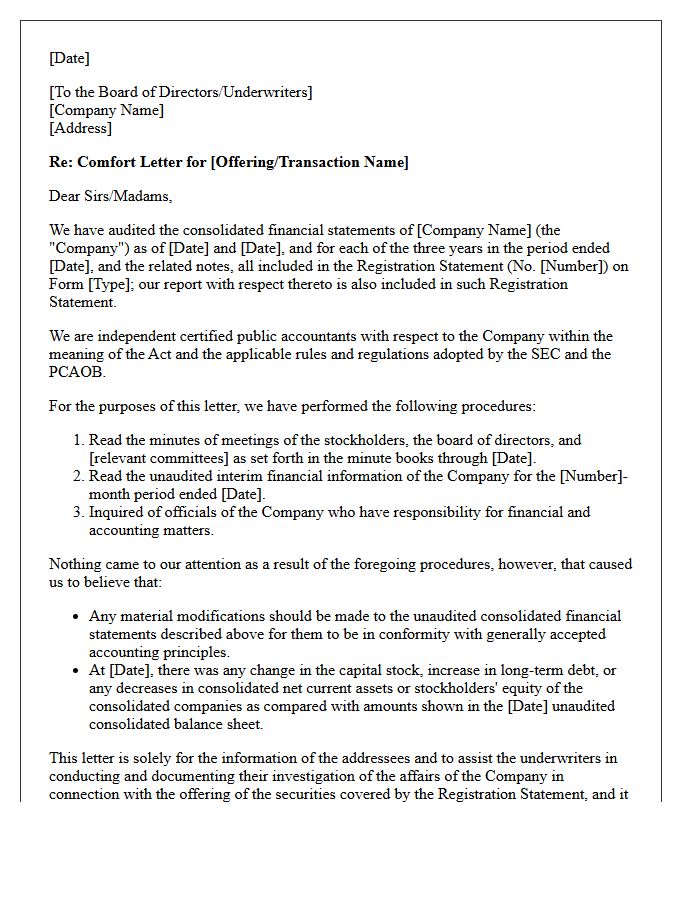

Initial Draft Comfort Letter

An Initial Draft Comfort Letter is a preliminary document issued by an independent auditor to underwriters during a securities offering. It provides negative assurance regarding the accuracy of financial data not covered by audited reports. This document serves as a critical component of due diligence, helping to protect parties from legal liabilities under securities laws. It outlines the scope of procedures the auditor intends to perform, ensuring that financial statements remain consistent and transparent before the final transaction is executed.

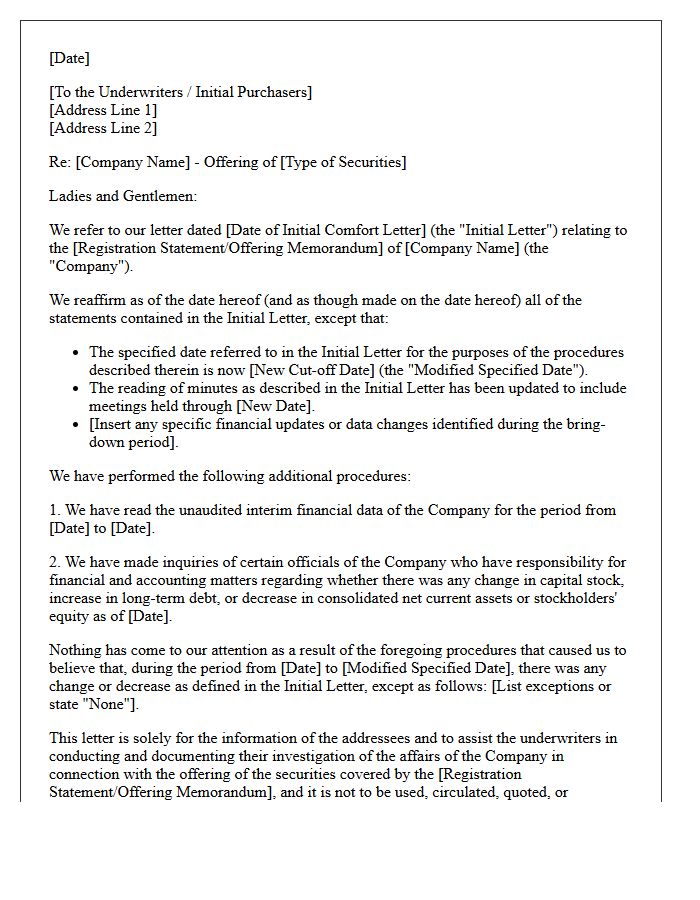

Pricing Bring-Down Comfort Letter

A Pricing Bring-Down Comfort Letter is a critical financial document issued by independent auditors to underwriters. It serves to reconfirm the financial data and negative assurances previously provided in the initial comfort letter. This update is essential because it bridges the gap between the initial signing and the actual pricing date of a securities offering. By verifying that no material adverse changes have occurred in the interim, it protects underwriters from liability and ensures the continued accuracy of the registration statement before the deal is finalized.

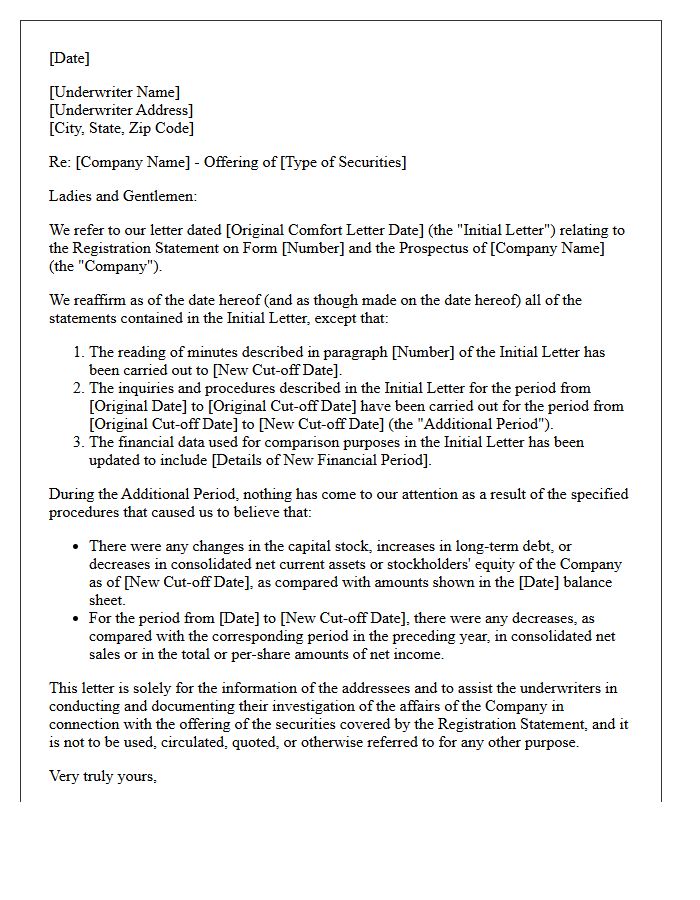

Closing Bring-Down Comfort Letter

A Closing Bring-Down Comfort Letter is a vital financial document issued by auditors at the final settlement of a securities offering. This letter confirms that no material adverse changes have occurred in the issuer's financial position since the initial cut-off date. It provides underwriters with a necessary due diligence defense, ensuring that financial data remains accurate and consistent with the registration statement. By verifying subsequent changes, it mitigates risk and validates the reliability of the financial information provided to potential investors at the moment of closing.

Negative Assurance Comfort Letter

A Negative Assurance Comfort Letter is a critical document issued by auditors to underwriters during securities offerings. It confirms that, based on a limited review, no material modifications are needed for the financial statements to align with accounting standards. Unlike a full audit, this provides limited assurance that nothing came to the auditors' attention indicating financial inaccuracies. It serves as a vital tool for due diligence, helping underwriters mitigate legal liability by demonstrating a reasonable investigation into the issuer's financial health before public distribution.

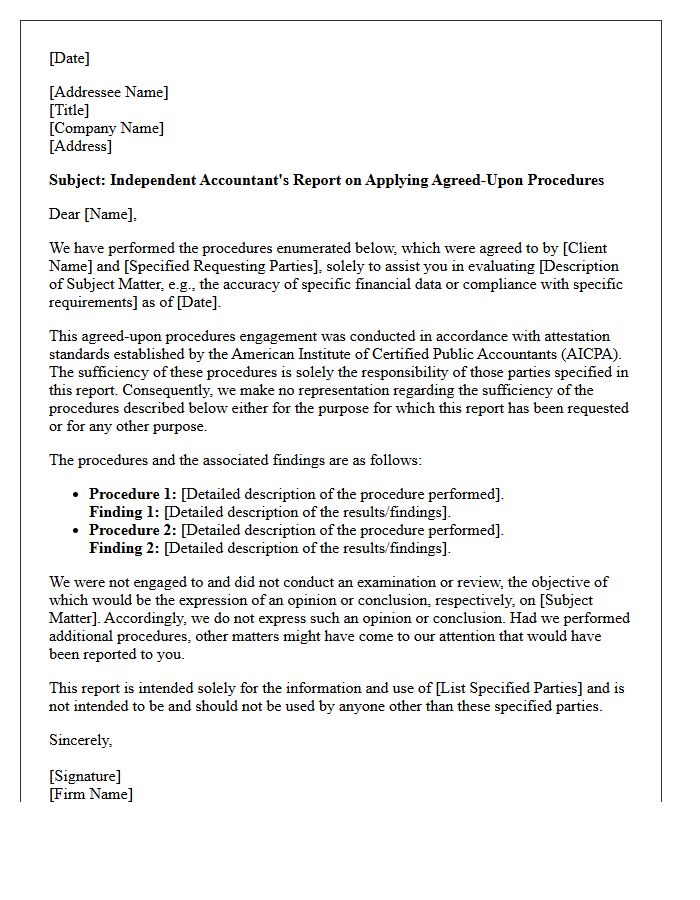

Agreed-Upon Procedures Comfort Letter

An Agreed-Upon Procedures Comfort Letter is a specialized report issued by an independent accountant to provide assurance to underwriters or lenders during financial transactions. Unlike a full audit, the practitioner performs specific financial verifications requested by the engaging party. The resulting comfort letter details factual findings without offering an official opinion. This document is essential for due diligence, helping parties mitigate risk by confirming the accuracy of financial data, subsequent changes, and compliance with specific regulatory requirements in securities offerings.

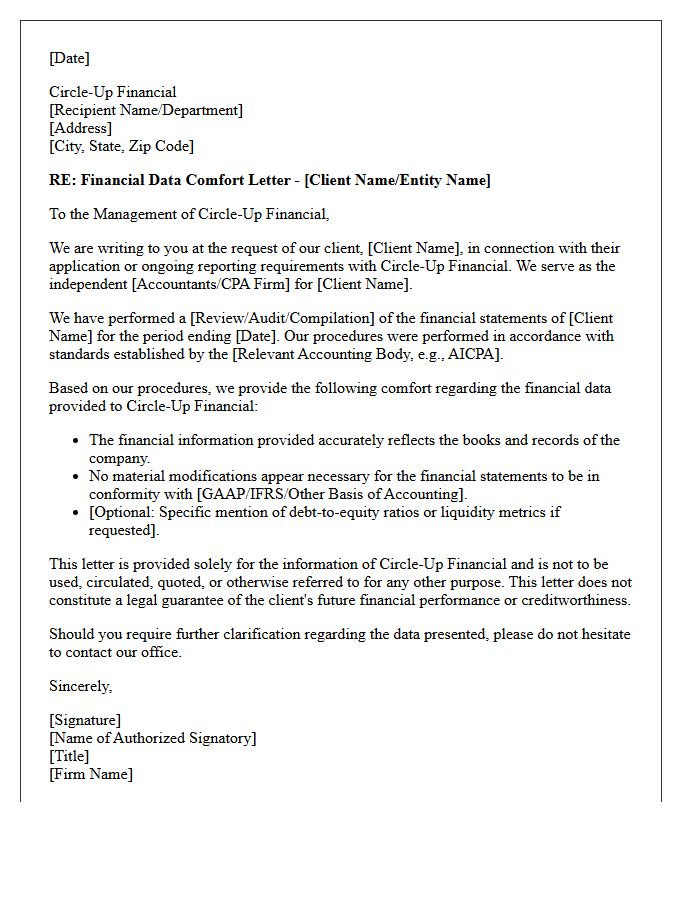

Circle-Up Financial Data Comfort Letter

A Circle-Up Financial Data Comfort Letter provides professional verification of a business's financial health, often required for underwriting or investment purposes. This document offers third-party assurance regarding the accuracy of reported metrics, helping to bridge the information gap between companies and lenders. By validating key figures like revenue and cash flow, it reduces risk and enhances transparency during funding rounds. Understanding this letter is essential for maintaining credibility and ensuring smoother financial due diligence processes within the investment ecosystem.

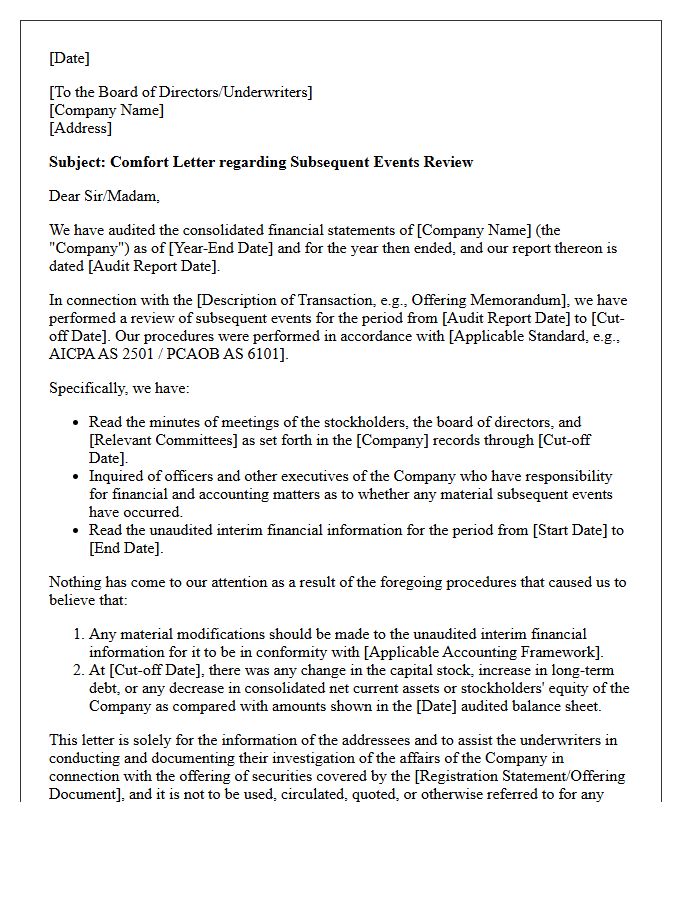

Subsequent Events Review Comfort Letter

A Subsequent Events Review is a critical procedure performed by auditors to identify material transactions occurring after the balance sheet date but before issuance. In the context of a comfort letter, underwriters require this verification to ensure financial statements remain accurate up to the effective date. This process mitigates risk by disclosing significant changes in capitalization or net interest. It provides negative assurance to parties involved in a securities offering, confirming that no material adverse changes have compromised the financial integrity of the issuer during the interim period.

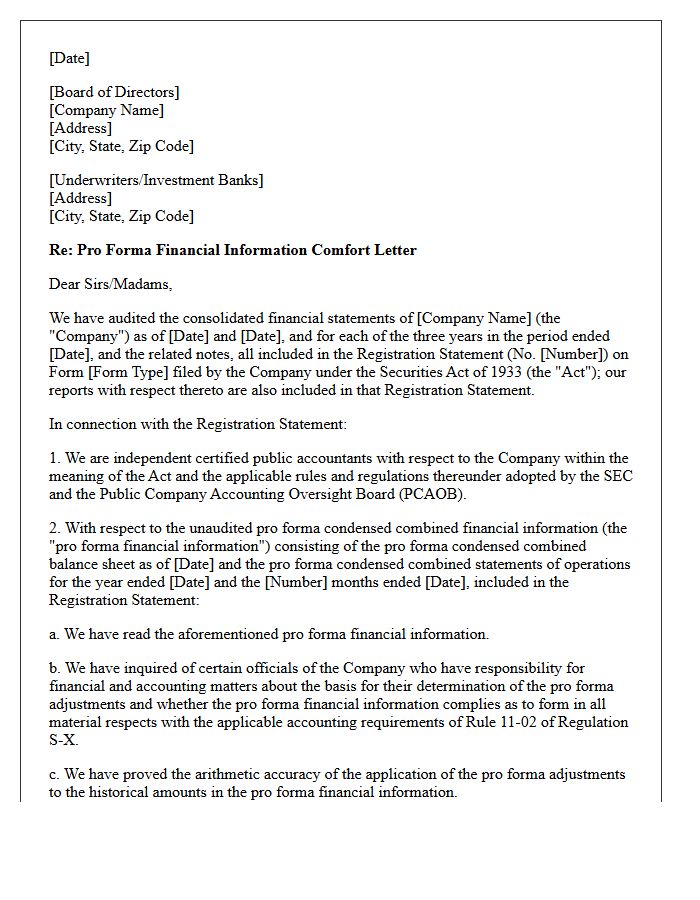

Pro Forma Financial Information Comfort Letter

A Pro Forma Financial Information Comfort Letter is a critical document issued by auditors to underwriters during securities offerings. It provides negative assurance regarding the compilation of pro forma data, ensuring it reflects the hypothetical impact of specific transactions or events. This letter confirms that the financial statements comply with SEC Regulation S-X and are based on reasonable accounting assumptions. By validating the consistency of adjustments and historical figures, the letter mitigates legal risks for financial intermediaries and enhances the credibility of the issuer's projected financial health for potential investors.

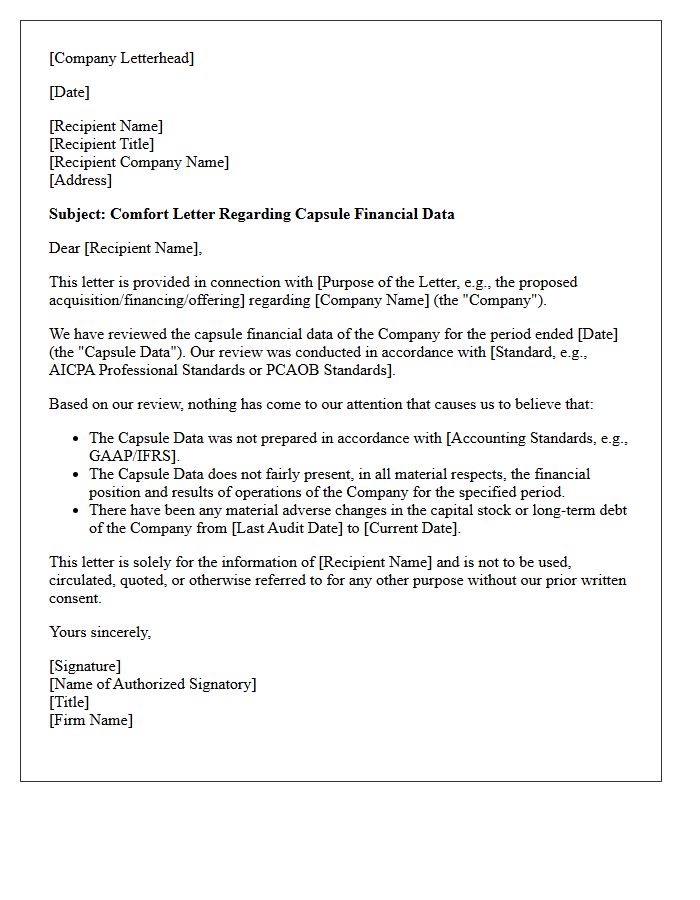

Capsule Financial Data Comfort Letter

A Capsule Financial Data Comfort Letter is a critical document issued by independent auditors to underwriters during a securities offering. It provides negative assurance that unaudited financial information for a recent period conforms to accounting standards and shows no material adverse changes. This letter bridges the reporting gap between the last audited statement and the effective date of the offering. It serves as an essential due diligence tool, helping to mitigate legal risks by verifying the accuracy of preliminary financial summaries presented to potential investors.

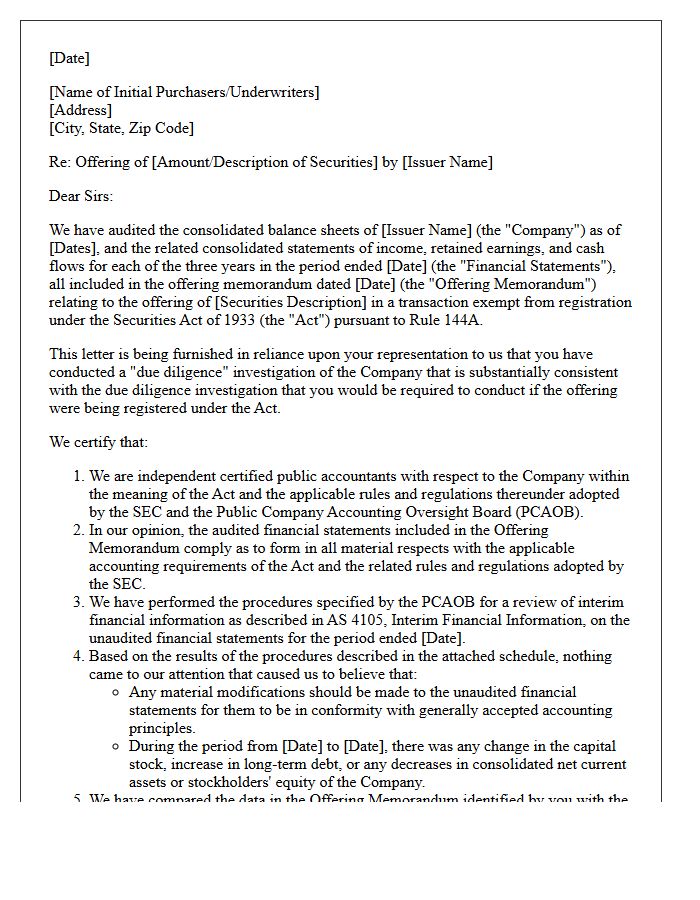

Rule 144A Offering Comfort Letter

A Rule 144A offering comfort letter is a critical document issued by independent auditors to underwriters during private placements. It provides negative assurance that the financial statements and unaudited data in the offering memorandum comply with accounting standards. This process facilitates the due diligence defense for financial intermediaries by verifying numerical accuracy. The letter mitigates legal risks under securities laws, ensuring that the qualified institutional buyers receive reliable financial information before executing transactions in the secondary market without formal SEC registration.

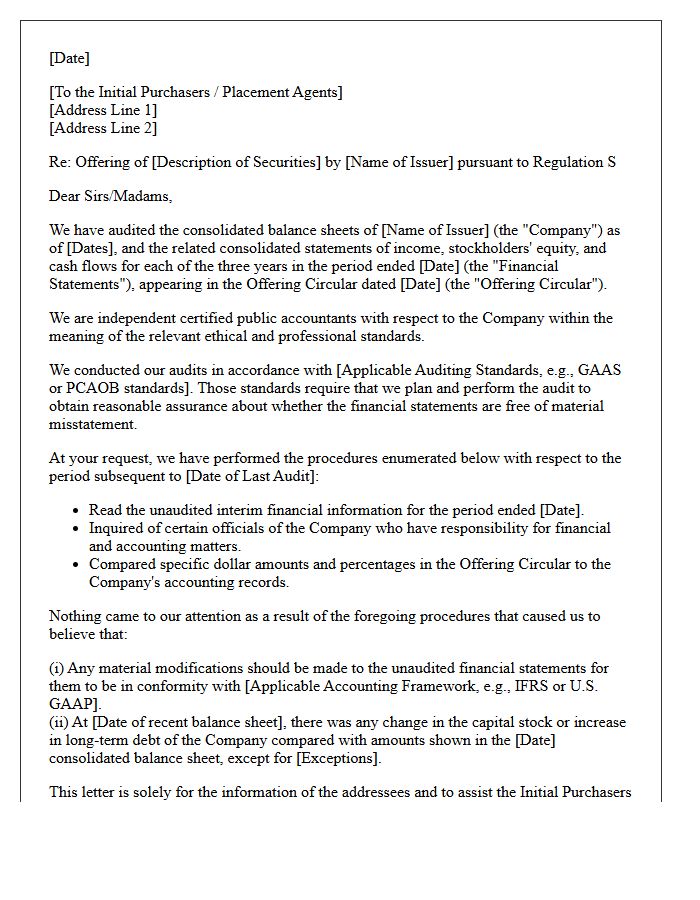

Regulation S Offering Comfort Letter

A Regulation S Offering Comfort Letter is a vital document issued by independent auditors to underwriters during offshore securities transactions. It provides negative assurance that the company's financial statements comply with accounting standards and have undergone no material adverse changes. This letter mitigates financial risk and establishes a due diligence defense for underwriters. By verifying financial data accuracy, it ensures the offering aligns with SEC Rule 901 guidelines for transactions occurring outside the United States, fostering investor confidence and legal protection for all parties involved in the international capital raise.

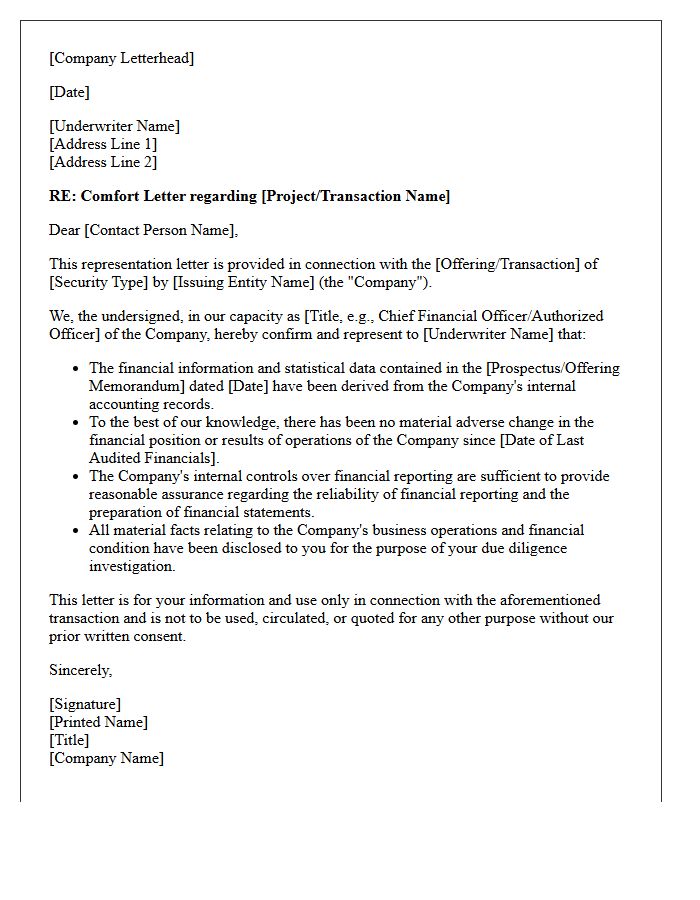

Underwriter Representation Comfort Letter

An Underwriter Representation Comfort Letter is a critical document issued by independent auditors to financial intermediaries during a securities offering. It provides negative assurance regarding the accuracy of unaudited financial data and ensures compliance with accounting standards. This process serves as a vital component of the due diligence defense, protecting underwriters from legal liability by verifying that financial statements are not misleading. By confirming that no material changes occurred since the last audit, it fosters market transparency and investor confidence during complex capital market transactions.

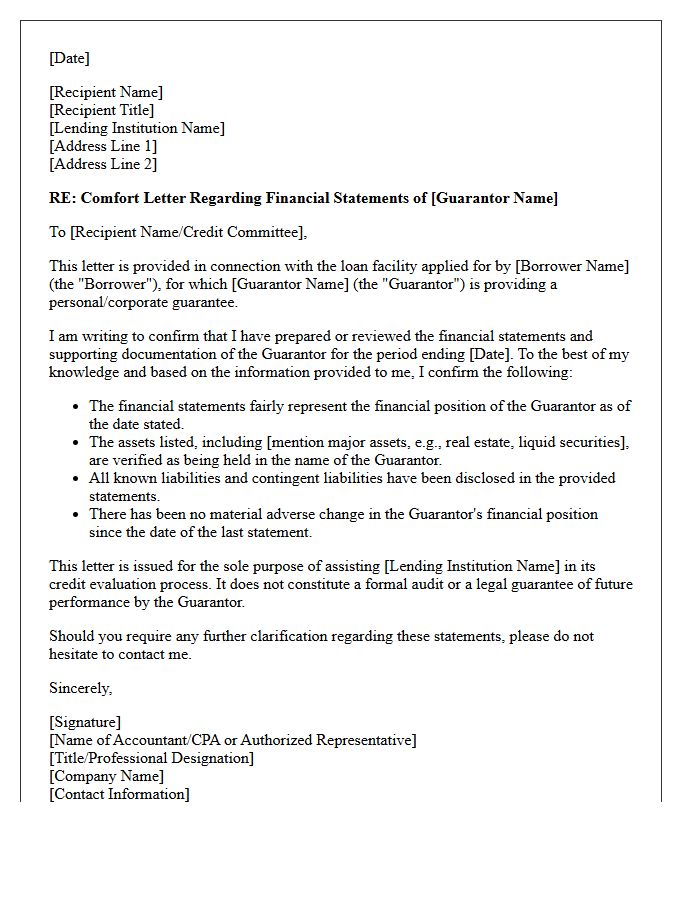

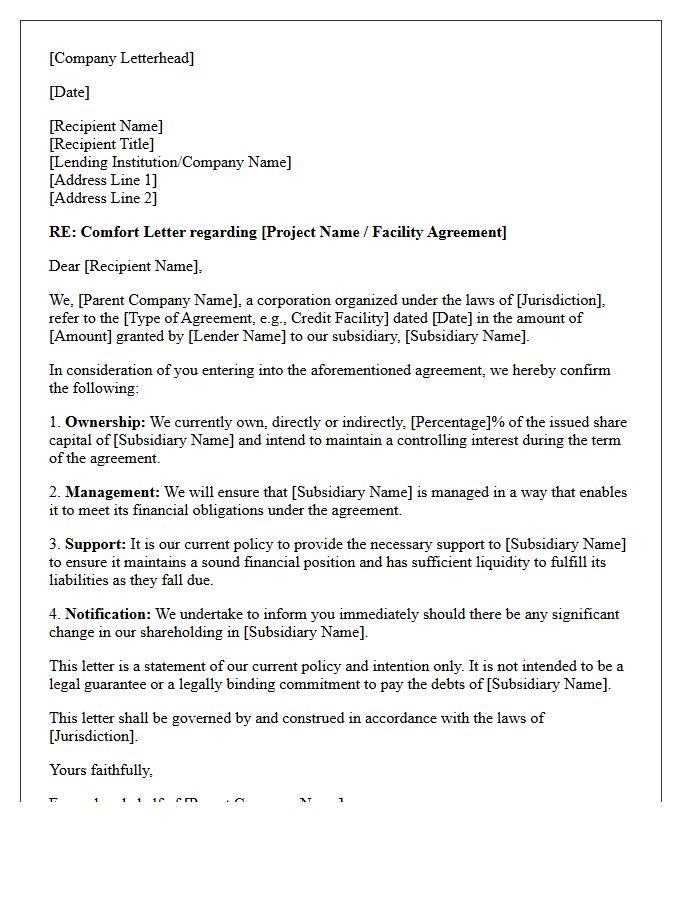

Guarantor Financial Statements Comfort Letter

A Guarantor Financial Statements Comfort Letter is a critical document issued by independent auditors to provide negative assurance regarding the financial integrity of a corporate guarantor. This letter verifies that no material adverse changes have occurred since the last audit, ensuring the subsidiary's debt is backed by a solvent parent entity. It bridges the information gap for underwriters and lenders during capital market transactions, effectively mitigating credit risk by confirming the guarantor's continued ability to fulfill its repayment obligations as outlined in the offering documents.

Final Executed Comfort Letter

A Final Executed Comfort Letter is a formal document issued by independent auditors to underwriters during a securities offering. It provides negative assurance that no material adverse changes have occurred in the issuer's financial position since the last audit. By verifying financial data not covered by audited statements, this signed letter serves as a critical due diligence tool. It mitigates legal liability for underwriters by confirming the accuracy of the financial information presented in the prospectus, ensuring regulatory compliance and investor confidence before the transaction closes.

What is the primary purpose of a comfort letter in a high-yield bond offering?

A comfort letter is issued by the issuer's independent auditors to provide "negative assurance" to underwriters, verifying that the financial data in the offering memorandum aligns with audited financial statements and that no material adverse changes have occurred since the last audit.

Which professional standards govern the issuance of comfort letters for debt securities?

In the United States, comfort letters are primarily governed by the Public Company Accounting Oversight Board (PCAOB) AS 6101 (formerly SAS 72), which establishes the framework for what auditors can verify and the specific wording required for legal due diligence defense.

What is the difference between "positive assurance" and "negative assurance" in a high-yield comfort letter?

Auditors provide positive assurance on audited financial statements, confirming they comply with GAAP. In contrast, for high-yield offerings, they provide negative assurance on unaudited interim data, stating that nothing came to their attention indicating the data is inaccurate or non-compliant.

What is a "bring-down" comfort letter in the context of a bond closing?

A bring-down comfort letter is a short-form document delivered at the closing of the bond offering that reaffirms the findings of the initial comfort letter, ensuring that no financial discrepancies have arisen between the pricing date and the settlement date.

How does a comfort letter support the "due diligence defense" for underwriters?

Under Section 11 and Section 12 of the Securities Act, underwriters can mitigate liability by showing they performed a reasonable investigation; the comfort letter serves as expert evidence that the financial information provided to investors was thoroughly vetted by an independent party.

Comments