A secondary offering comfort letter is a critical document issued by independent auditors to underwriters. It provides negative assurance regarding the financial health of a company during resale transactions by existing shareholders. This process mitigates liability risks and ensures due diligence standards are met under securities laws. To streamline your legal documentation and compliance process, below are some ready to use templates.

Image cover: Mastering Secondary Offering Comfort Letters: Samples and Essential Templates

Letter Samples List

- Draft Secondary Offering Comfort Letter

- Final Pricing Secondary Offering Comfort Letter

- Bring-Down Secondary Offering Comfort Letter

- Shelf Takedown Secondary Offering Comfort Letter

- Selling Shareholder Secondary Offering Comfort Letter

- Negative Assurance Secondary Offering Comfort Letter

- Pro Forma Financial Information Secondary Offering Comfort Letter

- Subsequent Events Secondary Offering Comfort Letter

- Capsule Financial Data Secondary Offering Comfort Letter

- Underwriter Due Diligence Secondary Offering Comfort Letter

- Agreed-Upon Procedures Secondary Offering Comfort Letter

- Block Trade Secondary Offering Comfort Letter

- Rule 144A Private Placement Secondary Offering Comfort Letter

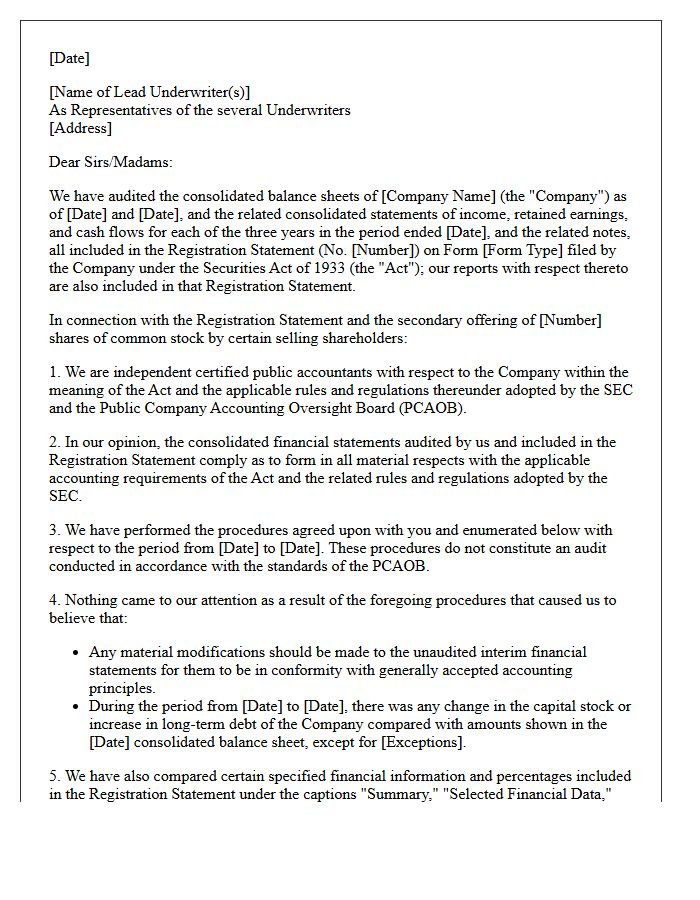

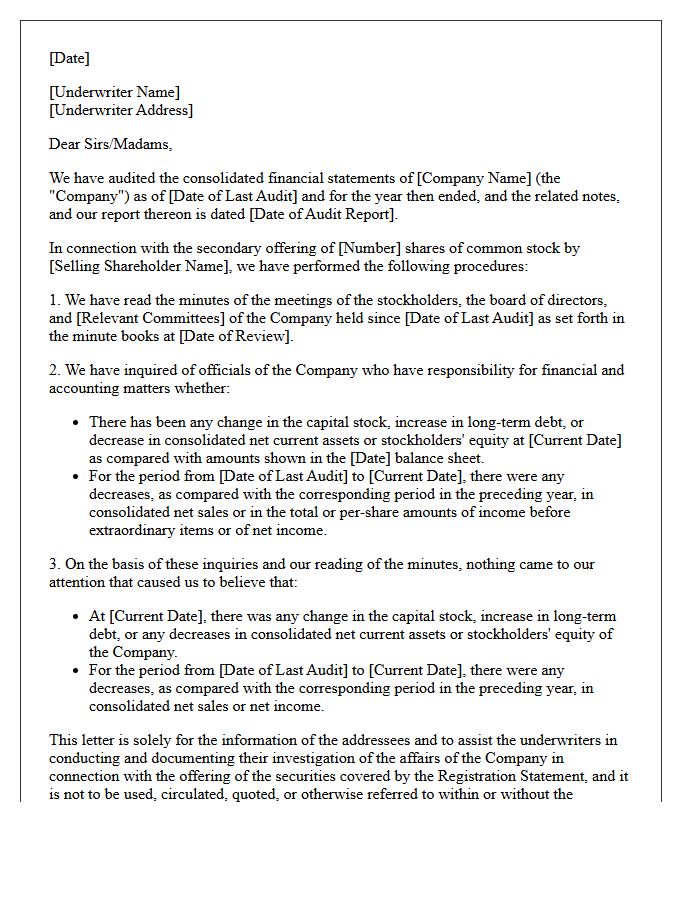

Draft Secondary Offering Comfort Letter

A Draft Secondary Offering Comfort Letter is a critical document provided by independent auditors to underwriters during a follow-on share sale. Its primary purpose is to establish due diligence by verifying that financial data in the prospectus aligns with audited records. This letter minimizes legal liability for intermediaries by providing "negative assurance" on unaudited interim figures and subsequent changes in financial position. It ensures transparency regarding the issuer's historical performance, protecting stakeholders against material misstatements during the secondary capital raise process.

Final Pricing Secondary Offering Comfort Letter

A final pricing secondary offering comfort letter is a critical document issued by auditors to underwriters. It provides negative assurance that no material changes occurred in the company's financial position between the effective date and the final pricing of the shares. This letter mitigates legal liability under the Securities Act by verifying that financial data in the prospectus remains accurate. It ensures transparency for investors and confirms the financial integrity of the offering, serving as a vital component of the due diligence process before the transaction is officially completed.

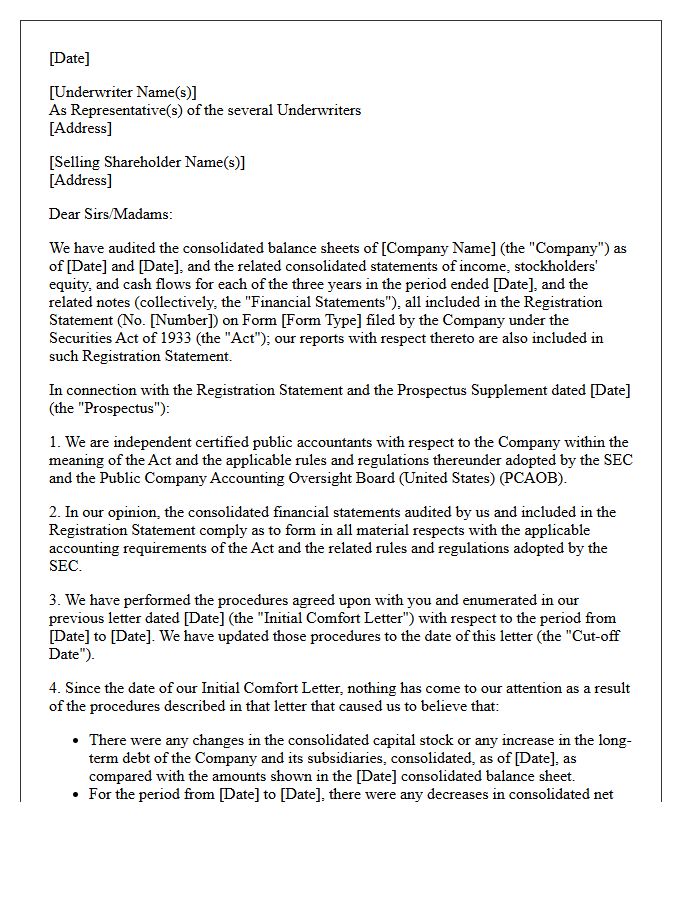

Bring-Down Secondary Offering Comfort Letter

A Bring-Down Comfort Letter is a critical document in a secondary offering that updates the initial financial assurances provided by auditors. It confirms that no material adverse changes have occurred in the company's financial position between the original audit and the closing date. This letter helps underwriters establish a due diligence defense by verifying that financial data remains accurate. It ensures transparency for investors by bridging the gap from the last comfort letter to the final sale of shares, maintaining the integrity of the secondary market transaction.

Shelf Takedown Secondary Offering Comfort Letter

A comfort letter is a critical document issued by independent auditors to underwriters during a shelf takedown secondary offering. It provides negative assurance that financial statements comply with GAAP and that no material adverse changes occurred since the last audit. This process mitigates underwriter liability under the Securities Act by demonstrating due diligence. By verifying financial data accuracy, the letter ensures market transparency and builds investor confidence during rapid capital raises from existing shelf registrations.

Selling Shareholder Secondary Offering Comfort Letter

A Secondary Offering Comfort Letter is a critical document provided by independent auditors to underwriters during a secondary sale of shares by existing stockholders. It ensures financial data accuracy and confirms that no material adverse changes occurred since the last audit. For a selling shareholder, this letter mitigates liability risks under securities laws by establishing a due diligence defense. It verifies that financial information in the prospectus aligns with audited statements, maintaining investor confidence and ensuring regulatory compliance throughout the transaction process.

Negative Assurance Secondary Offering Comfort Letter

A negative assurance statement is a critical component of a comfort letter issued by auditors during a secondary offering. It confirms that, based on specific procedures, nothing came to their attention suggesting the financial statements are materially misstated. This provides essential due diligence protection for underwriters, reducing legal liability. To receive this assurance, auditors must perform an SAS 122 review of interim financial data. It bridges the gap between audited annual reports and the current offering date, ensuring investor confidence through professional oversight without performing a full-scale audit.

Pro Forma Financial Information Secondary Offering Comfort Letter

In a secondary offering, a comfort letter provides negative assurance to underwriters regarding the reliability of financial data. Auditors verify that pro forma financial information accurately reflects the impact of hypothetical transactions based on historical results. This process ensures compliance with Regulation S-X, confirming that adjustments are mathematically sound and consistent with accounting policies. For investors, this verification reduces risk by validating that the presented adjustments realistically illustrate the company's financial position following the securities sale.

Subsequent Events Secondary Offering Comfort Letter

A comfort letter for a secondary offering is a critical due diligence document issued by auditors to underwriters. It provides negative assurance that no material changes occurred in the company's financial position during the subsequent events period following the last audit. This bridge ensures that the financial data remains reliable up to the effective date of the offering. Underwriters rely on this verification to establish a due diligence defense, mitigating legal risks associated with potential misstatements or omissions in the registration statement during the resale of shares by existing stockholders.

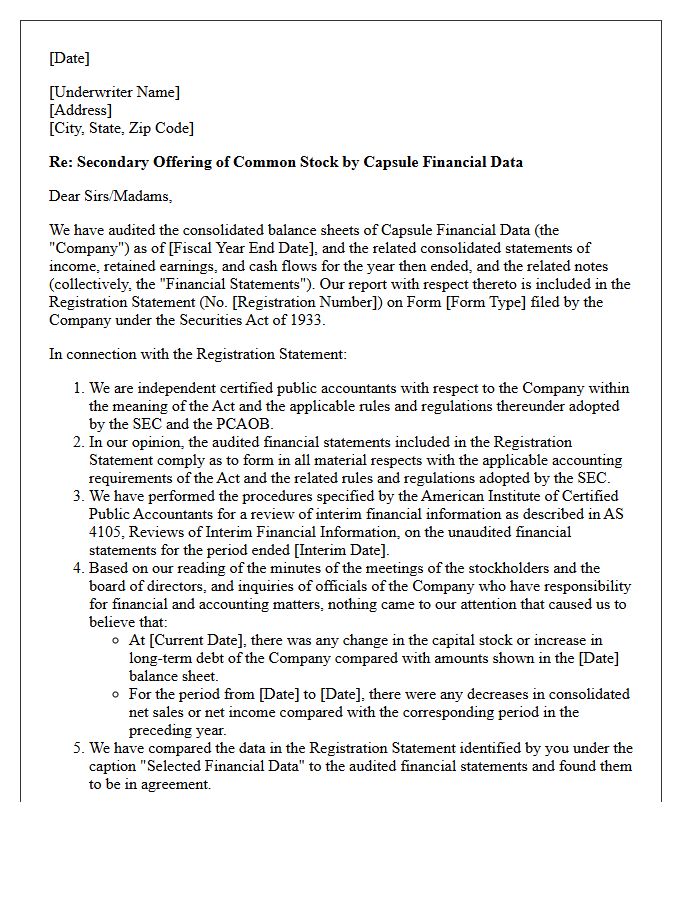

Capsule Financial Data Secondary Offering Comfort Letter

A comfort letter for a secondary offering is a critical document issued by independent auditors to underwriters. It provides negative assurance that the capsule financial data, which summarizes recent performance between formal audit periods, remains consistent with accounting standards. This process mitigates liability under securities laws by verifying that no material adverse changes have occurred. For investors and stakeholders, this letter serves as essential due diligence, confirming the financial integrity of the issuer's interim figures and ensuring the accuracy of the disclosures presented during the capital raising process.

Underwriter Due Diligence Secondary Offering Comfort Letter

In a secondary offering, underwriter due diligence is a critical legal defense requiring a "reasonable investigation" of financial data. To facilitate this, auditors issue a comfort letter, which provides negative assurance that interim financial statements align with GAAP and no material adverse changes occurred since the last audit. This document bridges the gap between audited filings and the offering date, mitigating liability risks for underwriters by verifying numerical accuracy. It serves as an essential component of the due diligence process, ensuring investor protection and regulatory compliance during capital raises.

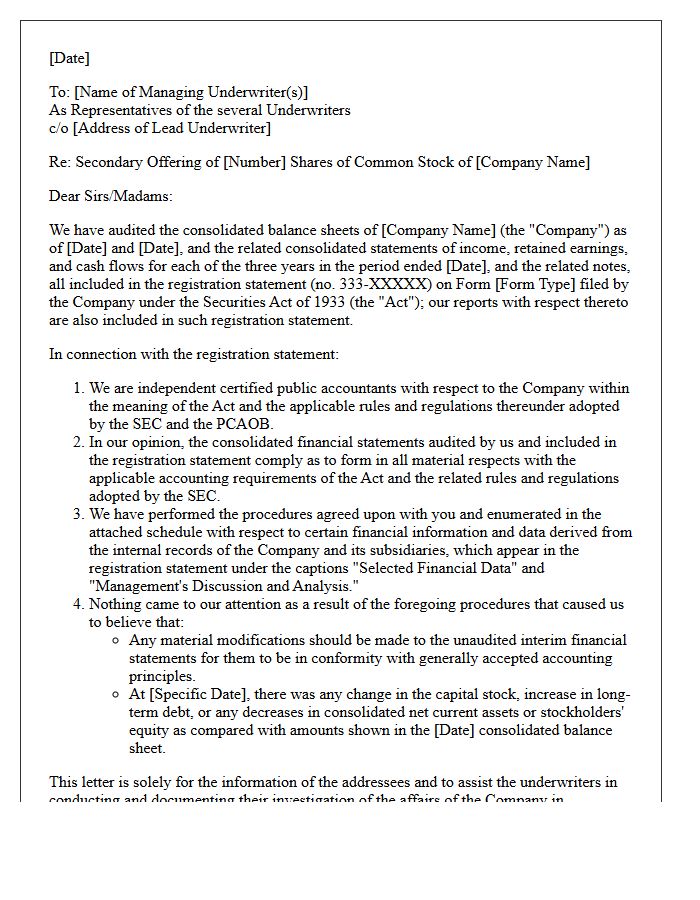

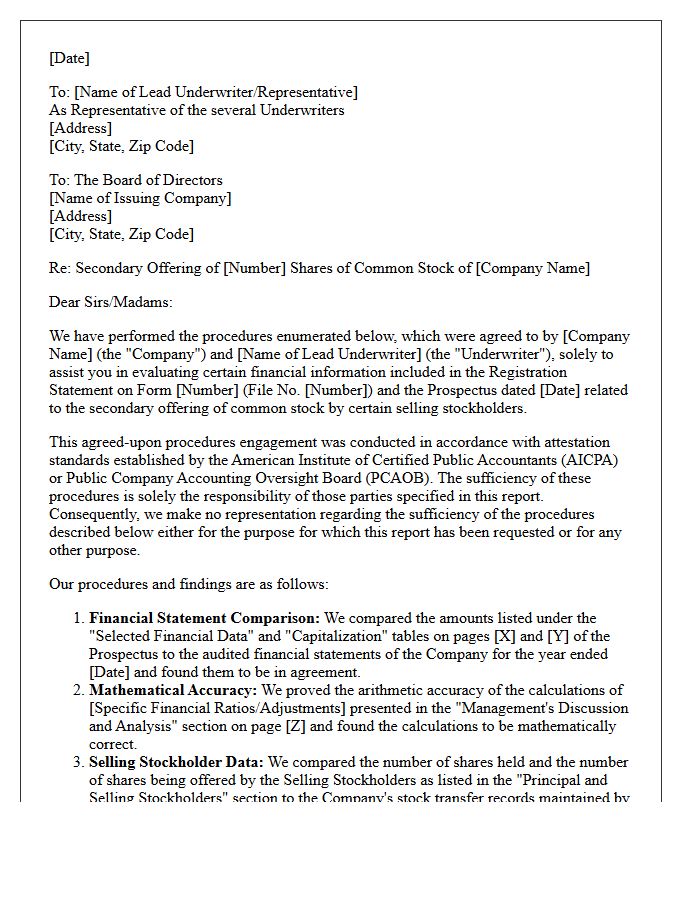

Agreed-Upon Procedures Secondary Offering Comfort Letter

An Agreed-Upon Procedures engagement for a secondary offering involves an independent auditor performing specific checks on financial data. The primary goal is to issue a comfort letter to underwriters, providing negative assurance regarding the accuracy of financial information in the registration statement. This process helps underwriters establish a due diligence defense by verifying that figures match the issuer's accounting records. It is a critical risk management tool that ensures financial transparency and minimizes legal liability during the sale of securities by existing shareholders in the secondary market.

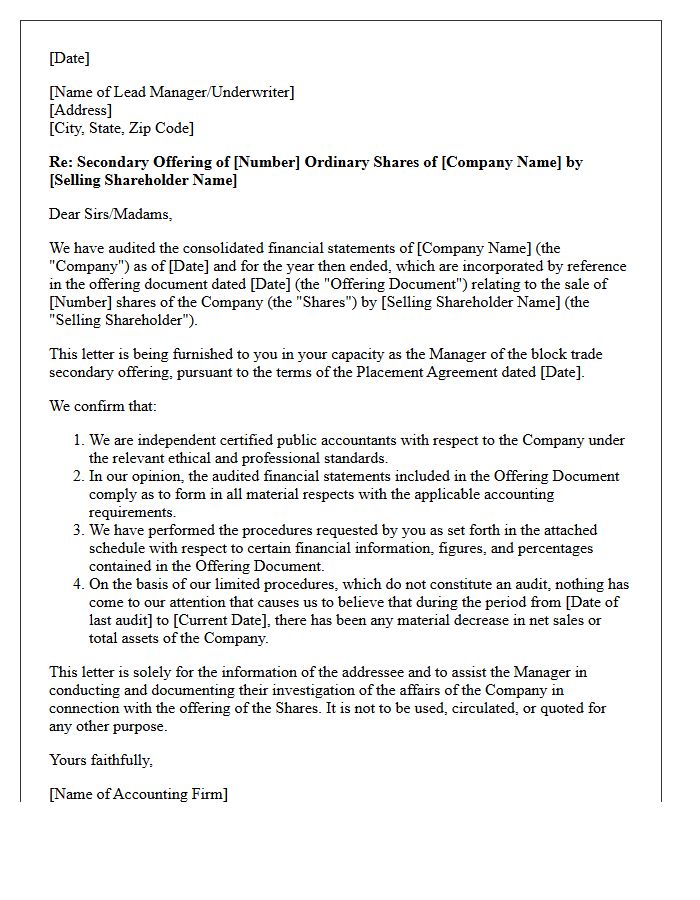

Block Trade Secondary Offering Comfort Letter

A comfort letter is a critical document issued by auditors to underwriters during a block trade or secondary offering. It provides negative assurance that the company's financial statements have not materially changed since the last audit. This verification mitigates legal risks for financial institutions by ensuring due diligence standards are met. By validating unaudited financial data, the letter builds investor confidence and facilitates the rapid execution of large-scale share liquidations in the secondary market.

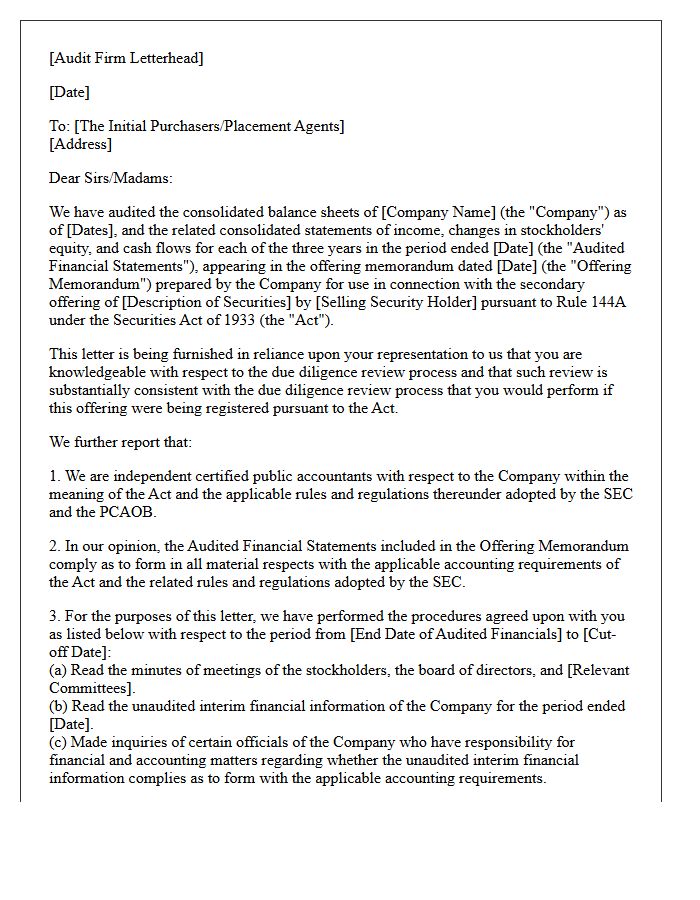

Rule 144A Private Placement Secondary Offering Comfort Letter

A Rule 144A comfort letter is a vital document provided by independent auditors to underwriters during a private placement. It ensures due diligence by verifying that financial data in the offering memorandum aligns with audited records. This letter mitigates legal liability for intermediaries facilitating the secondary offering to Qualified Institutional Buyers (QIBs). By confirming no material adverse changes have occurred since the last audit, it provides the necessary assurance to institutional investors that the issuer's financial disclosures remain accurate and consistent with professional accounting standards.

What is a comfort letter in a secondary offering?

A comfort letter is a document issued by an independent auditor to underwriters during a secondary offering. it provides negative assurance that the company's unaudited financial data, interim statements, and subsequent changes in financial position comply with GAAP and SEC requirements.

Why do underwriters require a comfort letter for secondary offerings?

Underwriters require a comfort letter as part of their "due diligence" defense under Section 11 of the Securities Act of 1933. It helps verify that the financial information provided by the selling shareholders or the issuing company is accurate and has not materially deteriorated since the last audited balance sheet.

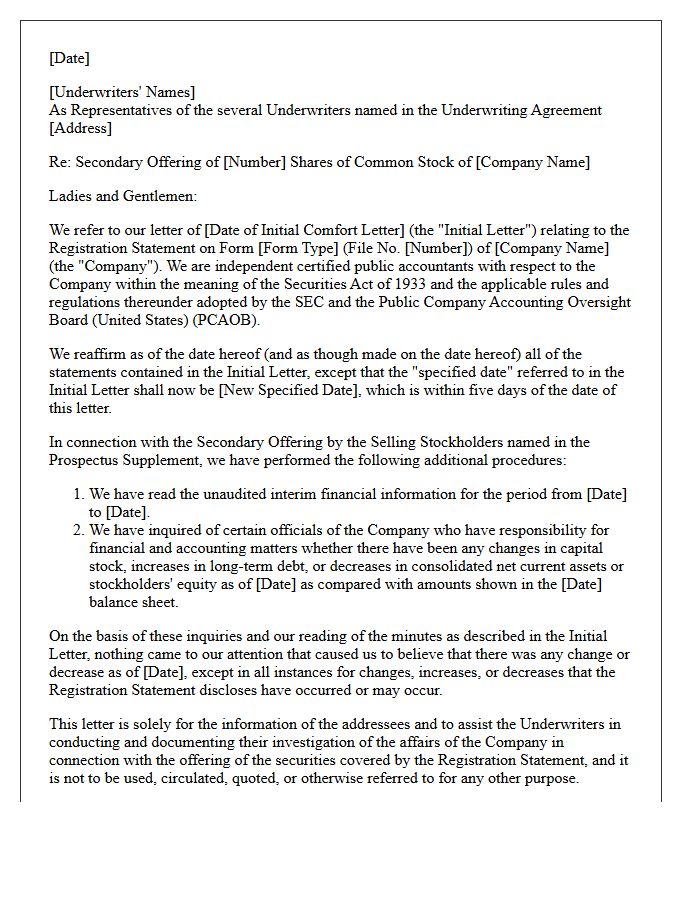

What is the difference between a "bring-down" comfort letter and the initial comfort letter?

The initial comfort letter is delivered at the time the underwriting agreement is signed, covering data up to that date. The "bring-down" comfort letter is delivered at the closing of the secondary offering to confirm that no material adverse changes have occurred between the signing and the delivery of the shares.

Which professional standards govern the issuance of comfort letters?

Comfort letters are primarily governed by the Public Company Accounting Oversight Board (PCAOB) AS 6101 (formerly SAS 72). These standards dictate the specific procedures auditors must follow and the language they must use to provide negative assurance on financial information.

What specific financial information is typically covered in a secondary offering comfort letter?

The letter typically covers unaudited interim financial statements, pro forma financial information, and "capsule" financial data. It also includes a "tick-and-tie" verification of specific figures, percentages, and financial ratios found throughout the prospectus or offering memorandum.

Comments