A Syndicated Loan Agreement Comfort Letter serves as a critical document providing assurance from a parent company regarding a subsidiary's financial obligations. While not a formal guarantee, it strengthens creditworthiness and builds trust among participating lenders during complex financing arrangements. Understanding its legal nuances is essential for risk management. To assist your documentation process, below are some ready to use template.

Image cover: Strategic Comfort Letter Templates for Syndicated Loan Agreements

Letter Samples List

- Agreed-Upon Procedures Comfort Letter

- Negative Assurance Comfort Letter

- Syndicated Loan Bring-Down Comfort Letter

- Financial Covenant Compliance Comfort Letter

- Pro Forma Financial Information Comfort Letter

- Subsequent Events Comfort Letter

- Auditor Independence Confirmation Letter

- Working Capital Requirements Comfort Letter

- Borrowing Base Calculation Comfort Letter

- Syndication Engagement Reliance Letter

- Draft Financial Statements Comfort Letter

- Material Adverse Change Assurance Letter

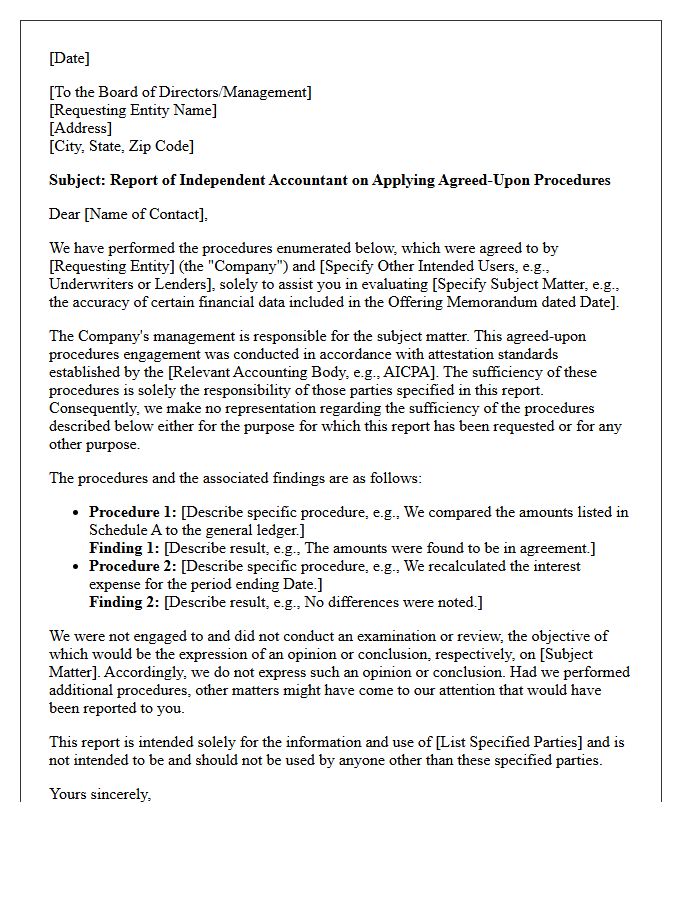

Agreed-Upon Procedures Comfort Letter

An Agreed-Upon Procedures Comfort Letter is a specialized report issued by independent auditors to underwriters or lenders during financial transactions. Unlike a full audit, the accountant performs specific testing procedures requested by the client and reports factual findings without providing a formal opinion. It is crucial for establishing due diligence and mitigating risk in securities offerings. By validating financial data and subsequent changes, these letters provide assurance regarding the accuracy of information included in registration statements or offering memorandums, ensuring transparency for all parties involved in the investment process.

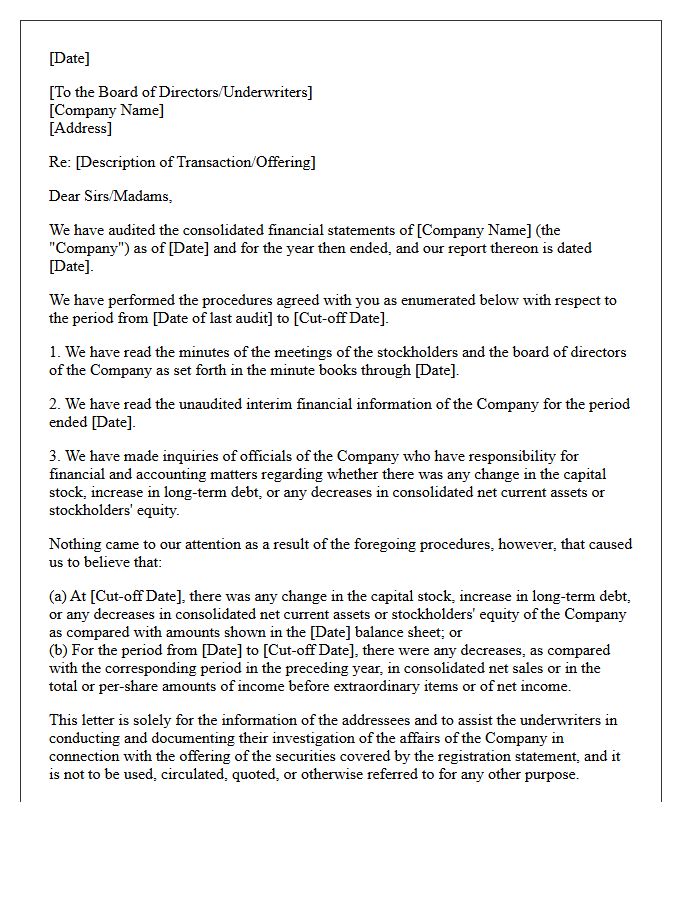

Negative Assurance Comfort Letter

A Negative Assurance Comfort Letter is a critical document issued by independent auditors to underwriters during securities offerings. It provides a statement of belief that, based on specific procedures, no material modifications are required for the financial statements to conform with accounting standards. While not a full audit, it reduces legal risk by demonstrating due diligence under the Securities Act. This letter bridges the gap between the last audit and the effective date of the offering, ensuring financial transparency and building investor confidence during capital market transactions.

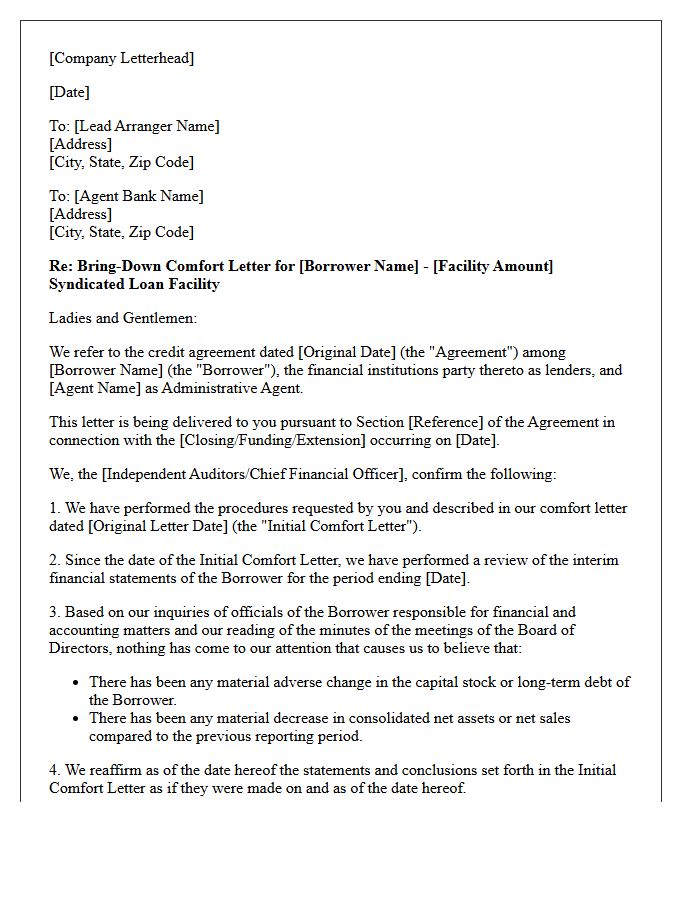

Syndicated Loan Bring-Down Comfort Letter

A Syndicated Loan Bring-Down Comfort Letter is a critical financial document issued by auditors to confirm that a borrower's financial condition hasn't materially deteriorated since the last audit. It serves as an update to the initial comfort letter, ensuring that financial statements remain reliable during the closing period. This process mitigates risk for the lending syndicate by verifying negative assurance regarding subsequent changes. For lead arrangers, this document is essential for maintaining due diligence standards and securing the final funding commitment under the agreed credit facility terms.

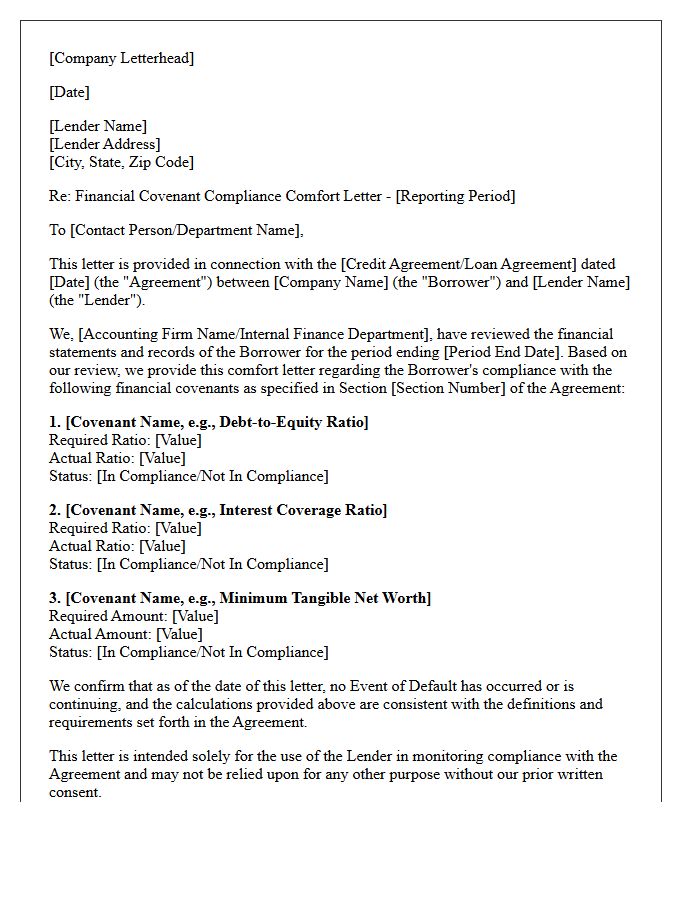

Financial Covenant Compliance Comfort Letter

A Financial Covenant Compliance Comfort Letter is a formal document issued by an independent auditor to lenders. It provides negative assurance that a borrower's financial statements align with specific loan agreement ratios. This letter confirms that the calculations used to determine covenant compliance are mathematically accurate and based on audited data. It serves as a critical risk mitigation tool, offering creditors extra confidence in the borrower's financial stability and reporting integrity during the life of a loan or after a significant corporate transaction.

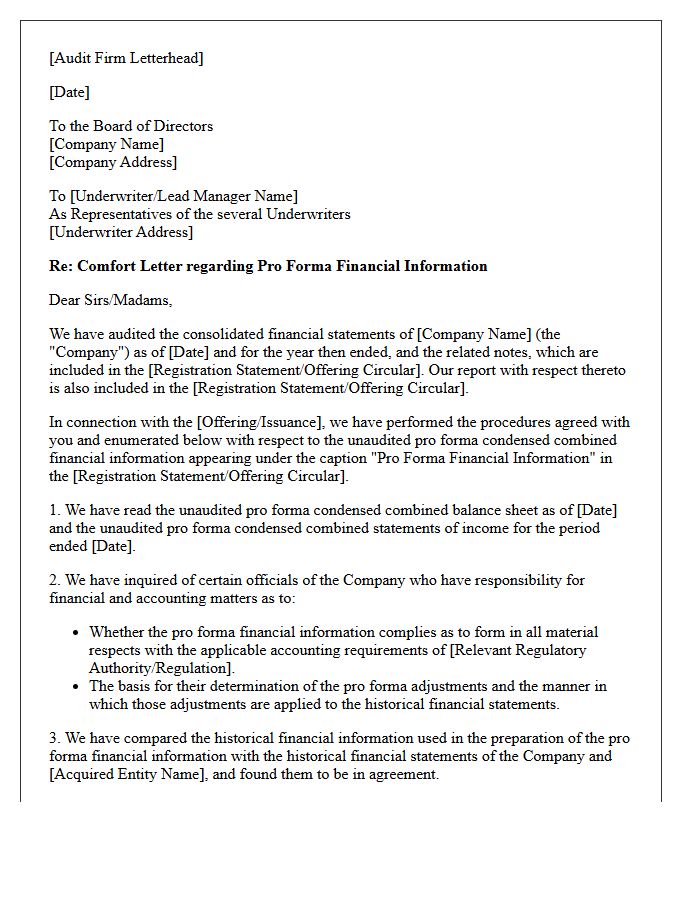

Pro Forma Financial Information Comfort Letter

A Pro Forma Financial Information Comfort Letter is a critical document issued by auditors to underwriters during securities offerings. It provides negative assurance that pro forma adjustments comply with applicable accounting regulations and reflect the hypothetical impact of specific transactions. This letter verifies that financial statements are mathematically accurate and logically consistent with Regulation S-X guidelines. By validating these forward-looking estimates, auditors help mitigate legal liability and ensure due diligence, offering investors increased confidence in the projected financial position of the issuing company following a merger, acquisition, or restructuring event.

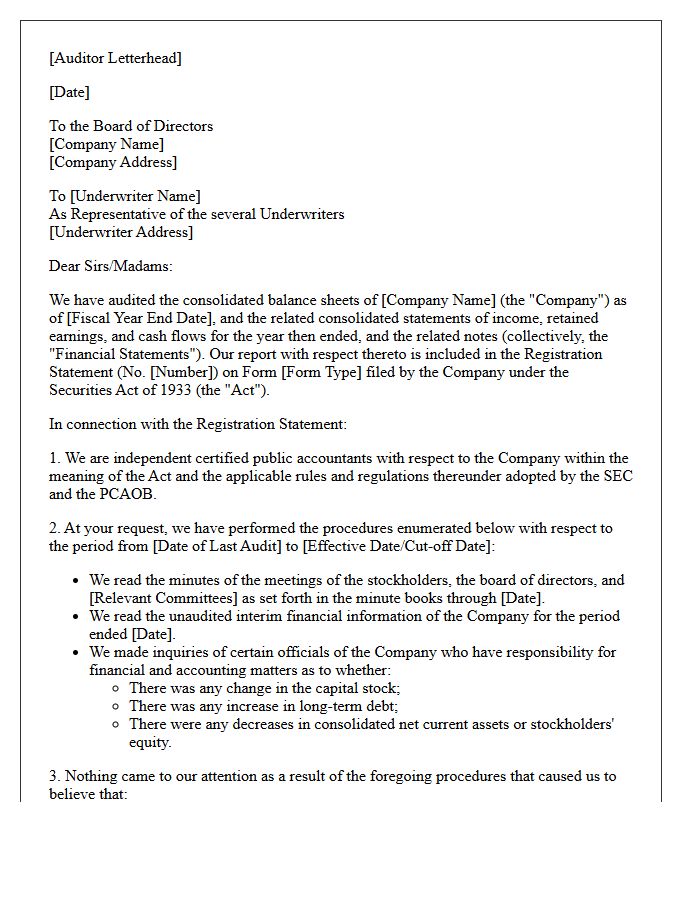

Subsequent Events Comfort Letter

A Subsequent Events Comfort Letter is a critical document provided by auditors to underwriters during securities offerings. It confirms that no material changes occurred in the company's financial position between the last audit and the effective date of the registration statement. Auditors perform a negative assurance review, examining interim records and minutes to identify potential risks. This process mitigates liability under the Securities Act by establishing due diligence, ensuring investors receive the most current financial insights before a transaction is finalized.

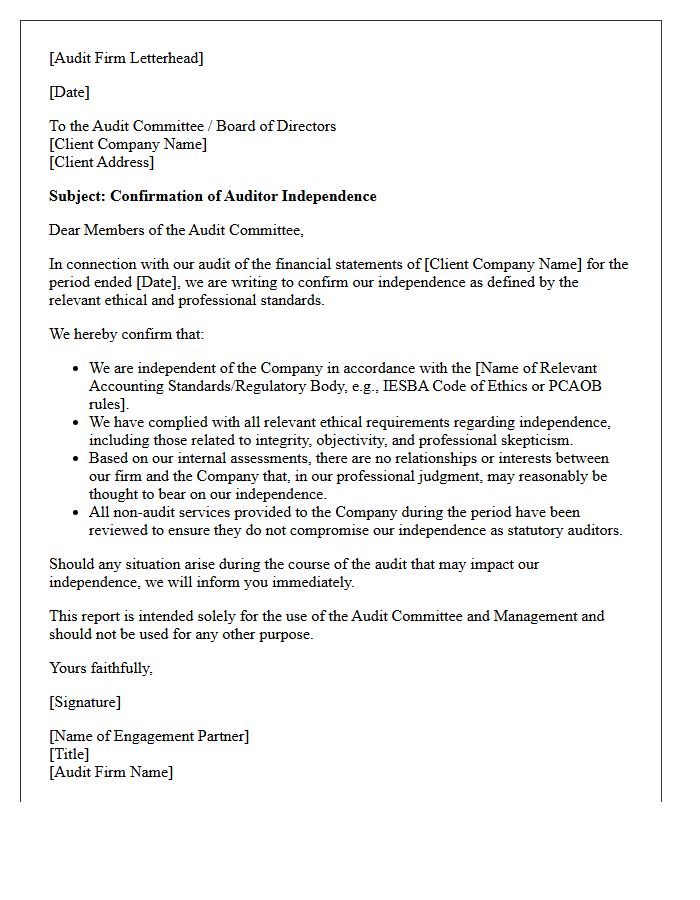

Auditor Independence Confirmation Letter

An Auditor Independence Confirmation Letter is a formal document verifying that an external auditor maintains objective impartiality from their client. Required by regulatory standards like PCAOB or IESBA, it confirms the absence of financial, familial, or professional conflicts of interest that could compromise an audit's integrity. This statement ensures stakeholder trust by certifying that the audit firm remains unbiased. It is a critical component of corporate governance, providing the audit committee with written assurance that the auditor's professional judgment remains untainted throughout the financial reporting process.

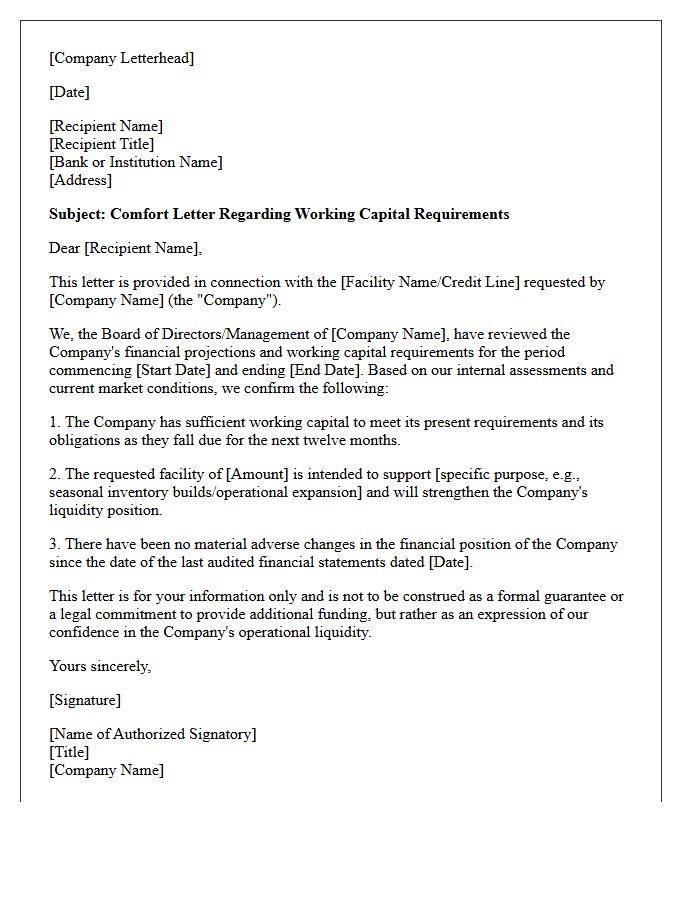

Working Capital Requirements Comfort Letter

A Working Capital Requirements Comfort Letter is a formal document issued by an auditor or financial institution to provide assurance regarding a company's liquidity position. It confirms that the entity possesses sufficient funds to meet its short-term obligations and operational needs for a specific period, typically twelve months. This letter is crucial during capital raises or IPOs, as it builds investor confidence by validating financial stability. It ensures that the business can sustain its ongoing activities without facing immediate solvency risks or requiring emergency financing interventions.

Borrowing Base Calculation Comfort Letter

A Borrowing Base Calculation Comfort Letter is a formal document issued by an external auditor to provide assurance regarding a borrower's reported asset values. It validates the accuracy of collateral, such as inventory and receivables, which determine the available credit limit. Lenders require this to mitigate risk and ensure the collateral integrity supports the loan amount. By verifying underlying financial data, the letter enhances transparency between the parties, confirming that the borrowing base certificate aligns with agreed-upon formulas and reporting standards throughout the financing period.

Syndication Engagement Reliance Letter

A Syndication Engagement Reliance Letter is a critical legal document allowing third-party lenders to rely on the due diligence and reports prepared by a lead arranger. It bridges the gap between the original underwriting and the broader syndication group, ensuring all participants have a shared legal basis for credit decisions. This letter mitigates risk by establishing formal accountability and defining the scope of liability. Understanding this document is essential for financial institutions to ensure transparency and protect their legal standing throughout the collaborative lending process.

Draft Financial Statements Comfort Letter

A Draft Financial Statements Comfort Letter is a document issued by independent auditors to underwriters during due diligence. It provides negative assurance, confirming that no material changes have occurred since the last audit. This letter helps stakeholders mitigate financial risk by validating that preliminary figures align with accounting standards. It is a critical component in capital market transactions, ensuring transparency and building investor confidence before a formal offering is finalized. Although not a full audit, it serves as a vital verification tool for financial accuracy.

Material Adverse Change Assurance Letter

A Material Adverse Change (MAC) Assurance Letter is a formal document used in financial transactions to confirm that no significant negative events have occurred since the last financial disclosure. It provides legal certainty to lenders or buyers that the target entity's financial stability and operational integrity remain intact. This assurance minimizes risk exposure during the closing period of a deal. If a substantial decline in value or performance is detected, the letter allows the parties to renegotiate terms or terminate the agreement to prevent financial loss.

What is a comfort letter in a syndicated loan agreement?

A comfort letter is a document issued by a parent company or a third party to a lending syndicate, providing assurance regarding the financial health, management stability, or support of a subsidiary borrower without creating a legally binding guarantee.

What is the difference between a comfort letter and a legal guarantee?

Unlike a legal guarantee, which creates a binding obligation to repay a debt if the borrower defaults, a comfort letter is generally a "statement of intent" or moral obligation that provides psychological assurance to lenders rather than a direct claim on the issuer's assets.

Why do lenders in a syndicated loan request a comfort letter?

Lenders request comfort letters when a parent company is unwilling to provide a full guarantee, yet the syndicate requires confirmation that the parent intends to maintain its shareholding and ensure the subsidiary remains in a position to meet its financial obligations.

Are comfort letters legally enforceable in court?

The enforceability of a comfort letter depends on its specific wording; while most are drafted as non-binding statements of policy, courts may deem them legally binding if the language includes promissory terms such as "we undertake" or "we ensure" rather than mere expressions of intent.

What are the common levels of commitment in a comfort letter?

Comfort letters typically range from "weak" (acknowledging the loan and stating ownership policy) to "strong" (confirming the intent to support the subsidiary's liquidity), though they are carefully structured by legal counsel to avoid being classified as a formal indemnity or guarantee.

Comments