Effective financial oversight requires a robust Management Letter on Going Concern Assessment and Liquidity Risk Mitigation. This article explores essential strategies for evaluating operational viability, identifying solvency threats, and implementing proactive cash flow controls to satisfy auditing standards and ensure long-term stability. Learn how to document management's plans and address potential uncertainties clearly. To assist your process, below are some ready to use template.

Image cover: Navigating Going Concern Assessments and Liquidity Risk Strategies: Best Practice Templates for Management Letters

Letter Samples List

- Management Letter on Going Concern Assessment

- Auditor Letter Regarding Liquidity Risk Mitigation

- Client Representation Letter on Going Concern Matters

- Advisory Letter on Short-Term Liquidity Constraints

- Deficiency Letter on Cash Flow Forecasting Controls

- Engagement Letter for Solvency and Liquidity Review

- Audit Communication Letter on Debt Covenant Breaches

- Recommendation Letter for Liquidity Mitigation Strategies

- Follow-Up Letter on Management Remediation Plans

- Assurance Letter on Capital Infusion Initiatives

- Observation Letter Regarding Working Capital Deficits

- Concluding Letter on Going Concern Viability

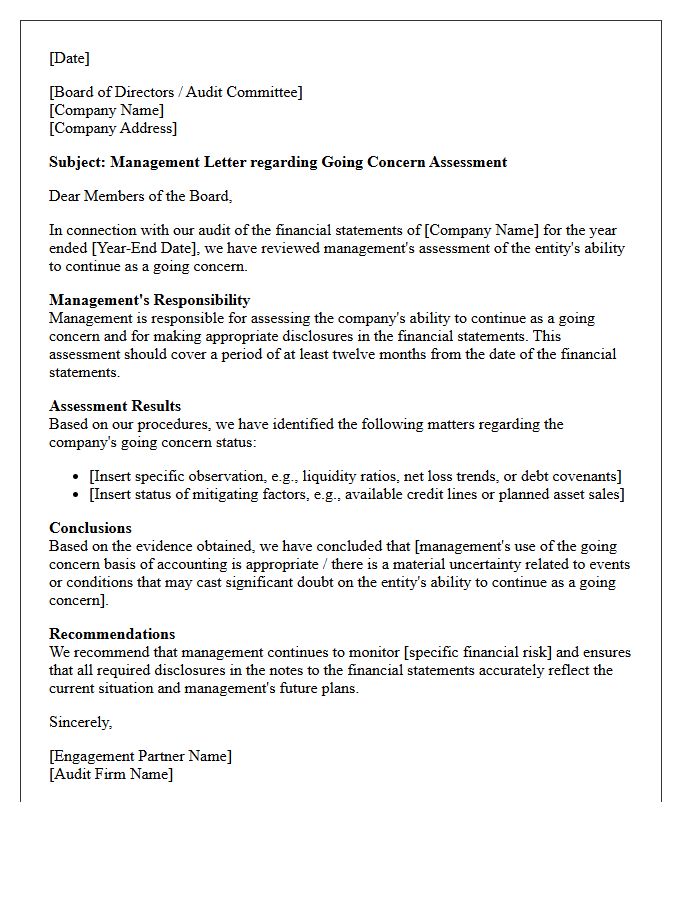

Management Letter on Going Concern Assessment

A management letter on going concern assessment provides critical written representations regarding an entity's ability to continue operations for at least twelve months. It outlines management responsibilities for identifying material uncertainties that could cast doubt on business continuity. Auditors analyze this document to evaluate financial viability, risk mitigation plans, and the adequacy of financial statement disclosures. This formal communication is a vital component of the audit process, ensuring transparency between leadership and stakeholders concerning the organization's long-term operational stability and future solvency.

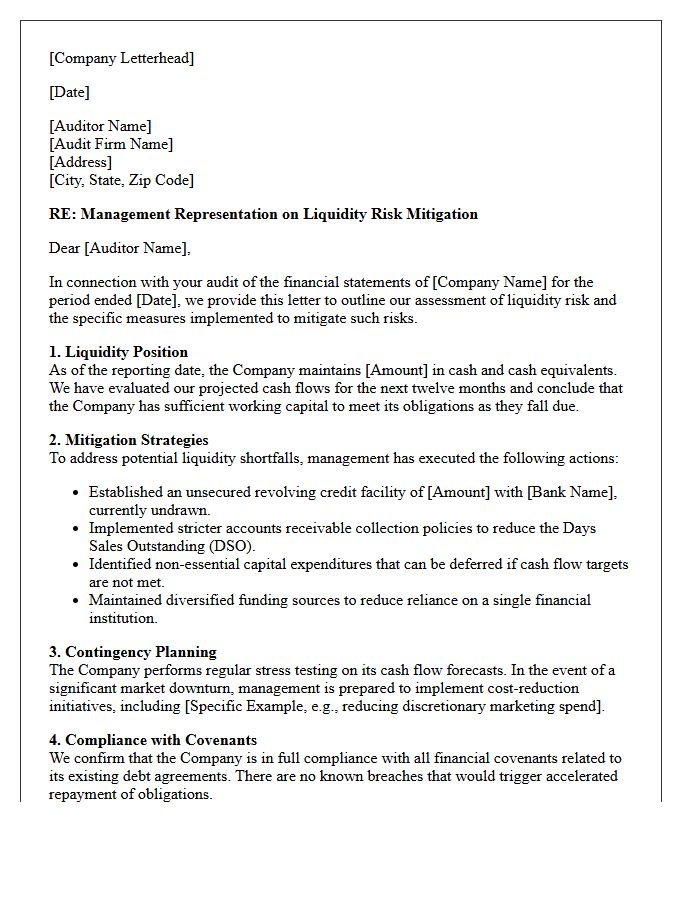

Auditor Letter Regarding Liquidity Risk Mitigation

An Auditor Letter Regarding Liquidity Risk Mitigation provides critical assurance that a company maintains sufficient cash flow and financial resources to meet its short-term obligations. This formal statement evaluates management's strategies, such as credit facilities or asset sales, to prevent insolvency. For stakeholders, it serves as a vital indicator of going concern status, confirming the entity can survive potential financial distress. Understanding this document is essential for assessing financial stability and ensuring the business remains operational under adverse economic conditions.

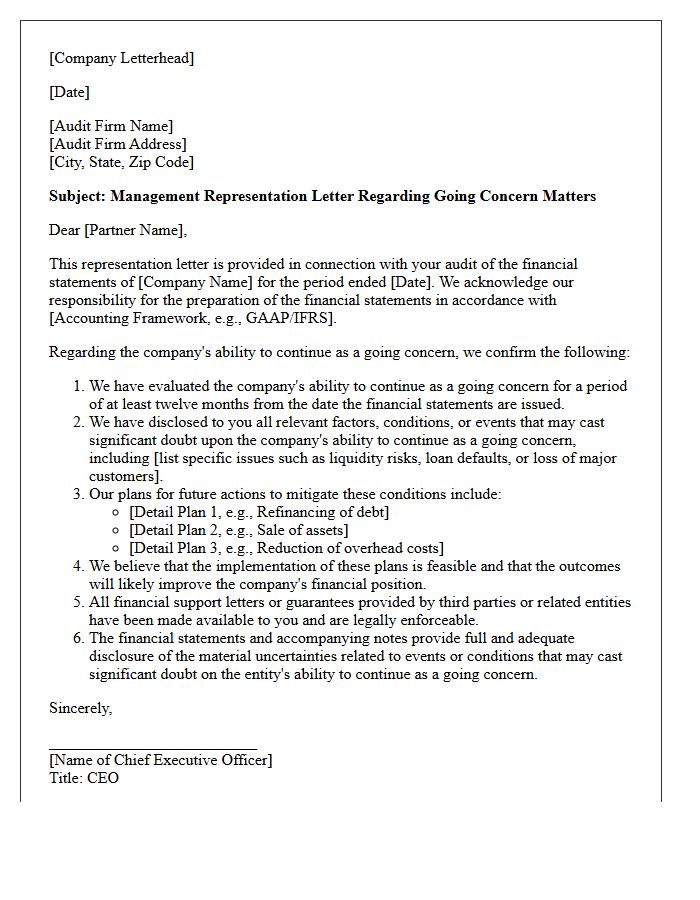

Client Representation Letter on Going Concern Matters

A Client Representation Letter on going concern matters is a formal document where management confirms their responsibility for assessing the company's ability to continue operations. It ensures that all material uncertainties and strategic plans to mitigate financial distress have been fully disclosed to auditors. This letter serves as critical audit evidence, documenting management's intentions and the completeness of data regarding liquidity risks. By signing, leadership acknowledges that no significant factors threatening the business's viability over the next twelve months have been omitted from the financial statements.

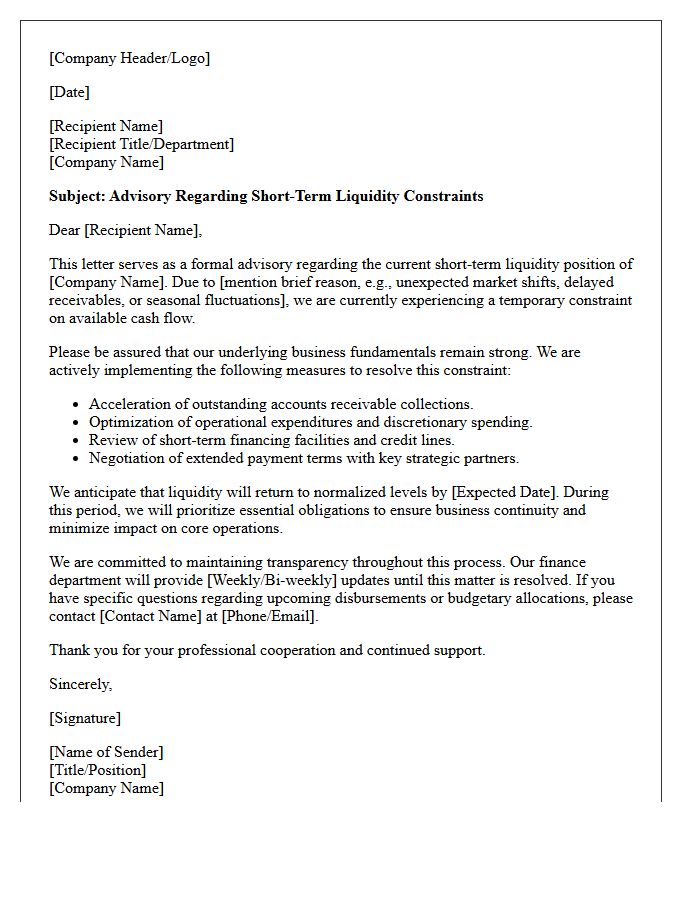

Advisory Letter on Short-Term Liquidity Constraints

An Advisory Letter on Short-Term Liquidity Constraints notifies stakeholders about immediate cash flow challenges. It serves as a formal communication tool to manage financial obligations while maintaining transparency with creditors or investors. Key elements include identifying the root cause of the deficit and outlining a strategic repayment plan to restore stability. Proactive notification helps preserve professional credibility and provides a structured framework for negotiating temporary relief or alternative financing arrangements during periods of financial volatility.

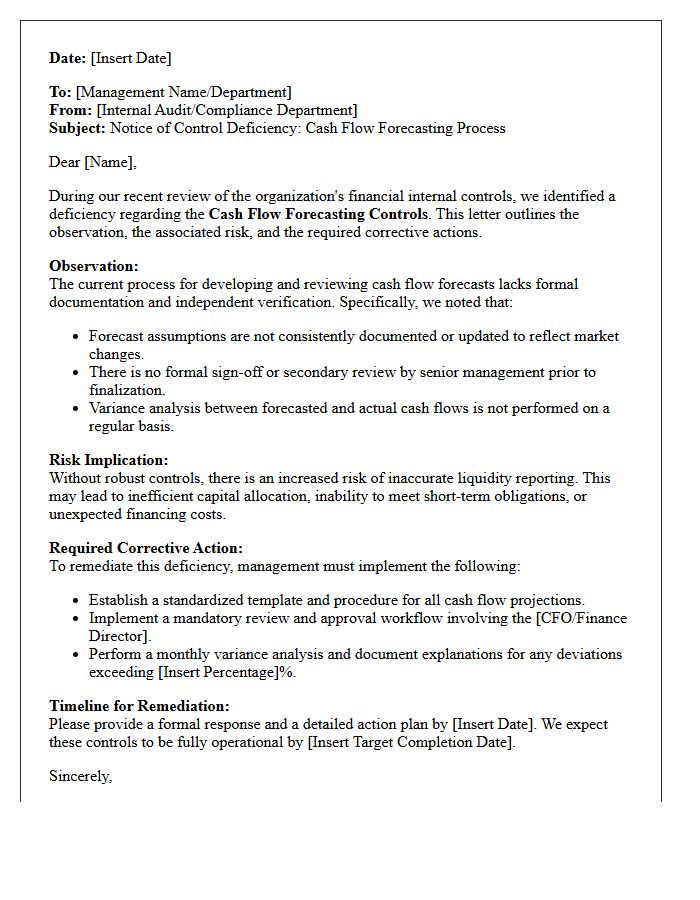

Deficiency Letter on Cash Flow Forecasting Controls

A deficiency letter regarding cash flow forecasting controls signifies that an auditor identified material weaknesses or significant deficiencies in your financial reporting processes. It highlights a lack of internal controls necessary to ensure accurate liquidity projections and risk assessment. Organizations must respond by implementing robust reconciliation procedures, enhancing data integrity, and documenting management oversight. Addressing these gaps is crucial to maintain stakeholder confidence, ensure audit compliance, and prevent potential financial misstatements that could impact the company's strategic decision-making and overall fiscal health.

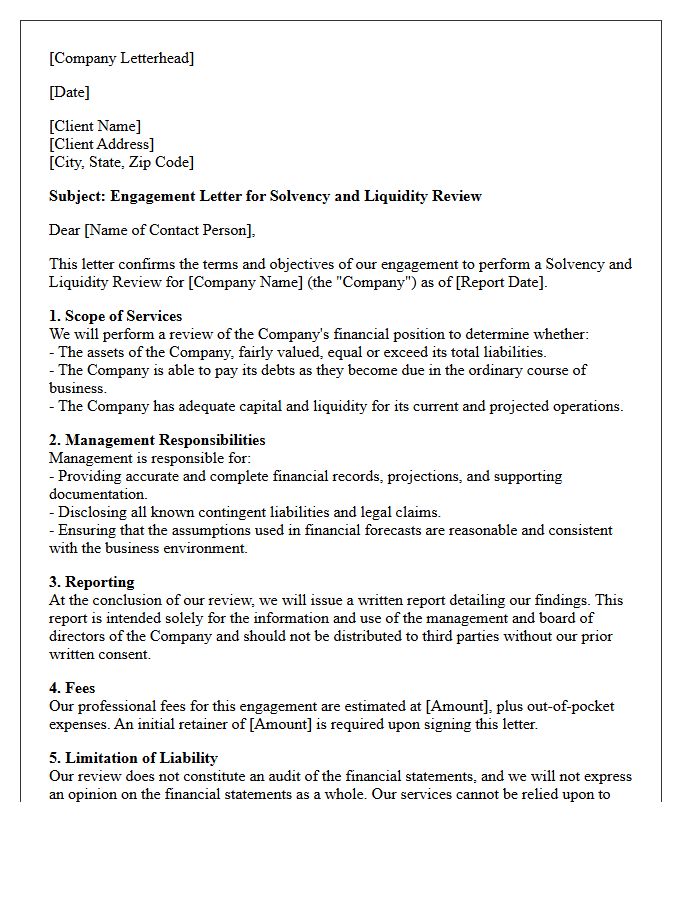

Engagement Letter for Solvency and Liquidity Review

An engagement letter for a solvency and liquidity review is a formal contract defining the scope of financial assessment. It ensures a company can meet its long-term obligations and short-term cash needs. Key elements include reporting standards, fee structures, and management responsibilities. This document protects both parties by clarifying legal liabilities and the specific financial metrics to be analyzed. It is essential for maintaining transparency during corporate restructuring, dividend declarations, or share buybacks, providing a clear framework for professional independent verification of a firm's financial health.

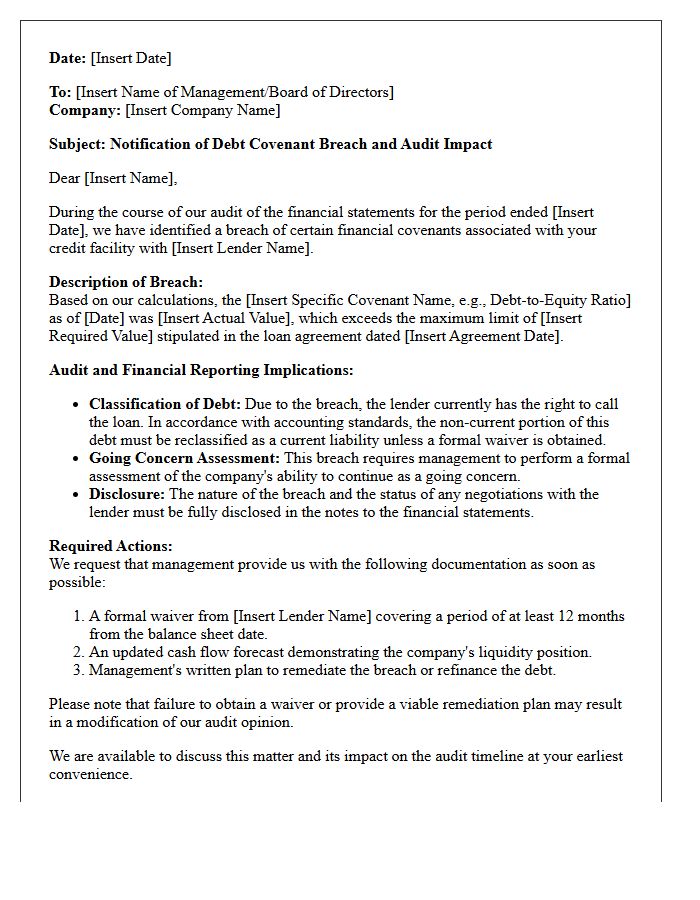

Audit Communication Letter on Debt Covenant Breaches

An Audit Communication Letter formally notifies management and those charged with governance about identified debt covenant breaches. This document is critical because violations can trigger immediate repayment demands, reclassifying long-term liabilities as current debt. Auditors use this letter to outline the financial reporting implications and the potential impact on the entity's going concern status. It ensures transparency regarding technical defaults, allowing stakeholders to evaluate remediation efforts, such as obtaining waivers or restructuring agreements, to maintain financial stability and compliance with contractual lending obligations.

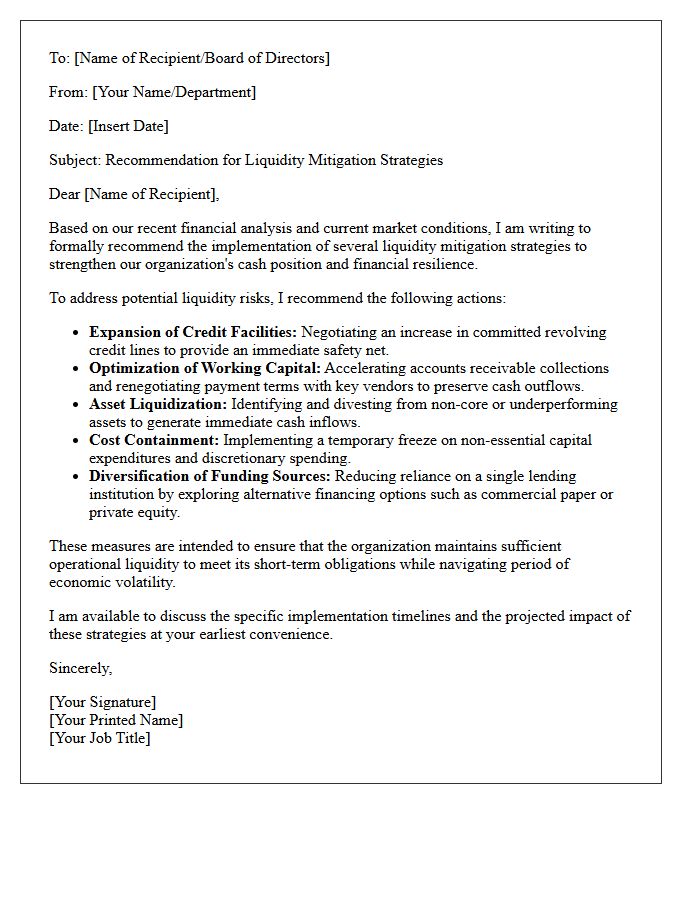

Recommendation Letter for Liquidity Mitigation Strategies

A recommendation letter for liquidity mitigation strategies outlines critical actions to preserve cash flow during financial stress. It serves as a formal advisory document, highlighting risk management protocols and tactical adjustments like credit line optimization or asset reallocation. The primary goal is to ensure institutional stability by addressing potential funding gaps before they escalate. Such letters must provide data-driven insights and proactive measures to maintain solvency and investor confidence during market volatility.

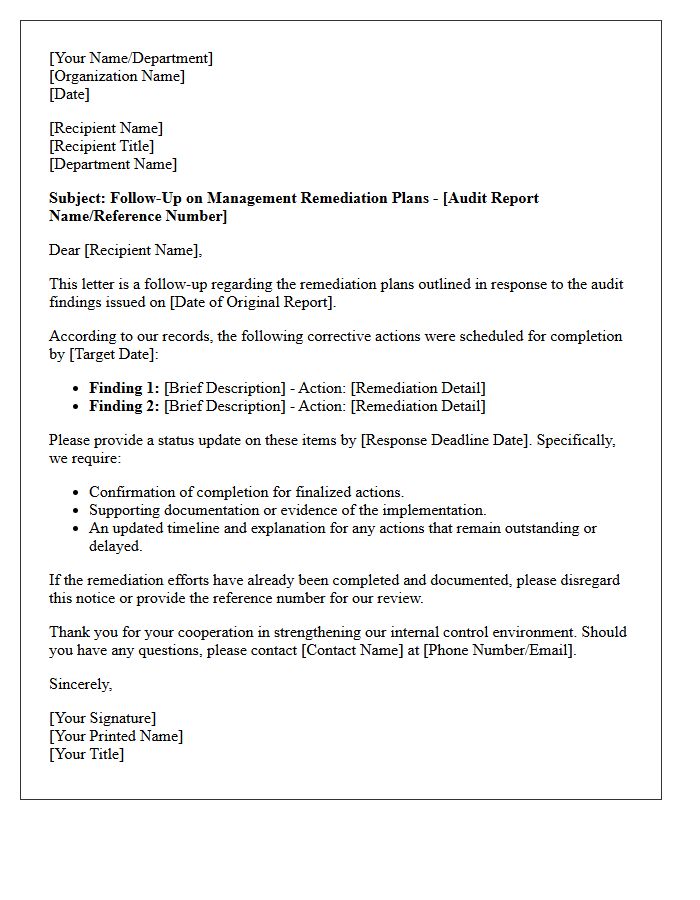

Follow-Up Letter on Management Remediation Plans

A Follow-Up Letter on Management Remediation Plans serves as a critical audit communication tool to track progress on previously identified internal control weaknesses. It ensures that management accountability is maintained by documenting the implementation status of corrective actions. This letter highlights any outstanding risks or delayed timelines, providing stakeholders with assurance that vulnerabilities are being addressed. Timely follow-up validates the effectiveness of the remediation process and strengthens the organization's overall governance framework by confirming that identified issues are successfully resolved.

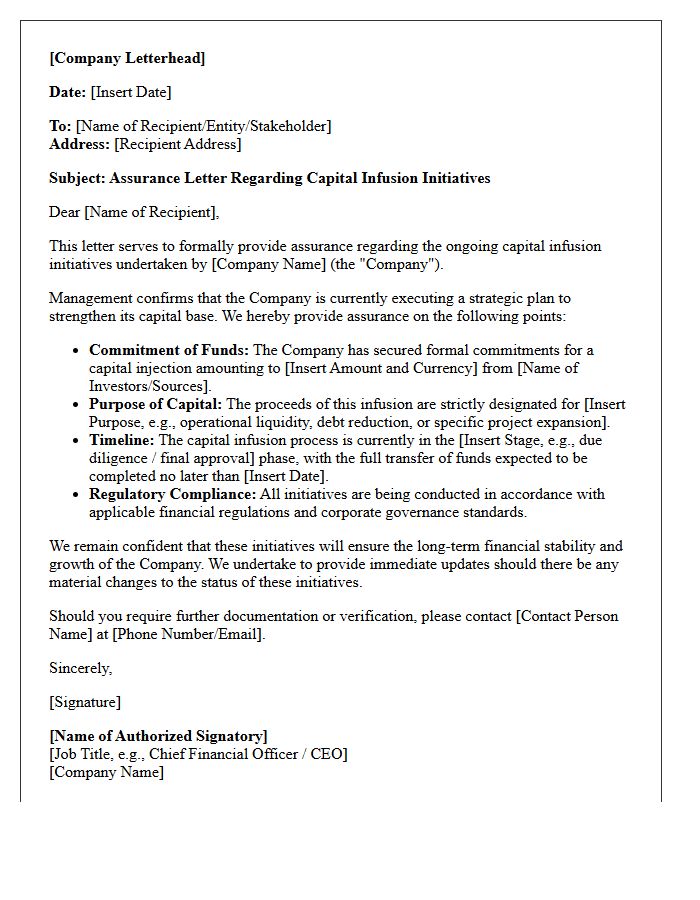

Assurance Letter on Capital Infusion Initiatives

An Assurance Letter on Capital Infusion Initiatives is a formal document where investors or parent companies pledge to inject funds into a business. This letter serves as a binding commitment to maintain liquidity and solvency during financial transitions. Regulators and financial institutions rely on these guarantees to verify that a company possesses the necessary financial backing to meet its operational obligations. Understanding the legal enforceability and specific timelines within the letter is crucial for ensuring long-term stability and building stakeholder confidence during critical restructuring or growth phases.

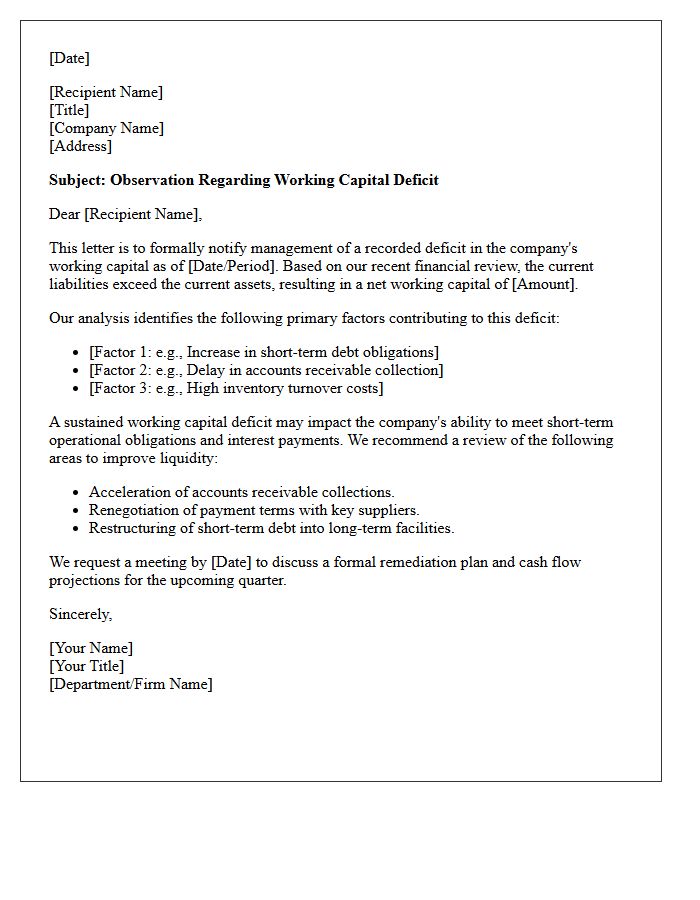

Observation Letter Regarding Working Capital Deficits

An Observation Letter is a formal notice issued by auditors or regulators when a company's current liabilities exceed its current assets. This document serves as a critical warning regarding liquidity risk and the entity's ability to meet short-term obligations. Addressing a working capital deficit is essential to maintain going concern status and operational stability. Stakeholders use this letter to evaluate financial health, necessitating immediate remediation plans, such as debt restructuring or asset liquidation, to restore solvency and ensure long-term business continuity.

Concluding Letter on Going Concern Viability

A Concluding Letter on Going Concern Viability is a critical audit document assessing an entity's ability to continue operations for the foreseeable future. It provides reasonable assurance that no material uncertainties exist regarding financial solvency over the next twelve months. Auditors evaluate cash flows, debt obligations, and management plans before issuing this final evaluation. If significant doubt arises, it must be disclosed to prevent audit failure and inform stakeholders. This letter serves as the definitive summary of an organization's operational endurance and long-term financial stability.

What is the primary purpose of a Management Letter regarding going concern assessment?

The Management Letter serves to document the board's evaluation of the entity's ability to continue operations for at least twelve months from the reporting date. It outlines the specific internal and external factors considered, the underlying assumptions used in financial forecasting, and the formal conclusion regarding the company's status as a going concern.

How should a company document its assessment of liquidity risk in financial reporting?

Liquidity risk documentation should include a detailed analysis of projected cash inflows and outflows, available credit facilities, and the maturity profile of existing financial liabilities. It must demonstrate that the entity maintains sufficient liquid assets or access to funding to meet its obligations as they fall due under both normal and stressed conditions.

What specific mitigation strategies address material uncertainty related to going concern?

Common mitigation strategies include securing new equity financing, restructuring existing debt obligations, liquidating non-core assets, or implementing significant cost-reduction programs. The Management Letter must detail these plans, assess their feasibility, and explain how they will effectively eliminate or reduce the identified risk to an acceptable level.

How does management justify the "reasonable expectation" of continued operations during periods of economic volatility?

Management justifies this expectation by providing stress-tested cash flow forecasts that account for varying market scenarios. This includes sensitivity analysis on key variables such as revenue growth, interest rates, and currency fluctuations, ensuring that the liquidity cushion remains adequate even if primary financial assumptions are not fully met.

What disclosures are required if a significant liquidity risk is identified but the going concern basis remains appropriate?

If a significant risk is present, management must disclose the nature of the uncertainty, the specific events or conditions that may cast doubt on the entity's ability to continue, and the comprehensive plans to mitigate these risks. These disclosures ensure transparency for stakeholders regarding the financial resilience and the strategic interventions planned by the board.

Comments