This management letter provides a comprehensive overview of revenue recognition policies aligned with ASC 606 standards. It outlines essential internal controls, Five-Step Model compliance, and documentation requirements to ensure financial reporting accuracy and audit readiness. Strengthening these accounting frameworks mitigates risk and enhances transparency for stakeholders. To assist your implementation, below are some ready to use template.

Image cover: Mastering ASC 606: Professional Revenue Recognition Management Letter Templates and Best Practices

Letter Samples List

- Management Letter on ASC 606 Revenue Recognition Implementation

- Advisory Letter Concerning ASC 606 Contract Modification Controls

- Audit Findings Letter Regarding Variable Consideration in Revenue Recognition

- Management Letter on Identifying Performance Obligations Under ASC 606

- Internal Control Deficiency Letter for ASC 606 Revenue Policies

- Executive Summary Letter of ASC 606 Revenue Recognition Transition

- Management Recommendation Letter on Standalone Selling Price Allocation

- Compliance Assessment Letter for ASC 606 Revenue Recognition Disclosures

- Client Advisory Letter on Principal Versus Agent Revenue Recognition

- Audit Completion Letter Highlighting ASC 606 Policy Adjustments

- Management Letter Addressing Software Revenue Recognition Under ASC 606

- Post-Audit Review Letter for ASC 606 Capitalized Contract Costs

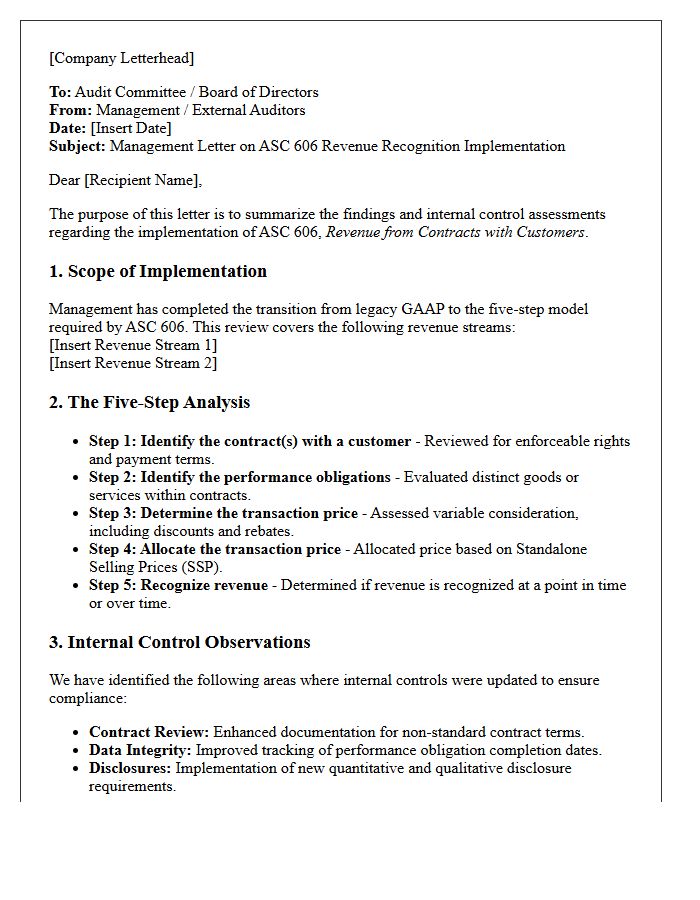

Management Letter on ASC 606 Revenue Recognition Implementation

A management letter regarding ASC 606 implementation evaluates an entity's transition to the five-step revenue recognition model. It highlights internal control weaknesses, identifies gaps in contract review processes, and assesses the accuracy of performance obligation identification. Auditors use this document to communicate material weaknesses or significant deficiencies found during the adoption phase. Understanding these findings is essential for ensuring financial reporting integrity, improving disclosure transparency, and maintaining compliance with complex accounting standards governing revenue from contracts with customers.

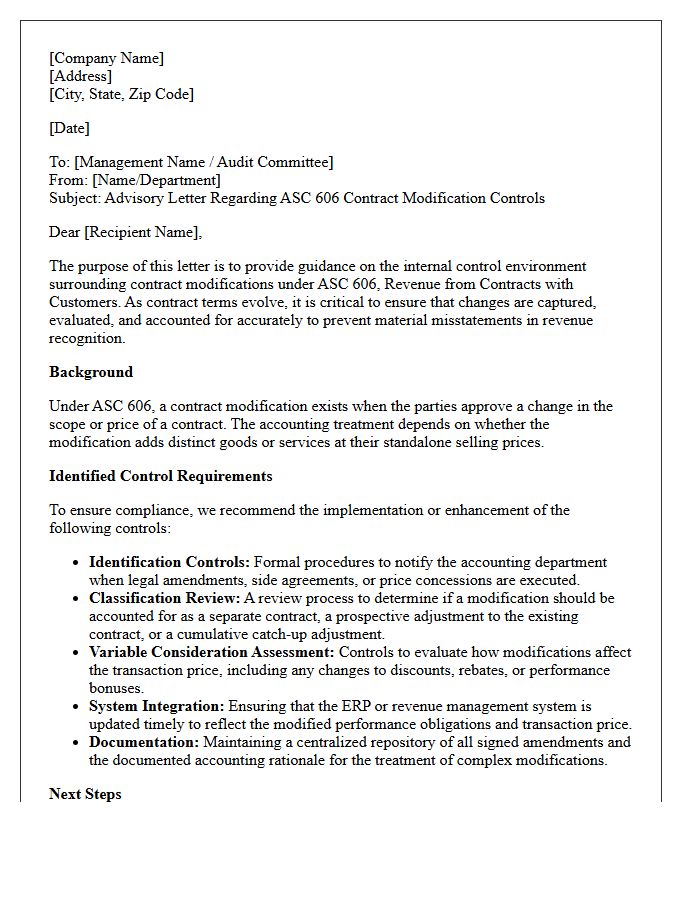

Advisory Letter Concerning ASC 606 Contract Modification Controls

The Advisory Letter highlights critical internal control deficiencies regarding ASC 606 revenue recognition. It emphasizes that companies must implement rigorous monitoring controls to identify and evaluate contract modifications accurately. Failure to distinguish between separate contracts and modifications can lead to material financial misstatements. Auditors focus on the enforceability of rights and the timing of revenue capture. Organizations should strengthen their documentation processes and cross-departmental communication to ensure all structural changes to customer agreements align with GAAP standards and maintain financial reporting integrity.

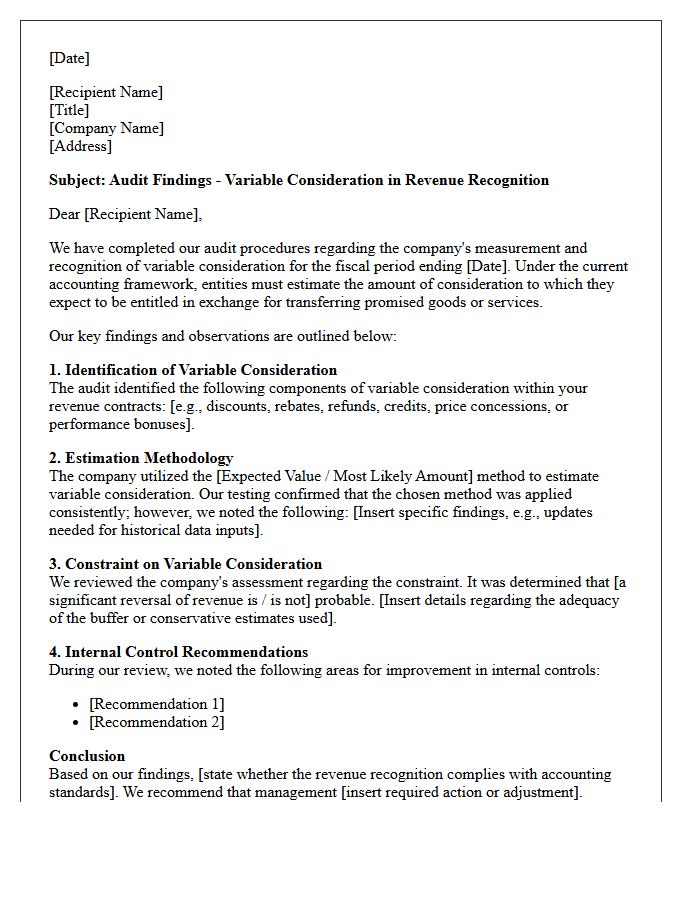

Audit Findings Letter Regarding Variable Consideration in Revenue Recognition

An audit findings letter regarding variable consideration evaluates how a company estimates future income from discounts, rebates, or performance bonuses. Auditors scrutinize management's estimation methodology to ensure revenue is only recognized when it is highly probable that a significant reversal will not occur. Key issues often include the use of expected value or most likely amount methods under ASC 606. Accurate data validation is essential to justify these projections, as material misstatements in variable components directly impact the reliability of reported earnings and financial transparency.

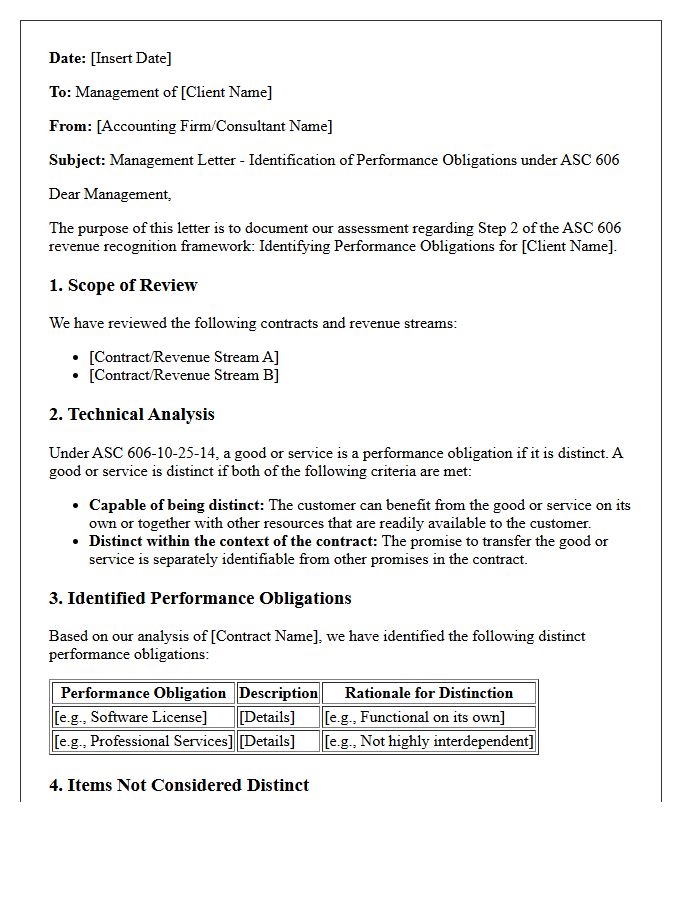

Management Letter on Identifying Performance Obligations Under ASC 606

A management letter regarding ASC 606 must accurately document the process of identifying performance obligations within a contract. It is critical to evaluate whether promised goods or services are distinct, meaning the customer can benefit from them individually. Failure to correctly separate or combine these obligations can lead to significant revenue recognition errors. This formal assessment ensures compliance by confirming that the transaction price is allocated appropriately across all contractual promises, reflecting the true economic substance of the agreement and maintaining financial reporting integrity for auditors and stakeholders.

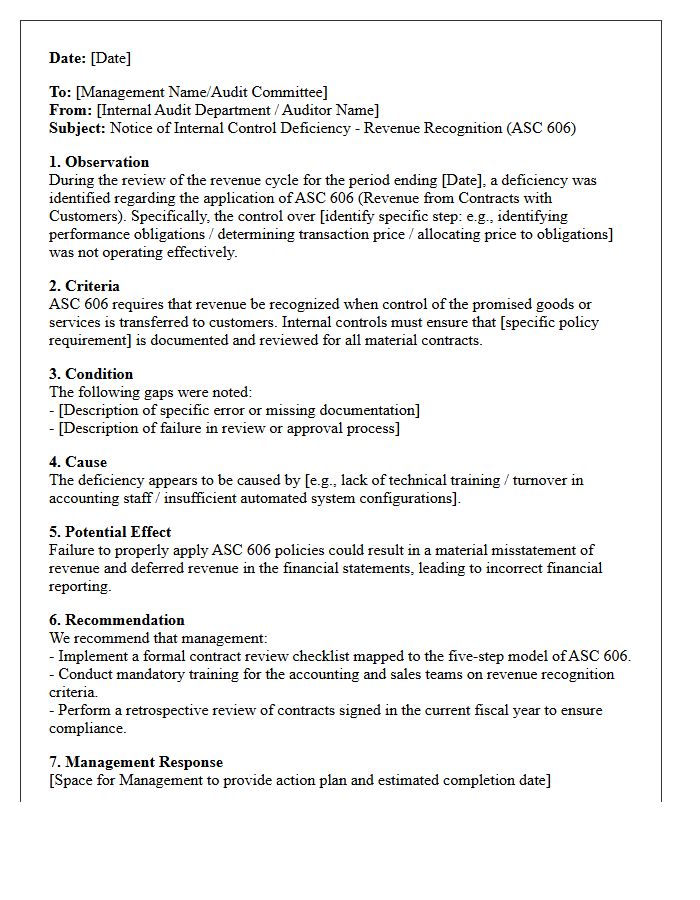

Internal Control Deficiency Letter for ASC 606 Revenue Policies

An Internal Control Deficiency Letter identifies weaknesses in financial reporting processes, specifically regarding ASC 606 revenue recognition standards. This document highlights failures in monitoring performance obligations, variable consideration, or contract modifications. For auditors, these findings signal a risk of material misstatement in revenue figures. Management must address these gaps by enhancing documentation and oversight to ensure compliance. Resolving these deficiencies is critical for maintaining investor trust and ensuring that financial statements accurately reflect the timing and measurement of earned revenue in accordance with modern accounting frameworks.

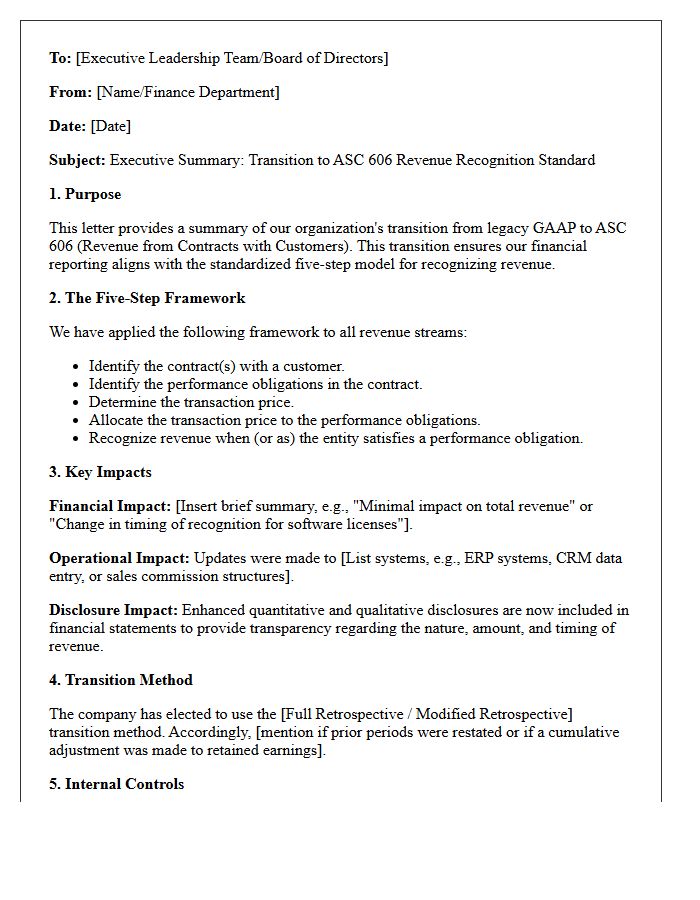

Executive Summary Letter of ASC 606 Revenue Recognition Transition

An executive summary letter for the ASC 606 revenue recognition transition provides stakeholders with a high-level overview of financial reporting changes. It highlights the shift from industry-specific guidance to a standardized five-step framework. Key disclosures include the cumulative effect adjustment on retained earnings and the chosen transition method, such as full or modified retrospective. This document ensures transparency regarding how the new timing and measurement of revenue impact the balance sheet, helping investors understand the transition's effect on historical comparability and future earnings predictability.

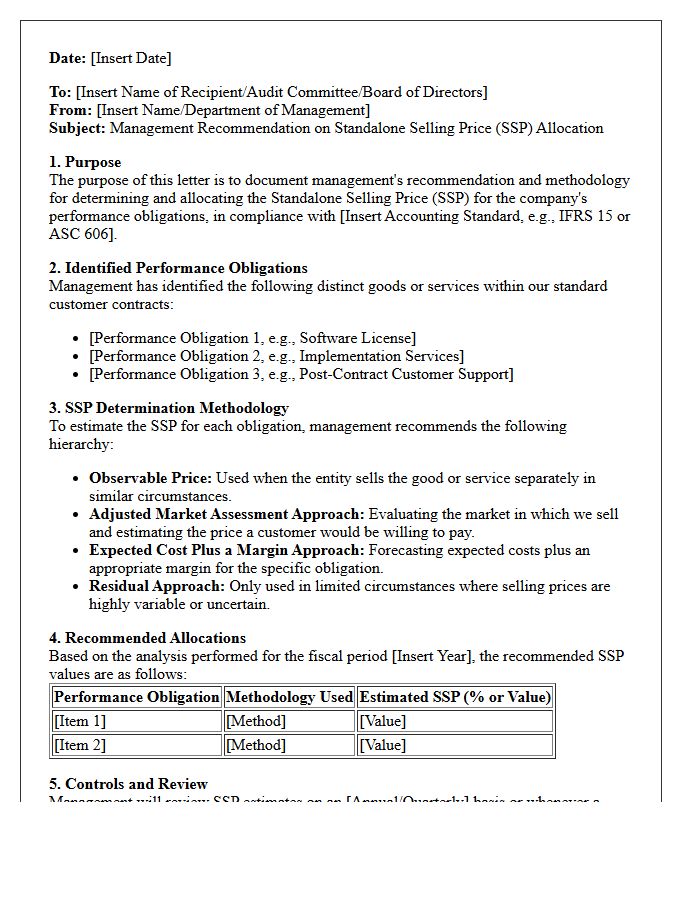

Management Recommendation Letter on Standalone Selling Price Allocation

A management recommendation letter on Standalone Selling Price (SSP) allocation is crucial for compliance with IFRS 15 or ASC 606 revenue recognition standards. It outlines the formal methodology used to determine the individual value of distinct goods or services within a multi-element contract. This document justifies estimation methods, such as adjusted market assessment or expected cost plus margin, ensuring that revenue is accurately distributed. Management must validate these assumptions to provide auditors with a transparent audit trail, mitigating risks of financial misstatement and ensuring consistent reporting across all business transactions.

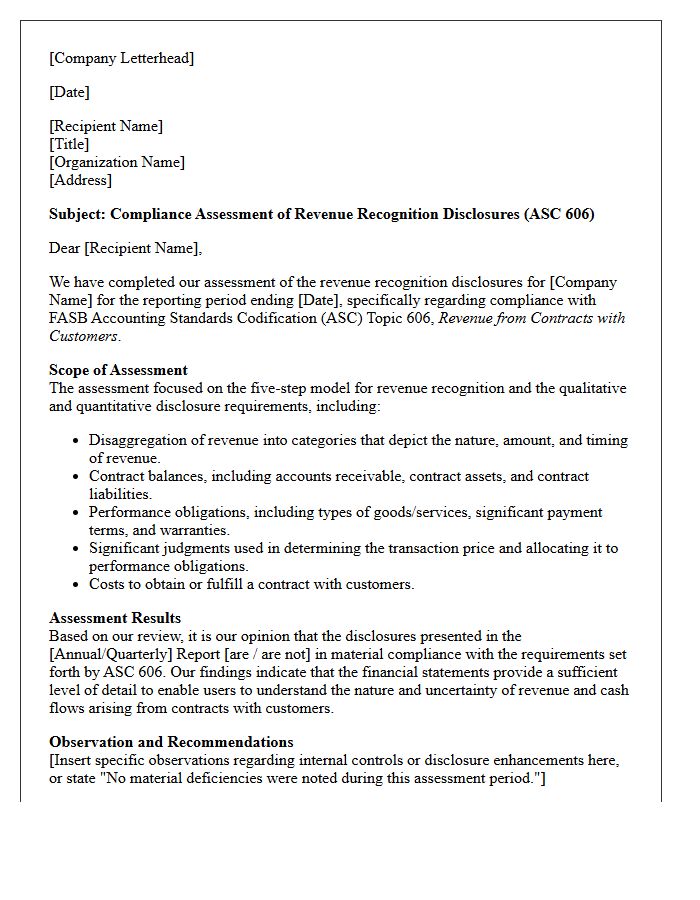

Compliance Assessment Letter for ASC 606 Revenue Recognition Disclosures

A Compliance Assessment Letter evaluates how accurately a company adheres to ASC 606 standards. It focuses on the five-step model for revenue recognition, ensuring contract terms and performance obligations are correctly reported. This document provides stakeholders with assurance that financial statements are transparent and free from material misstatements. Key areas analyzed include variable consideration, transaction price allocation, and specific disclosure requirements. Obtaining this assessment helps mitigate audit risks, improves financial integrity, and ensures regulatory alignment for businesses reporting under GAAP.

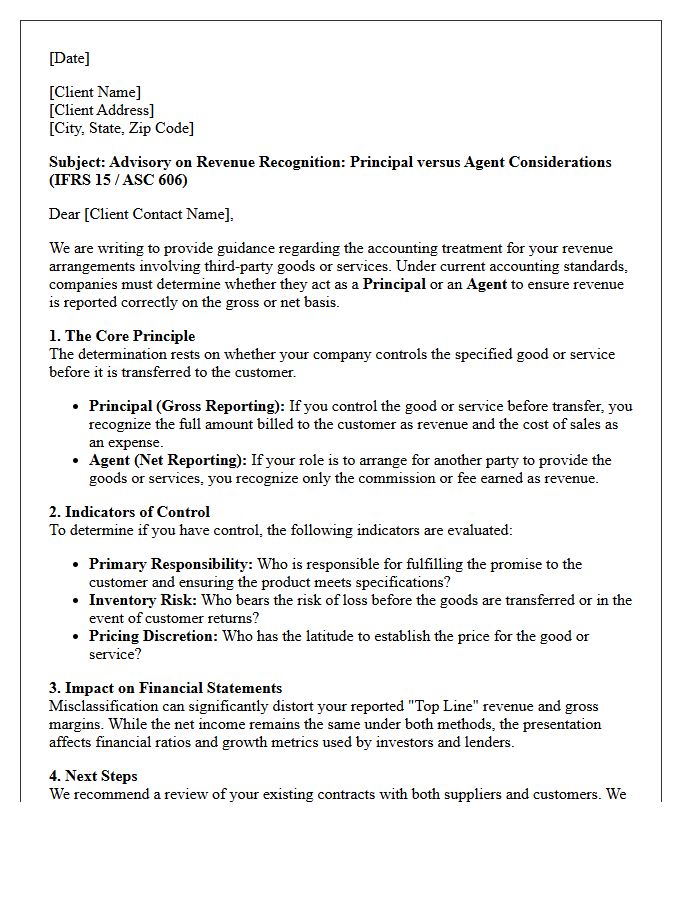

Client Advisory Letter on Principal Versus Agent Revenue Recognition

A client advisory letter clarifies the Principal versus Agent revenue recognition standards under ASC 606 or IFRS 15. The primary distinction depends on whether a company controls a specified good or service before it is transferred to the customer. Principals record gross revenue for the full amount billed, while agents record net revenue as a commission fee. Misclassification can significantly distort financial statements. Companies must evaluate key indicators like primary responsibility for fulfillment, inventory risk, and discretion in establishing prices to ensure accurate regulatory compliance and reporting.

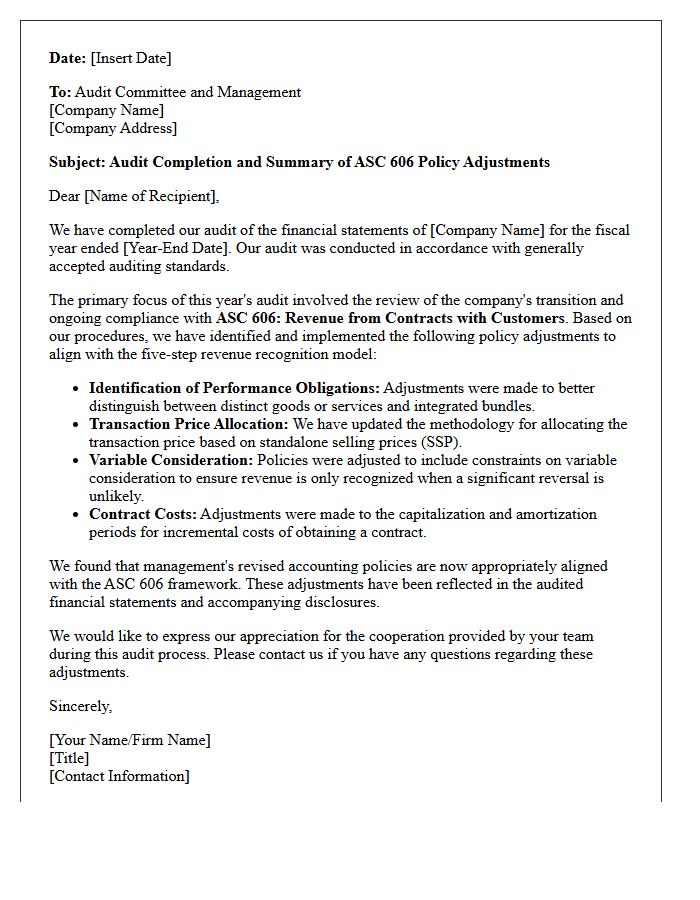

Audit Completion Letter Highlighting ASC 606 Policy Adjustments

An audit completion letter serves as formal confirmation that the examination of financial statements is finalized. A critical component involves disclosing significant changes resulting from ASC 606 revenue recognition standards. This letter highlights how policy adjustments impact the timing and measurement of contracts, ensuring compliance with FASB requirements. It outlines any identified material weaknesses or adjustments made during the transition. For stakeholders, understanding these updates is vital for assessing the company's ongoing financial health and the transparency of its reported earnings following rigorous professional scrutiny.

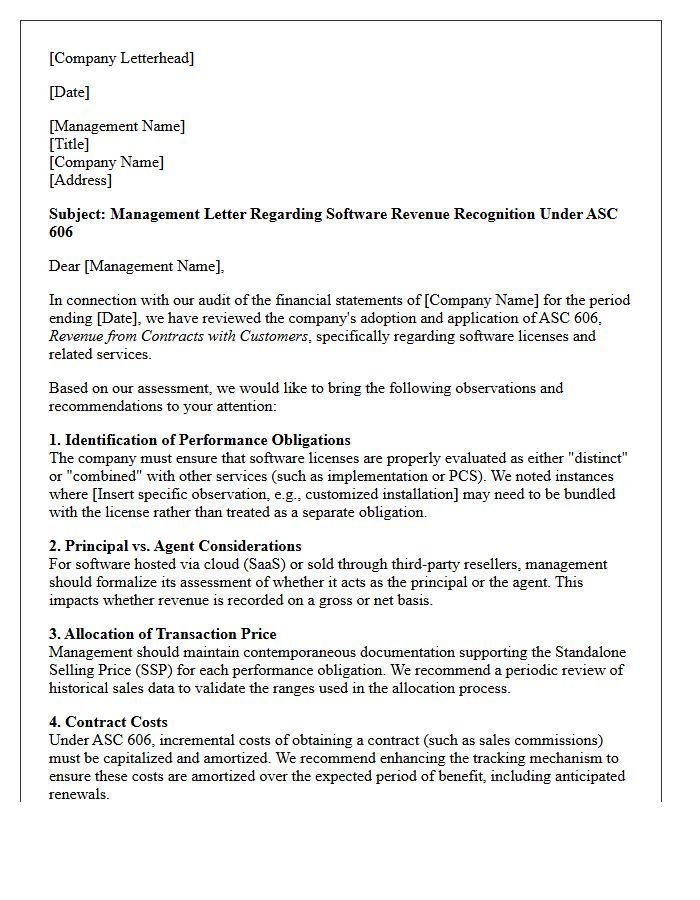

Management Letter Addressing Software Revenue Recognition Under ASC 606

A management letter concerning software revenue recognition ensures compliance with ASC 606 standards. It must detail the five-step framework, specifically focusing on identifying performance obligations and determining the transaction price. Key disclosures should address distinct licenses versus integrated services to ensure accurate timing of revenue. Auditors use this document to validate internal controls and verify that contract milestones align with financial reporting. Clear documentation of estimates and judgments is essential to mitigate audit risks and ensure transparency for stakeholders regarding the company's recurring revenue streams and long-term profitability.

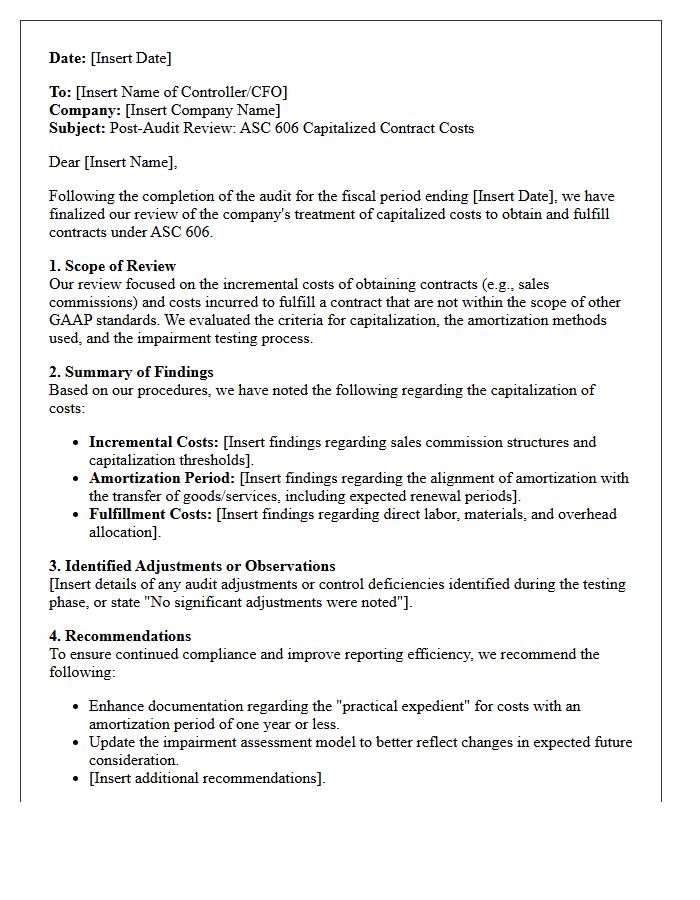

Post-Audit Review Letter for ASC 606 Capitalized Contract Costs

A Post-Audit Review Letter for ASC 606 serves as a formal evaluation of how an organization identifies and amortizes Capitalized Contract Costs. This document highlights incremental costs, such as sales commissions, that must be recognized over the expected customer life rather than expensed immediately. It ensures internal controls align with revenue recognition standards, addressing potential discrepancies found during the auditing process. Understanding these adjustments is essential for maintaining accurate financial reporting and ensuring long-term compliance with GAAP requirements regarding contract acquisition and fulfillment assets.

What is the primary purpose of a Management Letter regarding ASC 606 revenue recognition?

The Management Letter serves as a formal communication from auditors to management, identifying internal control weaknesses, policy gaps, and operational inefficiencies related to the five-step revenue recognition model under ASC 606.

How does ASC 606 impact the internal control environment for revenue?

ASC 606 requires robust internal controls around contract identification, the determination of distinct performance obligations, and the estimation of variable consideration to ensure revenue is recognized as control is transferred to the customer.

What are the common audit findings regarding revenue recognition policy documentation?

Auditors frequently find that management letters highlight a lack of detailed documentation regarding significant judgments, such as the stand-alone selling price (SSP) allocations and the timing of satisfaction for performance obligations over time versus at a point in time.

Why is the disclosure of variable consideration critical in a Management Letter?

Variable consideration, including rebates, discounts, and performance bonuses, must be estimated using either the "expected value" or "most likely amount" method; failures to apply the constraint on these estimates are common points of concern in management letter comments.

What improvements are typically recommended for ASC 606 compliance?

Recommendations often include enhancing the contract review process, automating the allocation of transaction prices across multiple-element arrangements, and improving the precision of disclosures related to contract assets and liabilities.

Comments