Weak internal controls in payroll systems often lead to financial inaccuracies and compliance risks. This article explores critical Management Letter on Payroll Processing and Timekeeping Vulnerabilities, identifying gaps in attendance tracking and authorization workflows. Learn how to strengthen oversight, prevent overpayments, and ensure regulatory adherence through rigorous audit procedures. Below are some ready to use template options to streamline your reporting.

Image cover: Strengthening Payroll Controls: Management Letter Templates and Advisory Samples

Letter Samples List

- Management Letter on General Payroll Processing and Timekeeping Vulnerabilities

- Management Letter Regarding Ghost Employee Risks in Payroll Processing

- Management Letter Addressing Unauthorized Overtime and Timekeeping Controls

- Management Letter on Segregation of Duties in Payroll Administration

- Management Letter Identifying Manual Timesheet Manipulation Vulnerabilities

- Management Letter on Information Technology Access Controls Within Payroll Systems

- Management Letter Concerning Buddy Punching and Automated Timekeeping Vulnerabilities

- Management Letter on Worker Misclassification and Associated Payroll Risks

- Management Letter Highlighting Payroll Tax Withholding and Reporting Vulnerabilities

- Management Letter on Insufficient Supervisor Approval in Timekeeping Procedures

- Management Letter Regarding the Timely Removal of Terminated Employees From Payroll

- Management Letter Identifying Paid Time Off Accrual and Processing Vulnerabilities

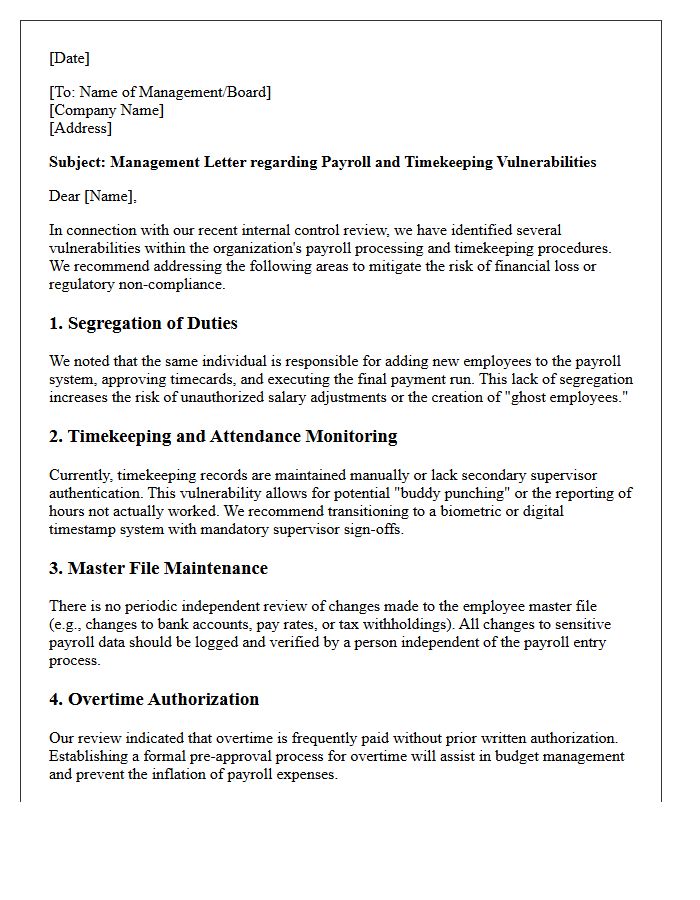

Management Letter on General Payroll Processing and Timekeeping Vulnerabilities

A Management Letter identifies critical internal control weaknesses within payroll processing and timekeeping systems. These vulnerabilities often include inadequate segregation of duties, lack of formal overtime authorization, and manual data entry risks. Such gaps increase the likelihood of financial inaccuracies, fraud, or non-compliance with labor laws. Addressing these findings is essential to ensure regulatory adherence and operational integrity. Organizations must implement automated tracking and robust oversight to mitigate financial leakage and protect organizational assets from exploitation.

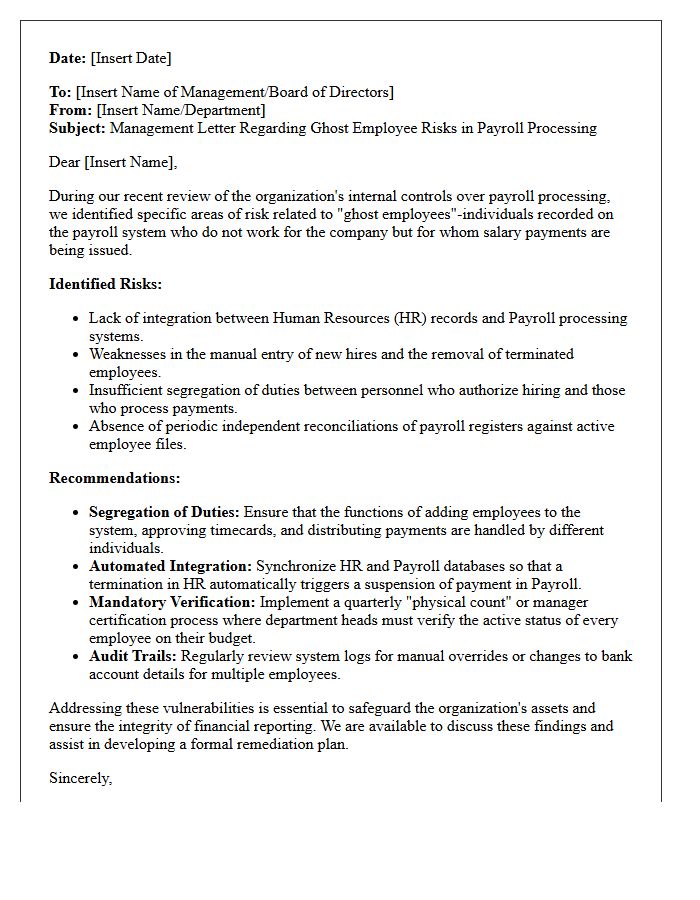

Management Letter Regarding Ghost Employee Risks in Payroll Processing

A management letter addressing ghost employee risks is vital for maintaining payroll integrity. It identifies vulnerabilities where non-existent workers receive unauthorized payments due to weak internal controls. Key recommendations typically focus on strengthening segregation of duties between HR and finance, implementing mandatory physical verification of staff, and performing regular data matching between payroll records and employee files. Proactive monitoring through independent audits ensures that organizations detect fraudulent entries early, safeguarding financial resources and ensuring compliance with internal governance standards during the payroll cycle.

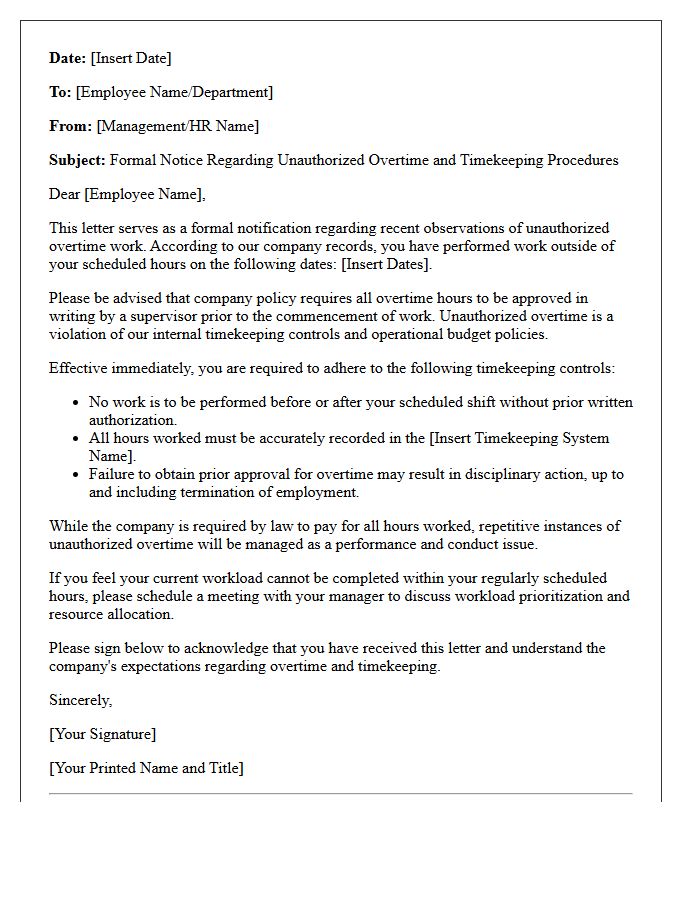

Management Letter Addressing Unauthorized Overtime and Timekeeping Controls

A management letter addressing unauthorized overtime highlights critical weaknesses in internal timekeeping controls. It identifies instances where employees exceed scheduled hours without prior approval, increasing operational costs and legal risks. To mitigate these issues, management must enforce strict authorization protocols and improve the accuracy of attendance monitoring systems. Clear policies and regular supervisory reviews ensure labor law compliance and budget stability. Addressing these deficiencies promptly prevents fraudulent reporting and ensures that organizational resources are allocated efficiently while maintaining transparent audit trails for all compensated hours.

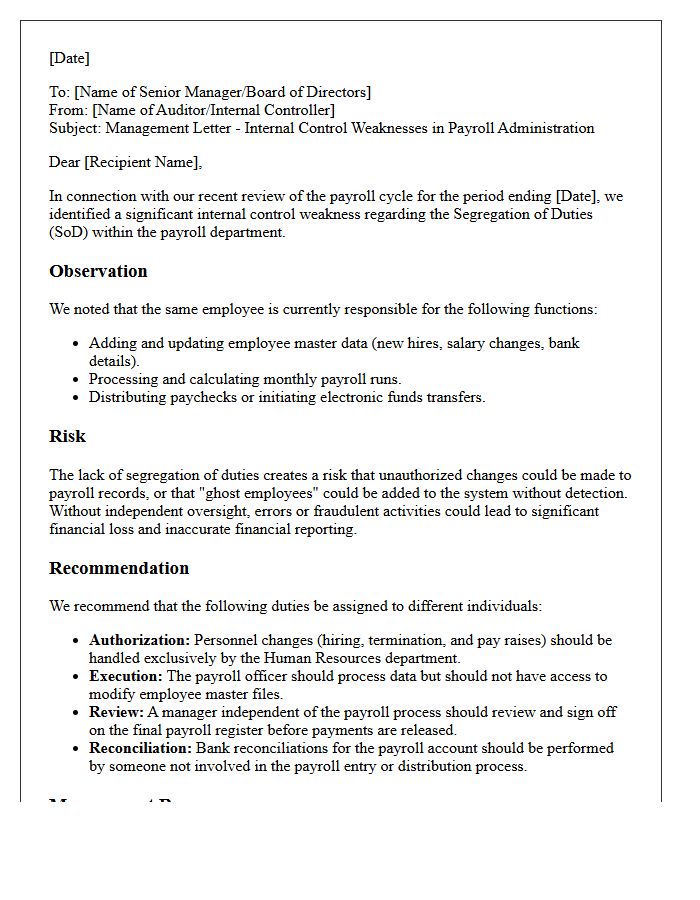

Management Letter on Segregation of Duties in Payroll Administration

A management letter regarding segregation of duties in payroll administration highlights critical internal controls designed to prevent fraud and errors. It emphasizes that no single employee should manage the entire payroll lifecycle, such as adding employees, approving hours, and processing payments. Dividing these responsibilities ensures accountability and reduces the risk of unauthorized salary adjustments or ghost employees. Implementing these oversight procedures strengthens financial integrity and protects organizational assets from potential misappropriation during the disbursement process.

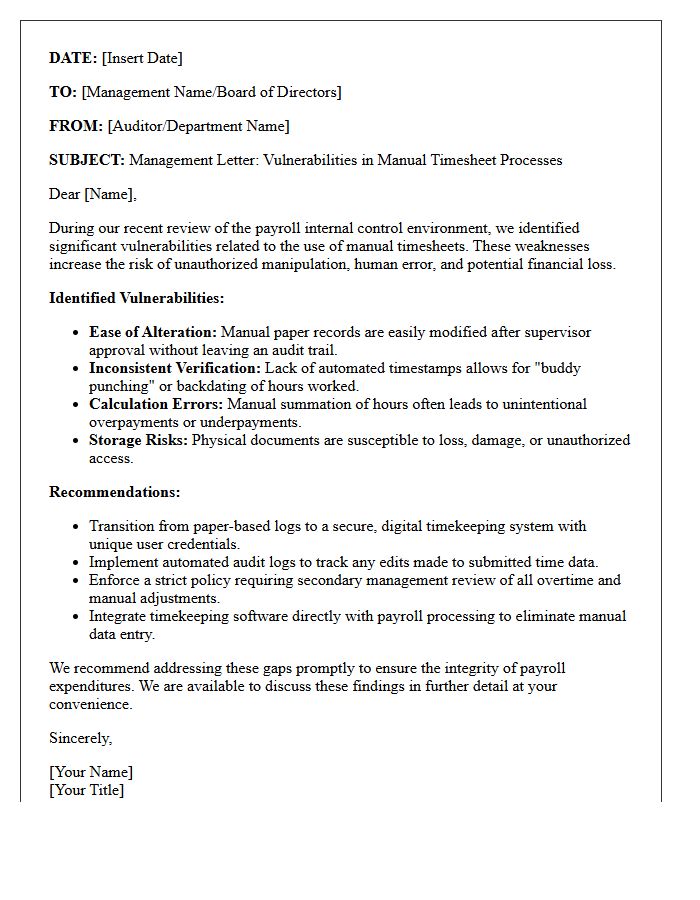

Management Letter Identifying Manual Timesheet Manipulation Vulnerabilities

A management letter highlights critical internal control deficiencies, specifically addressing manual timesheet manipulation risks. These vulnerabilities occur when employees or supervisors bypass time-tracking protocols to alter hours worked. Such weaknesses often stem from a lack of automated validation and insufficient segregation of duties. Implementing robust audit trails and digital authentication is essential to prevent payroll fraud and ensure regulatory compliance. Addressing these findings promptly strengthens financial integrity and mitigates the risk of unauthorized labor cost increases within the organization.

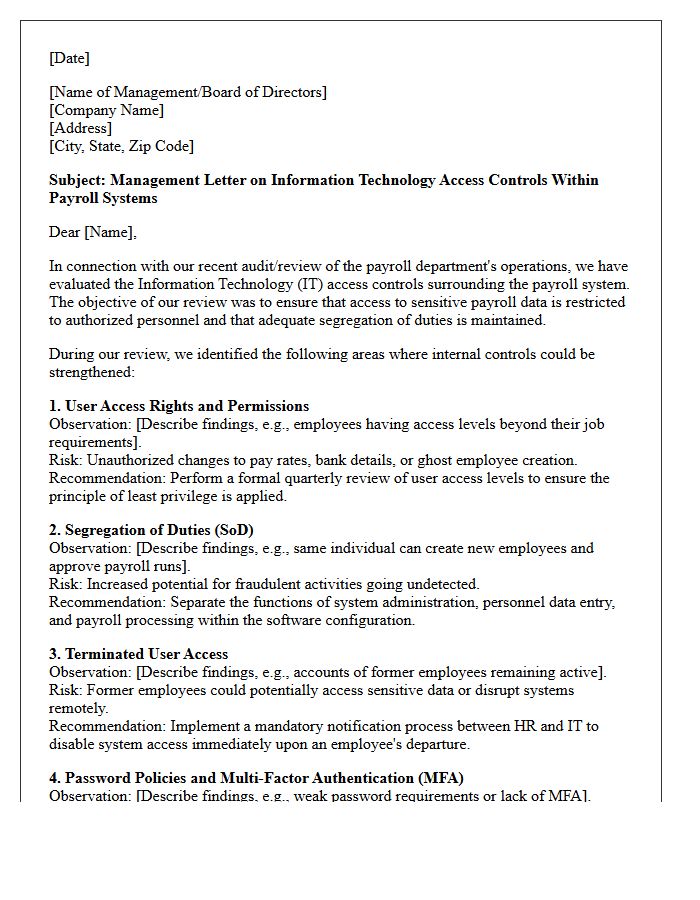

Management Letter on Information Technology Access Controls Within Payroll Systems

A management letter regarding IT access controls in payroll systems highlights critical security gaps. It evaluates how organizations manage user permissions and restrict sensitive data entry to authorized personnel only. Ensuring a strong segregation of duties prevents unauthorized salary adjustments and data breaches. Effective identity management and regular audit trails are essential to mitigate internal fraud risks. Strengthening these controls protects financial integrity and ensures compliance with regulatory standards, making it a vital document for organizational oversight and long-term risk management.

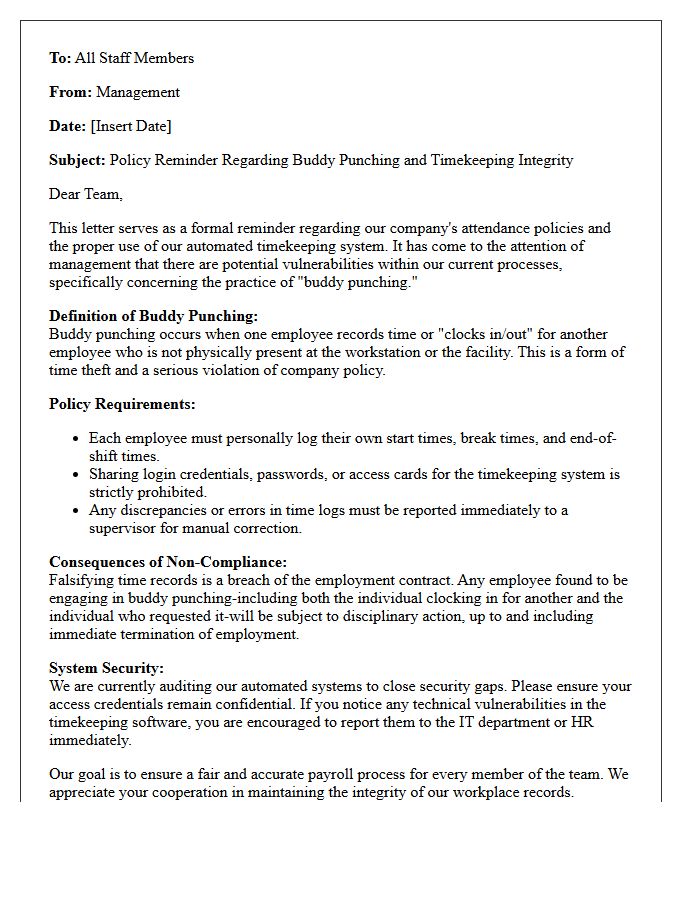

Management Letter Concerning Buddy Punching and Automated Timekeeping Vulnerabilities

Addressing buddy punching is critical for payroll integrity. This management letter highlights how manual entry and weak authentication create financial leakage. Implementing automated timekeeping systems with biometric verification or geofencing mitigates these vulnerabilities. By upgrading to automated systems, your organization ensures accurate labor tracking, reduces administrative errors, and maintains strict compliance with labor laws. Eliminating fraudulent clock-ins protects the bottom line and fosters a culture of accountability among staff.

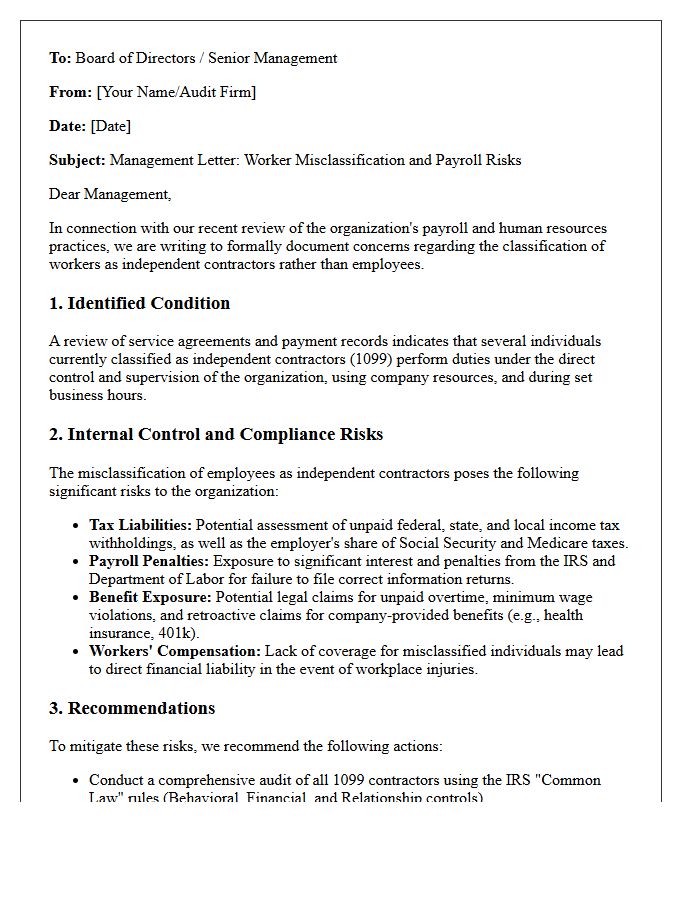

Management Letter on Worker Misclassification and Associated Payroll Risks

A management letter regarding worker misclassification serves as a critical warning about the legal and financial liabilities of treating employees as independent contractors. Incorrect categorization triggers significant payroll tax risks, including unpaid back taxes, interest, and substantial penalties from tax authorities. Organizations must conduct regular audits to ensure compliance with labor laws and reporting requirements. Proactively addressing these discrepancies protects the company's reputation and prevents costly litigation or regulatory enforcement actions. Understanding the distinction between contractors and staff is essential for maintaining operational integrity and fiscal health.

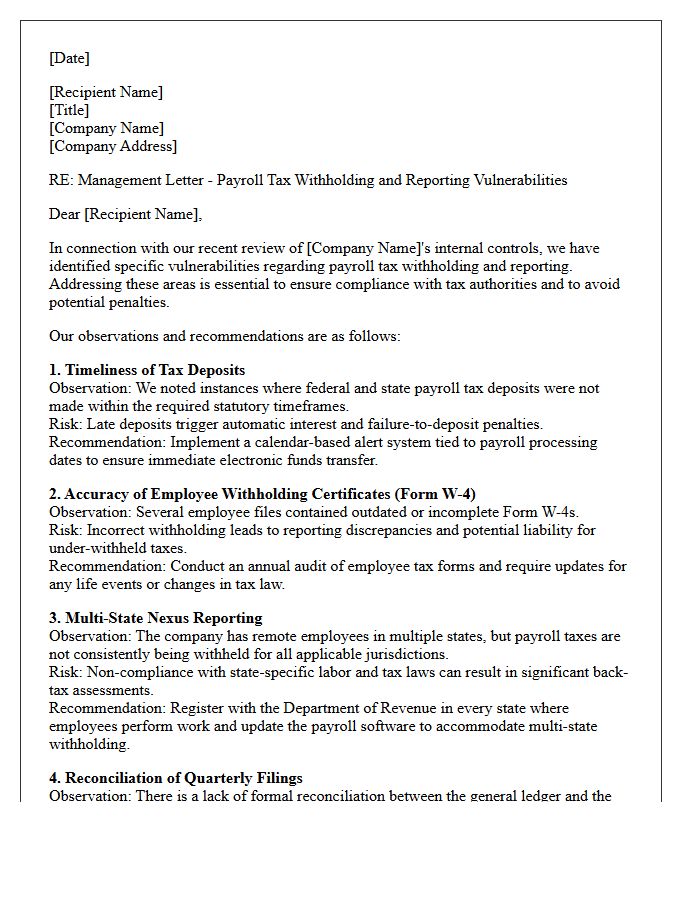

Management Letter Highlighting Payroll Tax Withholding and Reporting Vulnerabilities

A management letter identifies critical gaps in your payroll tax compliance framework. It highlights vulnerabilities such as incorrect withholding calculations, missed filing deadlines, and poor record-keeping practices. Failure to address these internal control weaknesses can lead to substantial IRS penalties and legal liabilities. Organizations must prioritize reporting accuracy and timely tax deposits to mitigate financial risks. Implementing robust oversight ensures all employee earnings and statutory deductions are documented correctly, protecting the entity from audit findings and ensuring full adherence to federal and state tax regulations.

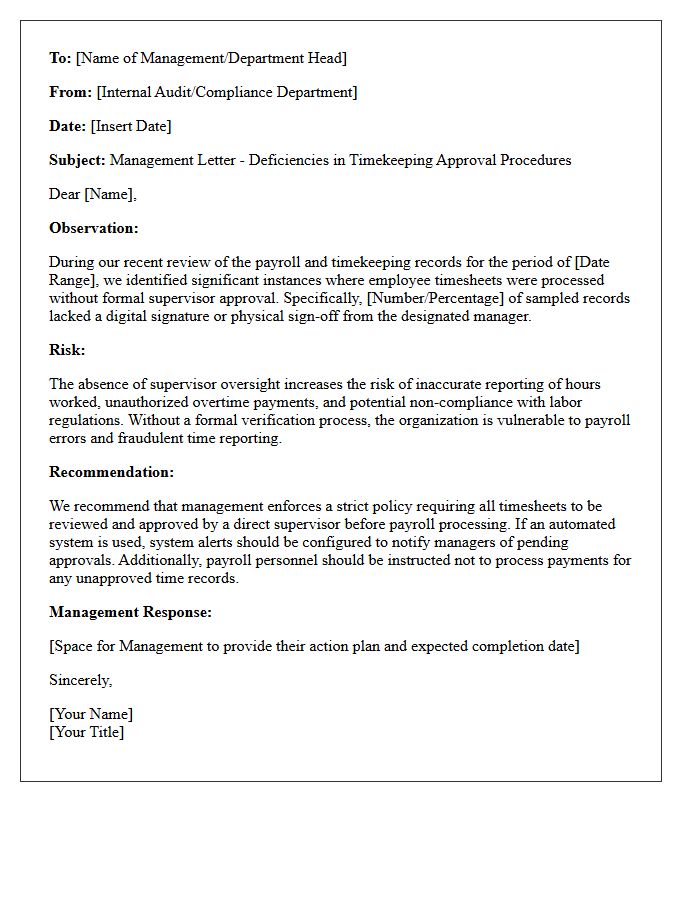

Management Letter on Insufficient Supervisor Approval in Timekeeping Procedures

A management letter addressing insufficient supervisor approval in timekeeping procedures highlights critical internal control weaknesses. When managers fail to verify hours worked, it increases the risk of payroll errors, unauthorized overtime, and potential fraud. Proper oversight ensures labor costs align with actual productivity and legal compliance. Organizations must implement strict verification protocols to maintain financial integrity and audit readiness. Strengthening these timekeeping controls is essential to prevent budgetary discrepancies and ensure that every hour billed is accurately reviewed and authorized by designated personnel.

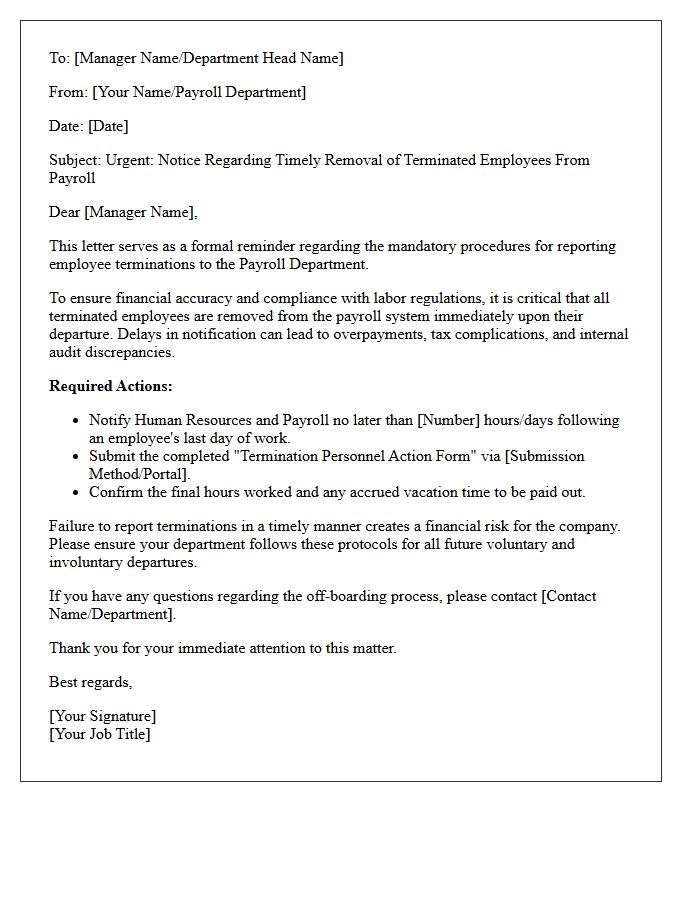

Management Letter Regarding the Timely Removal of Terminated Employees From Payroll

A management letter concerning the timely removal of terminated employees from payroll is a critical internal control document. It addresses the risk of ghost employees and unauthorized salary payments after a staff member leaves. Organizations must synchronize Human Resources data with payroll systems to prevent financial leakage and ensure regulatory compliance. Delays in deactivation can lead to significant budgetary losses and audit findings. Implementing automated workflows and immediate notification protocols is essential to maintain accurate financial records and uphold the integrity of the organization's payroll management processes.

Management Letter Identifying Paid Time Off Accrual and Processing Vulnerabilities

A management letter addressing Paid Time Off (PTO) accruals identifies critical weaknesses in financial reporting and internal control systems. These vulnerabilities often stem from manual processing errors, outdated tracking software, or a lack of secondary oversight. Failing to accurately calculate and record these liabilities can lead to significant budget variances and compliance risks. Organizations must implement automated reconciliation processes and strictly enforce segregation of duties to mitigate fraud and ensure that all employee leave balances reflect actual obligations within the annual financial statements.

What are the primary objectives of a management letter regarding payroll and timekeeping vulnerabilities?

The primary objectives are to identify internal control weaknesses, assess the risk of financial misstatement or fraud, and provide actionable recommendations to strengthen the integrity of payroll processing and timekeeping systems.

What common internal control weaknesses are identified in payroll processing audits?

Common weaknesses include a lack of segregation of duties between HR and payroll functions, inadequate review of payroll registers prior to disbursement, and the absence of formal procedures for deactivating terminated employees in the system.

How do timekeeping vulnerabilities contribute to payroll fraud?

Vulnerabilities such as manual override capabilities, lack of supervisor approval for overtime, and "buddy punching" allow for unauthorized hours to be recorded, leading to inflated wage payments and increased labor costs.

What recommendations are typically provided to mitigate payroll processing risks?

Key recommendations include implementing automated time-tracking systems with biometric verification, enforcing mandatory periodic audits of the employee master file, and requiring dual authorization for all payroll configuration changes.

Why is segregation of duties critical in a payroll management framework?

Segregation of duties ensures that no single individual has control over all phases of a transaction, preventing a single person from creating a fictitious employee, entering hours, and authorizing the subsequent payment.

Comments