A FASB ASC 740 Tax Opinion Letter provides essential professional substantiation for uncertain tax positions. It evaluates whether a tax benefit is more-likely-than-not to be sustained upon examination, ensuring corporate financial statements remain compliant with GAAP standards. This documentation mitigates risk and supports audit readiness. To simplify your documentation process, below are some ready to use template.

Image cover: FASB ASC 740: Professional Tax Opinion Letter Samples and Reporting Templates

Letter Samples List

- FASB ASC 740 Income Tax Provision Opinion Letter

- Uncertain Tax Position Assessment Opinion Letter

- Deferred Tax Asset Valuation Allowance Opinion Letter

- Management Representation Letter for Income Tax Accounting

- Unrecognized Tax Benefit Recognition Opinion Letter

- Interim Period Tax Provision Review Letter

- Business Combination Tax Allocation Opinion Letter

- Foreign Subsidiary Earnings Repatriation Tax Letter

- Effective Tax Rate Reconciliation Opinion Letter

- Intraperiod Tax Allocation Assessment Letter

- Internal Control Over Tax Provision Assessment Letter

- Enacted Tax Law Change Impact Opinion Letter

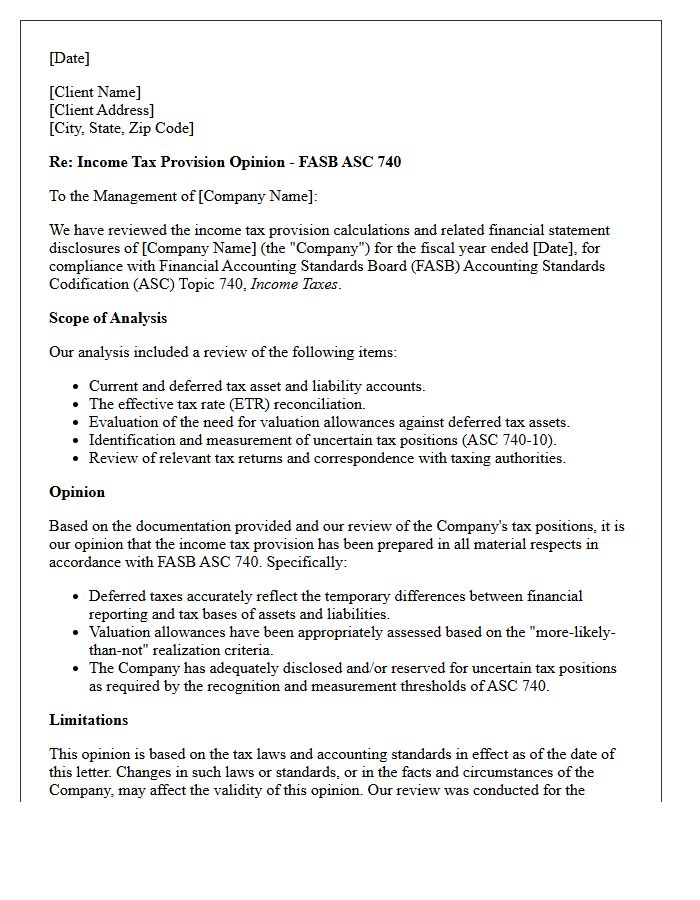

FASB ASC 740 Income Tax Provision Opinion Letter

A FASB ASC 740 Opinion Letter provides an independent expert assessment regarding a company's accounting for income taxes. It evaluates the accuracy of deferred tax assets, liabilities, and the effectiveness of internal controls over financial reporting. This document is essential for auditors to gain comfort over complex tax positions and uncertain tax benefits. By documenting technical compliance with GAAP, the letter mitigates risk, ensures financial statement integrity, and supports the valuation allowance assertions necessary for transparent corporate disclosure during annual audits.

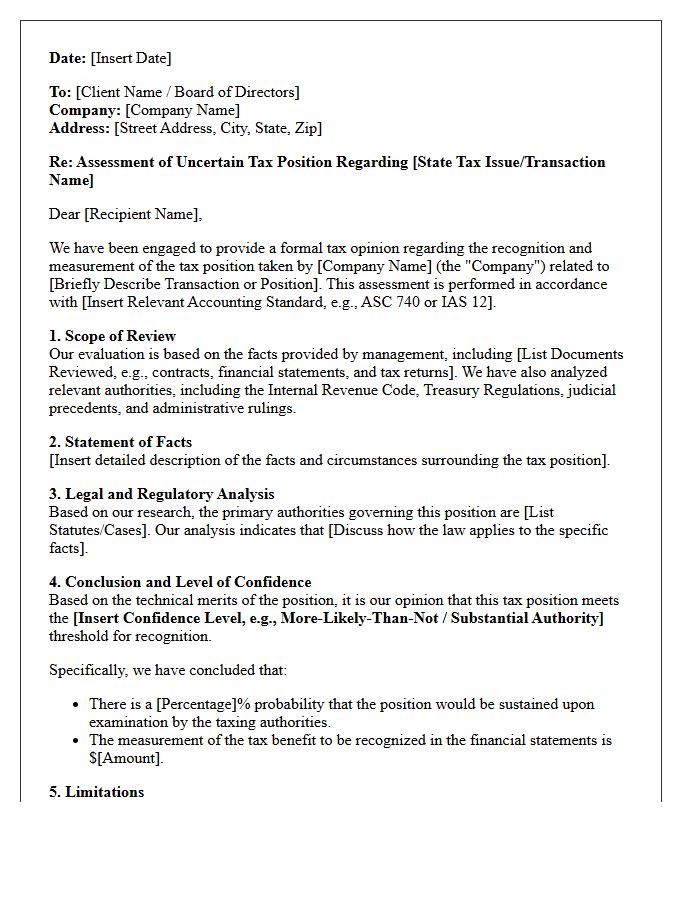

Uncertain Tax Position Assessment Opinion Letter

An Uncertain Tax Position Assessment Opinion Letter provides a legal or professional evaluation of a taxpayer's exposure regarding ambiguous tax treatments. This document is crucial for financial reporting and compliance with accounting standards like ASC 740. It assesses whether a position meets the "more-likely-than-not" threshold for recognition. By identifying potential tax liabilities and offering technical justification, the letter helps corporations mitigate risks, manage reserves, and provide transparency to auditors or tax authorities during audits. It serves as a vital defense tool in documenting professional due diligence and mitigating penalties.

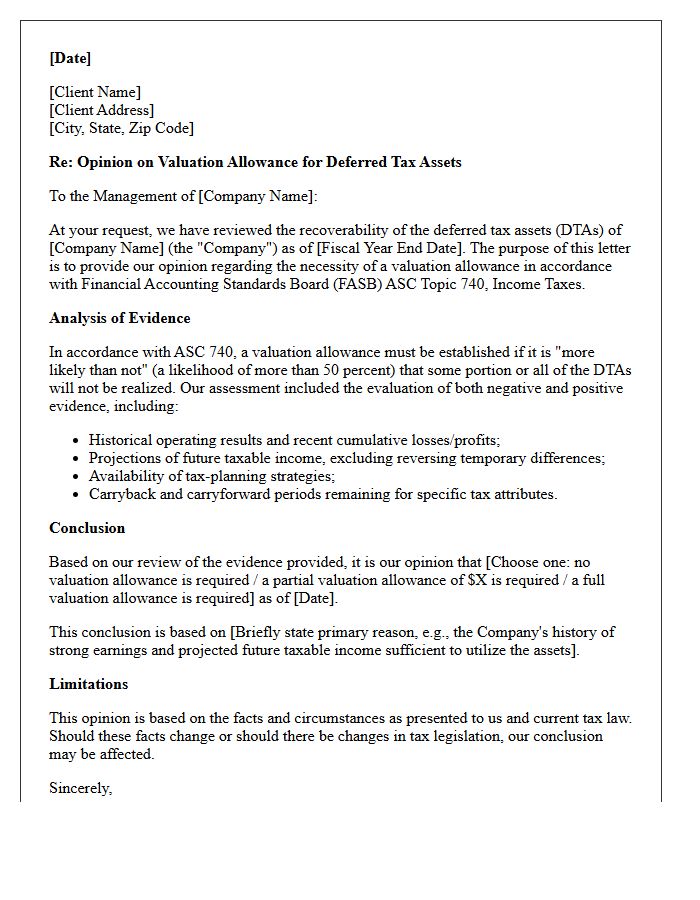

Deferred Tax Asset Valuation Allowance Opinion Letter

A Deferred Tax Asset Valuation Allowance Opinion Letter is a formal assessment by tax professionals regarding the realizability of tax benefits. It evaluates whether a company will generate sufficient future taxable income to utilize its deferred tax assets. Under accounting standards like ASC 740, a valuation allowance is required if it is "more likely than not" that some portion of the assets will not be realized. This letter provides critical documentation for auditors, justifying the management's judgment on valuation allowances and ensuring financial statement accuracy and tax compliance.

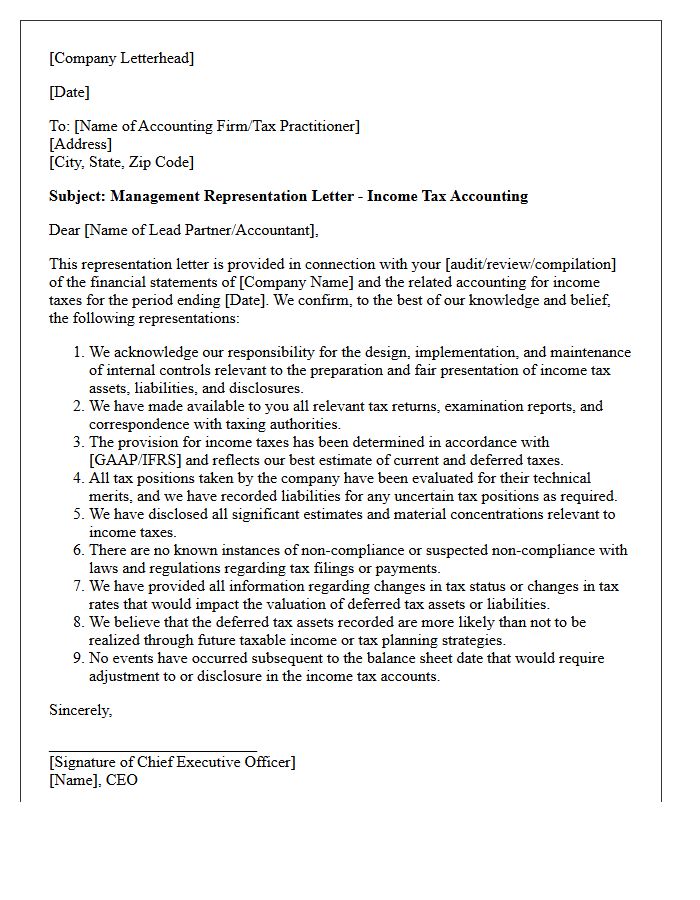

Management Representation Letter for Income Tax Accounting

A Management Representation Letter for income tax accounting is a formal document provided by company executives to external auditors. It confirms the accuracy and completeness of financial information related to tax provisions and deferred tax assets. This letter serves as audit evidence, ensuring that management acknowledges its responsibility for reporting uncertain tax positions and complying with statutory laws. By signing, leadership validates that all tax contingencies have been disclosed, reducing the auditor's risk regarding material misstatements in the financial statements.

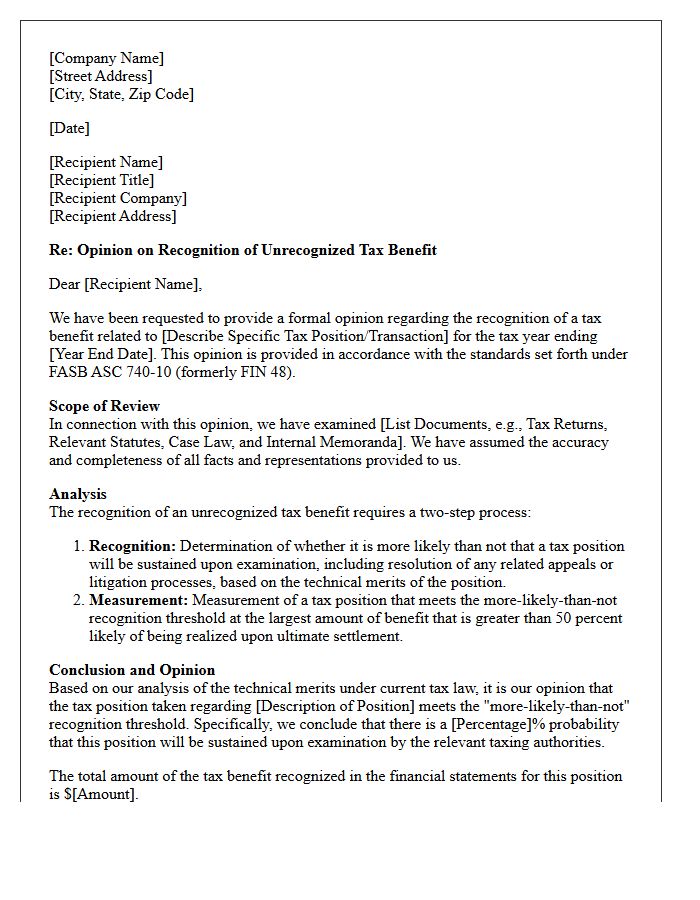

Unrecognized Tax Benefit Recognition Opinion Letter

An Unrecognized Tax Benefit Recognition Opinion Letter is a formal legal document assessing whether a tax position meets the "more-likely-than-not" threshold for financial reporting. Under standards like ASC 740, companies must evaluate uncertain tax positions to determine if benefits can be recognized in financial statements. The opinion provides a rigorous analysis of tax law and judicial precedents to support compliance and mitigate audit risk. It serves as essential documentation for auditors and regulators, ensuring that potential tax liabilities are accurately disclosed and adequately reserved against future challenges by authorities.

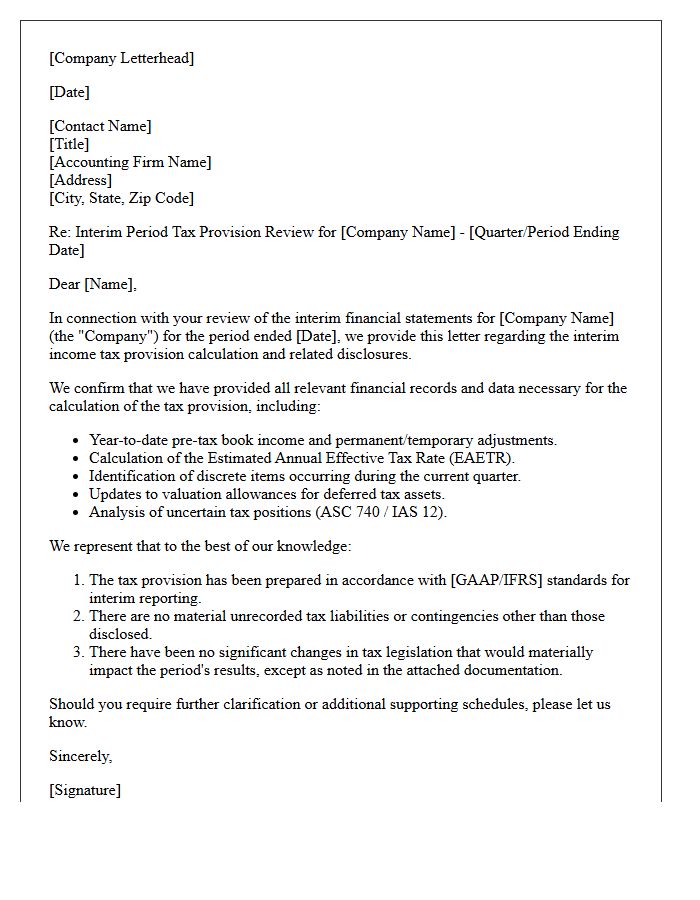

Interim Period Tax Provision Review Letter

An Interim Period Tax Provision Review Letter is a formal document issued by independent auditors after evaluating a company's quarterly tax estimations. This review ensures that the effective tax rate and deferred tax assets comply with accounting standards like ASC 740 or IAS 12. It provides stakeholders with assurance that interim financial statements accurately reflect current tax liabilities and potential risks. Understanding this letter is essential for maintaining regulatory compliance and financial transparency during mid-year reporting cycles before the final annual audit occurs.

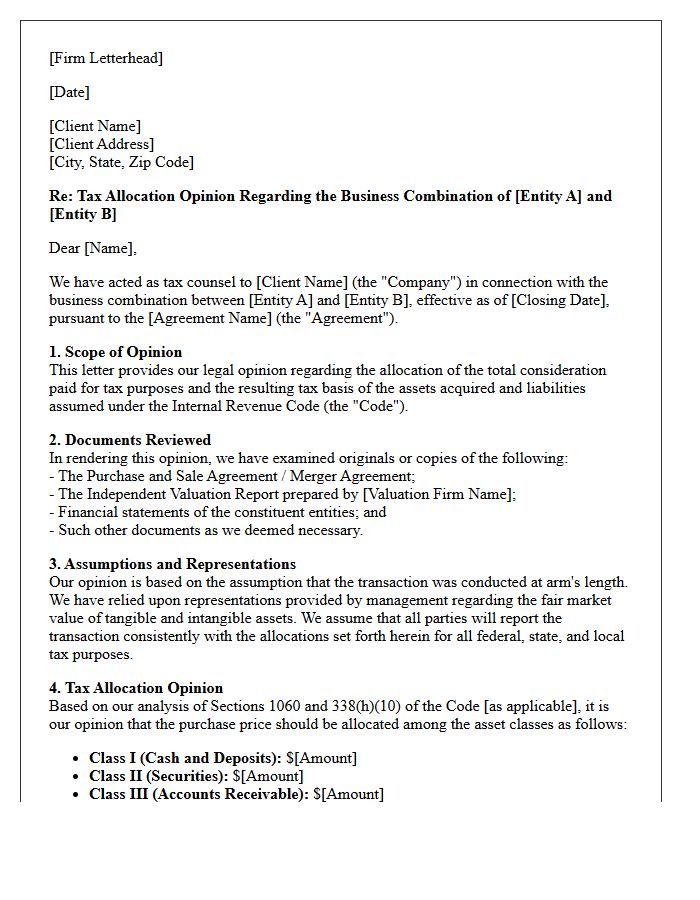

Business Combination Tax Allocation Opinion Letter

A Business Combination Tax Allocation Opinion Letter is a critical legal document used to validate the tax-free status of corporate reorganizations. It provides a formal legal basis for allocating purchase price components and determining tax liabilities under IRS guidelines. This opinion protects stakeholders by confirming that the transaction meets specific statutory requirements, such as continuity of interest. By securing this letter, companies mitigate risks associated with tax audits and ensure accurate financial reporting during mergers or acquisitions. It is an essential safeguard for ensuring regulatory compliance and optimizing the structural integrity of the deal.

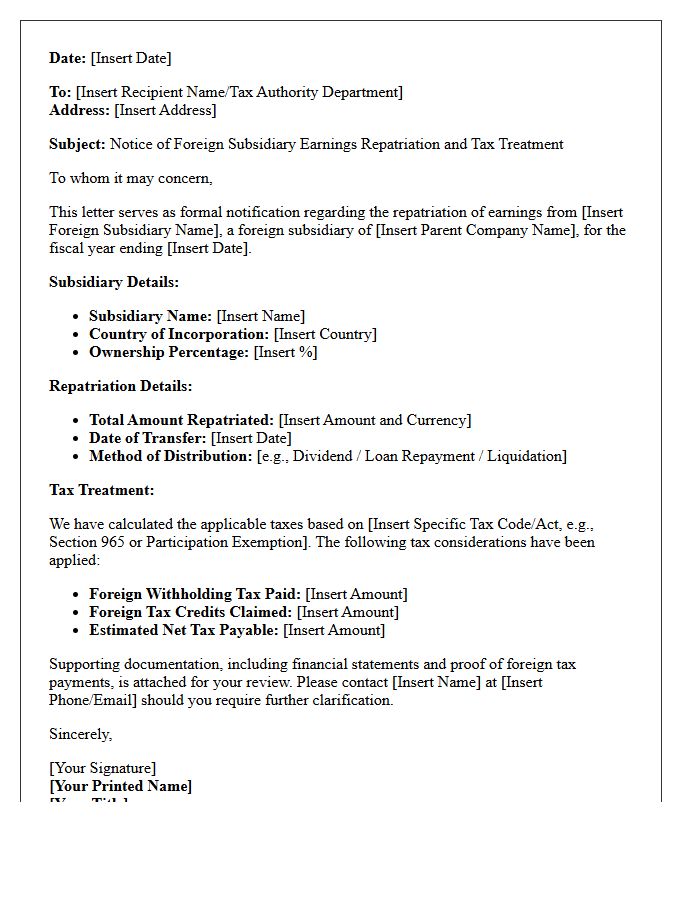

Foreign Subsidiary Earnings Repatriation Tax Letter

A Foreign Subsidiary Earnings Repatriation Tax Letter notifies shareholders about the mandatory transition tax on previously untaxed foreign profits. Under Section 965, the IRS requires U.S. taxpayers to pay a one-time levy on accumulated overseas earnings, regardless of whether the cash is physically brought home. This document details your specific tax liability, applicable discounted rates, and available installment payment elections. Understanding this letter is crucial for ensuring compliance with international tax reform and avoiding significant penalties related to offshore corporate holdings.

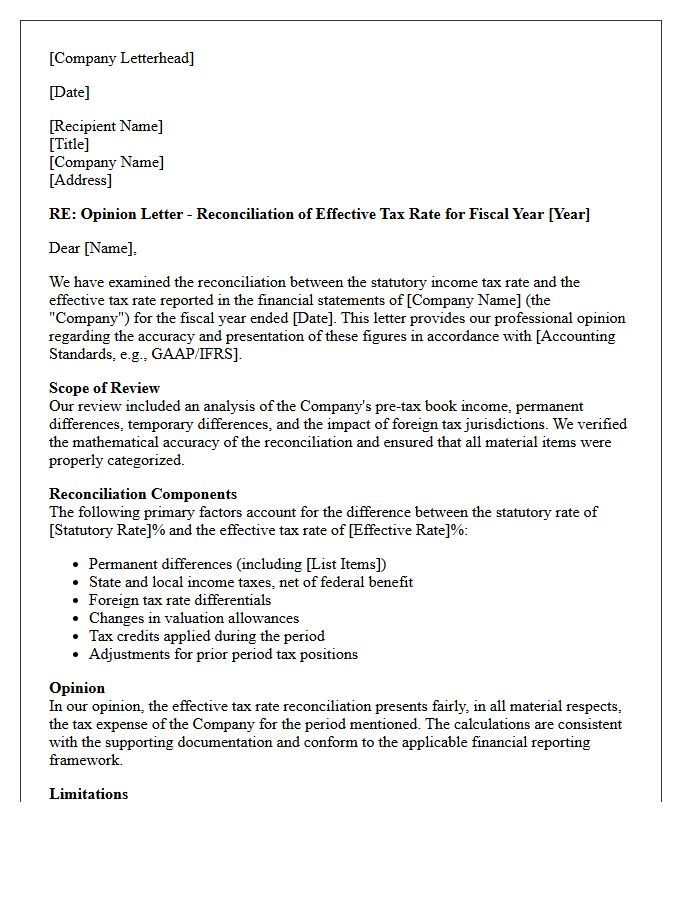

Effective Tax Rate Reconciliation Opinion Letter

An Effective Tax Rate Reconciliation Opinion Letter is a critical document used to validate the accuracy of a company's income tax provision. It provides a formal analysis explaining the difference between the statutory rate and the Effective Tax Rate. This letter ensures compliance with accounting standards like ASC 740 or IAS 12, offering audit-ready documentation for tax disclosures. It serves as essential evidence for stakeholders, confirming that all permanent and temporary adjustments are properly calculated, thereby mitigating risks of financial restatement and enhancing corporate transparency during external audits.

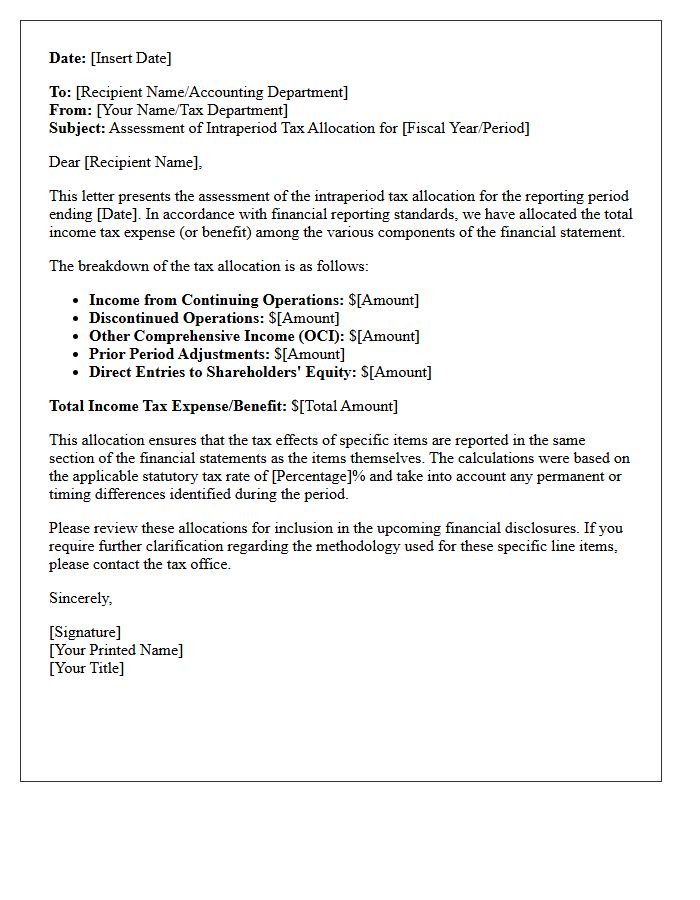

Intraperiod Tax Allocation Assessment Letter

An Intraperiod Tax Allocation Assessment Letter is a formal document used to communicate how income tax expense is distributed among different components of a financial statement. This process ensures that taxes associated with continuing operations, discontinued operations, and other comprehensive income are reported accurately within the same accounting period. It enhances transparency by matching taxes directly to the items that generated them, allowing stakeholders to assess a company's true operational performance. Understanding this letter is essential for verifying compliance with accounting standards and ensuring precise financial reporting of net income.

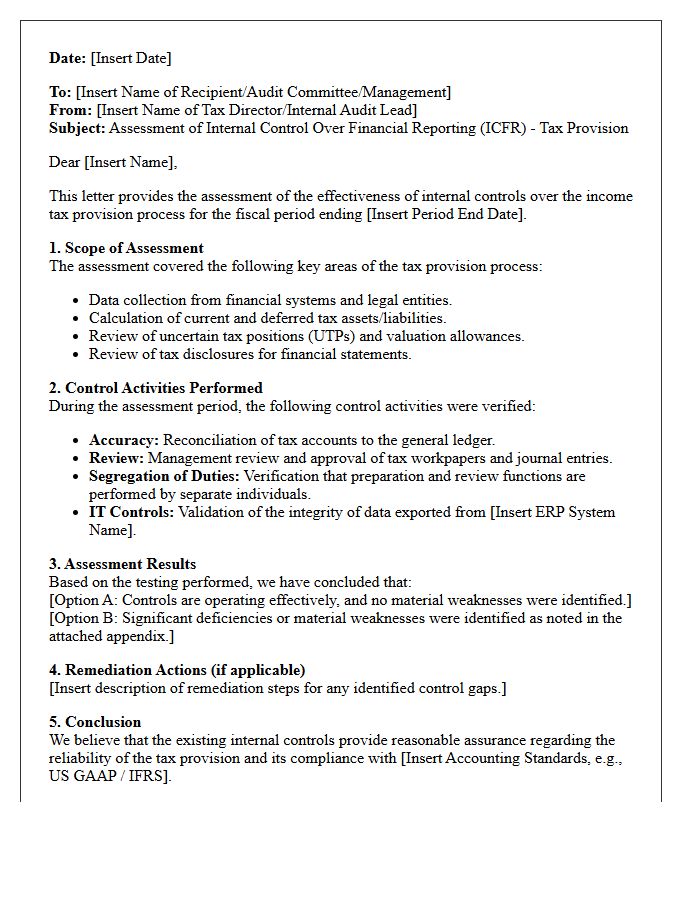

Internal Control Over Tax Provision Assessment Letter

An Internal Control Over Tax Provision Assessment Letter is a formal document validating the accuracy of a company's income tax calculations. It confirms that internal controls are effectively designed to prevent material misstatements in financial reporting. This assessment ensures compliance with accounting standards like ASC 740 or IAS 12. Auditors use this letter to evaluate risk management protocols regarding tax accounting. Understanding this document is essential for maintaining transparency, ensuring regulatory compliance, and securing stakeholder trust in the integrity of a corporation's disclosed tax liabilities and deferred tax assets.

Enacted Tax Law Change Impact Opinion Letter

An Enacted Tax Law Change Impact Opinion Letter provides a formal legal assessment regarding how new legislation affects specific financial structures. This document is crucial for mitigating tax risks and ensuring compliance during regulatory transitions. It serves as a professional risk management tool, offering legal protection for taxpayers and corporations by documenting a reasonable basis for tax positions. Stakeholders rely on these letters to understand liability shifts and to make informed decisions before tax deadlines, ensuring that all reporting aligns with the most current statutory requirements and judicial interpretations.

What is an ASC 740 tax opinion letter?

An ASC 740 tax opinion letter is a formal document provided by tax professionals that evaluates the "more-likely-than-not" probability of a company's tax positions being sustained upon examination. This letter serves as critical evidentiary documentation for auditors to validate tax reserves and unrecognized tax benefits (UTBs) presented in financial statements.

When is a formal tax opinion required under FASB ASC 740?

A formal tax opinion is typically required when a tax position involves significant technical uncertainty or complexity, such as cross-border transactions, R&D credits, or complex mergers and acquisitions. It provides the necessary legal and technical justification to meet the recognition threshold required by U.S. GAAP for uncertain tax positions.

How does an ASC 740 opinion letter support the "More-Likely-Than-Not" standard?

The letter provides a detailed legal analysis of tax authorities, judicial precedents, and legislative intent to conclude that there is a greater than 50% probability the position will be upheld. This objective analysis allows management to recognize the tax benefit in their financial reporting without establishing a valuation allowance or tax reserve for that specific position.

What are the essential components of an ASC 740 tax opinion?

An effective ASC 740 opinion letter must include a comprehensive statement of facts, an analysis of relevant Internal Revenue Code (IRC) sections, Treasury Regulations, and applicable case law. It must specifically address the technical merits of the position and provide a definitive conclusion regarding the likelihood of success based on the "unit of account" being measured.

Can auditors rely solely on an ASC 740 tax opinion letter for financial statement sign-off?

While an ASC 740 tax opinion is a primary piece of evidence, auditors must still perform independent due diligence to verify the underlying facts and the reasonableness of the legal conclusions. The opinion serves as the basis for the company's assertion, but the auditor must ensure the documentation sufficiently mitigates the risk of material misstatement in the income tax provision.

Comments