A Transfer Pricing Opinion Letter provides a professional legal or tax justification for intercompany pricing strategies. It ensures compliance with arm's length principles, mitigating the risk of audits and costly penalties from tax authorities. This document serves as critical evidence for corporate transparency and international tax alignment. To streamline your documentation process, below are some ready to use template.

Image cover: Comprehensive Guide to Transfer Pricing Opinion Letter Samples and Templates

Letter Samples List

- Transfer Pricing Penalty Protection Opinion Letter

- Arm's Length Standard Affirmation Letter

- Intercompany Transaction Valuation Opinion Letter

- Advance Pricing Agreement Consultation Letter

- Cost Sharing Arrangement Opinion Letter

- Intangible Property Transfer Pricing Letter

- Intercompany Financing Safe Harbor Letter

- Management Fee Allocation Opinion Letter

- Transfer Pricing Audit Defense Letter

- Country-By-Country Reporting Compliance Letter

- Tangible Goods Pricing Opinion Letter

- Transfer Pricing Documentation Engagement Letter

- Benchmarking Study Conclusion Letter

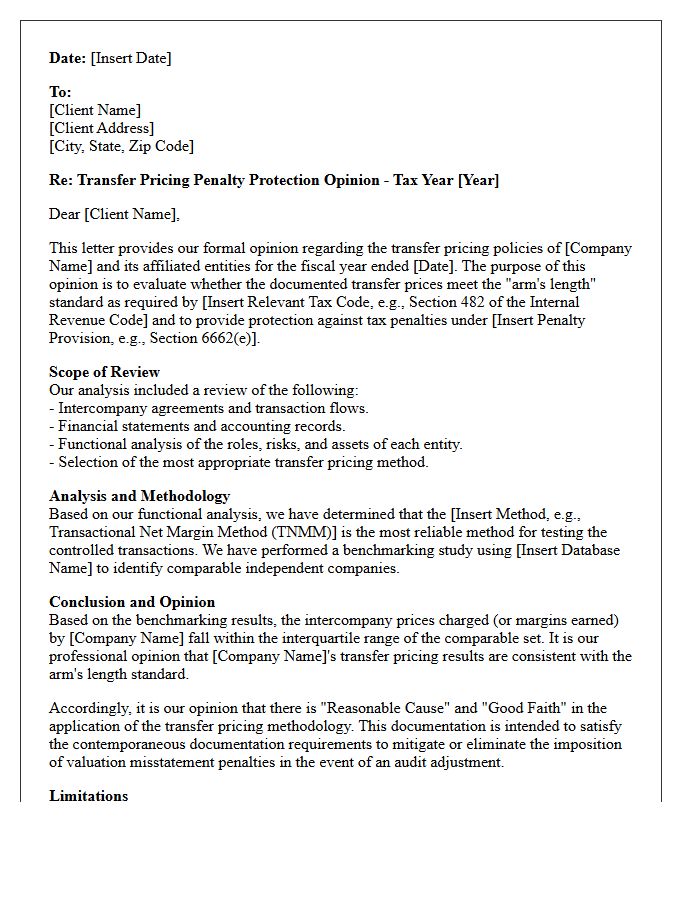

Transfer Pricing Penalty Protection Opinion Letter

A Transfer Pricing Penalty Protection Opinion Letter provides a legal defense against substantial IRS penalties under Section 6662. By documenting that a company's intercompany pricing aligns with the arm's length principle, this formal report demonstrates reasonable cause and good faith. It is a critical risk management tool that justifies specific transfer pricing methodologies used in cross-border transactions. Having this contemporaneous documentation in place ensures that even if an audit results in a tax adjustment, the taxpayer can avoid costly accuracy-related penalties that typically range from 20% to 40% of the underpayment.

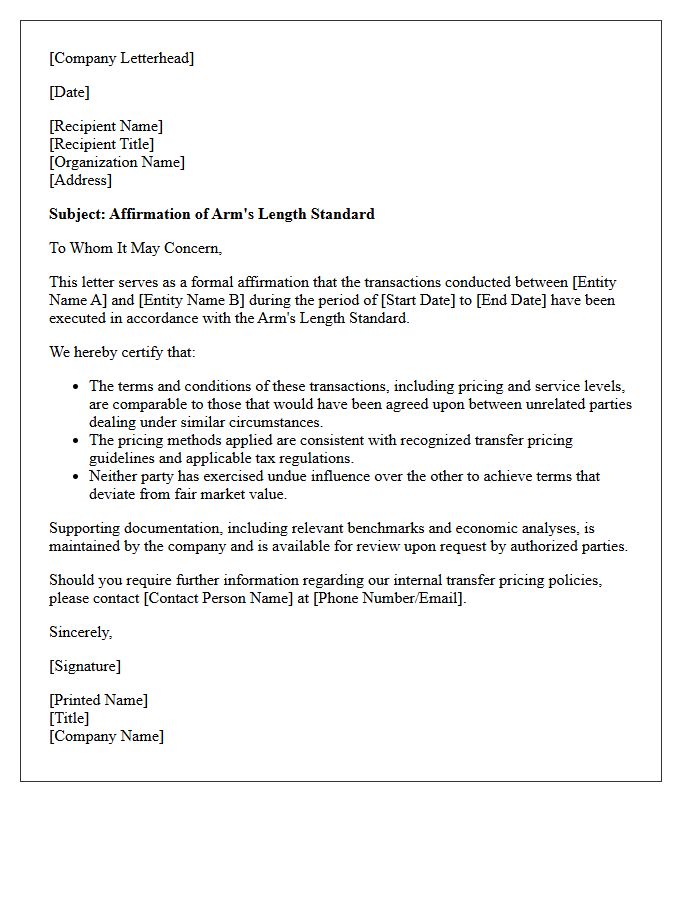

Arm's Length Standard Affirmation Letter

An Arm's Length Standard Affirmation Letter is a formal document used in transfer pricing to confirm that transactions between related entities reflect fair market conditions. This statement affirms that controlled dealings align with prices independent parties would agree upon under similar circumstances. Tax authorities, such as the IRS, require this affirmation to prevent profit shifting and ensure tax compliance. By signing this letter, a company validates its commitment to OECD guidelines, providing essential regulatory documentation that mitigates the risk of audits, penalties, and tax adjustments during financial reviews.

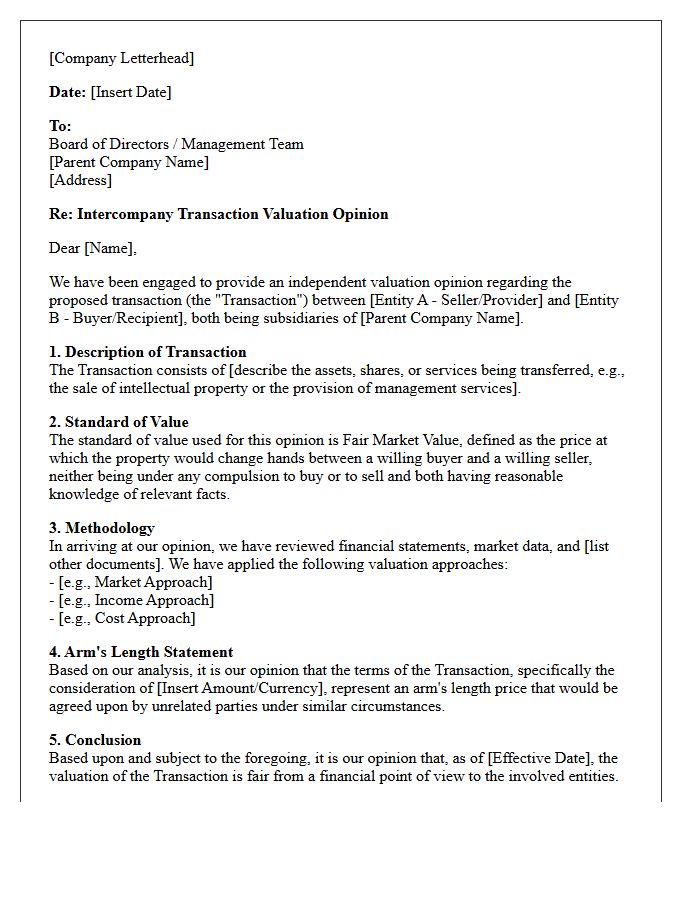

Intercompany Transaction Valuation Opinion Letter

An Intercompany Transaction Valuation Opinion Letter provides a formal, independent assessment to ensure asset transfers or services between related entities align with the arm's length principle. This document is essential for tax compliance and financial reporting, defending the transaction against regulatory scrutiny by tax authorities like the IRS. By establishing a fair market value, the letter mitigates risks of penalties, double taxation, and transfer pricing disputes. It serves as critical evidentiary support that proves internal dealings mirror open-market conditions, protecting the corporate group's financial integrity and legal standing.

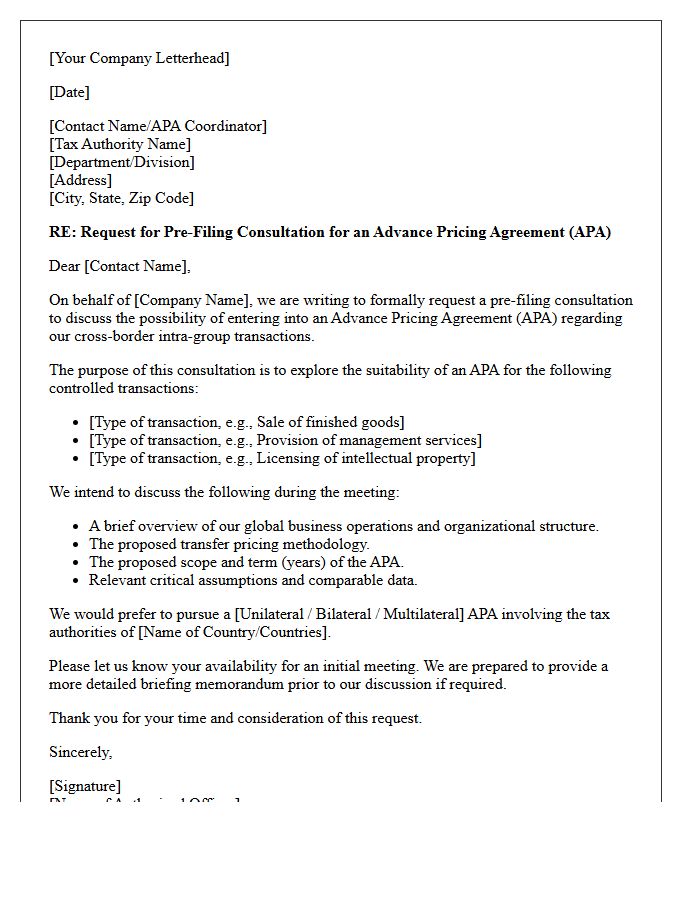

Advance Pricing Agreement Consultation Letter

An Advance Pricing Agreement (APA) Consultation Letter serves as the formal initiation for taxpayers to discuss intercompany pricing strategies with tax authorities. This document outlines the proposed transfer pricing methodology to prevent future double taxation and minimize audit risks. It provides a structured framework for transparency between multinational enterprises and governments, ensuring legal certainty over international transactions. By submitting this letter, companies seek a unilateral, bilateral, or multilateral agreement to secure pre-approved tax treatments, ultimately fostering a predictable compliance environment for complex global operations and cross-border trade.

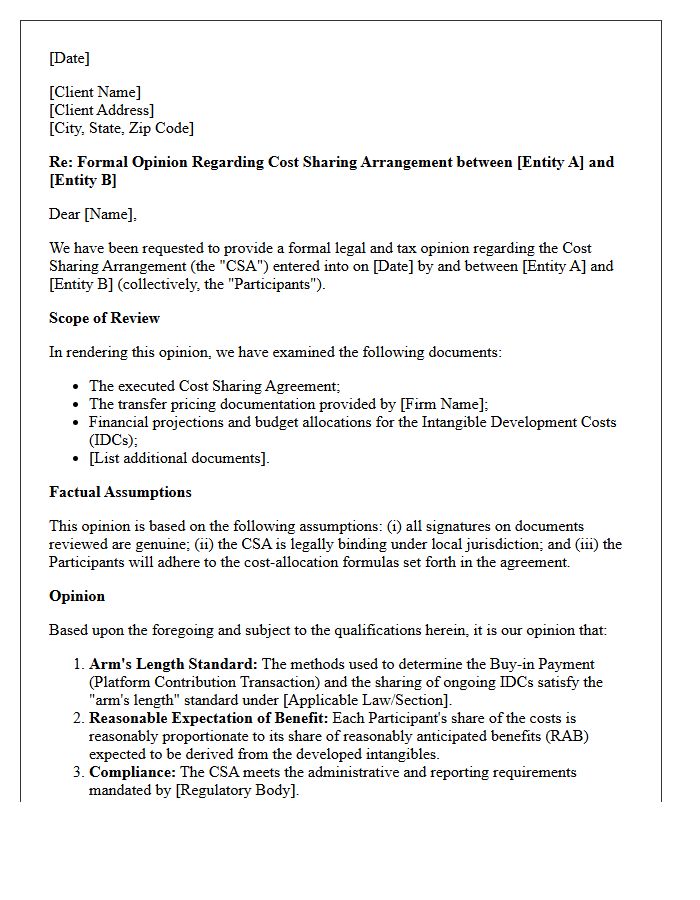

Cost Sharing Arrangement Opinion Letter

A Cost Sharing Arrangement (CSA) Opinion Letter provides a formal legal and tax validation of how entities distribute costs for developing intangible property. This document is essential for transfer pricing compliance, ensuring that participants share R&D expenses in proportion to their anticipated benefits. By obtaining this letter, multinational companies mitigate the risk of IRS adjustments and penalties. It serves as critical evidence that the arm's length principle was applied correctly, offering a robust defense for the cost-allocation methodology used within the corporate group to satisfy international tax regulations.

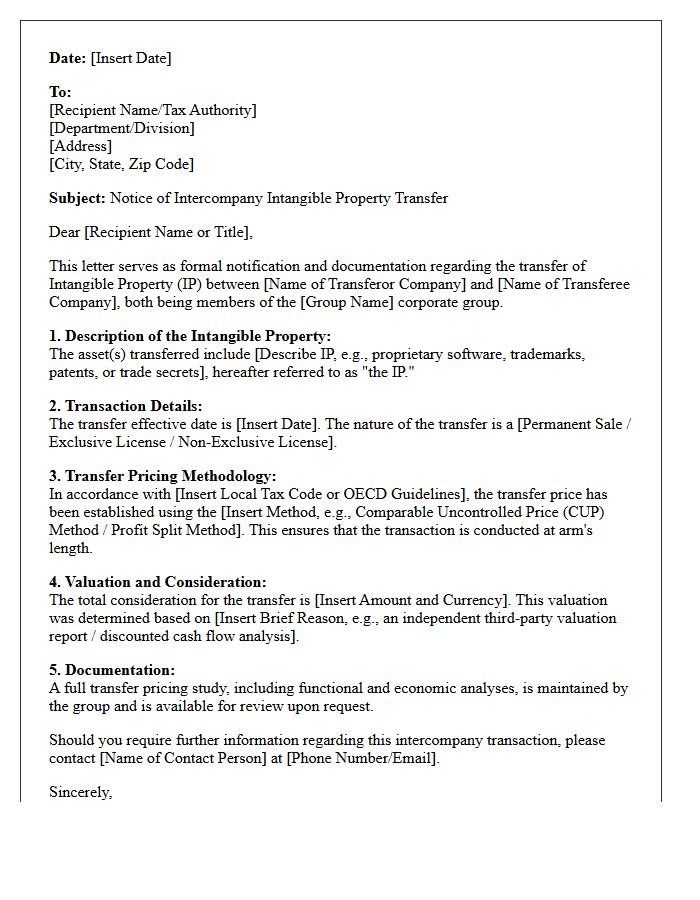

Intangible Property Transfer Pricing Letter

An Intangible Property Transfer Pricing Letter is a formal document justifying the arm's length price for intercompany transfers of non-physical assets. This letter ensures compliance with tax regulations by outlining the economic valuation of assets like intellectual property, patents, and trademarks. It serves as critical documentation for tax authorities to prevent profit shifting. By detailing the functions, assets, and risks associated with the transfer, companies mitigate audit risks and support their global tax strategy while adhering to OECD guidelines for cross-border transactions.

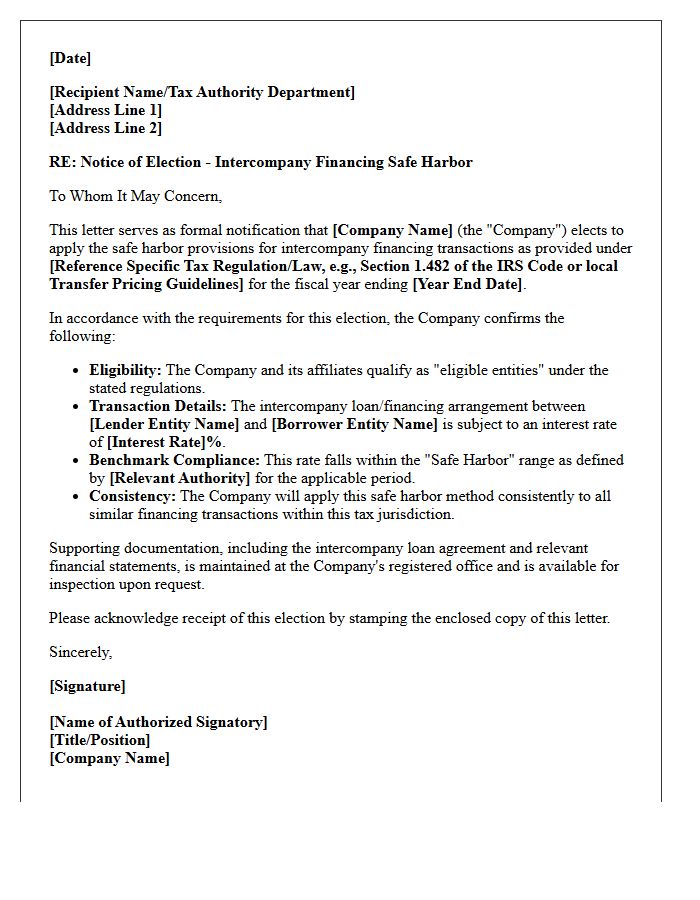

Intercompany Financing Safe Harbor Letter

An Intercompany Financing Safe Harbor Letter provides crucial legal protection for corporate groups. It formally documents that internal loans meet specific regulatory requirements, ensuring they are treated as debt rather than equity for tax purposes. By establishing arm's length interest rates and repayment terms, companies mitigate the risk of audits and double taxation. Obtaining this letter is an essential compliance measure that offers certainty during financial reporting and demonstrates transparency to tax authorities regarding cross-border or domestic fund transfers between related entities.

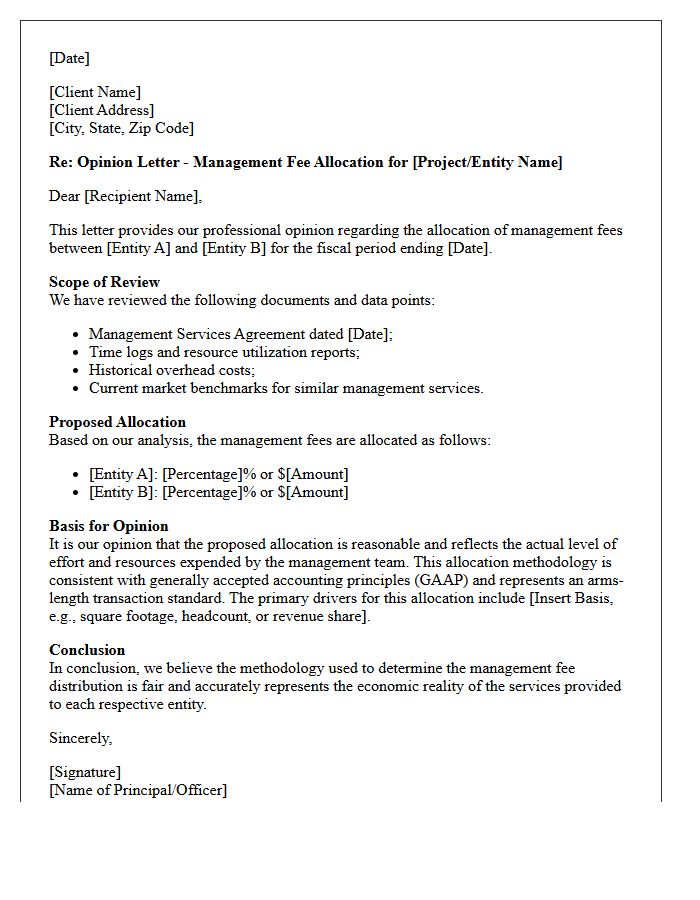

Management Fee Allocation Opinion Letter

A Management Fee Allocation Opinion Letter is a critical document used to ensure equitable distribution of shared costs within complex corporate structures. It provides an independent professional assessment to verify that fees charged between entities align with fair market value and regulatory standards. This letter mitigates conflict of interest risks among stakeholders and helps prevent tax challenges by justifying the underlying economic rationale. By documenting the methodology used for cost allocation, companies demonstrate transparency and fiduciary responsibility, protecting directors from potential litigation regarding financial mismanagement or unfair intercompany transactions.

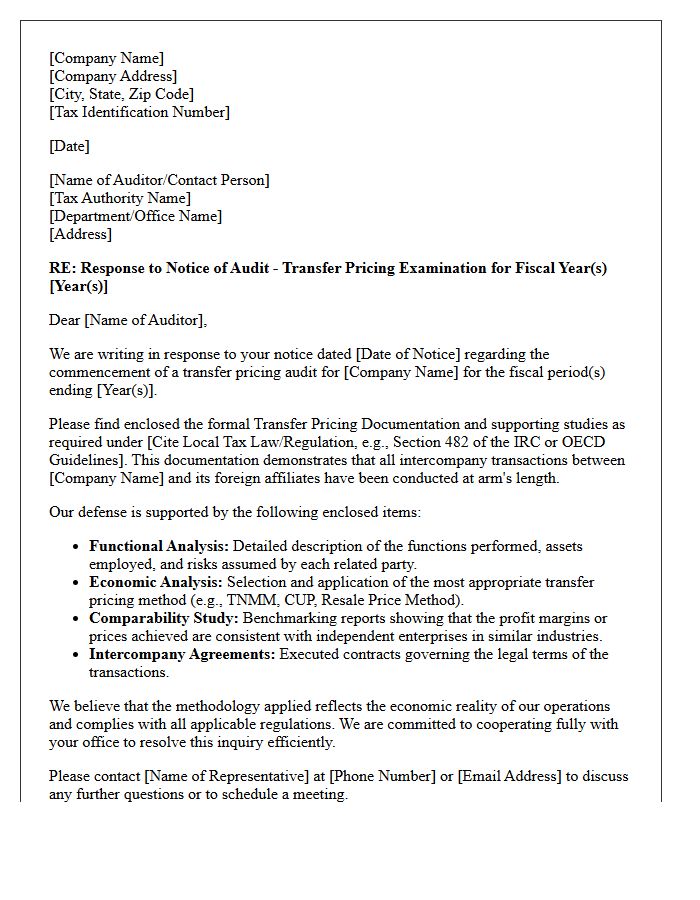

Transfer Pricing Audit Defense Letter

A Transfer Pricing Audit Defense Letter is a critical legal response justifying intercompany pricing strategies during tax authority inquiries. It serves as a formal justification to demonstrate that cross-border transactions comply with the arm's length principle. To be effective, the document must bridge gaps between contemporaneous documentation and specific auditor queries, providing economic analysis and functional profiles. A robust letter mitigates the risk of double taxation and significant penalties by clearly articulating the business rationale and methodology used to determine fair market value across global jurisdictions.

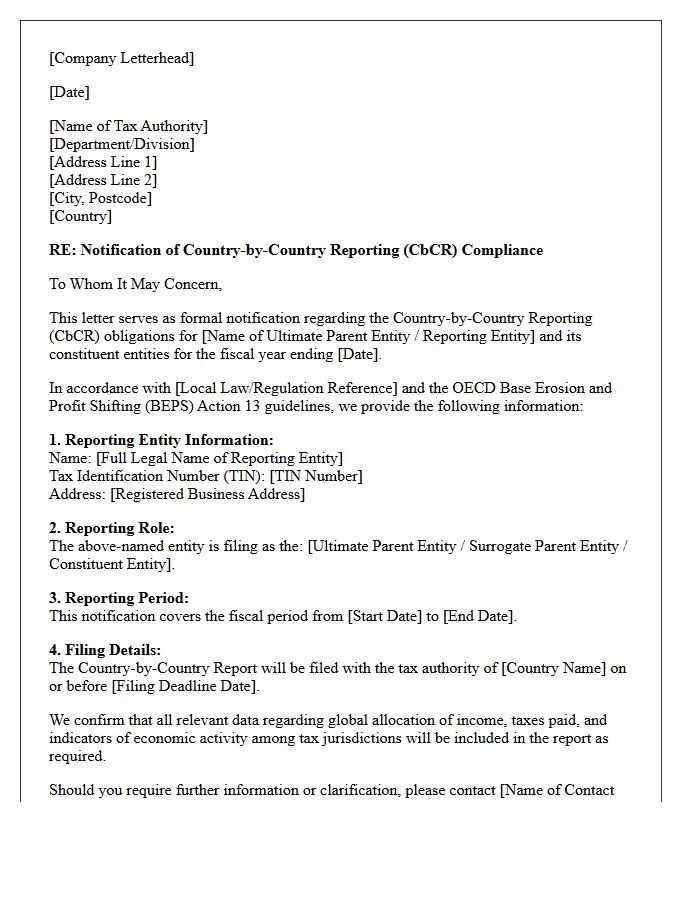

Country-By-Country Reporting Compliance Letter

A Country-By-Country Reporting Compliance Letter is a formal notification issued by tax authorities to multinational enterprises regarding their BEPS Action 13 obligations. It ensures companies accurately disclose global income, taxes paid, and economic activities across all jurisdictions. Receiving this letter indicates that a firm must verify its CbC report filings or clarify inconsistencies to avoid significant penalties. Compliance is essential for transparency and helps authorities assess transfer pricing risks effectively. Timely responses and precise data alignment are critical to maintaining regulatory standing and avoiding intensive audits by international tax offices.

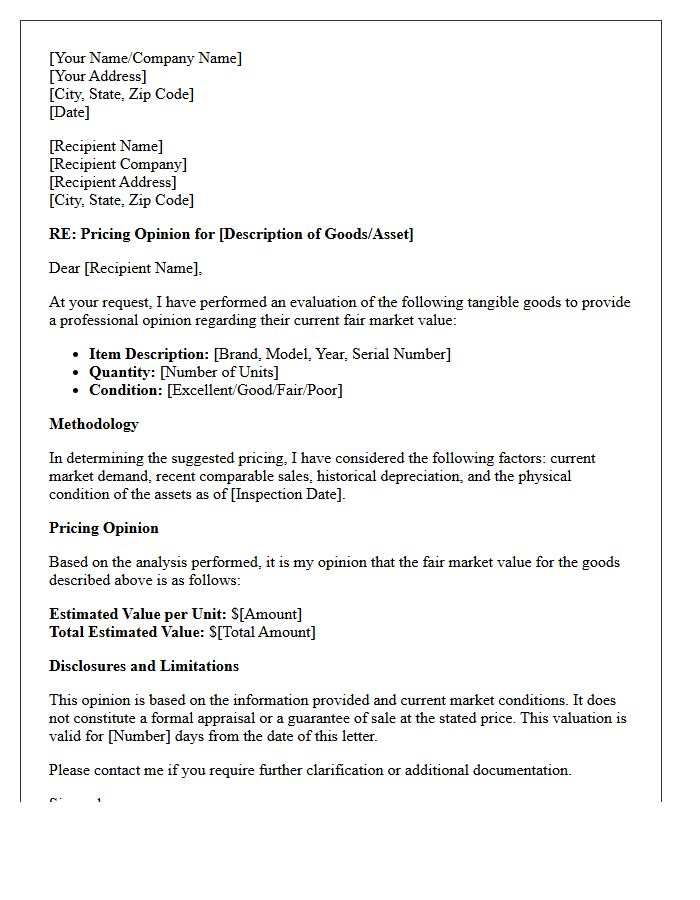

Tangible Goods Pricing Opinion Letter

A Tangible Goods Pricing Opinion Letter is a formal document used to establish the fair market value of physical assets for tax, insurance, or legal purposes. It provides an expert assessment of items like machinery or inventory, ensuring compliance with regulatory standards. This letter acts as critical evidence during audits or business liquidations, justifying specific valuations to authorities. By obtaining a professional opinion, stakeholders mitigate financial risks and ensure transparency in high-value transactions involving physical property.

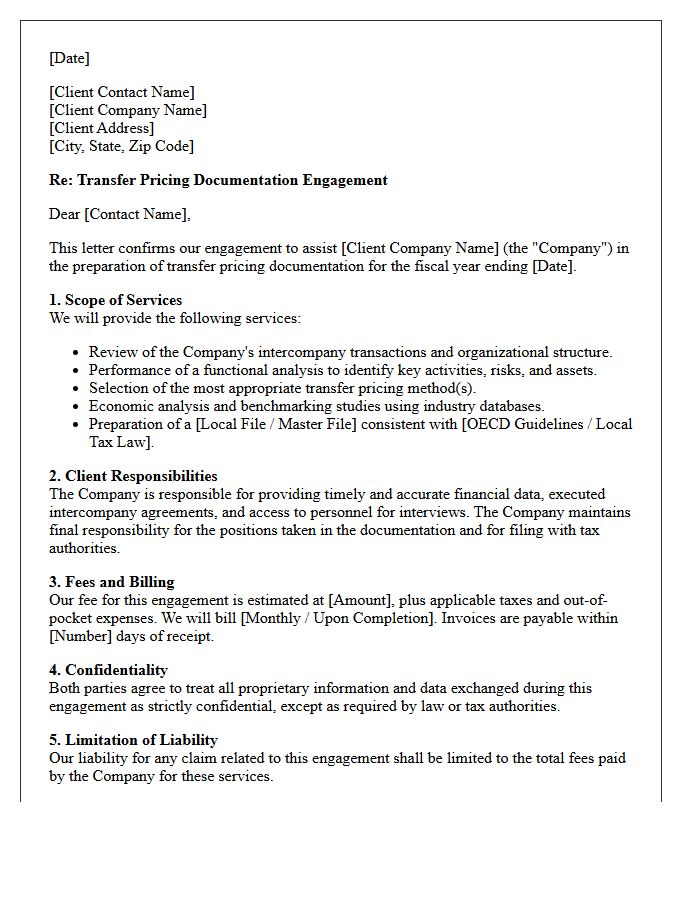

Transfer Pricing Documentation Engagement Letter

A Transfer Pricing Documentation Engagement Letter is a formal contract between a tax advisor and a taxpayer. It defines the specific scope of services, professional fees, and legal responsibilities involved in preparing compliance reports. This document is essential for mitigating tax risks and ensuring adherence to OECD guidelines or local regulations. By clearly outlining the timeline and data requirements, it protects both parties and establishes a defense against potential penalties during tax audits. Understanding the terms helps manage expectations regarding professional liability and jurisdictional reporting obligations.

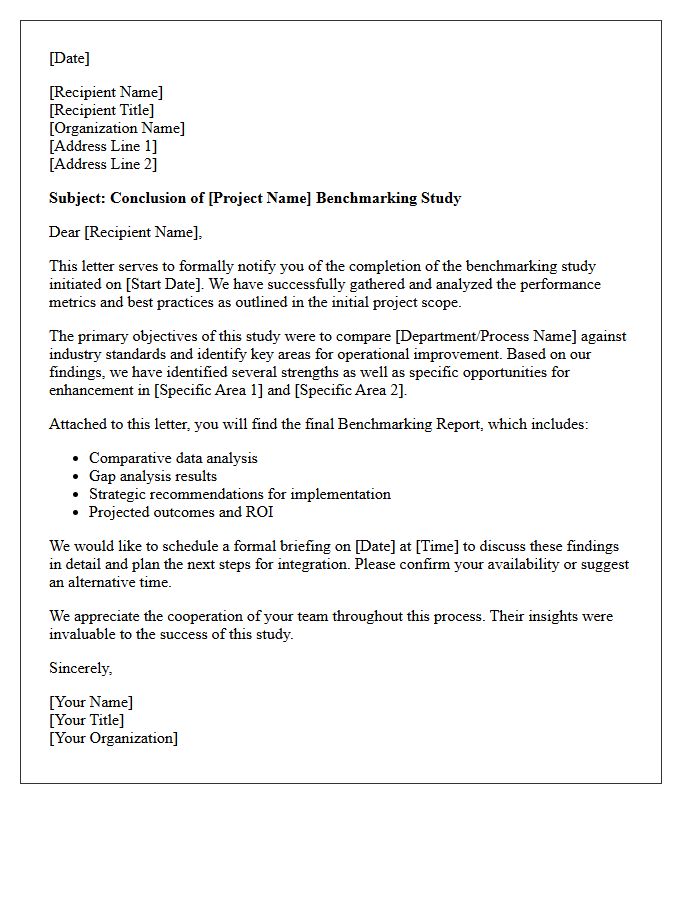

Benchmarking Study Conclusion Letter

A Benchmarking Study Conclusion Letter serves as formal verification that a company's intercompany pricing aligns with the arm's length principle. This document summarizes the economic analysis, database searches, and selection criteria used to establish market-based profitability ranges. It is a critical component of tax compliance documentation, providing a defensive shield during audits. By confirming that transfer pricing policies meet regulatory standards, the letter mitigates the risk of adjustments and penalties while ensuring global transparency for tax authorities and stakeholders.

What is a Transfer Pricing Opinion Letter?

A Transfer Pricing Opinion Letter is a formal document issued by tax professionals or economists that provides a legal and economic justification for the pricing of intercompany transactions. It confirms that the transactions are conducted at "arm's length" in compliance with Section 482 of the IRS code or OECD guidelines.

Why does a company need a Transfer Pricing Opinion Letter?

Companies require these letters to mitigate the risk of tax penalties, defend their tax positions during audits, and satisfy the requirements of FIN 48 (ASC 740-10) regarding uncertain tax positions. It serves as a critical component of a robust tax defense strategy for multinational enterprises.

What are the core components of a Transfer Pricing Opinion?

A standard opinion letter includes a functional analysis of the entities involved, a selection of the most appropriate transfer pricing method (such as TNMM or CUP), a benchmarking study of comparable companies, and a formal conclusion regarding the arm's length nature of the pricing.

How does an Opinion Letter differ from a Transfer Pricing Documentation report?

While documentation provides the comprehensive data and calculations required by tax authorities, an Opinion Letter provides a high-level professional conclusion and legal interpretation. The letter is often used to provide assurance to auditors, stakeholders, and board members regarding tax compliance and liability risks.

When should a Transfer Pricing Opinion Letter be updated?

An opinion letter should be updated annually or whenever there is a significant change in the business model, functions performed, risks assumed, or when new tax regulations are enacted. Regular updates ensure that the intercompany pricing remains defensible under current market conditions and legal standards.

Comments